OKE - ONEOK: One Big Caveat To Remember In 2023

2023-03-23 03:24:50 ET

Summary

- ONEOK enjoyed a strong end to 2022 with the full year seeing new record-setting operating cash flow.

- When looking at their now formalized guidance for 2023, on the surface their adjusted EBITDA forecasts a very impressive circa 26% year-on-year.

- There is one big caveat to remember, which is their insurance payout during 2023 influences the year-on-year comparison versus 2022.

- This means that investors should not get too excited when reviewing their results for 2023, as skyrocketing earnings will only be temporary.

- Since their underlying earnings are still forecast to increase almost 10% year-on-year during 2023, I still believe that maintaining my buy rating is appropriate.

Introduction

By late 2022, it had been nearly three years since ONEOK ( OKE ) paused their dividend growth but thankfully, it finally seemed that 2023 was shaping up great for dividend fans because as my previous article highlighted, there were prospects for their dividend growth to restart. Much to the delight of shareholders, this was proven apt with management increasing their dividends early in 2023 as was hoped when conducting the previous analysis. At the same time, they also formalized their previous generalized guidance for the year ahead and whilst it seems very impressive on the surface, alas there is one big caveat to remember in 2023 that influences their upcoming results.

Coverage Summary & Ratings

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

{kind=link}

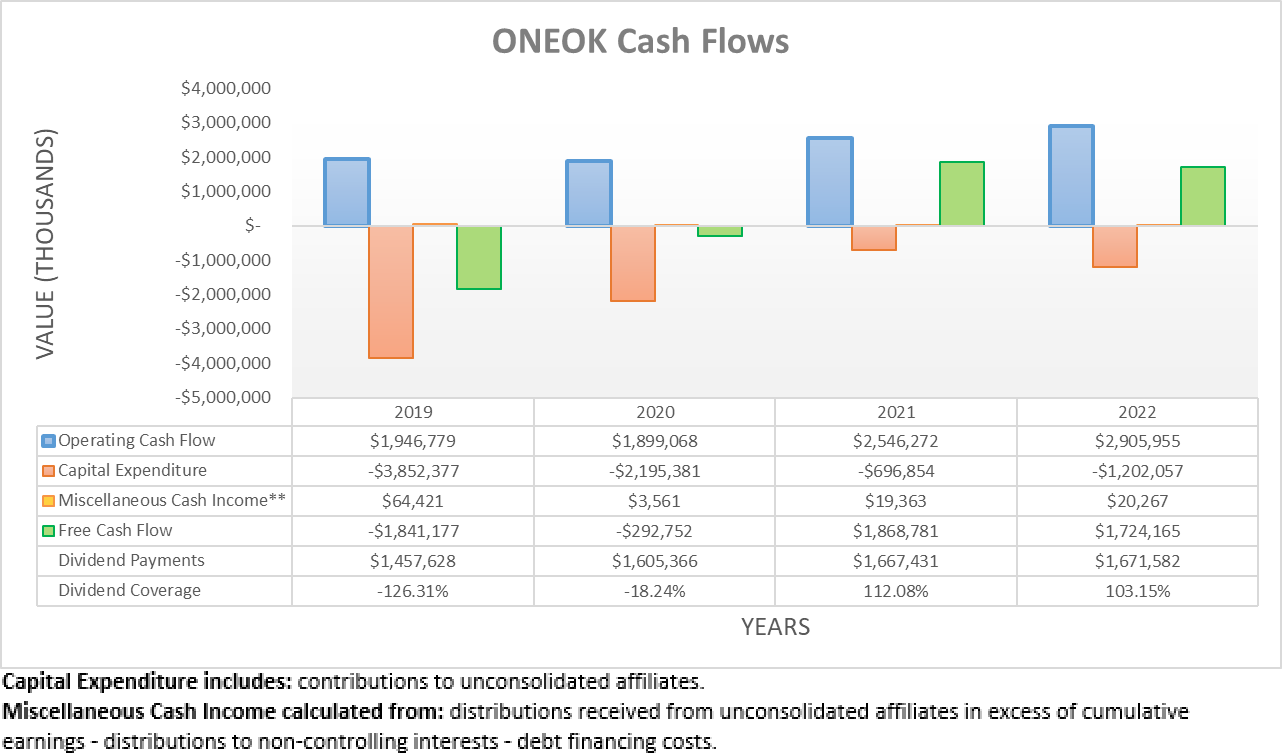

Following their impressive performance earlier in the year, it was positive to see 2022 end on a strong note with their operating cash flow landing at $2.906b. Apart from representing a new record-setting result, it also represents an impressive circa 14% increase year-on-year versus their previous result of $2.546b during 2021. When everything was said and done elsewhere within their cash flow performance, they ultimately translated $1.724b of this operating cash flow into free cash flow during 2022, which was able to provide adequate dividend coverage of 103.15% to their accompanying payments of $1.672b.

