OKE - ONEOK Is A Buy With Or Without Magellan Midstream

2023-06-23 13:56:49 ET

Summary

- ONEOK, Inc. is facing opposition in its bid to acquire Magellan Midstream Partners, L.P. from the latter's equity owners.

- Magellan Midstream Partners units are a Sell or Hold, depending on the tax impact for its investors.

- ONEOK, Inc. shares are a Buy regardless of whether a deal closes or not.

There was big news today concerning proposed ONEOK, Inc. ( OKE ) acquisition of Magellan Midstream Partners, L.P. ( MMP ). Energy Income Partners, a large MMP equity owner, has come out against the deal . Energy Income Partners holds 3% of MMP shares, which makes it the company's fourth largest unitholder. It wants MMP to remain a standalone entity.

It's not surprising to see a large institution that has held MMP units for many years opposed to the deal. A sale will trigger huge tax obligations for longtime MMP holders, which in some instances will exceed the cash portion of the deal. Also, OKE's acquisition price undervalues MMP equity.

The recent widening of MMP's unit price and OKE's offering price has grown larger, implying that the market is doubtful the deal will go through. At the moment, MMP trades at $59.80. OKE trades at $57.50, putting its offer consideration for MMP at $63.35 based on the formula of $25 per share of cash and 0.667 OKE shares for each MMP share.

We had expected the deal to go through. We detailed our thoughts in a previous article . Excluding tax implications for MMP unitholders, while the deal undervalues MMP, the new post-merger entity will generate attractive long-term returns for current MMP unitholders.

The deal is also attractive for OKE shareholders. It would add to OKE's intrinsic value by increasing its long-term cash flow generation potential, while adding operational diversification and new assets that generate high returns on capital to OKE's existing high-return asset base. OKE will emerge from the deal generating one of the highest returns on capital in the midstream sector and by far the highest return on capital among its large-cap midstream peers.

MMP Could be Either a Hold or a Sell

Whether the deal goes through or not, there has been no change in the fundamental outlook for either MMP or OKE on a standalone basis since the deal was announced on May 14.

For MMP holders, a decision to sell depends primarily on an investor's tax obligation triggered by the sale.

If an MMP unitholder's tax obligation is high, the units could be a Hold due to the chance that the deal falls through. However, the unit price would probably fall to its pre-deal trading level in the mid-$50s, implying roughly 10% downside from its current $61.75

If an MMP unitholder's tax obligation is low, MMP could be a sell due to the higher probability that the deal goes through, as well as the fact that attractive MLP alternatives exist at the moment. Enterprise Products Partners ( EPD ), MPLX ( MPLX ), and Plains All American ( PAA ) ( PAGP ) are among them.

OKE Remains a Buy

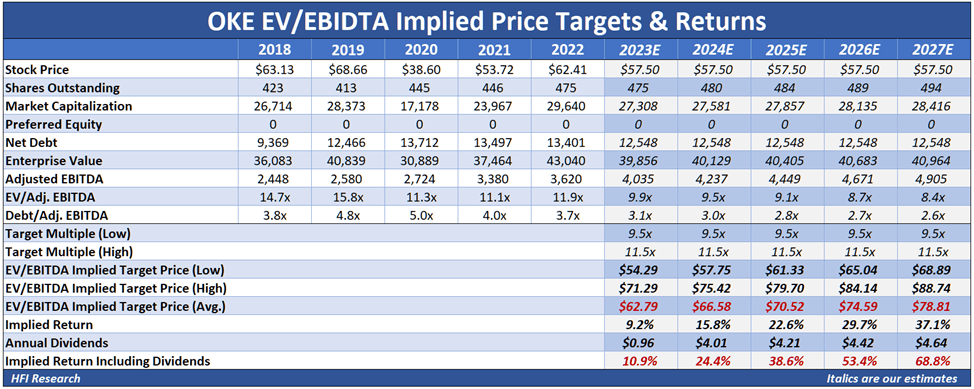

For OKE, the recent selloff in response to the announced MMP acquisition has pushed the shares 12.9% below our $66 price target and 8.4% below our EV/EBITDA valuation of $62.79 for 2023. OKE is now trading at a discount in the neighborhood of large-cap MLP peers, which are subject to a persistent MLP discount.

OKE's dividend yield has grown to 6.6% as its stock has sold off, making it also underpriced relative to other high-yielding corporate equities when its cash-flow stability and high-quality assets are taken into consideration. At the moment, the yield is one of the highest in the S&P 500. OKE's dividend is also safe, covered 1.21-times by free cash flow and is well-protected from inflation. With or without MMP, we expect it to grow at a low-to-mid single-digit percentage rate over the next few years. At their current price, OKE shares are particularly attractive for income investors.

