OKE - ONEOK Has Reliable Cash Flow Growth Potential

2023-07-31 17:17:04 ET

Summary

- ONEOK, Inc. is a more expensive company but it has a strong position in the natural gas industry.

- The company has a $30 billion market capitalization and an almost 6% dividend yield that it has a long history of increasing.

- The company is investing heavily within its business and we expect it to continue its growth, generating strong free cash flow and shareholder returns.

ONEOK, Inc. (OKE) is a large natural gas corporation with a market capitalization of $30 billion. The company has an incredibly impressive portfolio of natural gas midstream assets that continue to drive substantial volume, making the company a valuable investment. We expect the company's growth to continue going forward.

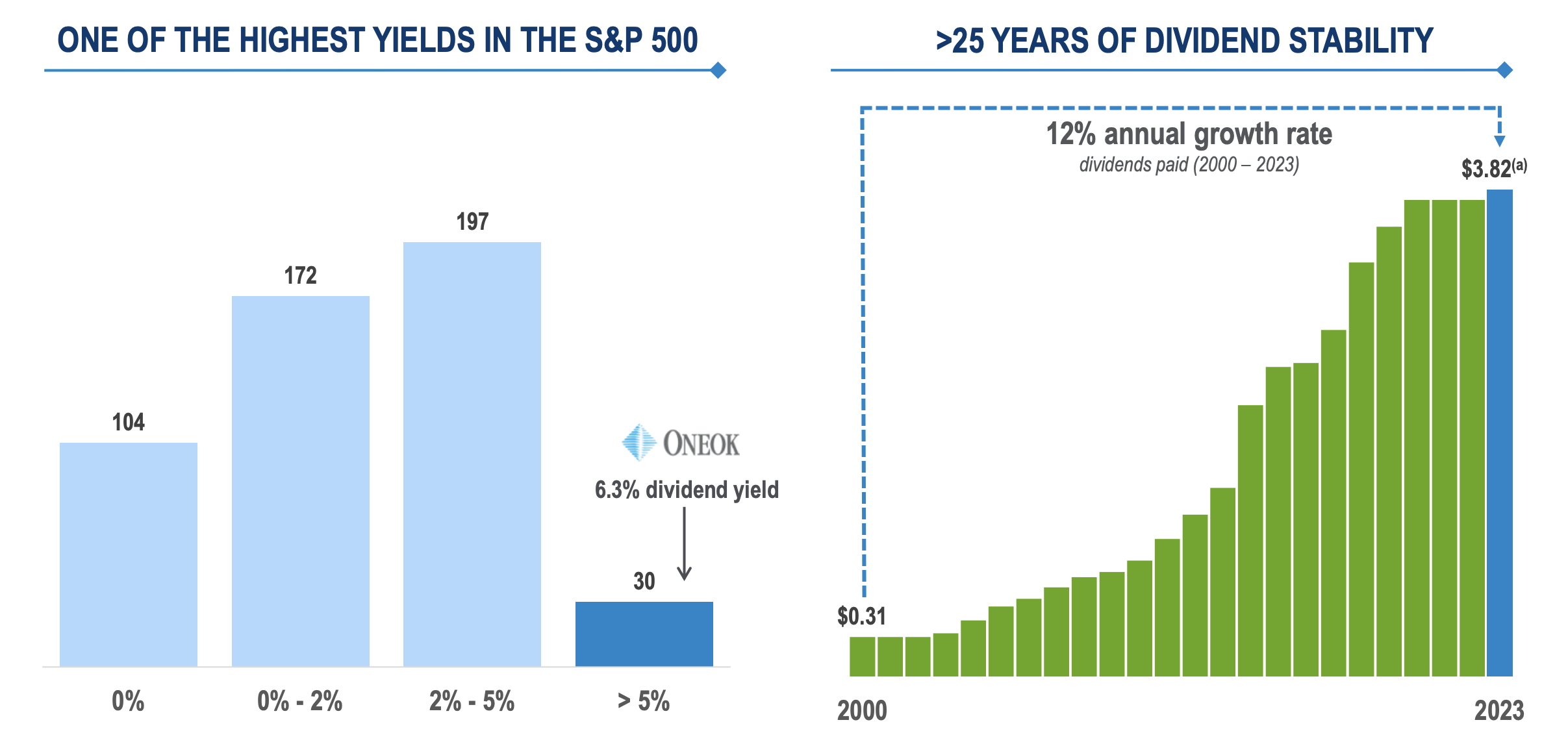

Oneok Dividend Profile

The company has performed incredibly well recently, showing its financial strength.

