ONEW - OneWater Marine: Guidance And The Electric Boat Market Imply Undervaluation

2023-05-24 15:10:02 ET

Summary

- OneWater Marine is one of the largest marine products retail distribution companies in the United States.

- I believe that the numbers delivered for the year 2023 are beneficial. Management is expected to deliver an EBITDA of close to $200-$225 million and EPS close to $7.5-$8.

- The expertise of management, the diversified product portfolio, previous acquisitions, and new motorized boats market growth could imply significant FCF generation in the coming years, in my view.

OneWater Marine Inc. ( ONEW ) expects 2023 EBITDA close to $200-$225 million and EPS close to $7.5-$8 per share. I also believe that the expertise of management could bring surprising FCF growth. Besides, further investments in the global electric boat market, which exhibits double-digit growth, could bring substantial revenue growth enhancement. There are risks from M&A failures, competition, or lack of acquisition targets, but I still believe that the company could trade at higher marks.

Business Model And Guidance

OneWater Marine is one of the largest marine products retail distribution companies in the United States, currently made up of 96 dealerships, 12 distribution centers, and multiple online sales channels. The concessionaires are located mainly in the Southeast, Gulf Coast, Mid-Atlantic, and Northeast regions, allowing them to access strategic markets, where the consumption and need for this type of product prevail.

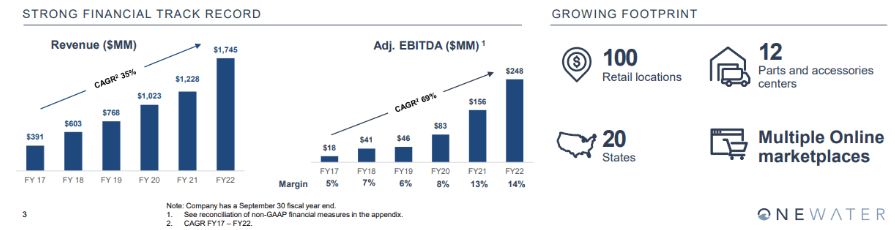

I believe that the recent revenue growth of close to 35% CAGR and Adjusted EBITDA growth of around 69% CAGR are great reasons to execute due diligence on this name .

{kind=link}

I also believe that the recent acquisitions and M&A strategies are worth a few comments. The company recently acquired T-H Marine Supplies and Ocean Bio-Chem, which not only allows it to capture a portion of the related market but also to add valuable products to its portfolio, specifically in terms of parts and accessories.

Since the acquisition of Ocean Bio-Chem, the company's structure was reformulated, and its activities are currently divided into two reportable segments: concessionaires and distribution. The first of these is made up of the 96 OneWater Marine concessionaires in the United States and represents approximately 92% of the company's annual revenue. Some of the relevant data regarding the operation of this segment is that, during the year 2022, more than 10,500 boats were sold, new as well as used, which come from its agreements with more than 50 manufacturers, providing it the possibility to offer more than 70 boat brands in its catalogs. This segment also offers coverage or financing services for maritime activities, repair and maintenance of boats, sale of parts and accessories, and in some regions mooring or storage spaces.

The distribution segment, which comprises the remaining 8% of OneWater Marine's annual profits, is made up of the activities of three businesses that are wholly owned by the company. These operations are based on the manufacturing, assembly, and distribution of maritime products that are sold to distributors, retail outlets, or direct consumers through online sales channels.

To understand the position and growth of OneWater Marine, it is good to look at the data on the nature of the marine products market. For the year 2021, the operations of related products were calculated at $56.7 trillion dollars, being a number 12% higher than that in the previous year. For the same year, sales of new motorized boats were estimated at $15.4 billion in total, resulting in a 12% annual growth since 2010. Considering the growth of the market, I believe that OneWater Marine is operating in a beneficial environment.

The global electric boat market was valued at $5.0 billion in 2021, and is projected to reach $16.6 billion by 2031, growing at a CAGR of 12.9% from 2022 to 2031. Source: Electric Boat Market Size, Share, Analysis, Trends by 2031

I also believe that the numbers delivered for the year 2023 are beneficial. The company is expected to deliver an EBITDA close to $200-$225 million and EPS close to $7.5-$8 per share.

The Company is maintaining its previously issued fiscal full year 2023 outlook. For fiscal full year 2023, OneWater anticipates same store sales to be flat to up mid-single digits. Adjusted EBITDA is expected to be in the range of $200 million to $225 million and earnings per diluted share is expected to be in the range of $7.50 to $8.00. Source: Quarterly Results

Balance Sheet

In the last quarterly report, the company reported an impressive increase in the total amount of assets driven by an inventory increase. Considering the increases in prices reported by the company in the last quarterly earnings and recent inventory growth, I believe that we could expect revenue sales growth in the coming months.