{kind=link}

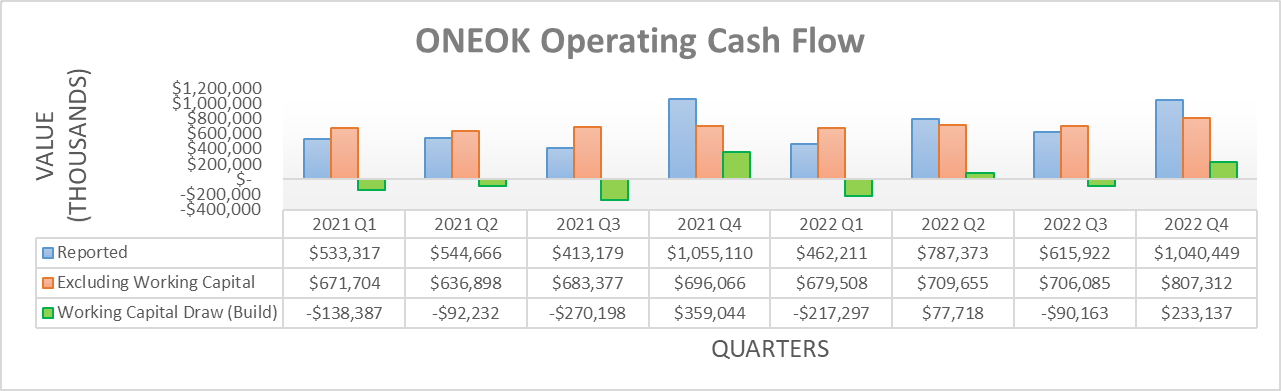

When viewed on a quarterly basis, it shows the fourth quarter of 2022 was particularly strong with their reported operating cash flow actually breaching the $1b mark, which is a rare feat for their company. Admittedly, this was aided by an additional cash infusion from a working capital draw of $233.1m but even if excluded, their underlying result of $807.3m was still a strong result and the highest in recent history since at least the beginning of 2021.

That said, this particularly strong result was also due to $100m of proceeds during the fourth quarter of 2022 pertaining to the insurance payout from the Medford incident, as detailed within their fourth quarter of 2022 results announcement . If also excluded from their underlying operating cash flow, it would still leave a result of $707.3m and thus similar to their previous results of $709.7m and $706.1m during the second and third quarters, respectively. Once applied to their full-year results, excluding working capital movements and insurance proceeds leaves a result of $2.802b. Interestingly, when looking ahead into 2023, their previously linked fourth quarter of 2022 results announcement flags that another $830m of insurance proceeds landed during the first quarter of 2023 and thus going forwards into the year ahead, there is one big caveat to remember.

ONEOK Fourth Quarter Of 2022 Results Presentation

Since conducting the previous analysis, they have now formalized their generalized guidance for 2023 that seems very impressive but alas, there is more to consider. On the surface, their forecast sees their adjusted EBITDA hitting a massive $4.575b at the midpoint and if forthcoming, this would represent a very impressive circa 26% increase year-on-year versus their result of $3.62b during 2022 but as their previously linked fourth quarter of 2022 results announcement detailed, their adjusted EBITDA includes insurance income.