{kind=link}

The company has managed to achieve >25 years of dividend stability with a 12% annual growth rate. Unfortunately for the company, its dividend rate has stagnated in recent years. Of course there was a black swan event in between, but the company is slowly reverting to its prior history of growing its dividends.

The company currently has a 5.7% dividend yield and it's directing most of its cash flow towards dividends.

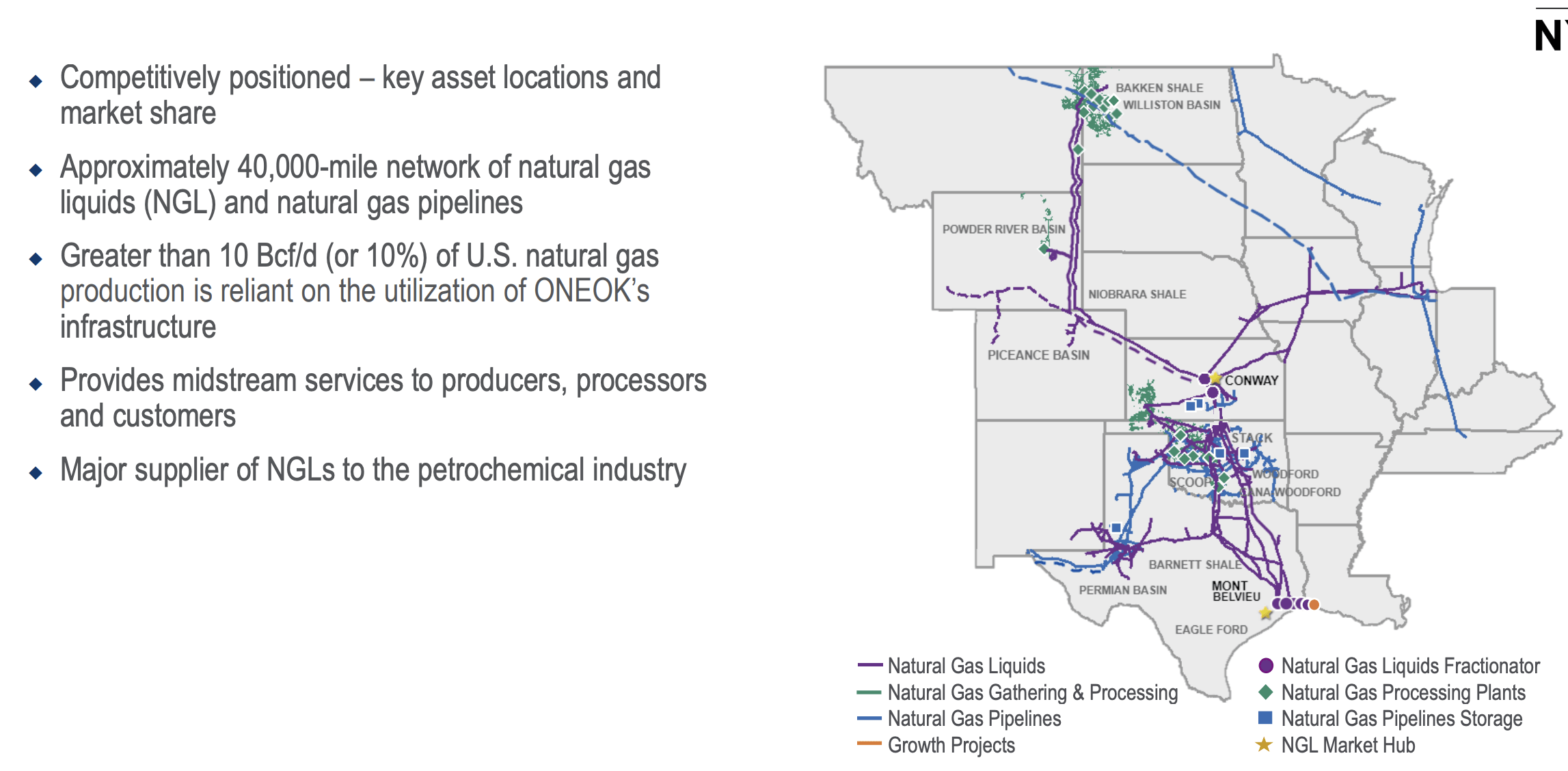

Oneok Asset Portfolio

The company has a strong portfolio of assets in the heartland of North America's energy production.

