OKE - ONEOK's Acquisition Of Magellan Bolsters Its Operations And Shareholder Returns

2023-05-16 12:20:44 ET

Summary

- ONEOK, Inc.’s acquisition of Magellan Midstream Partners, L.P. is good for ONEOK shareholders.

- The deal is not as good for Magellan unitholders, but allows for an exit into an attractive combined entity.

- The selloff in ONEOK shares is a buying opportunity.

- We’ll sell our Magellan units and reallocate into other bargain energy income equities.

Midstream investors awoke to the news yesterday morning that another MLP will be exiting the market, as ONEOK, Inc. ( OKE ) announced a deal to acquire Magellan Midstream Partners, L.P. ( MMP ). In the proposed deal, each MMP unitholder will receive $25 in cash and 0.677 shares of OKE stock for each MMP unit they own. The offer came at a 22% premium over MMP's previous day's closing price. OKE expects the deal to close in the third quarter.

The deal values MMP at 11.8 times our estimate of 2024 Adjusted EBITDA. By comparison, we estimate before the announcement, MMP was trading at 10.4 times 2024 EV/Adjusted EBITDA and OKE was trading at 9.7 times 2024 EV/Adjusted EBITDA. MMP's higher multiple reflects its relatively high return on capital, though its multiple has been depressed by the discount its equity receives from being an MLP. Based on our estimate of 2024 free cash flow, the offer price represents an approximately 8.1% distributable cash flow yield on MMP's market cap.

The deal will be fully taxable for MMP unitholders. Management negotiated a large cash component in the deal so that unitholders can fund the tax obligations triggered upon the transfer of ownership.

For OKE, the deal pushes back the impact of the corporate alternative minimum tax until 2027, representing tax savings with a net present value of $1.5 billion. The deal's tax benefits could increase if OKE completes new projects or acquisitions.

We currently hold MMP units but don't own OKE shares. MMP units were one of our first buys on December 13, 2020, for our HFI Research Energy Income portfolio at $46.58. Assuming MMP's current price of $63.00 and the $9.3475 of distributions we have received since our purchase, our MMP investment generated a 55.3% undiscounted total return, or a 19.96% compound annual return.

Since we believe the deal will go through, we plan to sell our MMP units and reallocate the proceeds into various bargain-priced income-generating energy equities.

The Market Penalizes OKE

OKE shares traded down 9.1% yesterday, presumably because MMP doesn't offer OKE appreciable prospects for operational growth funded by capex. Nevertheless, we believe the deal is attractive for OKE.

We've seen all too often that in midstream that operational growth fails to translate into highly profitable net income or free cash flow growth. But MMP is a unique operator. Its assets have an important feature most midstream assets lack, namely, pricing power . So while MMP's assets may not be a suitable destination for OKE's marginal growth capex dollar, their pricing power is all but certain to contribute many years of growth to OKE's EBITDA and cash flow at very low risk to shareholder returns.

MMP's pricing power was most recently on display in the company's first-quarter 2023 earnings report on May 4, where it disclosed its refined product transportation rates were set to increase by an average of 11% beginning on July 1, 2023. The rate hike is the largest in a long succession of annual rate hikes.

MMP's pricing power derives from the entrenched position enjoyed by its irreplaceable refined product pipeline assets, which limits competition from other pipelines. The regularity with which it has boosted rates indicates that its high return on capital is sustainable. It also means that its assets are protected from the impact of rising inflation. In an inflationary environment, MMP's assets will generate higher revenues coupled with minimal capex requirements and low operating expenses. As a result, a greater proportion of revenue can drop to the bottom line.

