OKE - ONEOK: Get Paid A 6% Yield And Beat The S&P 500

2023-11-24 04:46:33 ET

Summary

- Buying high-yielding blue chips with excellent fundamentals can produce attractive investment results over the long haul.

- ONEOK's recent operating results suggest that it is firing on all cylinders.

- The company's dividend is supported by a well-covered payout ratio and an investment-grade balance sheet.

- ONEOK is currently trading just below fair value.

- The midstream could narrowly beat the S&P 500 in the next two years and almost 2X it over the coming 10 years.

Oftentimes, when you think of a high-yield, yield trap comes to mind. This is to say that high yields often come about because a company's valuation is so beaten down that the yield is artificially high. That implies that the risk of a dividend cut is elevated.

But now and then, there are exceptions to this rule. Because midstream companies tend to heavily emphasize returning cash to shareholders, this industry overall is an exception. ONEOK ( OKE ) is a great example of why I like high-yielding, high-quality businesses.

{kind=link}

{kind=link}

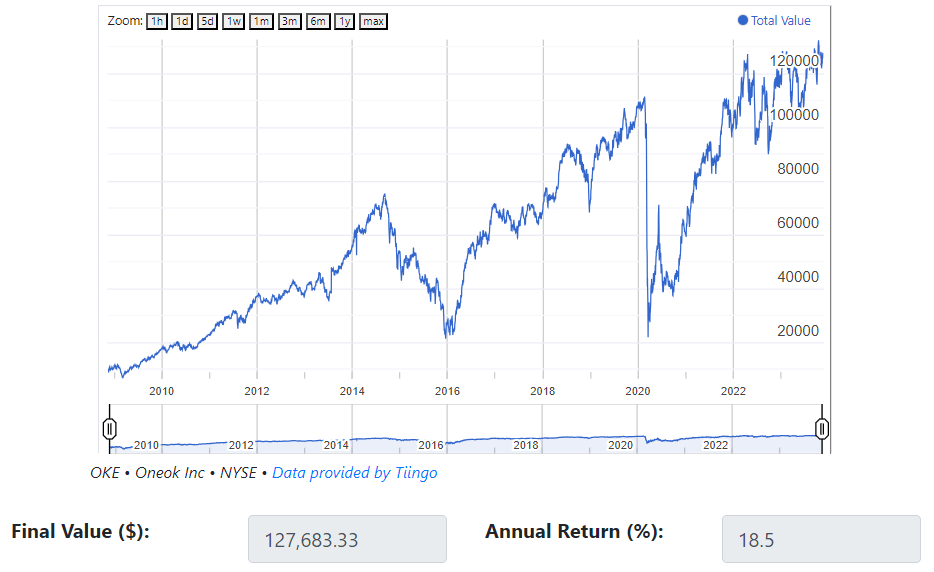

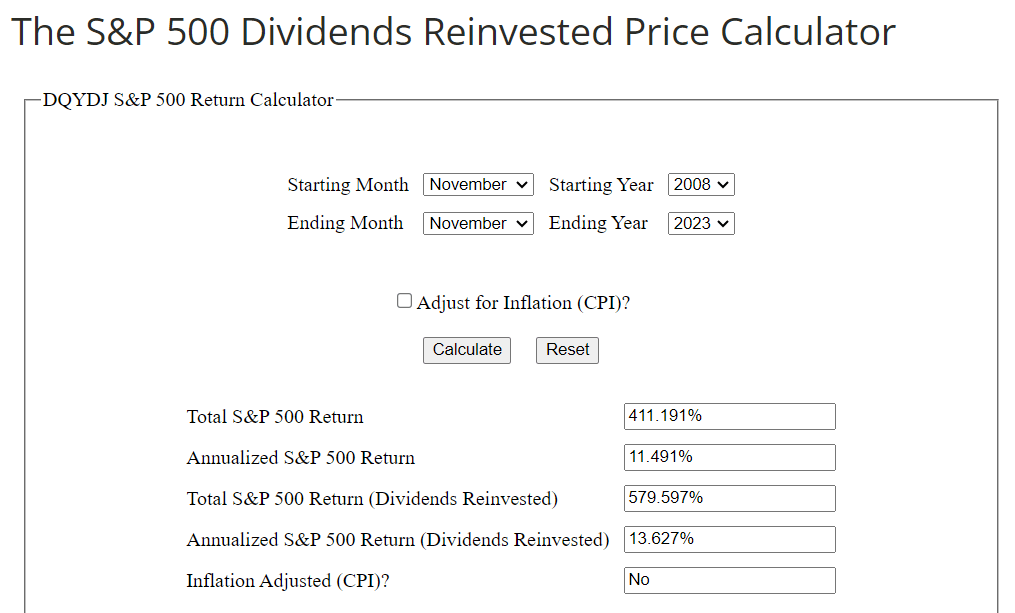

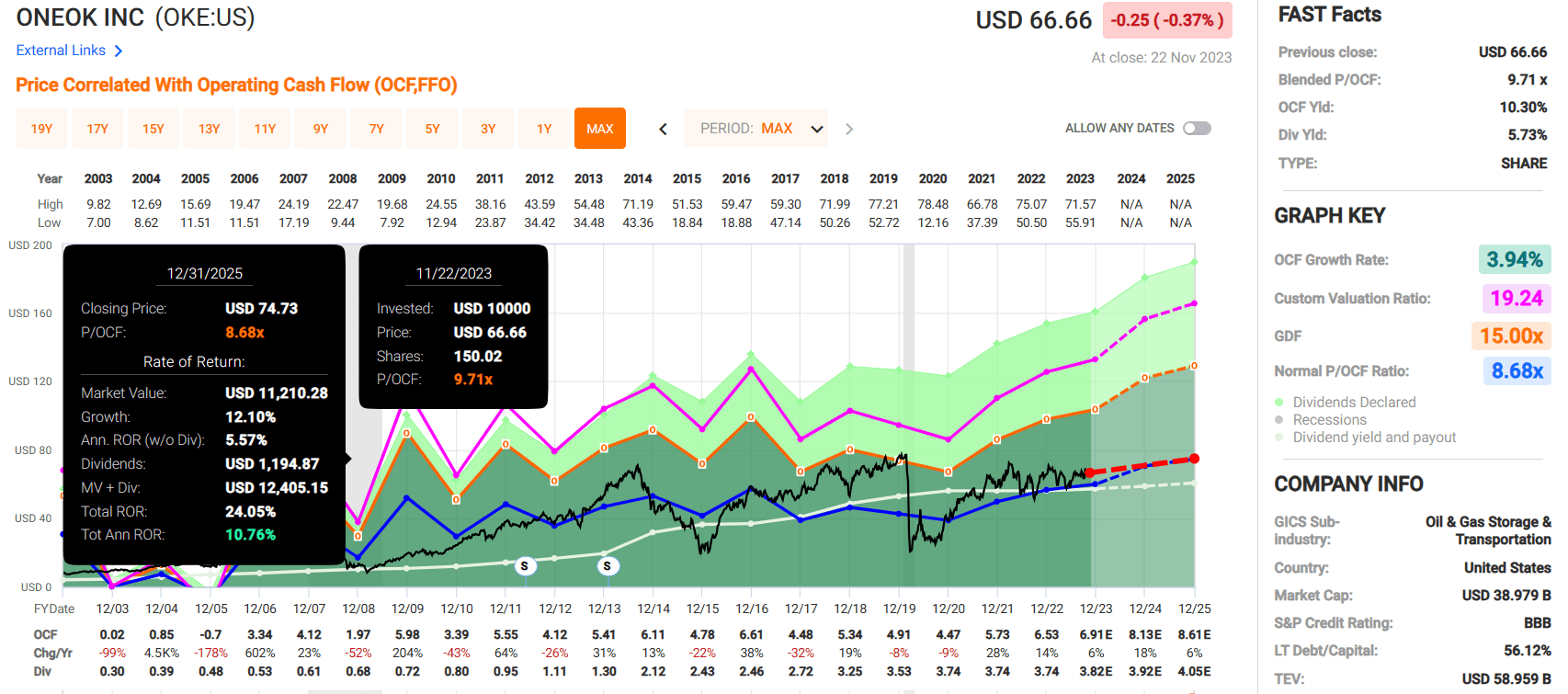

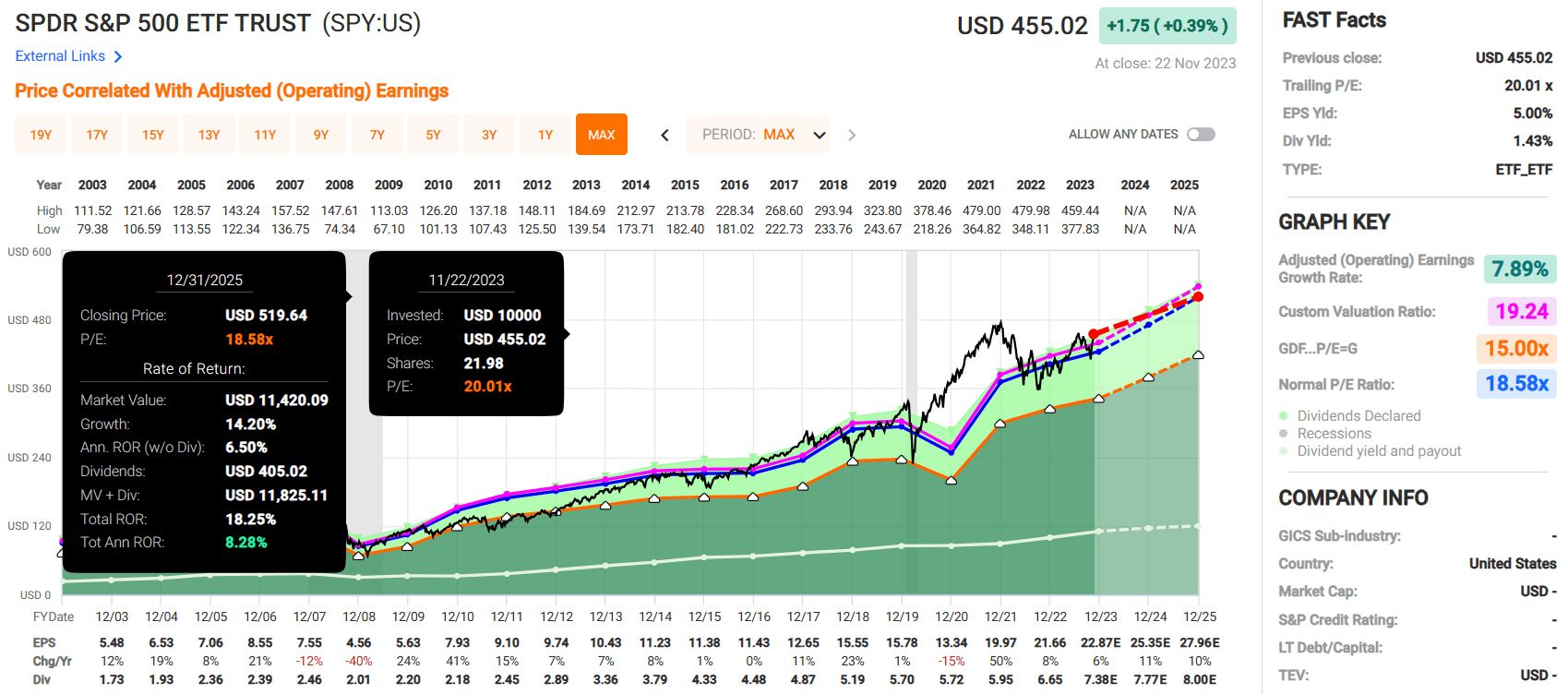

Imagine you purchased a $10,000 position in the company back in 2008: You would now be sitting on $128,000 with dividends reinvested - - an 18.5% compound annual growth rate. Relative to the $68,000 that the same amount invested in the S&P 500 ( SP500 ) would have grown to during that time, your total returns doubled the index.

The beauty of investing in superb high-yielders is that they don't have to grow at a fast rate to make for excellent investments. This is because reinvesting dividends alone made up about half of the total returns for ONEOK. If you missed the boat on ONEOK in the past 15 years, the good news is that I believe that it can keep beating the S&P 500 for the foreseeable future. Let's dive into the company's fundamentals and valuation to understand why.