As the industry continues to return to historical seasonal cycles with more normalized pricing and inventory levels, we will utilize our robust sales platform and inventory management tools to continue to outperform the industry, gain market share and create value for our shareholders. Source: OneWater Marine Inc. Announces Fiscal Second Quarter 2023 Results

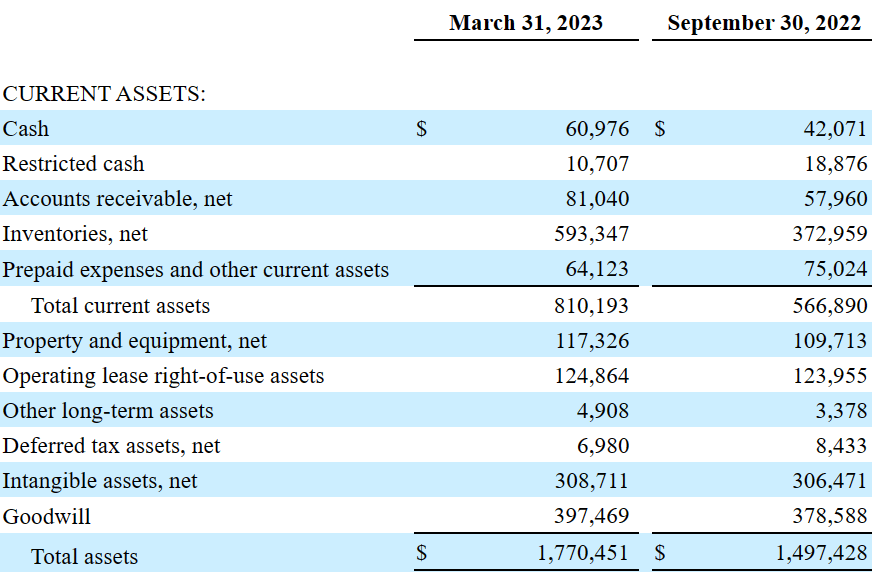

As of March 31, 2023, the company reported cash worth $60 million, restricted cash worth $10 million, and accounts receivable of $81 million. Inventories were equal to $593 million, with prepaid expenses and other current assets of $64 million. Total current assets were worth $810 million.

Property and equipment stood at $117 million, with operating lease right-of-use assets of $124 million, other long-term assets of $4 million, and intangible assets of $308 million. Finally, with goodwill of $397 million, total assets stand at $1.770 billion.

OneWater Marine Inc. Announces Fiscal Second Quarter 2023 Results

{kind=link}

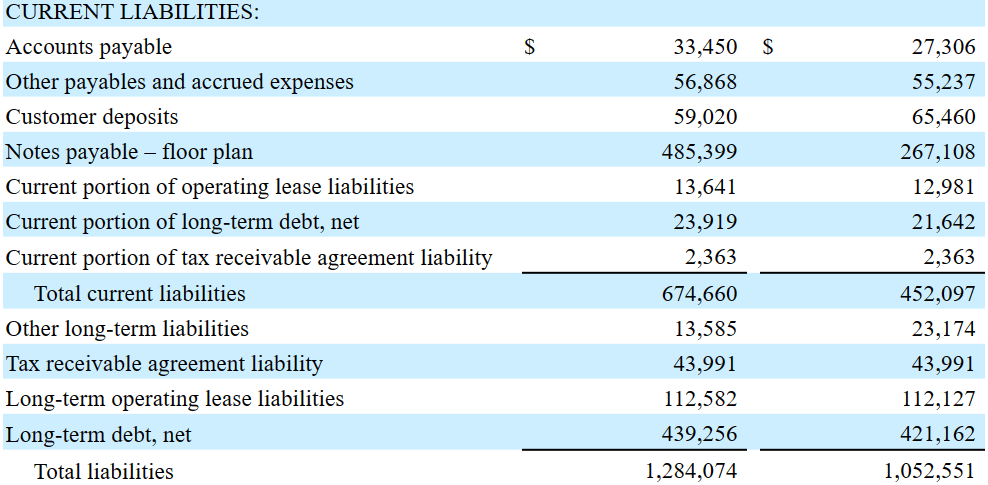

The list of liabilities includes accounts payable worth $33 million, other payables and accrued expenses around $56 million, customer deposits of $59 million, and notes payable of close to $485 million. Also, with a current portion of long-term debt of close to $23 million, total current liabilities stood at $674 million, lower than the total amount of current assets.

