HZO - OneWater Marine: Poor Growth Priced In Already Could Likely Lead To Long-Term Upside

2023-08-23 04:27:22 ET

Summary

- OneWater's shares dropped almost 30% after the Q3 earnings report because of a guidance lowering.

- Although the new guidance is bad, the share price already reflects this, and now it could be an opportunity.

- The fragmented market in the boat industry offers an attractive opportunity for long-term growth.

Editor's note: Seeking Alpha is proud to welcome Gustavo Larraga Tapia as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Shares of OneWater Marine (ONEW) plunged nearly 30% after cutting guidance in its latest quarterly report. However, it seems that the current price already discounts a negative scenario, making it a potentially favorable starting point for obtaining good long-term returns.

History

The company was founded as Singleton Marine in 1987 and during the 1990s, the company focused on organic growth, opening new locations on various lakes in Atlanta. It wasn't until the recession hit in 2008 that the current CEO, Austin Singleton Jr., realized that many dealerships were operating without succession plans. Numerous owners were relying on their children, nephews, and grandchildren to run the family business. However, when that approach didn't work, they found themselves with no options to continue the business. Thus, the recession acted as a catalyst for small business owners to seek a way out. In 2008, Singleton Marine began its growth through mergers and acquisitions.

This strategy is one that is quite common in small companies within fragmented industries: maintaining the brand, retaining staff, removing responsibilities from exiting owners, and placing them in less time-intensive positions, such as maintaining interpersonal relationships within their work area. This approach generates sales and leaves a decentralized structure, similar to Warren Buffett's style with Berkshire Hathaway.

As I mentioned, this understanding of the strategy gives us insight into the philosophy that guides the business's operations and provides an idea of what we could expect from ONEW.

Business Model

"OneWater operates as a recreational boat retailer in the United States. The company offers new and pre-owned recreational boats and yachts, as well as related marine products, such as parts and accessories. It also provides boat repair and maintenance services. In addition, the company arranges boat financing, insurance and other ancillary services, including indoor and outdoor storage." Source: Business description by Seeking Alpha .

Used boats, parts, and maintenance played a crucial role in my decision to write about OneWater. The new yacht and boat segment tends to be quite cyclical. However, similar to cars, during a recession or economic slowdown, buying used boats and yachts becomes the preferable option for consumers. This preference for used options often leads to increased demand for repairs and maintenance services for these boats and yachts.

