MPX - OneWater Marine: Still Fantastically Cheap

Summary

- OneWater Marine continues to grow sales nicely, though the firm has shown some weakness and indicated that some future weakness lies ahead.

- This may discourage some investors, but the company's overall financial condition looks solid.

- The stock is also incredibly cheap and likely offers tremendous upside from here.

I pride myself in my solid investment track record. For the most part, the calls that I make tend to turn out quite well. This is especially true for the companies that I rate a 'strong buy'. Unfortunately, not every prospect that I or any other investor will pick ends up having a desirable outcome. So far, one firm that has experienced a great deal of pain is OneWater Marine ( ONEW ). Mixed financial performance reported by management, combined with broader concerns about the economy, have been instrumental in pushing shares of the business down even though they look incredibly cheap. In retrospect, I underestimated just how bearish the market would turn. Having said that, the fundamental condition of the business is still very much robust and the near-term outlook provided by management is encouraging. Given these considerations, I do believe that the company still warrants the 'strong buy' rating I assigned it last year.

Even more attractive now

The last article I wrote about OneWater Marine was published in the middle of September 2022. A business that focuses on the retail sale of boats and other related offerings may not exactly seem like an attractive place to put your money given the state of the economy right now. Inflation, higher interest rates, and concerns about employment moving forward are not exactly conducive to the purchase of marine craft. But in that article, I talked about how well the company had been doing, with a combination of strong demand and multiple acquisitions fueling its growth. I did recognize that risk remained for investors and that the near-term picture for the company may be less appealing than the recent past had been. But because of how cheap shares were, I had no choice but to rate the business a 'strong buy' to reflect my view that shares should significantly outperform the broader market moving forward. Fast-forward to today, and things have not gone exactly as planned. While the S&P 500 is down 2.8%, shares of OneWater Marine have seen a downside of 21.1%.