The balance sheet also included other long-term liabilities worth $13 million, tax receivable agreement liability of close to $43 million, and long-term debt close to $439 million. In sum, total liabilities stood at $1284 million, which implied an asset/liability ratio of 1.37x.

OneWater Marine Inc. Announces Fiscal Second Quarter 2023 Results

{kind=link}

A Lot Of Competition

Competition is given by boat manufacturers and sellers as well as the recreation industry in general. This generates a highly competitive market with high levels of fragmentation. MarineMax ( HZO ) and Bass Pro Shops are the two companies of big size that compete with OneWater, in addition to a large number of regional distributors that have only two or three stores on their property.

There is also competition from manufacturers of accessories and related products, which, in many cases, have greater resources and infrastructure than One Water Marine. Ultimately and to a lesser extent, the company has as competitors certain online sales channels, especially with regard to used boats.

DCF Model

Under my financial model, I assumed that the experience accumulated by management will continue to offer innovative ideas in the industry, which will most likely bring revenue growth and EBITDA growth.

{kind=link}

With regards to my previous words about management, I would be expecting further growth like we saw in the most recent quarter. In my view, if the team can deliver such quarterly figures, we may see similar figures in the future.

Our team once again showcased its ability to execute in a dynamic environment, delivering a 19% growth in sales during the quarter, on top of a 34% increase in the prior year period. Same store sales grew 11% year-over-year driven by a balance of unit and price increases. Additionally, our higher margin service, parts and other sales grew 28% in the quarter. Source: OneWater Marine Inc. Announces Fiscal Second Quarter 2023 Results

I also think that the diversified product portfolio offered by OneWater will most likely interest investors. As a result, the company will be able to finance its operations at good conditions, which will likely have a beneficial impact on the stock valuation. Let's note that management believes that unifying a significant number of brands will most likely bring economies of scale and cash flow generation.

{kind=link}

In my view, the growing amount of customer data available and defined interests from customers also appear quite valuable. If marketing professionals inside the organization can make good use of this data, I believe that revenue growth could increase in the coming years.

I want to also add the acquisition strategy, which has been very successful for OneWater Marine. The company integrated new businesses and brands from targets into its own business, but keeping the names, which, in my view, is a wise decision. Let's keep in mind that the maritime products market is largely based on the recognition and tradition of certain companies that were born as family businesses. From its founding to date, OneWater Marine has managed to incorporate 72 dealerships and 12 distribution centers through its acquisitions.

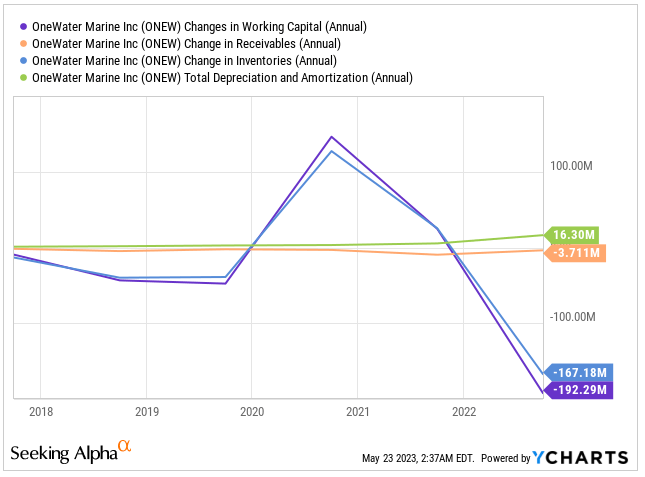

For the financial model of OneWater Marine, I didn't really think out-of-the-box. I checked the changes in working capital, changes in receivables, changes in inventories, and depreciation and amortization reported in the past. My figures are pretty much aligned with the figures seen in previous cash flow statements.

