OKE - ONEOK: Ready For A Dividend Increase In 2023

Summary

- ONEOK, Inc. reported a Q3 earnings miss but executed well on the operations front.

- Management guided to more than 10% EBITDA growth in 2023.

- ONEOK remains one of our favorite midstream corporations.

ONEOK, Inc. ( OKE ) has been our go-to among large-cap midstream corporations in 2022. While third quarter financial results disappointed, we expect the company to grow and reward shareholders with an increasing dividend over the next few years. ONEOK, Inc. units are trading on the high end of our value range, and as such we reiterate our Hold rating.

ONEOK, Inc. Q3 Earnings Miss Overshadowed by Bullish Guidance

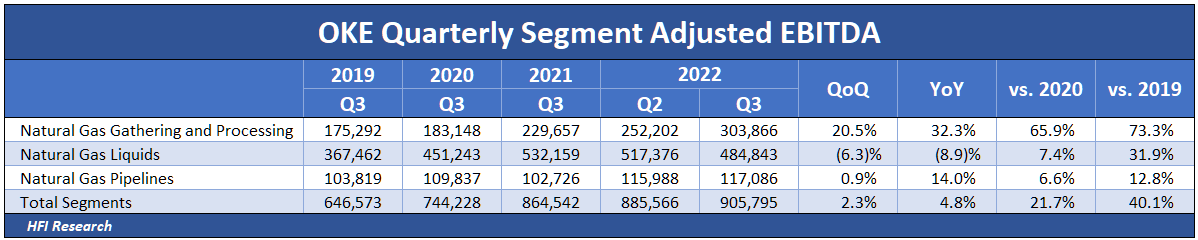

OKE’s third-quarter Adjusted EBITDA missed analyst consensus expectations, with the company reporting $902 million of Adjusted EBITDA versus expectations of $918 million.

The miss was attributable to lower-than-expected EBITDA in OKE’s NGL segment. The segment’s EBITDA declined by 8.9% from the third quarter of 2021 due to unfavorable basis differentials and higher operating costs partly due to the fire at OKE’s Medford, Oklahoma fractionation facility, as well as the inability to offset certain operating costs via inflation escalators in OKE’s service contracts.

OKE’s other segments performed well, with Natural Gas G&P posting an impressive 32.3% year-over-year gain.

{kind=link}

We expect the NGL segment to bounce back over future quarters as volumes increase, commodity prices stabilize from the volatile third quarter, and new NGL assets are placed into service.

Operationally, OKE’s throughput volumes increased across the board, as the $5 billion of growth projects from the past few years have been placed into service.

{kind=link}

In OKE’s third-quarter earnings conference call, management focused investor attention away from the third-quarter miss and toward its rosy full-year 2023 Adjusted EBITDA guidance of $4 billion, which is more than 10% above 2022. The news caused OKE’s stock to increase from $60.50 the day before its earnings announcement, to $66.00 today, for a gain of 9.1%. Over the same timeframe, the Alerian MLP Index fell by 5.3%.

OKE’s stepped-up 2023 guidance is attributable to management’s expectation that natural gas volumes will be up across all three of OKE’s main basins, namely, the Bakken, the Mid-continent, and the Permian. The rising volumes will benefit the $1.2 billion of growth projects that OKE has entering service next year, such as its fifth Mont Belvieu fractionator.

Flipping to a Cash Flow Surplus

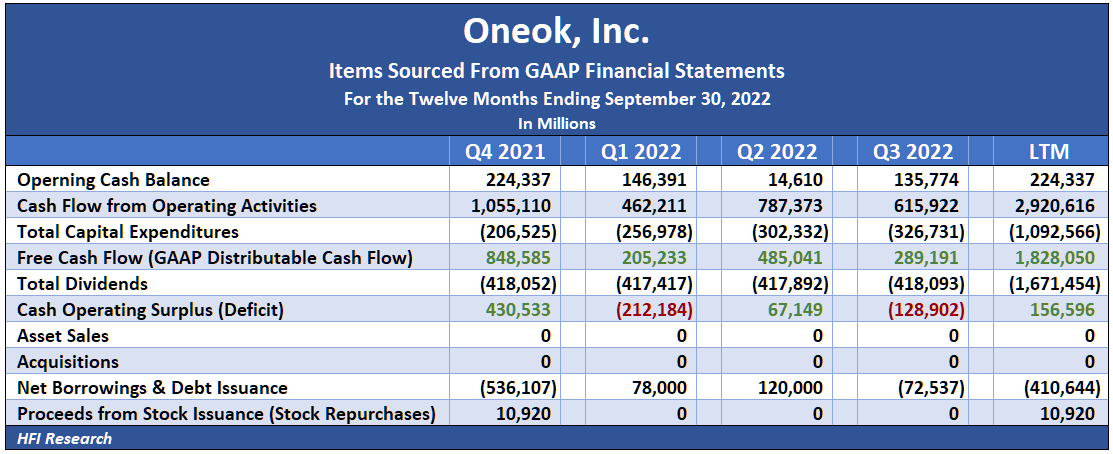

Over the past twelve months, through the end of the third quarter, OKE generated $2.92 billion of operating cash flow. After it spent $1.67 billion on common dividends and $1.09 billion on capital expenditures, the company ended up with a $156 million cash flow surplus. Management allocated the surplus and cash on hand toward reducing leverage.