{kind=link}

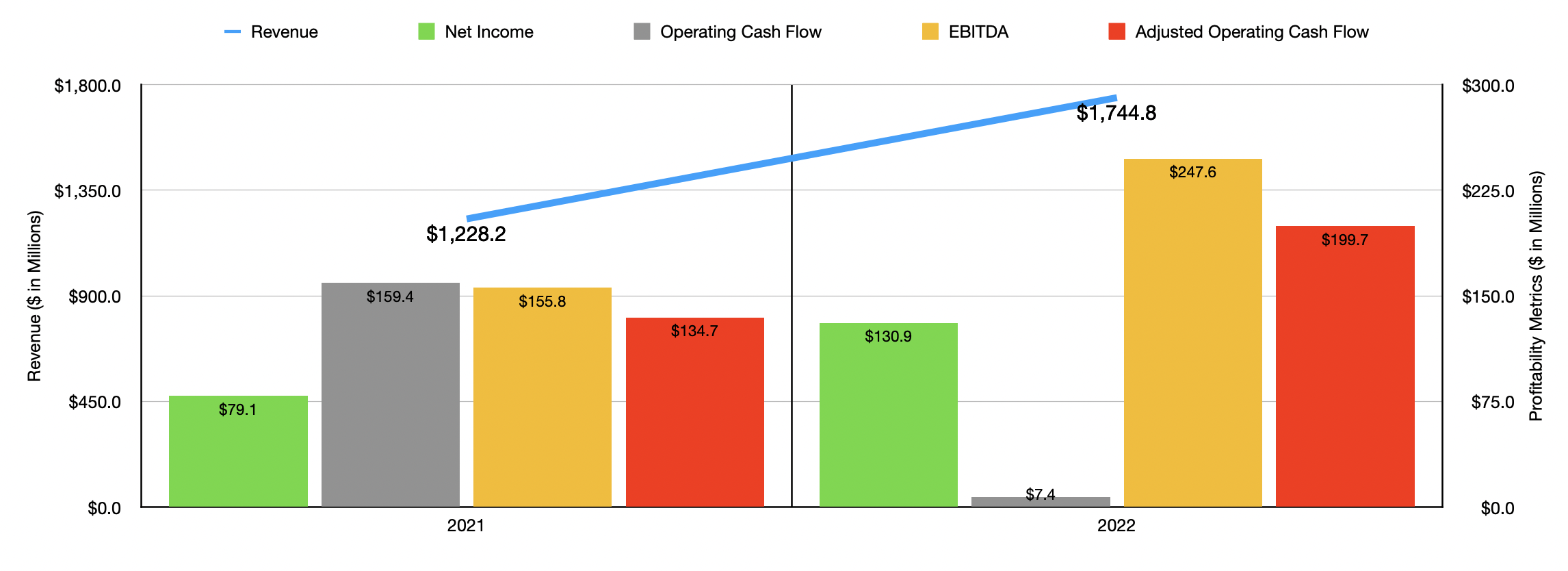

This kind of return disparity is typical of a company that has already experienced fundamental weakness. But that hasn't exactly been the case. Rather, financial data reported by the company has been somewhat mixed. Consider how the company performed during its 2022 fiscal year . Revenue for that period came in at $1.74 billion. That represents an increase of 42.1% over the $1.23 billion the company reported only one year earlier. In absolute dollar terms, the greatest growth for the company came from its new boat operations. Revenue here surged 30.6%, climbing from $872.7 million to $1.14 billion. This rise was driven by a combination of factors, including the firm's continued execution of operational improvements on previously acquired dealers, a change in the mix of boat brands and models sold, and higher prices per unit sold. Preowned boat sales jumped 36.2%, while finance and insurance income revenue grew 31.2%. But at just 16.9% of sales and 3.2% of sales, respectively, compared to the 65.3% of sales that new boat activities accounted for, these increases were less meaningful for shareholders. Another heavy lifter for revenue involved the company's service, parts, and other activities. Revenue here spiked 164.1% from $96.4 million to $254.7 million. This increase, according to management, was driven largely by acquisitions the company made over the past year or so.

Although revenue for the company rose nicely, bottom line results were somewhat mixed. For the most part, however, they were very solid. Net income, for instance, jumped from $79.1 million to $130.9 million. On the other hand, operating cash flow plunged from $159.4 million to $7.4 million. If we adjust for changes in working capital, however, we would have seen operating cash flow actually improve nicely, climbing from $134.7 million to $199.7 million. Meanwhile, EBITDA shot up from $155.8 million to $247.6 million.