{kind=link}

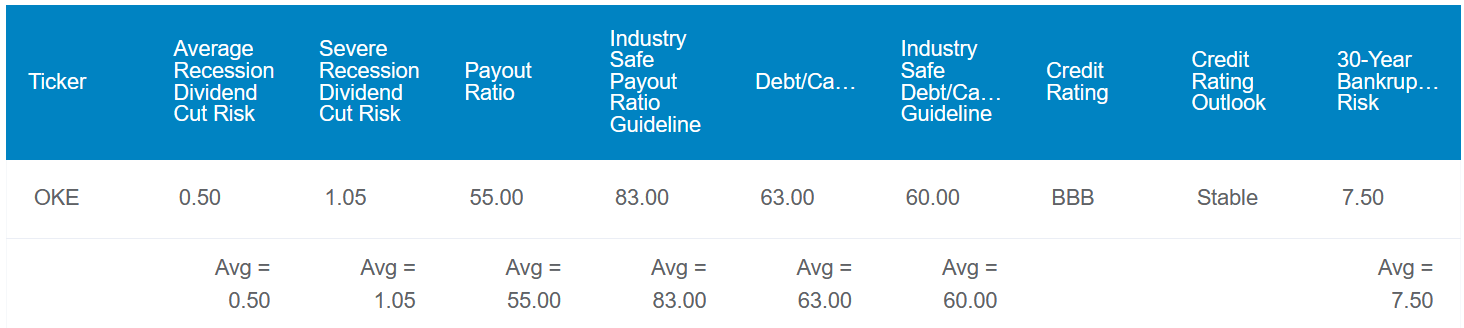

ONEOK's 5.7% dividend yield is about 130 basis points above the current 10-year U.S. treasury rate of 4.4% . Shareholders can rest assured that this dividend is quite sustainable. That is because the company's new DCF payout ratio with Magellan Midstream Partners incorporated into its business is just 55%. That is well below the 83% that rating agencies prefer from the midstream industry per Dividend Kings.

As I'll expand on further in the article, ONEOK is also a financially healthy business. This is evidenced by its 63% debt-to-capital ratio, which is about in line with the industry safe guideline put forth by credit rating agencies of 60%. This is why the company enjoys a BBB credit rating, which implies a somewhat modest 7.5% risk of going out of business by 2053.

{kind=link}

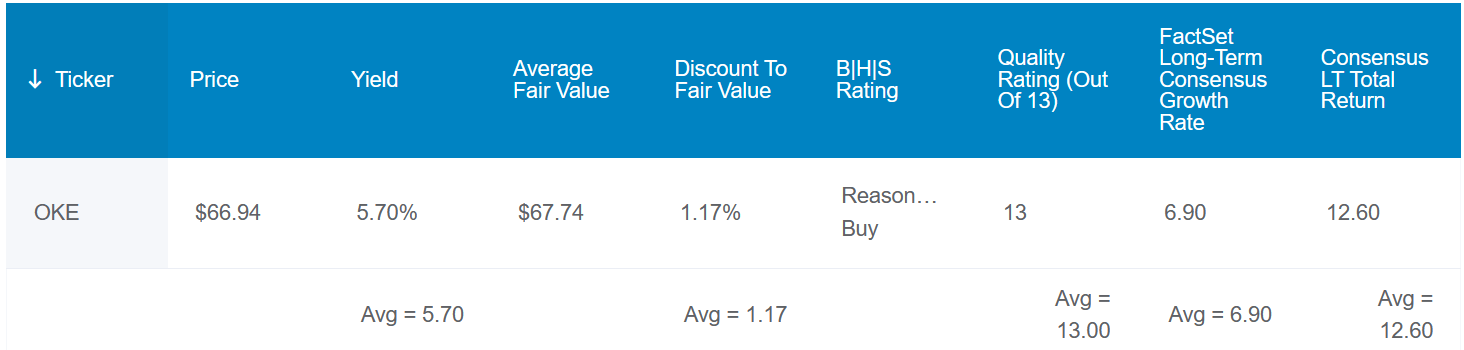

ONEOK also appears to be trading at a reasonable valuation. Based on historical yield and P/E ratio, the stock is approximately 1% discounted relative to its current $67 share price.

