OKE - ONEOK: Strong Cash Flow Outlook For 2023 Boosted By One-Time Insurance Payout

2023-04-30 04:42:16 ET

Summary

- ONEOK could provide a high dividend yield of about 6% and long-term dividend stability of over 25 years.

- The increase in OKE's adjusted EBITDA from the insurance payout would positively impact the improvement of operating cash flow, which would then be reflected in free cash flow in 2023.

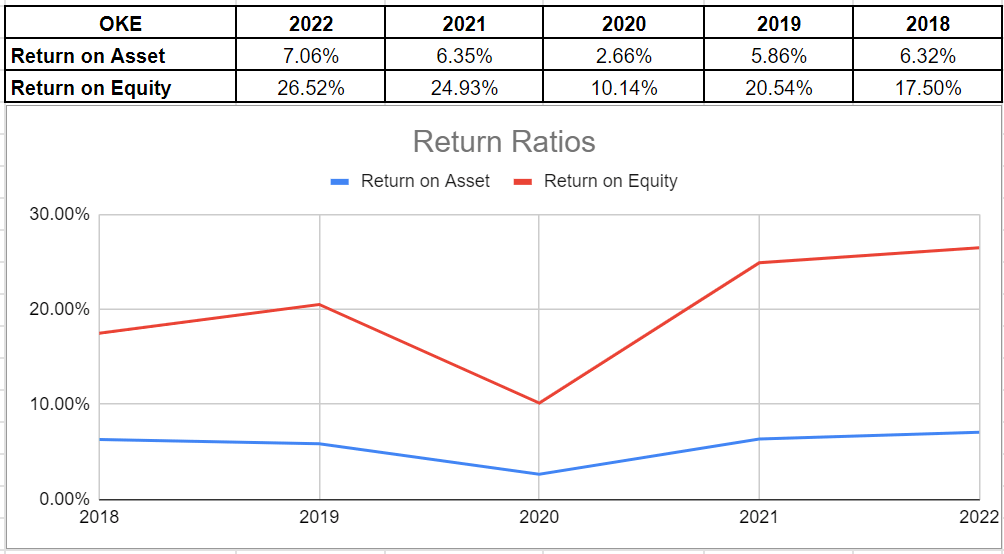

- In 2022, OKE achieved its highest percentage of ROA ratio compared to previous years, landing at 7.06%. Also, its ROE ratio was considerably high at over 26.5% last year.

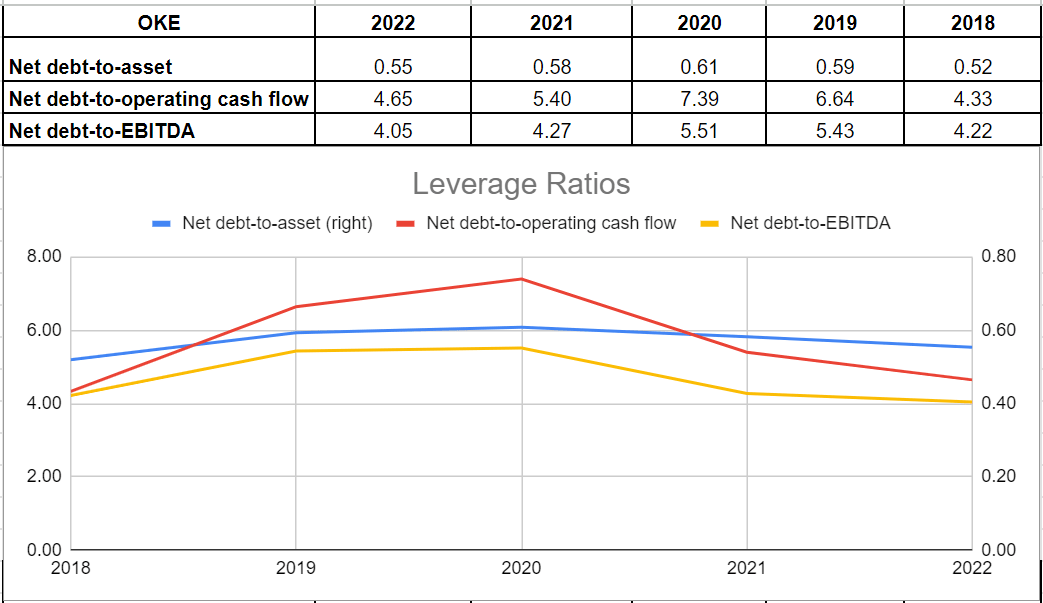

- The net debt-to-EBITDA and net debt-to-operating cash flow both decreased to 4.05x and 4.65x, respectively at the end of 2022, from 4.27x and 5.4x, respectively in 2021.