Revenue Distribution

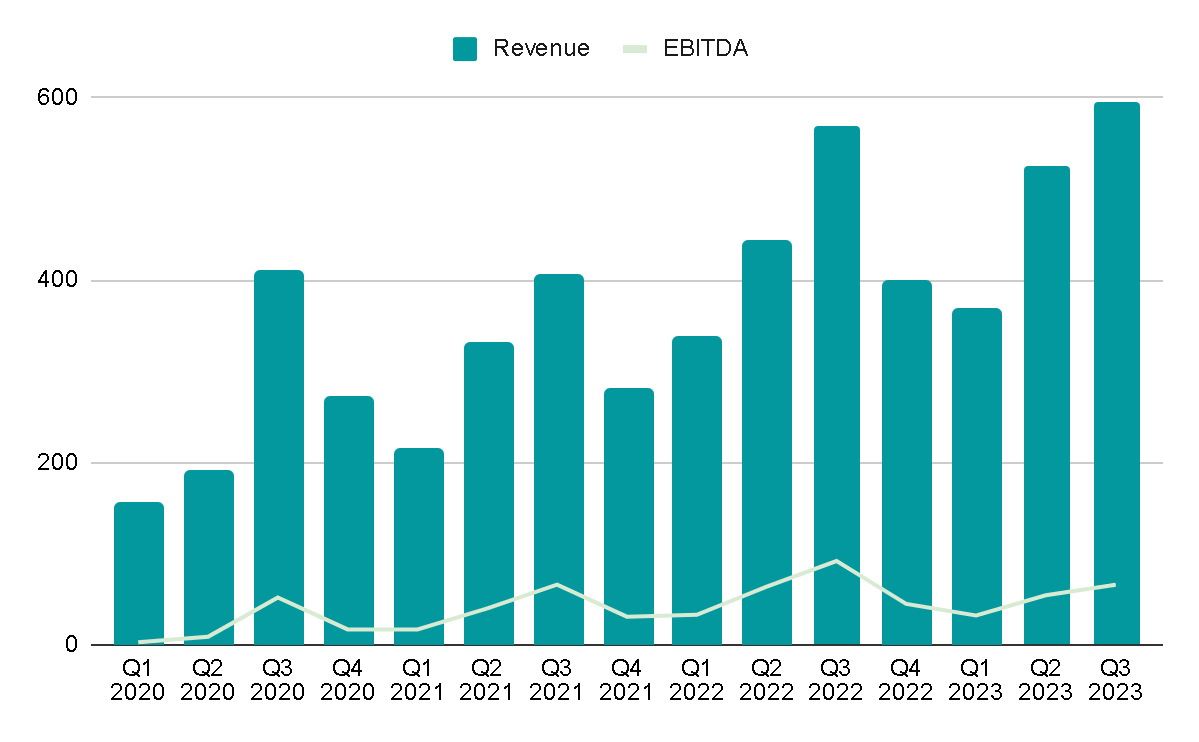

The business exhibits significant seasonality. During the autumn and winter months (Q4 and Q1 of the company), sales volumes are lower, as most yachts are typically used during the spring and, especially, the summer (Q2 and Q3). The following graph perfectly illustrates this pattern:

Quarterly Revenue (Author's representation)

{kind=link}

While sales exhibit seasonality, noteworthy growth trends can still be observed. For instance, between Q4 2022 and Q4 2021, there was a year-over-year growth of 42%, even though it was one of the weaker quarters. This growth trend is also evident in the comparison between Q3 2023 and Q3 2022, with a growth of 4%.