This may not be the biggest margin of safety in midstream. On the other hand, there are only a few companies in its space of comparable quality. So, any discount is compelling enough in my opinion to warrant a buy rating on ONEOK.

If the company can meet the analyst growth consensus and revert to fair value, here is what investors could stand to receive in total returns for the next 10 years:

- 5.7% yield + 6.9% annual growth consensus + 0.1% annual valuation multiple expansion = 12.7% annual total return potential or a 231% cumulative total return against the 9% annual total return potential of the S&P 500 or a 137% cumulative total return

A Highly Reliable Midstream Company

{kind=link}

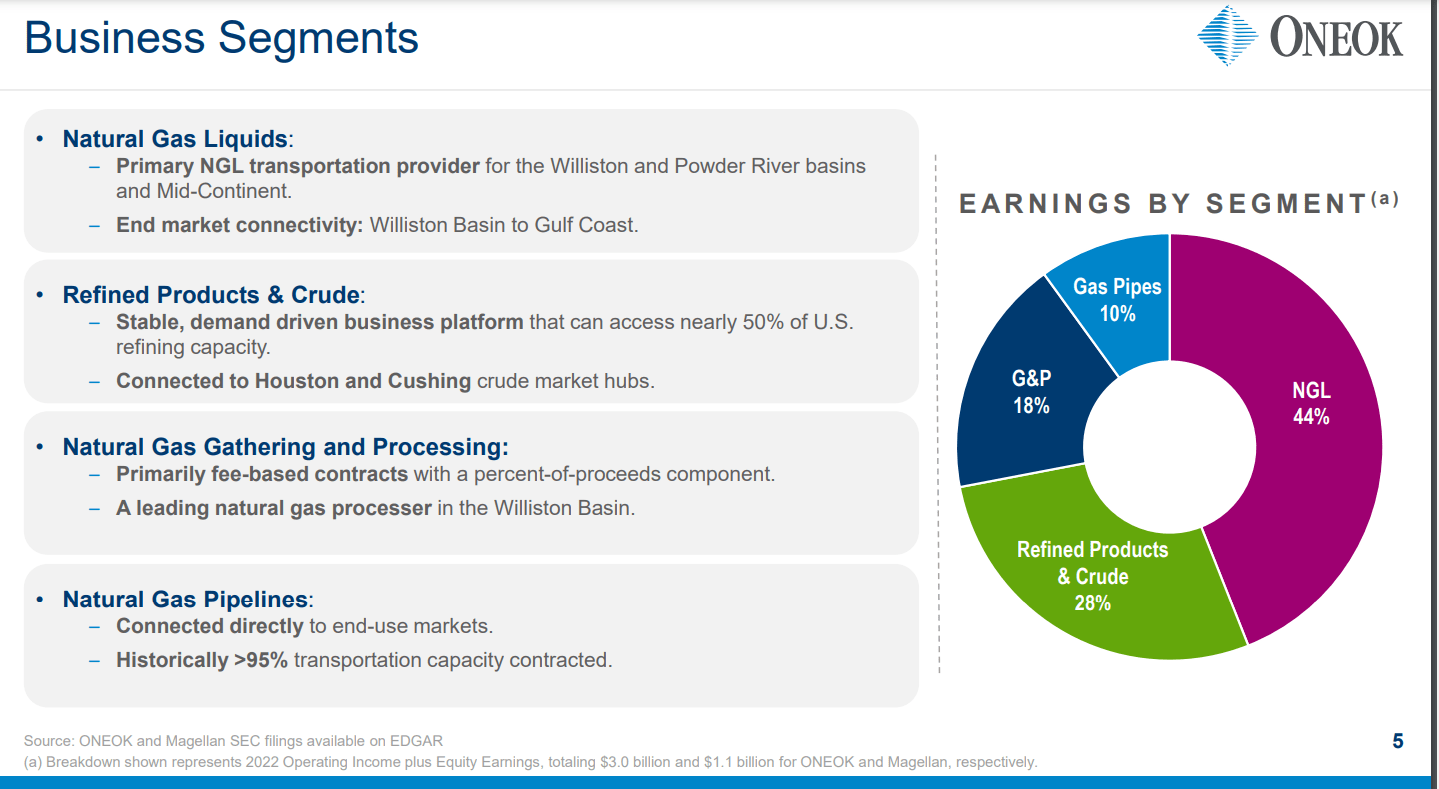

Owning over 50,000 miles of natural gas and NGL pipelines, crude oil pipelines, and refined products pipelines, ONEOK plays an important role in the U.S. economy. The company's infrastructure has access to roughly 50% of the country's refining capacity.