Personally, I would have preferred to see the boost from insurance income excluded from their adjusted EBITDA because in my eyes, the purpose of "adjusted" earnings is removing abnormal impacts that influence their comparability. Alas, at least they have provided enough information for investors to handle this task manually with their adjusted EBITDA forecast during 2023 including a $779.3m boost, whilst their result during 2022 included a $150.7m boost.

Before moving forwards, it should be clarified that a difference exists between their cash and accrual-based results due to the delay before receiving insurance proceeds versus when it was recorded on their income statement but at the end of the day, both total $930m. To this point, their operating cash flow saw $100m of proceeds during 2022 with a further $830m following during 2023, whilst their income statement saw $150.7m and $779.3m across these same two points in time, respectively.

If these boosts are excluded from their adjusted EBITDA forecast for 2023, the underlying forecast is $3.796b, whilst the same process for their results during 2022 shows an underlying result of $3.469b. In reality from a fundamental perspective, their earnings during 2023 should increase around 9.50% year-on-year at the underlying level, which is still impressive but nevertheless, this is a big difference versus the circa 26% that investors will otherwise see on the surface given their insurance income.

When looking at their capital expenditure guidance for 2023, thankfully it is quite straightforward with a forecast of $1.375b at the midpoint, which is only a slight increase year-on-year versus their spending of $1.202b during 2022. After having increased their dividends slightly as expected when conducting the previous analysis, their new quarterly rate of $0.955 per share will see a cost of $1.708b per annum, given their latest outstanding share count of 447,220,972. In total, this sees their estimated cash outflows for 2023 at circa $3.083b, give or take a little depending on where their capital expenditure lands within their guidance range.

When it comes to their estimated cash inflows, the $830m proceeds from insurance stands to see these easily outpace these outflows but in my opinion, the more important question is how they would fair without this boost. In theory, their underlying operating cash flow during 2022 of $2.802b should see a similar increase as their adjusted EBITDA given its positive correlation, thereby increasing circa 9.50% year-on-year to circa $3.07b, once again give or take a little depending upon working capital movements and where their results land within their guidance range. This sees their estimated cash inflows effectively matching their accompanying outflows and thus similar to 2022, it sees adequate dividend coverage.