Introduction

ONEOK ( OKE ) is a top-tier midstream service provider that boasts ownership of one of the most exceptional natural gas liquids systems in the United States. With approximately 10% of U.S. natural gas production relying on ONEOK's infrastructure, the company offers midstream services to producers, processors, and customers, and is a significant supplier of NGLs to the petrochemical industry. In 2022, ONEOK demonstrated a robust financial structure and is expected to reap significant benefits from its insurance payment in 2023. Consequently, I recommend buying shares in ONEOK.

ONEOK’s performance and 2023 outlook

In 2022 , OKE demonstrated a robust cash and capital structure. The company could meet its 2022 guidance midpoint and achieve an impressive $967 million adjusted EBITDA in 4Q 2022, which is over 14% higher year-over-year compared with 2021. The major part of this boost was driven by higher natural gas and NGL volumes, higher average fee, and storage rates.

Additionally, ONEOK generated over $2.9 billion in operating cash flow, resulting in a substantial free cash flow of $1.7 billion during 2022. As a result of this financial performance, it is not surprising to see that OKE could provide a high dividend yield of about 6% and long-term dividend stability of over 25 years. The company paid a $3.76 dividend per share in 2022, which brings a dividend cost of about $1.7 billion per year, given their latest number of outstanding common shares of 447.2 million.

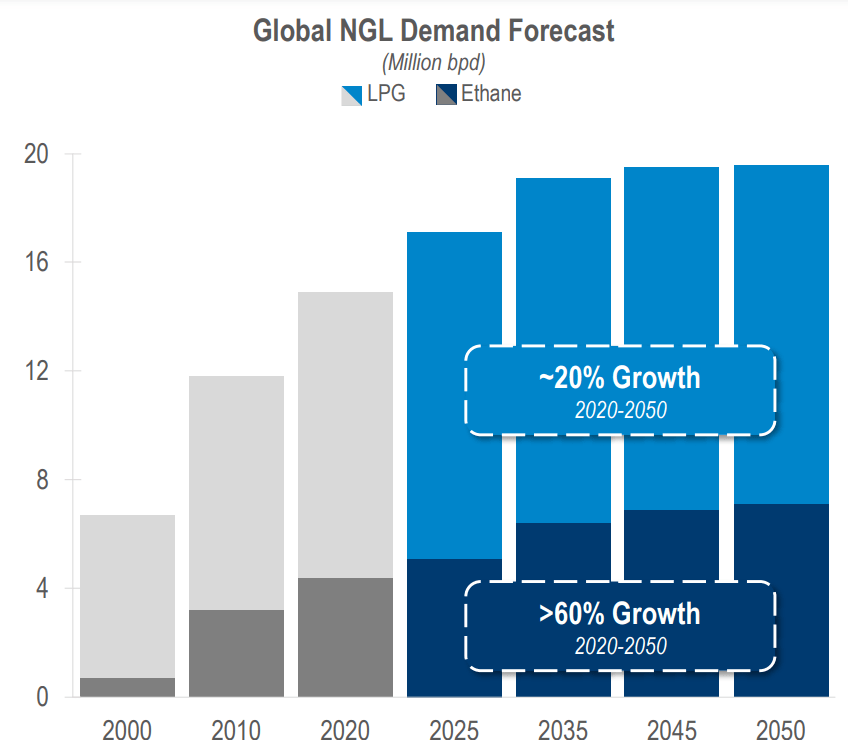

Looking ahead to 2023, OKE plans to keep its capital expenditures almost unchanged at $1010-$1190 million. Moreover, the company anticipated boosting its adjusted EBITDA to $4.4 billion to $4.7 billion in 2023. It's worth mentioning that $830 million of this increase is derived from a one-time insurance settlement gain. Overall, based on the 2023 guidance, the most portion of adjusted EBITDA is devoted to Natural Gas Liquids segment, about $2.9 billion. The company plans to increase its natural gas and NGL volumes from producer activities and expects its NGL earnings to be over 90% fee-based from inflation-based escalators. When looking ahead, it goes with no surprise that the global NGL demand is anticipated to grow by about 20% in Liquified Petroleum Gas (LPD) and over 60% in Ethane by 2050 (see Figure 1). The main NGL demand drivers are petrochemical products like health care products, residential uses, and transportation fuels. When all was said and done, ONEOK’s boost in adjusted EBITDA would affect a similar improvement in operating cash flow. Thus, a well amount of the company’s operating cash flow will be translated to free cash flow in the following year.