In 2022, ONEOK's business was mostly natural gas and NGL-based (72%), with the remainder of earnings (28%) being derived from refined products and crude, including Magellan. In total, the company anticipates that over 85% of its consolidated earnings will be fee-based this year. Simply put, ONEOK is largely insulated from the ebb and flow of fossil fuel commodities.

The company reported encouraging operating results for its third quarter ended September 30. ONEOK's adjusted EBITDA surged 11% higher over the year-ago period to $1 billion during the quarter. These results were driven by double-digit growth rates in NGL and natural gas processing volumes across the company's pipeline network. This includes an 18% boost in NGL raw feed volumes in the Gulf Coast/Permian region, a 6% increase in Rocky Mountain region NGL raw feed volumes, and a 12% bump in natural gas volumes processed in the quarter.

The industry remains as strong as ever according to ONEOK's President and CEO Pierce Norton. According to Mr. Norton's opening remarks on the Q3 2023 earnings call , North Dakota natural gas production reached a new all-time high in August. This helped to push the company's volumes higher for the third quarter.

Moving forward, there are plenty of catalysts that can continue to fuel growth for ONEOK. For 2024, management expects to generate at least $6 billion in adjusted EBITDA (versus approximately $5.1 billion in 2023). A full year of contributions from Magellan Midstream will largely contribute to this growth. Looking out to 2025, ONEOK expects meaningful projects to come online. Both the Mont Belvieu-6 Fractionator and the West Texas NGL pipeline expansion are on track to be completed in the first quarter of that year.

On the balance sheet front, ONEOK is also doing well. CFO Walt Hulse expects that the company's net debt to adjusted EBITDA ratio will clock in at a 3.7x annualized run-rate basis, excluding merger costs. For context, that would be ahead of the company's expectations when it announced its acquisition of Magellan. This puts ONEOK well on pace to get to its target leverage ratio of 3.5, which will give it more options to return value to shareholders.

The Dividend Can Steadily Move Higher

Regarding ONEOK's dividend, the company has either maintained or grown it for more than 25 consecutive years. This makes it an exceptional pick for a stable income.

As the company diverts more of its free cash flow toward share repurchases, more generous dividend increases that it has handed out in recent years should be the norm. That's because share buybacks will keep the overall dividend obligation in check. This is why I would anticipate mid-single-digit annual dividend growth from the company once it reaches its targeted leverage ratio.

Risks To Consider

ONEOK earns a perfect 13/13 quality rating from Dividend Kings. However, like any business, it has risks that investors should be able to handle before buying.

As is the case with all midstream companies, ONEOK faces counterparty risk. If its upstream and downstream customers encounter significant industry headwinds, some could go bankrupt. This would impact their ability to pay ONEOK for its services and the company's ability to recover these lost revenues.

Current trends suggest that demand for the products that ONEOK gathers, stores, and transports should slowly grow for at least the next few decades. If total reserves of fossil fuels prove to be inaccurate and the company hasn't already significantly shifted its business model by that point, its fundamentals could suffer, though.

Summary: A Favorable Risk/Reward Dynamic

{kind=link}

{kind=link}

ONEOK is a fundamentally sound company. Aside from its market-beating long-term return potential, it also has superior return potential in the next two years versus the SPDR S&P 500 ETF Trust ( SPY ).

Assuming a moderate downward reversion in its P/OCF ratio to its historical multiple of 8.7, OKE could generate a 24% total return through 2025 if it grows as expected. This is materially better than the 18% total return through 2025 that is forecasted for SPY. That's why I believe OKE is currently a buy.

For further details see:

ONEOK: Get Paid A 6% Yield And Beat The S&P 500