{kind=link}

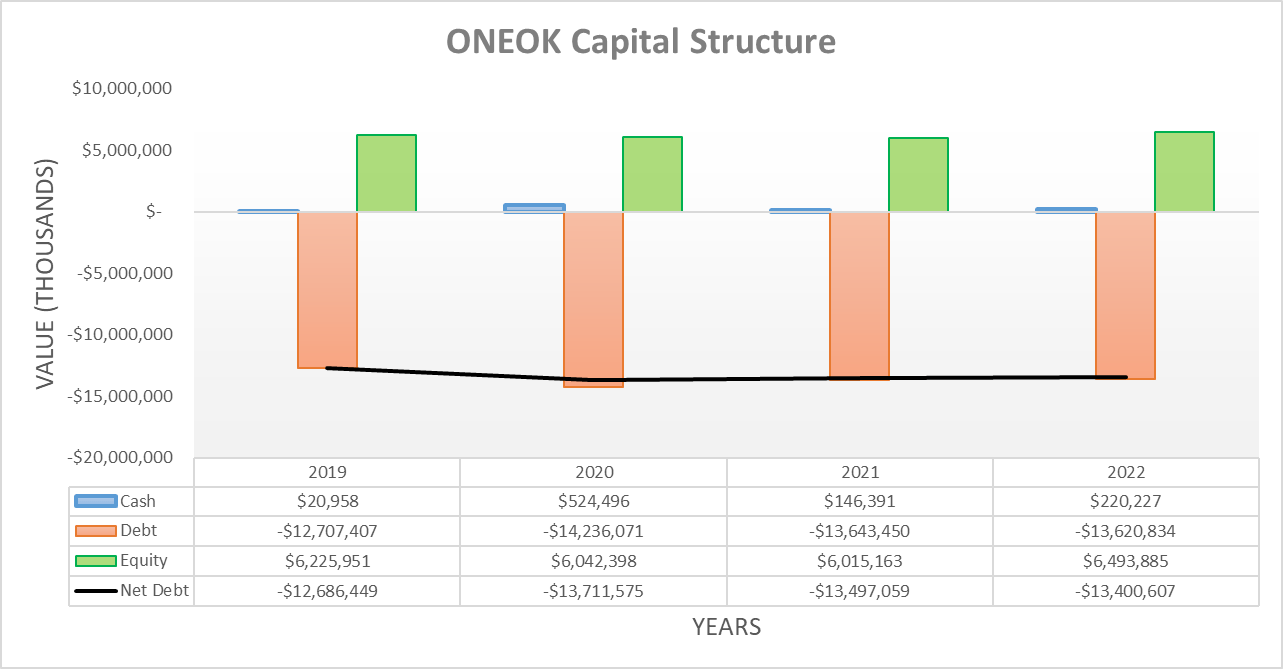

Thanks to the additional cash infusion from their working capital draw during the fourth quarter of 2022, their net debt actually decreased to $13.4b versus its previous level of $13.755b following the third quarter. Despite only being a small decrease in the grand scheme, this now sees two consecutive annual decreases, given that 2021 ended with net debt of $13.497b, whilst 2020 ended with a level of $13.712b.

Going forwards into 2023, their net debt should decrease but this is largely due to their $830m insurance payment, which by itself can shave away circa 6% of their net debt. At the underlying level absent of this boost, their aforementioned estimated cash inflows and accompanying outflows would have otherwise seen their net debt remain broadly unchanged.