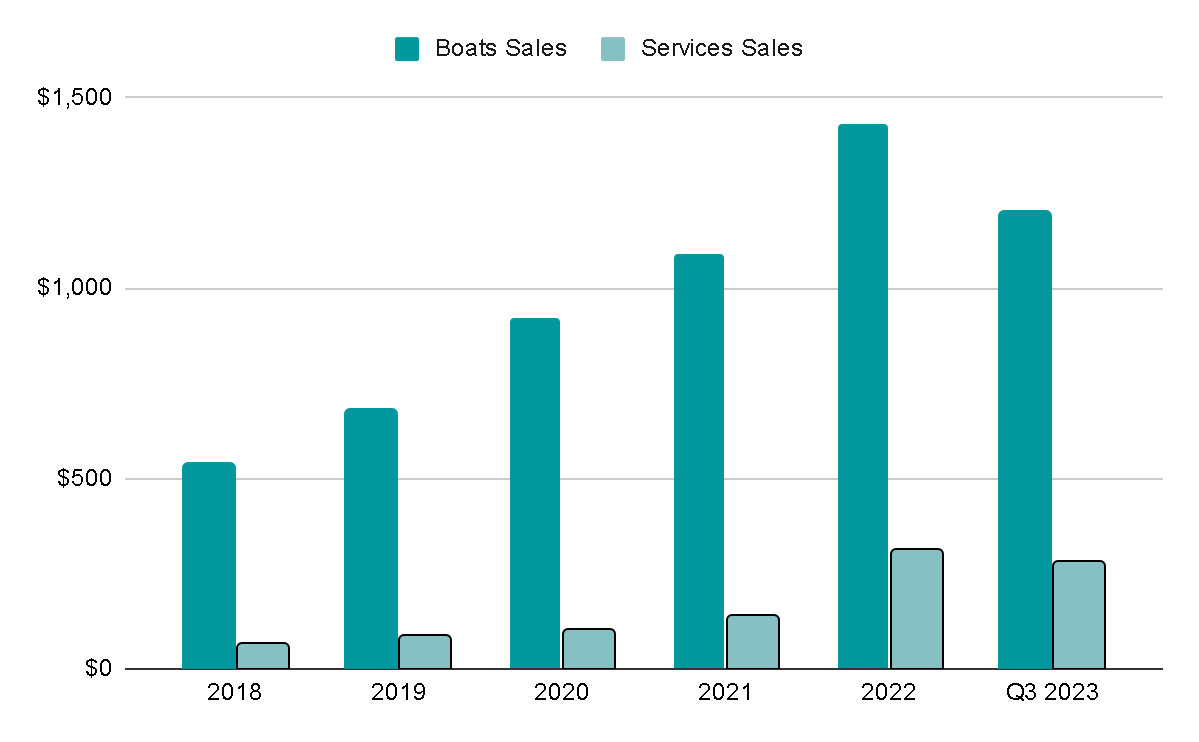

As mentioned earlier, a significant point of emphasis is the decreasing weight of boat sales in the company's revenue mix, while services such as maintenance are gaining greater relevance. This shift is vital as it mitigates the company's risk during economic downturns. The provided graph demonstrates a distinct improvement in sales generated by services during 2022 and the first nine months of 2023. Notably, these service-related sales accounted for almost 20% of the total sales during Q1-Q3 2023.

Revenue by type (Author's representation)

{kind=link}

And this is no coincidence, since in the Q4 2022 Conference Call the CEO, Austin Singleton, said the following:

We significantly expanded our parts and services business with the additions of TH Marine, Ocean Bio-Chem, YakGear and JIF Marine. We are excited about generating growth in this area and the margins it adds to our business.

The company appears to have a fairly capable CEO who is pursuing a goal that I believe is key to OneWater's success in the coming years.

Industry

Fragmented Market - Ideal For Acquisitions

The boat rental market is quite mature in the United States, however it's a fragmented industry that still has many small competitors that can be acquired, since the market is currently very regionalized (companies continue to sell within the same region) as you can see in the following article .

Market Growth (Grand View Research)

There are more than 4,000 boat stores across the country, whereas OneWater currently operates just 98 stores, representing roughly 2% of the market share.

Another significant point to note is that the four main competitors combined hold approximately 18% of the total market share. Furthermore, over 40% of the dealers operate as sole employees, which streamlines the acquisition process. Additionally, nearly 80% of independent repair shops are individual operators, presenting ample acquisition targets within the services sector.

The implications of this data suggest that the competitive landscape isn't highly aggressive. Beginning with a relatively small market share percentage indicates that the growth trajectory for the company will last longer. This positioning allows for sustained expansion over numerous years, both organically through the establishment of new stores and inorganically via acquisitions. The management team's acquisition strategy revolves around the following metrics:

- Acquiring dealerships at a value lower than 4x EV/EBITDA, and for businesses focused on repairs and accessories, the range is between 5x to 10x.

- Expanding geographically, given the company's current presence in only 20 out of the 50 US states, indicating substantial room for organic growth.

- Aiming for synergies that can double the EBITDA of the acquired businesses within the next two years.

Considering that goodwill constitutes just 25% of total assets and the Return on Capital Employed (ROCE) was 24% in 2022, it can be inferred that the company is not overpaying for acquisitions and is achieving favorable returns on its investment endeavors.

Management

Skin In The Game

As previously mentioned, the founder handed over the CEO role to his son, Austin Singleton, in 2006, and Austin has been leading the company since then. At present, he possesses a slightly over 4% ownership stake in the company, which equates to approximately $17 million worth of shares. This holding stands in contrast to his 2022 compensation, which totaled $3.7 million.