Operational Diversification Also Benefits OKE

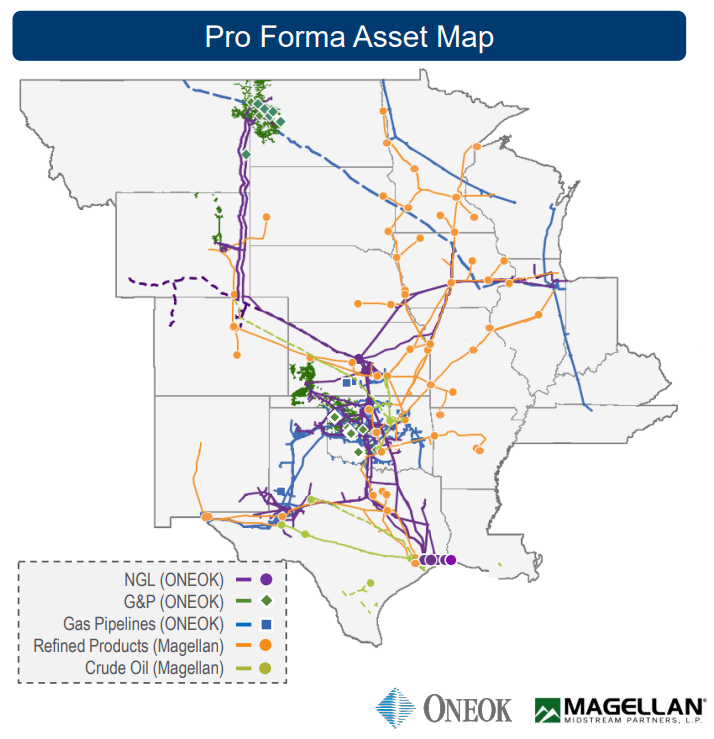

In addition to offering OKE low-risk growth, the deal complements OKE geographically, with MMP's and its own midstream system spanning the midsection of the U.S.

{kind=link}

Source: ONEOK Magellan Midstream Partners Acquisition Presentation , May 14, 2023.