{kind=link}

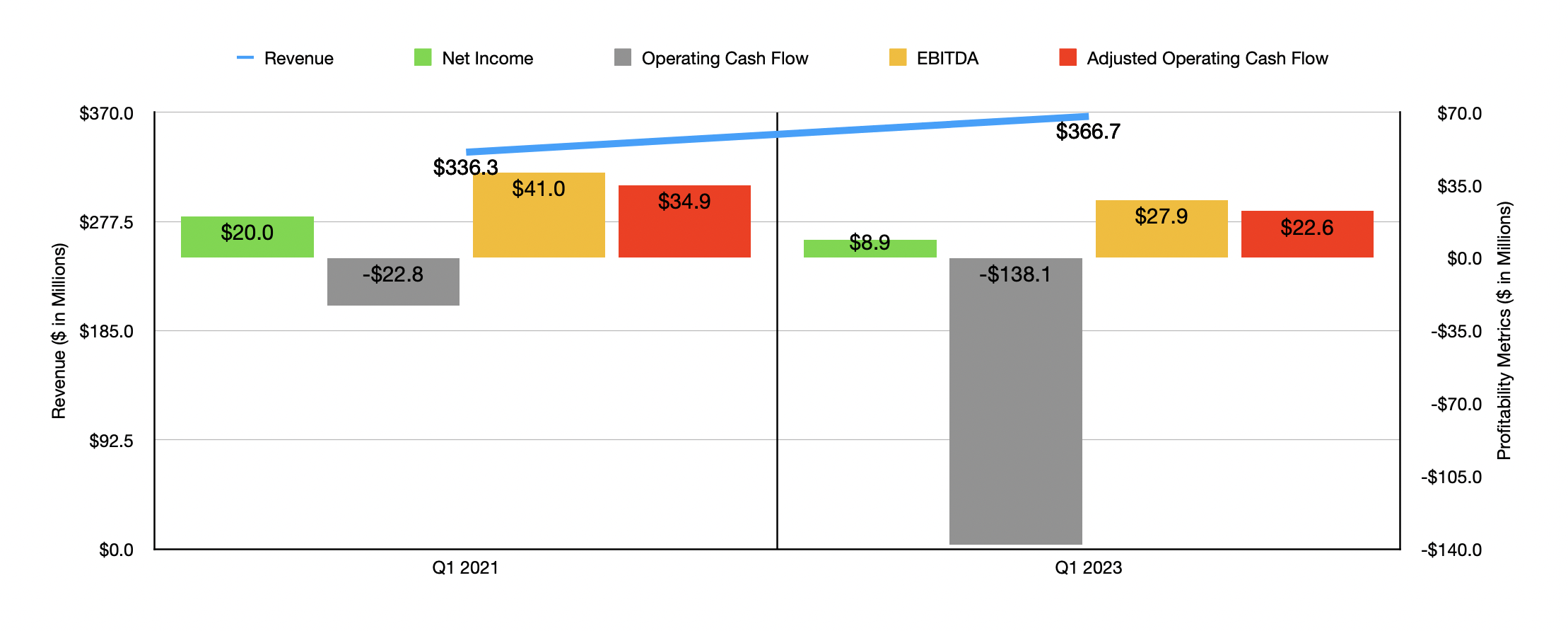

For the 2023 fiscal year, we currently only have data for the first quarter of the year. Sales during this time came in at $366.7 million. That's up 9% over the $336.3 million reported one year earlier. Unlike in the 2022 fiscal year, the first quarter did experience some weakness. New boat revenue, for instance, dropped by 1.6%, while finance and insurance income sales fell 4%. The drop in new boat sales for the company was driven largely by a fall in the number of units sold, some of which was offset by higher average selling prices. This is not to say that there was weakness across the board. Pre-owned boat sales actually rose 4.4% year over year, with that growth being driven largely by a rise in the number of units sold. In this particular quarter, the heavy lifting for the company was done by the service, parts, and other activities reported by management. Revenue here spiked 86.3% thanks in large part to the aforementioned acquisitions the company made.

On the bottom line, the company did report some weakness as well. Net income of $8.9 million came in far lower than the $20 million reported one year earlier. This came even in spite of higher sales and a gross profit margin that remained virtually flat year over year. The real pain for the company was associated with a 31.7% surge in selling, general, and administrative expenses. This increase was largely driven by an investment that the company made to support growing revenue and profits. This involved higher personnel expenses related to acquisitions, as well as an increase in marketing expenses related to increased boat show activity. Other profitability metrics also trended lower. Operating cash flow went from negative $22.8 million to negative $138.1 million. Even if we adjust for changes in working capital, it would have fallen from $34.9 million to $22.6 million. And finally, EBITDA declined from $41 million to $27.9 million.

For the 2023 fiscal year, management remains optimistic. They currently think that same-store sales will range between being flat and growing at a mid-single-digit rate. Earnings per share should be between $7.50 and $8. At the midpoint, this would translate to profits of $113 million. That is slightly lower than what the company reported in 2022. But considering broader economic conditions, the picture could be worse. They also are forecasting EBITDA of between $200 million and $225 million. If we assume that other profitability metrics should decrease at the same rate as EBITDA is forecasted to at the midpoint, that would translate to adjusted operating cash flow of $171.4 million.