{kind=link}

The company is incredibly competitively positioned. It has a 40 thousand mile network of pipelines one of the strongest, and >10% of U.S. natural gas production is reliant on the company's infrastructure. The company operates in many unique folds of the industry, and with assets like fractionation hubs etc. it has multi-decade demand.

Unlike crude oil or coal, natural gas has much more staying power as a transitional fuel that's not weather depending. We expect lower emission and renewable natural gas to form a substantial part of the U.S.' fuel source for decades to come.

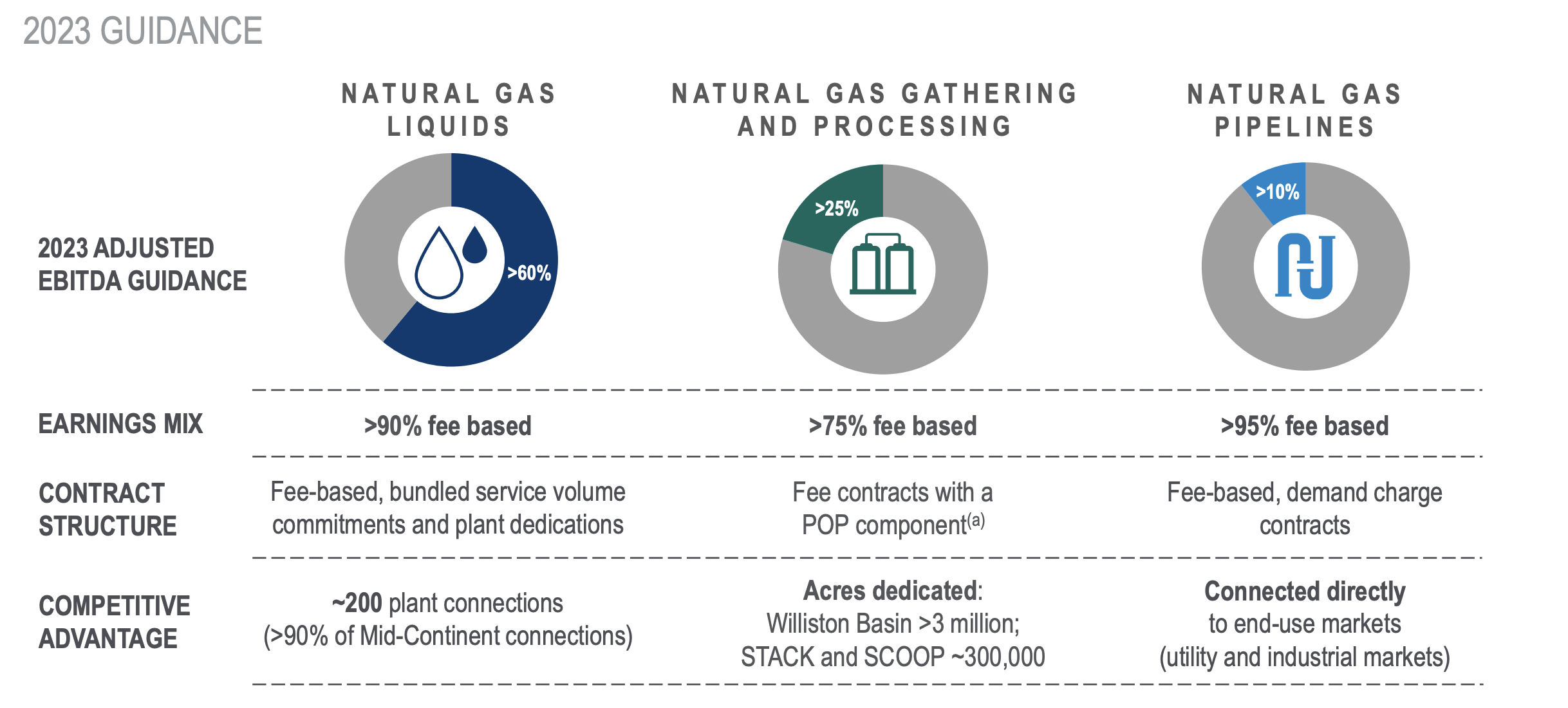

Oneok Business Segments

The company's business segments are fee based, but still susceptible to prices.

{kind=link}

The company's NGL business, it's largest, is >90% fee-based. Its strength here is its physical connection to a variety of plants, something that provides multi-decade reliability in earnings, and effectively a near monopoly for that position and segment of the company's business. The company's natural gas and processing business makes up ~25% of its EBITDA.