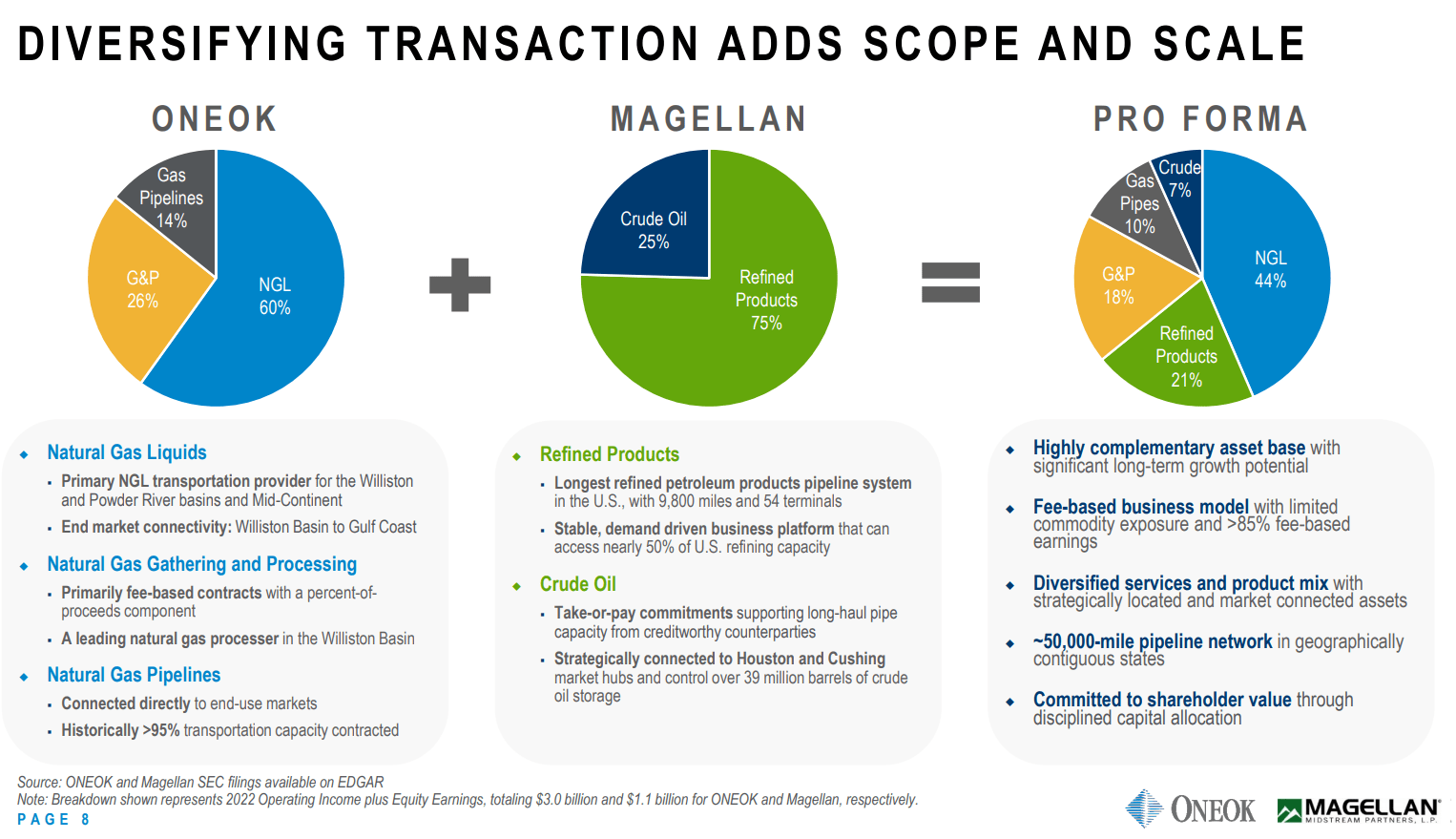

The deal brings desirable diversification to OKE's operations. The company will extend its gathering and transportation capabilities outside its legacy natural gas and NGLs markets and into crude oil and refined products.

{kind=link}

Source: ONEOK Magellan Midstream Partners Acquisition Presentation, May 14, 2023.

Increased operational diversification should allow OKE to increase its service offerings to customers, but it will also increase the stability of the company's cash flow. Furthermore, MMP's stable refined product throughput volumes will make the combined entity's cash flows less prone to energy market cyclicality.

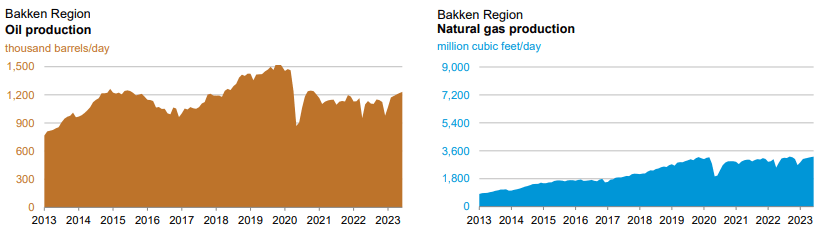

The main knock against OKE from long-term shareholders is its NGL transportation system's overreliance on Bakken volumes. Bakken oil and gas production has entered a mature phase of its life cycle. Over the next few years, the basin's oil, NGL, and natural gas production is likely to plateau and then decline.

{kind=link}

Source: EIA, May 2023 Drilling Productivity Report .

Declining Bakken volumes would adversely impact OKE's financial results. Since OKE's Bakken and Midcontinent NGL system is the main source of its mid-teens return on capital - which ranks among the highest in midstream - and, by extension, its stock's premium valuation multiple, management would be prudent to address the looming prospect of Bakken production declines as soon as possible. By acquiring MMP's assets, which are characterized by indefinitely long useful lives, OKE can allay shareholder concerns regarding Bakken declines.

Lastly, the addition of MMP assets will boost OKE's systemwide return on capital. OKE possesses one of the few management teams in midstream that has consistently excelled in capital allocation, so we expect the MMP assets to retain their high-return profile in the hands of OKE's capable management.

An MMP Unitholder's Perspective on the Deal

If you're a long-term MMP shareholder like we are, you might find it difficult to part with such attractive assets and high-caliber management. We considered our MMP investment to have an indefinite holding period, over which we expected increasing distributions. We don't share concerns that MMP's assets will fall out of use due to an energy transition, and we consider MMP management among the best capital allocators in any cyclical, capital-intensive industry. If MMP remained independent, we were confident that its units would generate strong returns for unitholders for many years to come.