{kind=link}

The cash flow surplus marks a turnabout from previous years, during which growth capex projects consumed most of OKE’s distributable cash flow, as shown in the chart below.

{kind=link}

While growth projects were a drag on cash flow, they’ve begun to come online. The reduced capex requirements will boost OKE’s distributable cash flow going forward.

Assuming OKE’s new projects generate as strong returns on capital as its other assets—as we suspect they will—the company’s cash flows will get a significant boost from new project income while its capex requirements fall. OKE generates some of the highest returns on capital employed and equity in the midstream sector.

{kind=link}

The figures are similar after asset impairments are accounted for.

OKE’s high returns on capital are a testament to management’s capital allocation skills and the company’s high-quality assets that feature a high-quality growth opportunity set.

Putting Surplus Cash to Work for Shareholders in 2023

Turning to 2023, management’s $4 billion Adjusted EBITDA guidance for 2023 implies operating cash flow of approximately $3.25 billion. OKE pulled forward some capex spending from 2023, so we expect capex to fall from $1.2 billion in 2022 to $1.0 billion in 2023. After $1.7 billion of dividends at their current quarterly rate, OKE will be left with $550 million of surplus cash that it can spend at management and the board’s discretion.

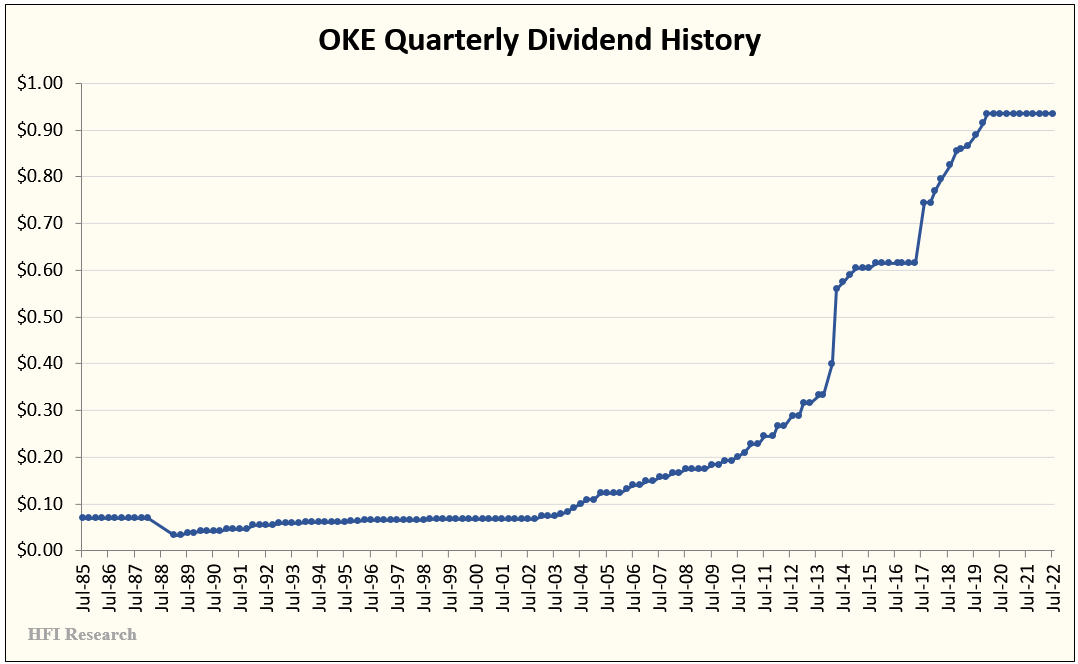

A 5% dividend increase would consume $83.6 million of the $550 million surplus, leaving $466 million to allocate at management’s discretion. OKE’s Adjusted EBITDA growth is likely to organically bring its leverage ratio below management’s target of 3.5 times, so debt reduction will become less of a priority. Management is therefore free to use the cash flow surplus for additional growth projects, share repurchases, or a special dividend of up to $1 per share. Any special dividend could come on top of a 5% increase in the base dividend. The special dividend would be one way of rewarding patient shareholders who have held while OKE took a break from its regular dividend hikes, as shown below.

{kind=link}

Management could also put the surplus cash toward an acquisition, though historically, OKE has eschewed major acquisitions in favor of organic growth. Still, we wouldn’t be surprised to see OKE acquire a Permian G&P to secure additional volumes for its growing downstream business.