{kind=link}

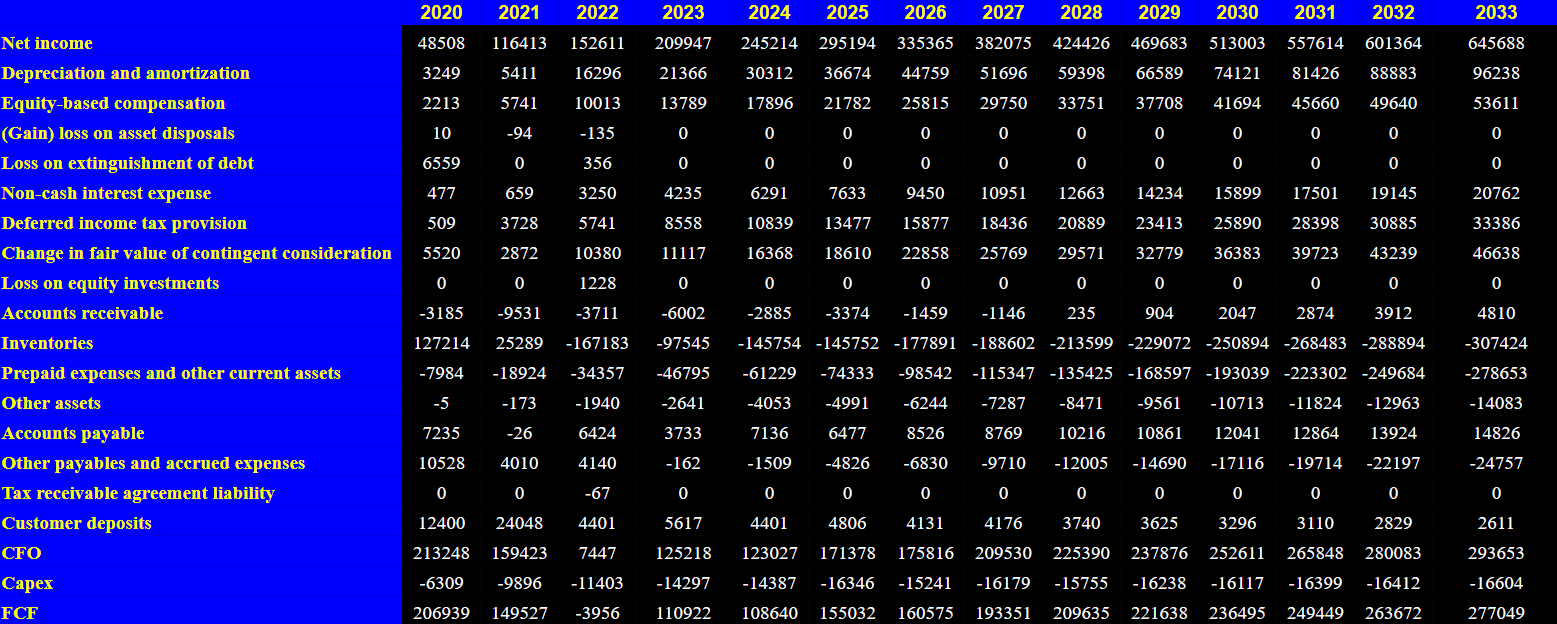

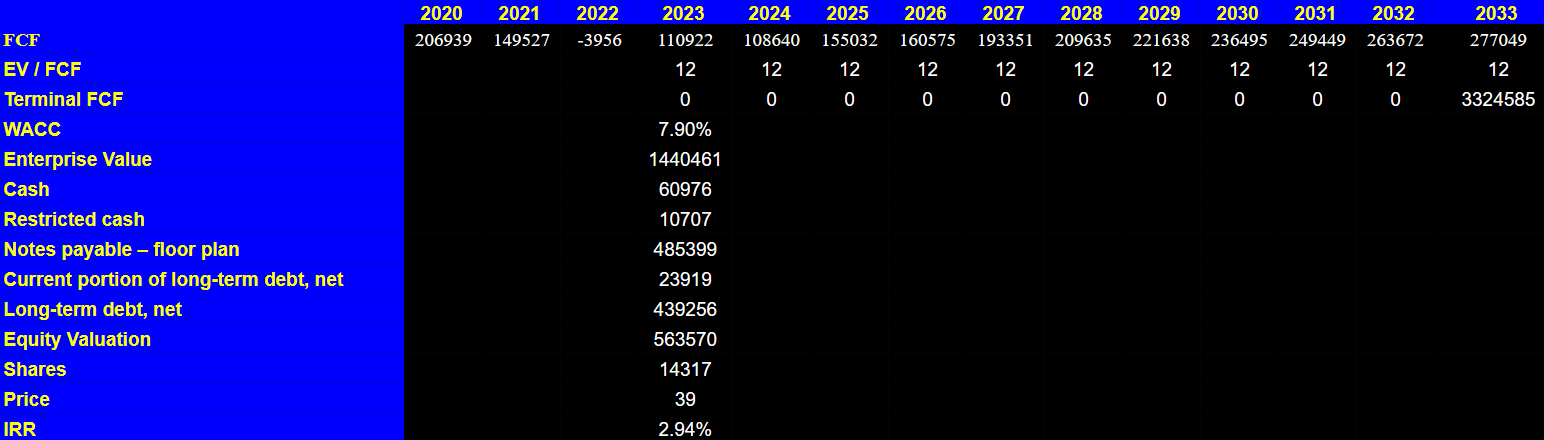

My cash flow model includes 2033 net income of $645 million with depreciation and amortization close to $96 million, equity-based compensation of around $53 million, and changes in accounts receivable of $4 million.