While we'd prefer MMP to remain independent, we have to face the reality that the midstream sector will consolidate, and MMP is among the most attractive acquisition candidates for the largest operators. So while we find the deal's price to be lower than we would have liked in an acquisition scenario, we expect it to gain approval from OKE shareholders, MMP unitholders, and regulators. Consequently, we plan on selling our units and reallocating the proceeds into one of the many discounted income-generating energy equities.

As for the arbitrage opportunity the deal currently offers, prospective returns will depend on the course of OKE's stock price. With OKE trading at around $58 and MMP at $63, the deal's consideration, combined with MMP's August $1.0475 distribution, bring the undiscounted prospective return over the next six months to 2.8%. We believe the odds are better than 80% that the deal will be approved and that it will close in the third quarter. The primary risk to the deal stems from OKE shareholders' failure to approve it. In that scenario, MMP would fall back to its pre-deal level of $55, or perhaps slightly higher, as the deal highlights MMP's substantial value to an acquirer.

In light of the slim return on offer and the slight risk that the deal fails, we don't believe the current premium offers sufficient compensation for unitholders looking for a low-risk arbitrage return. But that could change if MMP's unit price remains subdued and OKE's stock rallies over the coming weeks.

Pro Forma Financials for the Combined Entity

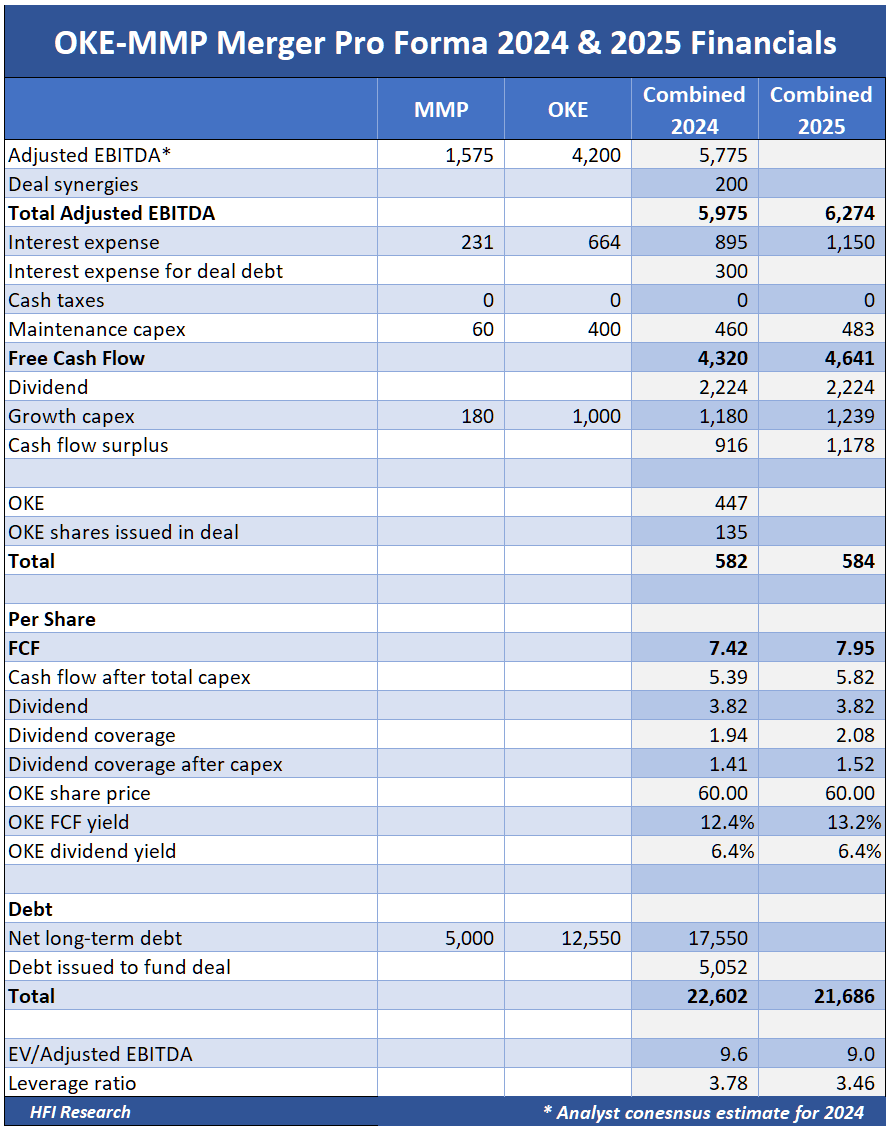

OKE reported in the deal's press release that it will be accretive to earnings per share in 2024 and deliver an additional 3%-to-7% boost from 2024 through 2027. Management expects synergies of approximately $200 million. It also expects OKE to end 2024 with a leverage ratio of approximately 4.0 times.

The following table shows our pro forma estimates for the combined entity for 2024 and 2025. We believe leverage will end 2024 at 3.8 times, lower than management's estimate. The combined entity is trading at an EV/EBITDA of 9.6 times for 2024 and a free cash flow yield of 12.4% on its market cap at $60 per share.

{kind=link}

At OKE's current price of $60, the combined entity's equity is being priced at a discount to OKE's recent historical average EV/EBITDA, which is in the range of 11-to-12 times. The addition of MMP's assets should boost its EV/EBITDA multiple due to MMP's significantly higher return on capital. In fact, if we assume EBITDA grows by 5% from 2024 to 2025 and that the company allocates all of its 2024 cash flow surplus toward paying down debt, at $60 per share, the combined entity's EV/EBITDA falls to a historically low 9 times in 2024.

HFI Research