{kind=link}

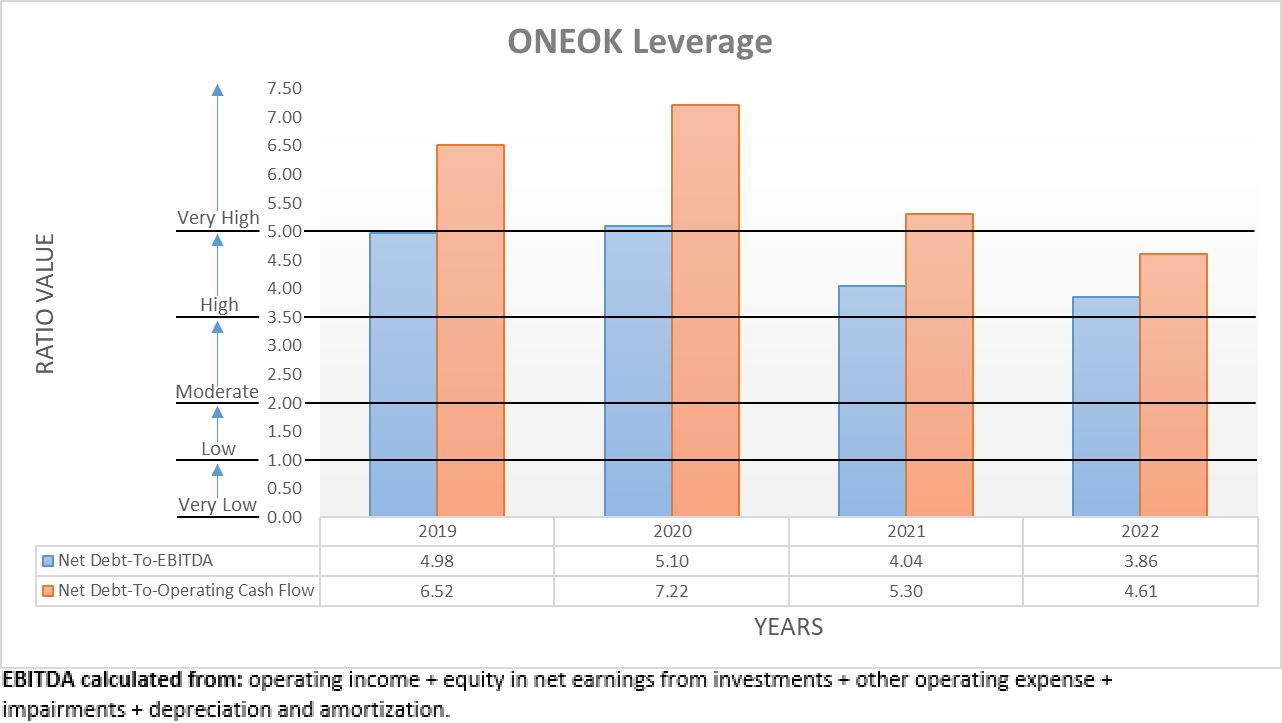

When it comes to their leverage, it also decreased in tandem with net debt during the fourth quarter of 2022. As a result, their net debt-to-EBITDA is now 3.86, whilst their net debt-to-operating flow is 4.61 and thus, both have decreased versus their previous respective results of 3.92 and 4.92 following the third quarter. Even though these see leverage remaining within the high territory of between 3.51 and 5.00, this is not concerning for a midstream company and importantly, it is positive to see these working their way lower, which should continue going forwards into 2023.

Since the aforementioned boost to their financial performance from their insurance payout is included within their results in 2023, the resulting circa 26% year-on-year increase will see their leverage decrease to a similar extent, even before considering their net debt decreasing. Whilst this would be wonderful, it would only be short-lived with 2024 obviously not seeing another boost. At least at the underlying level, their prospects for their earnings to increase circa 9.50% year-on-year should still see their leverage decrease, even after this boost fades into the past.