{kind=link}

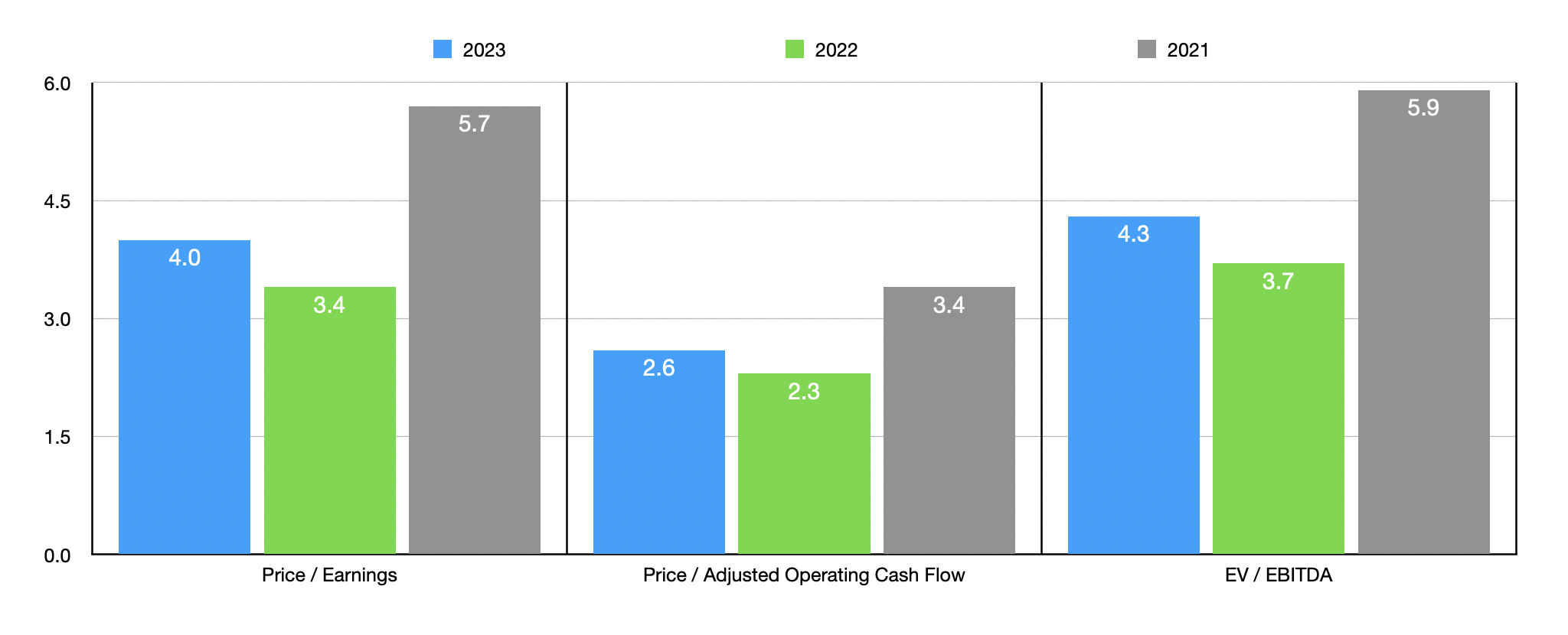

Valuing the company is fairly straightforward. Although, there is one caveat that needs to be taken into account. This relates to the company's balance sheet. At present, the firm has floor plan notes payable of $425.4 million. Although this is technically debt, it is also backed by the $527 million in net inventories on the company's books. Because of this, I have not included that figure into the enterprise value of the company. With that in mind, using data from 2023, I calculated that the company is trading at a forward price-to-earnings multiple of 4.0. The forward price to adjusted operating cash flow multiple is even lower at 2.6, while the EV to EBITDA multiple should come in at 4.3. As you can see in the chart above, these numbers are higher than what the company would be priced at using data from 2022. But they are still lower than if we used data from 2021. As part of my analysis, I also compared the company to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 4.2 to a high of 11.1. Using the price to operating cash flow approach, the range would be from 4.5 to 11.3. And when it comes to the EV to EBITDA approach, the range would be from 4.9 to 7.8. In all three cases, our prospect was the cheapest of the group.

| Company |

| Price/Earnings |

| Price/Operating Cash Flow |

| EV/EBITDA |

| OneWater Marine |

| 3.4 |

| 2.3 |

| 3.7 |

| MarineMax ( HZO ) |

| 4.2 |

| 9.1 |

| 5.0 |

| Malibu Boats ( MBUU ) |

| 7.4 |

| 8.0 |

| 4.9 |

| Brunswick ( BC ) |

| 9.8 |

| 11.3 |

| 6.9 |

| Marine Products Corporation ( MPX ) |

| 11.0 |

| 10.9 |

| 7.8 |

| MasterCraft Boat Holdings ( MCFT ) |

| 11.1 |

| 4.5 |

| 4.9 |

Takeaway

I do acknowledge that the near-term picture for OneWater Marine might be impaired to some degree because of general market conditions. But between management's optimism that things should hold fairly steady and how cheap shares are at the moment, I do believe that it makes for a great investment prospect worthy of a 'strong buy' rating. I currently have a very concentrated portfolio of only 10 holdings. And frankly, I would prefer to shrink that to 7 or 8. Some of my holdings are reaching the point where I would like to unload them. And as I do so, this is one prospect that is near the top of my list to consider putting some funds into.

For further details see:

OneWater Marine: Still Fantastically Cheap