If the combined entity traded at an 11 times multiple, OKE shares would trade at $74 in 2024 and $81 in 2025. Clearly, OKE shares are too cheap in the neighborhood of $60 per share. The company offers steady growth and stable cash flow. We rate the shares as a Buy with a price target of $66. We believe our price target is conservative, taking into consideration the slight probability that the deal fails and the attractive prospects for the combined entity.

MLPs Are Too Cheap

The 22% premium paid in this nearly $19 billion deal is a testament to the undervaluation that exists in the MLP space. Midstream oil and gas MLPs are cheap relative to every other stock market segment, particularly in light of the high quality of their cash flows.

The sector's discount isn't attributable to poor fundamentals. Full-year 2022 results for MLPs were strong. First-quarter 2023 results were arguably the strongest among the oil and gas sub-sectors.

Investors have grown accustomed to criticizing the MLP entity and its associated trading discount in the market. But companies like MMP have used that discount to their unitholders' advantage by repurchasing large quantities of units at bargain prices. The 11.5% reduction in MMP's unit count that has occurred since the end of 2019 boosted unitholders' returns from this acquisition.

Conclusion

The Magellan Midstream Partners, L.P. acquisition is a good deal for ONEOK, Inc. shareholders. We believe the selloff in OKE shares presents an attractive long-term buying opportunity. The OKE that will emerge from this deal will have greater scale and diversification. It will have a return on capital and cash flow stability on par with the highest-quality midstream operators. In fact, its return on capital will far and away be the highest among its peers and among the highest in the midstream sector.

While the deal is not as good for MMP unitholders, it provides them with an exit into a high-quality combined entity. For MMP investors seeking to remain in the MLP space, we recommend Enterprise Products Partners L.P. ( EPD ) and MPLX LP ( MPLX ) as two midstream operators with operational and financial stability on par with MMP. Their distribution safety, distribution yield, inflation resistance, and distribution growth prospects make them appealing alternatives to MMP.

We look forward to snatching up some high-quality bargains with the proceeds from our MMP unit sale. With investor sentiment toward the energy sector in the dumps, equity valuations are depressed and energy income investors are spoiled for choice. Fundamentals are on the upswing in both oil and natural gas, and we believe now is a good time to buy.

For further details see:

ONEOK's Acquisition Of Magellan Bolsters Its Operations And Shareholder Returns