Here is the company's largest source of susceptibility to prices. The company has >3.3 million acres dedicated, including a major position in the Williston Basin. The company's natural gas pipelines are its smallest segment, but the most reliable from an earnings perspective. This segment will generate long-term reliable cash flow.

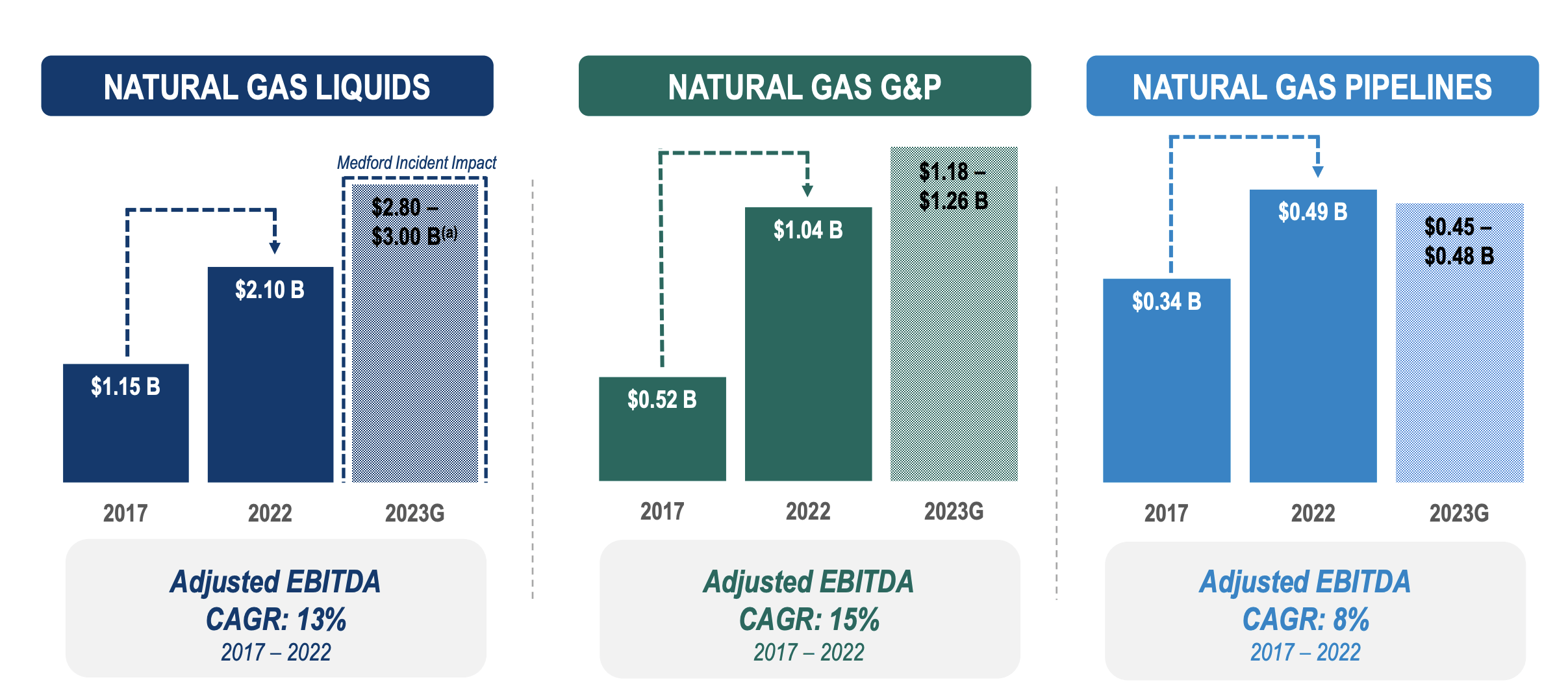

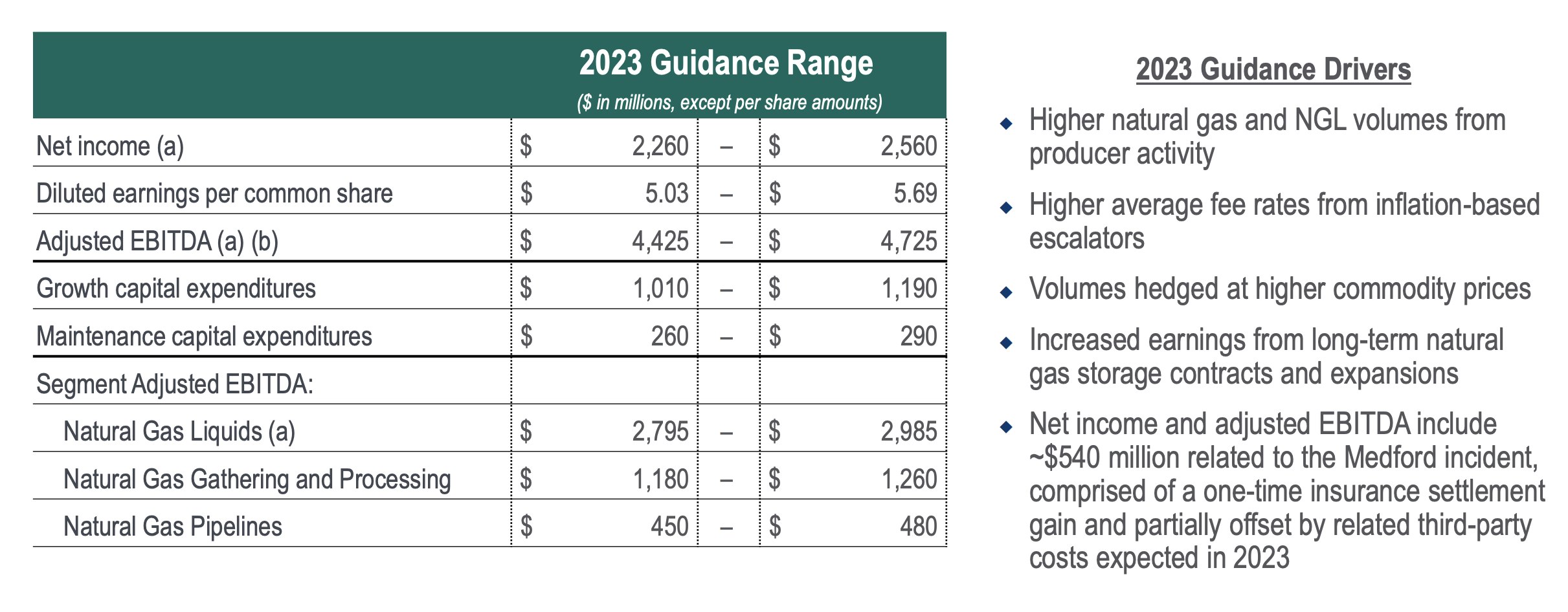

Oneok Guidance

The company's guidance shows the upside of its continued investments.

{kind=link}

The company is expecting its NGL business to earn $2.9 billion in adjusted EBITDA. That's substantial growth despite the impact of the Medford Incident and fire which recently had an agreement with insurers reached. The company's natural gas G&P business is expected 15% growth to $1.22 billion as the company sees double-digit growth across the board.

The company's NGL pipeline segment is expected to see a slight decrease in size, but as the company's smallest business it's less important.

{kind=link}

Financially, the company expects $2.4 billion in net income and $4.6 billion in adjusted EBITDA. The company's growth capital forecast is $1.1 billion with maintenance capital much smaller, growth capital spending that we've already discussed. The company is supported by higher volumes and earnings from inflation-based escalators, but it's impacted by $540 million in inflation.

The company's true EBITDA without those one-time effects is closer to $4.1 billion. Financially the company's guidance and strong growth will enable strong shareholder returns.

Thesis Risk

The largest risk to our thesis is the pricing of the goods that the company moves. The company is profitable but some segments are heavily dependent on both continued strength in prices and demands. At the same time, the company is investing heavily in growth capital (25% of its 2023 EBITDA, 3% of its market cap), investments it needs to pan out.

Either of these things could hurt the company substantially.

Conclusion

ONEOK, Inc. is one of the largest natural gas companies. The company has an almost 6% dividend yield and a long history of increasing its dividend. We expect it to continue that now that its EBITDA is growing rapidly, after the black swan event that was COVID-19. That dividend will continue to be the primarily source of returns, making the company more expensive.

The company's true risk is its massive growth capital spending and how it pans out. It has numerous incremental growth capital projects, but it's spending a substantial amount of its free cash flow. How that pans out remains to be seen, but we overall expect ONEOK, Inc. to continue generating strong and growing dividends for shareholders.

For further details see:

ONEOK Has Reliable Cash Flow Growth Potential