Valuation

As much as we like ONEOK, Inc. from the perspective of its management, capital allocation, and return on capital, its shares, at $66, are currently at the high end of our value range of $62 to $66 and above our price target of $64. We therefore maintain our Hold rating.

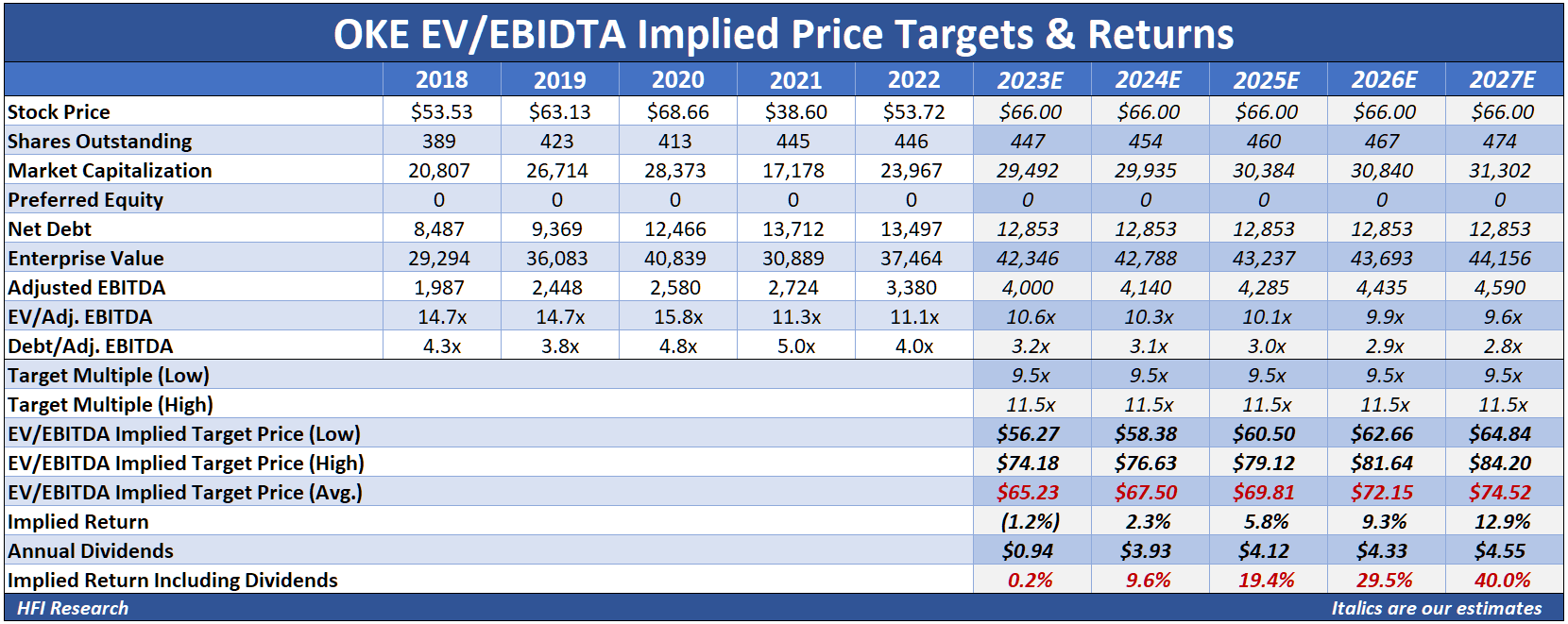

Nevertheless, if the company manages to grow Adjusted EBITDA in the low-single digits and increases its dividend as we expect, its shares offer upside over the next five years. Assuming Adjusted EBITDA grows by 3.5% annually and dividends grow by 5%, our EV/EBITDA valuation for ONEOK, Inc. implies 40% upside through 2027.

{kind=link}

In light of these returns on offer at the current share price, we recommend that current OKE owners continue to hold the shares. Their current 5.7% dividend yield is attractive, while a 5% distribution hike we expect next year will put the yield on today’s price close to 6%.

Conclusion

ONEOK, Inc.’s fourth-quarter earnings may fall short of expectations from the negative impact of the severe weather in December. No doubt its North Dakota and mid-Continent acreage were affected by natural gas well freeze-offs and compressor issues. However, we don’t expect these developments to have a significant negative impact on OKE’s stock because the market is focusing on the company’s bullish 2023 outlook. If the stock does fall below our value range, it may provide investors with an attractive buying opportunity.

Overall, ONEOK, Inc. continues to execute. The company is one of the best-managed midstream operators that owns a collection of top-tier assets. We’d like to own ONEOK, Inc. shares at a lower price. In the meantime, current owners would do well to sit tight over at least the next few years.

For further details see:

ONEOK: Ready For A Dividend Increase In 2023