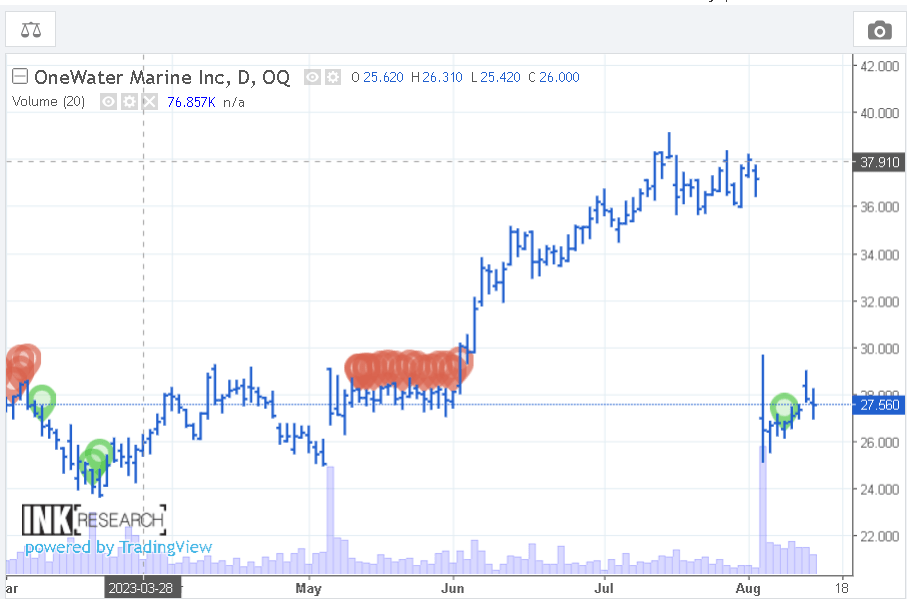

Between November and December of 2022, Austin acquired 10,400 shares at an average price of $31 per share, using around $322,000 of his personal funds to make the purchase. This action stands as a clear testament to his confidence in the business and his belief that its current value might be undervalued.

Furthermore, Austin's confidence continues to be demonstrated in his ongoing share purchases throughout 2023. On August 7th, he acquired an additional 10,000 shares. Worth noting, the sales shown in the chart originate from 'Jeffrey Lamkin,' an Independent Director who holds a 0.082% ownership stake in the company.

Insider buys and sells (Insider Tracking)

{kind=link}

Compensation

While the nearly $4 million in compensation he received falls in line with his peers and other companies of similar size, I find myself needing to exercise some criticism toward the compensation scheme. In fact, I would venture to say that it appears somewhat misleading.

The compensation structure is devised such that only 24% of the salary is provided as fixed cash, while the remaining 76% is divided between a cash incentive and a stock incentive. In theory, this setup seems favorable, as it provides an incentive for managers to actively pursue the achievement of financial objectives. However, a point of contention arises from the fact that the primary objective carries an 80% weight and revolves around meeting a certain threshold of Adjusted EBITDA.

CEO Compensation (OneWater Marine)

This concentration on a single financial metric can potentially skew decision-making and behavior towards short-term gains. Also it can incentivize managers to manipulate EBITDA adjustments to meet or exceed the target. EBITDA is known for being a metric that can be adjusted in various ways, sometimes leading to an inaccurate representation of a company's financial health.

Moreover, the provision of a 200% bonus for surpassing the Adjusted EBITDA target adds an extra layer of motivation for managers to potentially exploit these adjustments, possibly at the expense of accurate financial reporting.

CEO objectives (OneWater Marine)

While I cannot regard it as a direct reason to dismiss the company-given the 'skin in the game' and the long-term vision-it does, however, slightly taint my perspective of the management team.

I do like the company and the management team, but I wanted to address the negative aspects so that you can take them into consideration

Valuation

Valuing OneWater accurately in the long term is challenging due to the unpredictable nature of growth stemming from acquisitions and potential fluctuations in margins based on product mix. For instance, gross margins vary significantly depending on the segment: new boat sales at 55%, used boats at 15%, and maintenance services at 20%.

Additionally, I'd like to highlight that there seems to be little reason to project a valuation over 3 to 5 years, especially considering the uncertainty surrounding its performance even in the current year. The management team's continuous lowering of guidance throughout the 2023 fiscal year shows the unclear nature of the situation.