Also, with changes in inventories worth -$308 million, prepaid expenses and other current assets of -$279 million, and changes in accounts payable of $14 million, I included 2033 capex of -$17 million. In sum, 2033 FCF would be close to $277 million.

{kind=link}

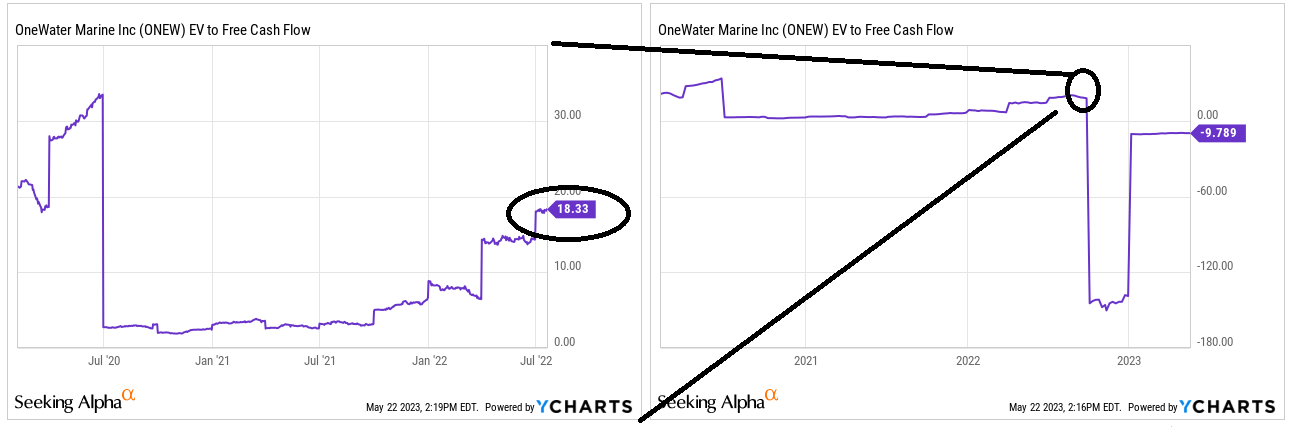

OneWater traded at close to 30x-4x FCF in the past, so I believe that a multiple of 12x appears quite conservative. By assuming a WACC of 7.9%, I obtained an enterprise value close to $1.44 billion.

{kind=link}

If we add cash of $60 million, $10 million in restricted cash, notes payable worth $485 million, current portion of long-term debt around $23 million, and long-term debt of $439 million, the equity valuation stands at close to $563 million. Finally, the implied valuation would stand at close to $39 per share.

{kind=link}

Risks

First of all, OneWater Marine suffers from heavy reliance on its manufacturers. 10 main reference brands accounted for more than 45% of sales in the last three years. Specifically, Malibu Boats ( MBUU ), through its brands, accounted for approximately 15% of total sales in the same period. Any disruption in the supply and distribution chain of its manufacturers as well as the rupture or inability to retain ongoing commercial agreements are high risk factors for the company's growth and operations.

In addition to the high competition that comes from the concessionaires and the recreation industry in general, the boat market is marked by a high seasonality over the summer months, which complicates the real projection of certain parameters into the future. Also, worth consideration are the variation in fuel prices and interest rates at the national level, which may affect the company's operations.

Ultimately, we can add that the inability to integrate future acquisition models into the current business model can be a complication for OneWater Marine. If accountants have to impair the goodwill accumulated, I believe that we may see a decrease in the book value per share, which may lead to stock price declinations. Besides, management might not find targets at ideal valuations, which might lower inorganic growth, and may lead to revenue growth declines.

Conclusion

OneWater Marine delivered beneficial quarterly results and optimistic 2023 guidance. The diversified product portfolio, previous acquisitions, and new motorized boats market growth could imply significant FCF generation in the coming years. I believe that OneWater Marine could be trading at much more than the current price mark. Even taking into account risks from competition, failed M&A, or lack of acquisition targets, in my view, the company remains undervalued.

For further details see:

OneWater Marine: Guidance And The Electric Boat Market Imply Undervaluation