{kind=link}

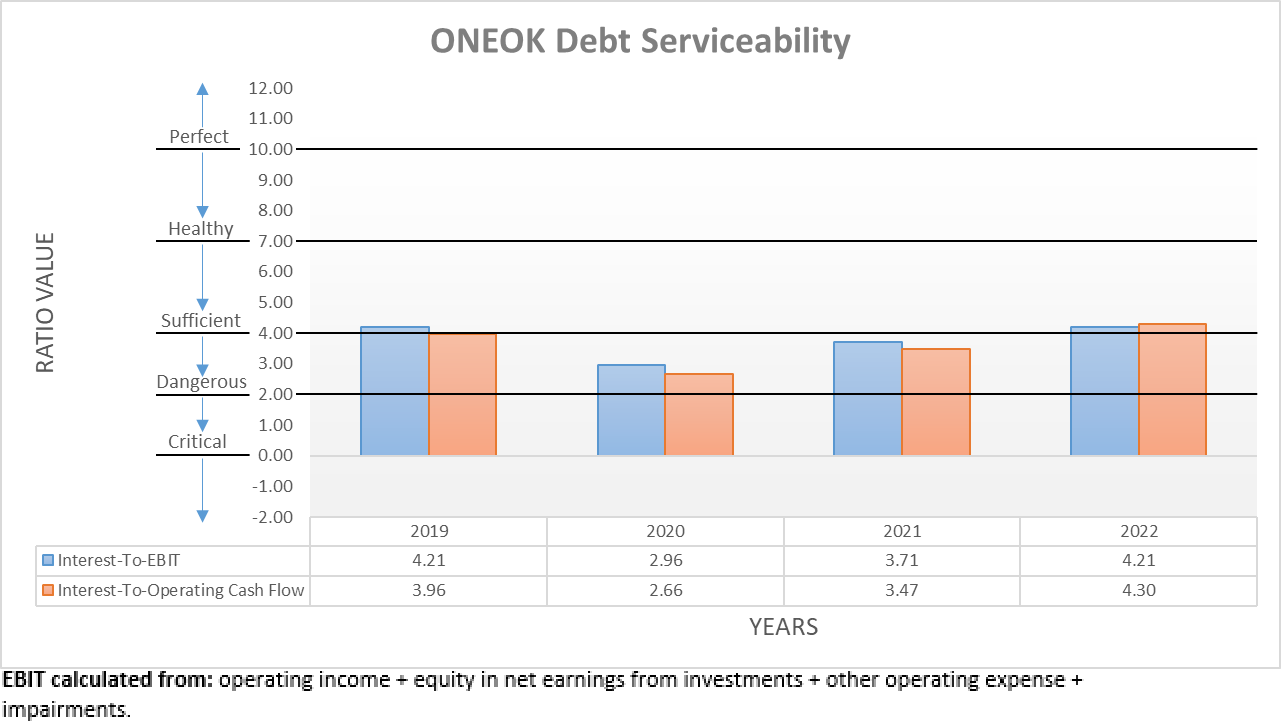

Whilst their net debt decreased during the fourth quarter of 2022, alas their debt serviceability was mixed with their interest coverage when compared against their EBIT virtually unchanged at 4.21 versus their previous result of 4.24 following the third quarter. Whereas due to their aforementioned working capital draw, their interest coverage when compared against their operating cash flow increased noticeably to 4.30 versus its previous result of 3.66 and thus, it now joins the former within the range that I consider healthy. Similar to their leverage, these both stand to see a large boost during 2023 due to their insurance payout but thankfully at the underlying level, their prospects to see their earnings increase will once again keep these improving even after this boost fades into the past.

{kind=link}

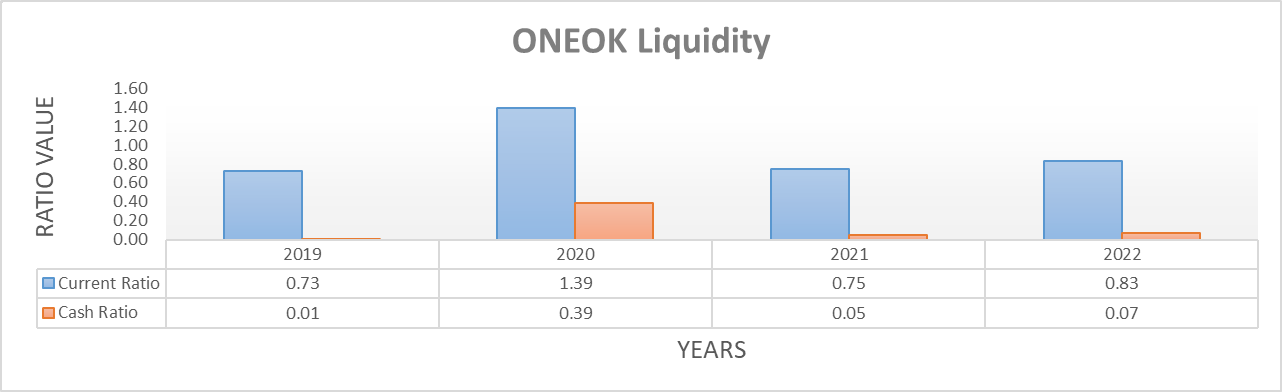

Even though the outlook for their leverage and debt serviceability is tricky, at least their liquidity is still straightforward. Thanks to their cash balance expanding to $220.2m during the fourth quarter of 2022 versus its previous balance of only $22.2m following the third quarter, their cash ratio increased to 0.07 versus 0.01 across these same two points in time, respectively. Concurrently, their current ratio also followed along in tandem by increasing to 0.83 versus 0.67, respectively. Since their aforementioned estimated cash inflows are effectively matching their accompanying outflows during 2023, they should not need to lean upon capital markets and thus by extension, the recent banking crisis does not pose too significant of a risk. Plus, as one of the largest midstream companies with growing earnings, they should still be capable of finding support to refinance debt maturities as required, regardless of where monetary policy heads.

Conclusion

When going into 2023 and reviewing their upcoming results, there is one big caveat to remember before getting too excited about their operating cash flow and earnings skyrocketing, whilst their leverage plunges. Namely, their results are going to see a boost from their insurance payout from the Medford incident and likewise, when 2024 rolls around in another year, it will also be important to remember the resulting unfavorable comparison before getting too disappointed. That said, even after excluding the boost of their insurance payout, it nevertheless seems that 2023 will still be a solid year at the underlying level with earnings forecast to see a near double-digit increase year-on-year and thus I believe that maintaining my buy rating is appropriate.

Notes: Unless specified otherwise, all figures in this article were taken from ONEOK's SEC filings , all calculated figures were performed by the author.

For further details see:

ONEOK: One Big Caveat To Remember In 2023