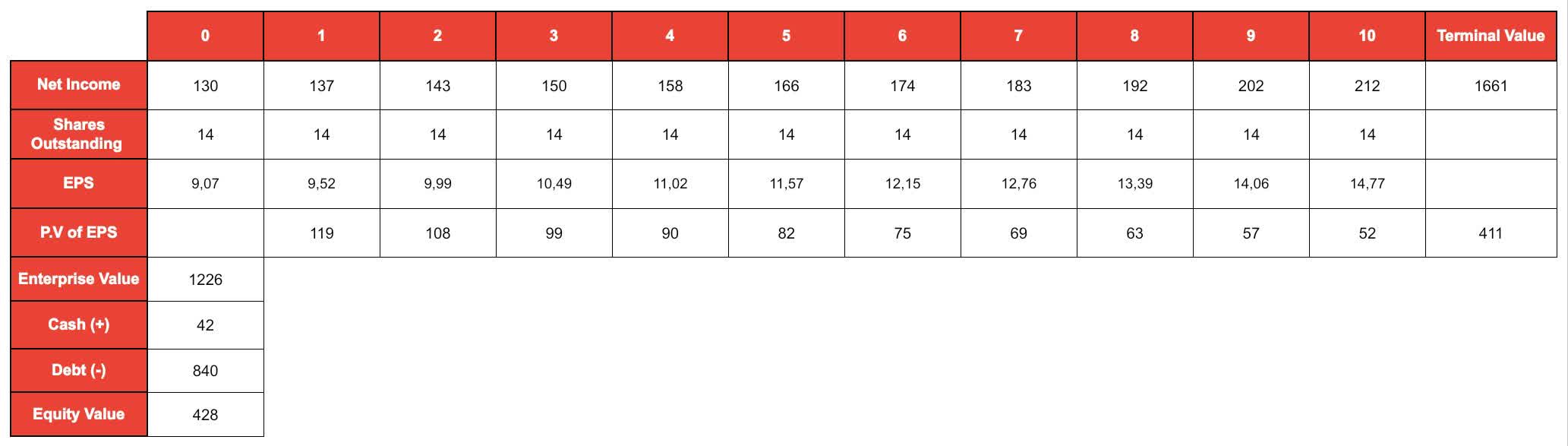

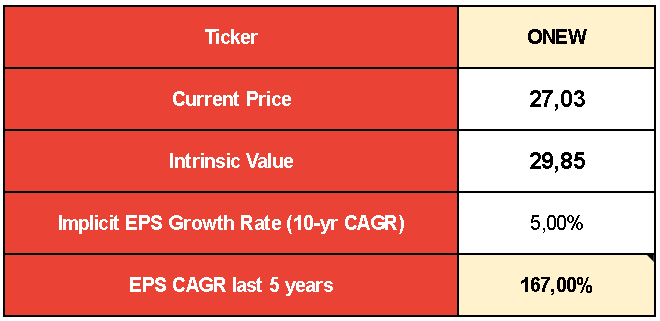

So, for my valuation approach, I'll use an inverted DCF model utilizing Net Income. I'll incorporate the known data and my inverted DCF model. This will reveal the growth rate required to achieve the expected return on my investment.

The data is the following (using the FY2022 numbers):

- Shares Outstanding: 14.34 million.

- Cash: 42 million

- 2022 Balance Sheet Debt: 840 million

- 2022 Net Income: 130 million

- Required Rate of Return: 15%

This means that the EPS would need to grow 5% annually in the next 10 years for the stock to be worth $30 today . I think this is really achievable, so I expect a 15% CAGR in my investment, a market beating return.

Net Income Projection (Author's Representation)

{kind=link}

In other words, OneWater could be generating $15 in EPS 10 years from now. Applying a 7x PER multiple, the price per share would be ~$105 and would mean a compound annual return of 14.5% from the current price of $27 USD.