OKE's return on capital employed and return on equity are up there with MMP's as some of the highest in the midstream sector. The returns are also among the highest in the entire energy sector.

{kind=link}

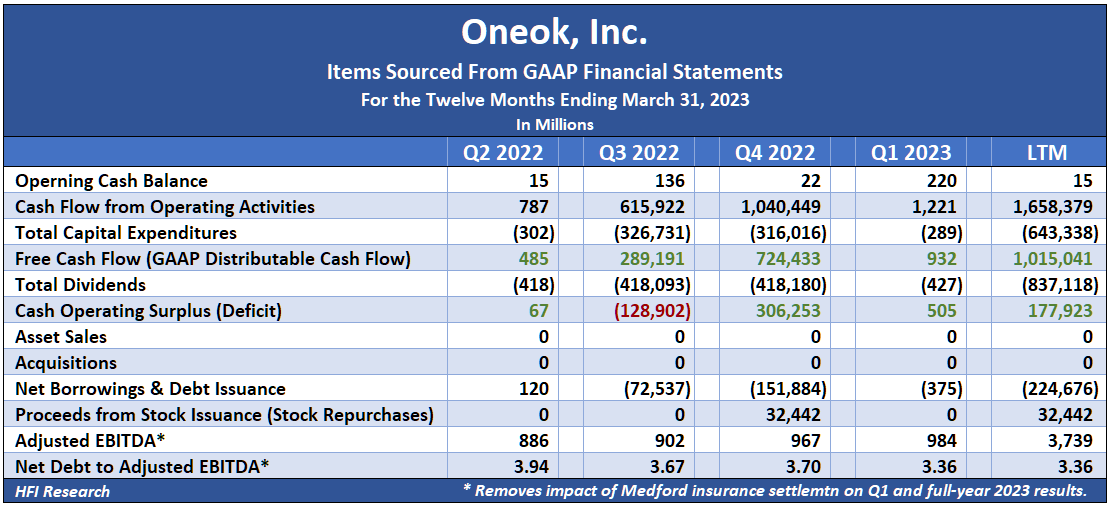

Over the past year, the company has allocated free cash flow and, to a lesser extent, proceeds from common equity sales, toward paying down debt. We should note that OKE's regular and significant equity sales over the years would typically raise alarm bells for its investors. However, the company is one of the exceptional cases where equity sales have been put to good use to fund high-return projects that have significantly increased both the company's longevity and its shareholder value.

{kind=link}

The table also shows that OKE's EBITDA has increased each quarter over the past year. Higher EBITDA and lower debt have reduced its leverage ratio to a conservative 3.36-times. Increased financial flexibility will allow for stepped-up share repurchases and/or dividends. The company generates enough free cash flow to boost its dividend by up to 10% from its current level of $3.82 per share.

OKE could also use its excess free cash flow to fund new growth projects. The company is one of the few management teams we would trust with growth capex and even acquisitions. We consider management's capital allocation skill one of the most attractive features of OKE shares.

Valuation

Our OKE price target is $66. It would remain unchanged if the deal is not consummated.

Assuming no deal occurs, our valuation for OKE based on an EV/EBITDA multiple implies the shares are worth $62.79, increasing to $72.99 by 2027. Assuming 5% Adjusted EBITDA growth and 5% dividend growth over the next five years, our valuation implies a 68.8% total return from the current level of $57.50. This is higher than most of OKE's large-cap midstream peers.

{kind=link}

OKE has the added benefit of pricing power, which protects its financial results against inflation. In the event inflation remains high, OKE shareholders should fare better than those of other large midstream operators such as Kinder Morgan ( KMI ) and Williams ( WMB ), both of which have more limited pricing power and lower returns on capital than OKE.

Since we believe the odds are good that inflation will remain elevated over the coming years, OKE's inflation protection-with or without the MMP deal-sets it apart from most yielding securities.

Conclusion

We view the combined OKE-MMP entity as superior to a standalone OKE. But in the event the deal fails to close, OKE's recent selloff makes its shares attractive for long-term holding. In the event the deal gets voted down, OKE shares are likely to pop back to the pre-deal range in the low-to-mid-$60s, providing a quick 10% return from current levels.

Given OKE's attractive economics and discounted shares, income-seeking investors should consider buying ONEOK, Inc. whether the Magellan Midstream Partners, L.P. deal closes or not.

For further details see:

ONEOK Is A Buy With Or Without Magellan Midstream