Figure 1 – Global NGL demand forecast

{kind=link}

ONEOK’s investor presentation as of April 2023

Furthermore, ONEOK’s financial strength is evident in its improved return and leverage metrics. The company has demonstrated its ability to generate profits and effectively utilize its assets, reassuring investors of its financial health. Notably, OKE’s revenue jumped by 35% from $16.5 billion at the end of 2021 to over $22.3 billion in 2022. Additionally, the company's investments in high-return organic projects and flexibility to grow at the same pace of demand will pave the way for further revenue and income growth in the upcoming years. Therefore, it would be prudent to examine OKE’s return ratios to assess its ability to provide profit.

After witnessing a promising increase in net income generation, from $15 billion in 2021 to $17.2 billion in 2022, it comes with no surprise that OKE has achieved well-improved return ratios. These ratios are indicative of the company's ability to generate returns for its shareholders. The ROA ratio measures the profit generated by the company for each dollar of its assets. In 2022, OKE achieved its highest percentage of ROA ratio compared to previous years, with a boost of 71 bps and landing at 7.06%, up from 6.35% at the end of 2021. Similarly, its ROE ratio was considerably high at over 26.5%, up from the previous level of 24.9% in 2021. The ROE ratio is crucial as it calculates the rate of return on capital invested in the business by shareholders. Overall, ONEOK’s impressive return ratios demonstrate its capability to generate cash and reduce dependency on debt financing (see Figure 2).

Figure 2 – ONEOK’s return ratios

{kind=link}

Author's calculations

ONEOK’s net debt level remained relatively stable, with only a slight decrease from $13.7 billion in 2021 to $13.5 billion in 2022. However, ONEOK’s increase in adjusted EBITDA is expected to significantly reduce the net debt level in 2023. Albeit a great extent of the excess is due to the one-time insurance payment, the company’s guidance to increase its natural gas and NGL volumes and earnings from long-term contracts would decrease its leverage even after the boost of 2023.

The net debt-to-EBITDA and net debt-to-operating cash flow both decreased to 4.05x and 4.65x, respectively, at the end of 2022 from 4.27x and 5.4x, respectively, in 2021. This is noteworthy as the company has targeted a debt-to-EBITDA ratio of 3.5x for this year. Furthermore, OKE’s net debt-to-asset ratio slightly decreased from 0.58x in 2021 to 0.55x at the end of 2022. This indicates that growth strategies and capital expenditures during the year have set a foundation for further growth and cash generation in the following year.

As a result of these positive developments, shareholders can expect continued deleveraging and growth in the coming year, leading to lower financing risks and higher distributions. This should also translate into a higher market share price for ONEOK (see Figure 3).

Figure 3 – ONEOK’s leverage ratios

{kind=link}

Author's calculations

Risks

Despite ONEOK's strong financial statements, investors must remain aware of potential risks that could threaten the company's operations in the future. One significant risk is related to natural gas and crude oil production of third-parties. As drilling naturally diminishes over time , it is likely that the company's revenue and cash flow will also decrease. Additionally, environmental, social, and governance ((ESG)) issues such as climate change are becoming increasingly important to investors. These factors may affect regulations and technologies that aim to reduce demand for hydrocarbon products and replace them with more environmentally-friendly energy sources. Consequently, these changes may reduce demand for ONEOK's services and increase their costs in the future. Furthermore, ONEOK's production involves expanding existing or constructing new pipelines, processing and storage facilities. These issues may bring risks of participating in projects that require significant capital expenditures while their revenue may not increase immediately. Additionally, these projects may increase labor force demand which could be difficult due to supply chain constraints.

Conclusion

After analyzing ONEOK's financial results for 2022 and reviewing their guidance for 2023, it is clear that the company is performing well and has the capability to continue its operations. The company's return ratios have improved due to increased net income and revenues in 2022, while also decreasing their leverage ratios. However, it is important to note that ONEOK's boost in 2023 is primarily due to a one-time insurance payout from the Medford incident. While this may partially eliminate in 2024, the company's solid financial structure leads me to believe that OKE stock is a good investment opportunity.

For further details see:

ONEOK: Strong Cash Flow Outlook For 2023 Boosted By One-Time Insurance Payout