Inversed DCF Model (Author's representation)

{kind=link}

Also, OneWater is trading at a PER of 5x, while close competitors like MarineMax ( HZO ) have been trading at 6-8x in recent years. This expansion of the PER would also help in the expected return on the stock.

Risks

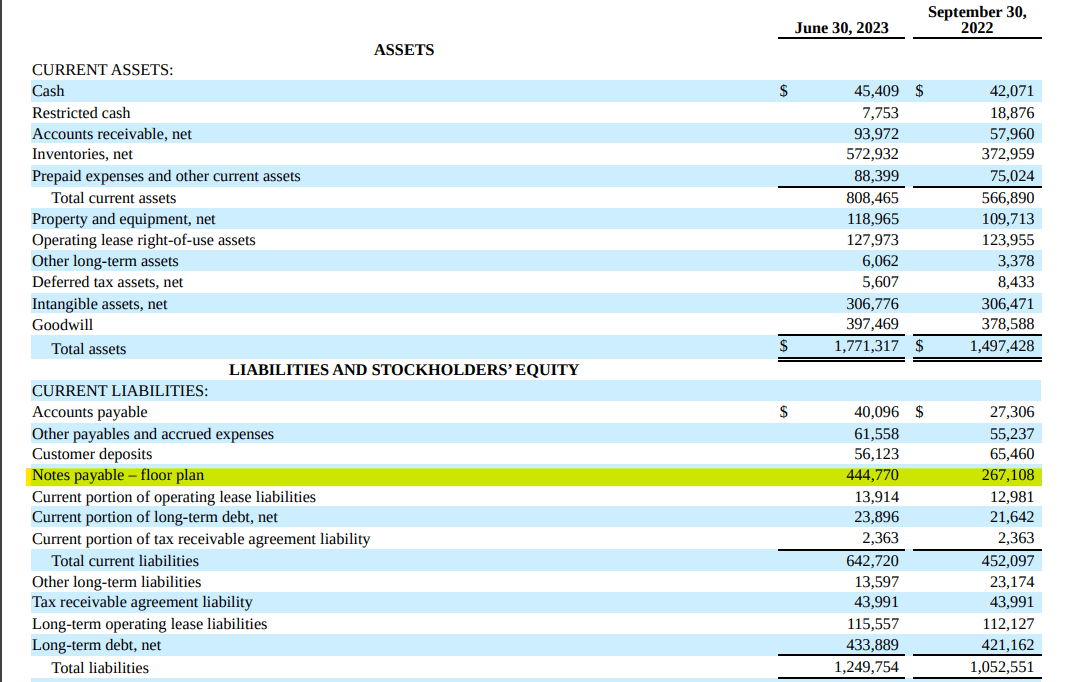

Debt: The long-term debt shouldn't been a problem since most of it ($428 million) has a maturing with a full repayment on August 9, 2027 with a bearing interest at 7.14%.

The real risk would be the "Notes payable - floor plan", an inventory financing program. As of June 30, 2023 the outstanding balance of the facility was $445M or an increase of 66% compared to the balance of September 2022.

{kind=link}

It's important to keep an eye on this situation because a failure to meet these obligations could limit the company's ability to sell assets (excluding inventory), pursue mergers and acquisitions, or distribute cash dividends. However, as of June 30 in the current year, OneWater was compliant with all the agreed-upon terms.

Recession: The boat industry is highly discretionary, and during a recession, consumer spending on it would be significantly impacted. This has been market's biggest fear this year, but for now, it appears that the much-discussed downturn has not materialized. Nevertheless, it should still be considered as a potential risk even after the cut-off of guidance.

Final Thoughts

In summary, while the recent decline in the stock's value seems justifiable, the present price already factors in a reasonable and conservative growth projection, potentially leading to a favorable long-term return. Although the business model may not be of exceptionally high quality, the adeptness of the management team is evident, and the industry presents significant growth prospects, both organically and through acquisitions.

For further details see:

OneWater Marine: Poor Growth Priced In Already Could Likely Lead To Long-Term Upside