ONLN - ONLN: A Year Later Outlook Still Very Mixed

2023-10-10 10:48:48 ET

Summary

- The ProShares Online Retail ETF is being evaluated as an investment at the current market price.

- Rising oil prices and geopolitical unrest in the Middle East are major headwinds for the discretionary retail sector.

- I am maintaining a "hold" rating on ONLN due to these factors and the potential impact on consumer confidence.

Main Thesis & Background

The purpose of this article is to evaluate the ProShares Online Retail ETF ( ONLN ) as an investment at the current market price. This fund takes an approach to own retailers that principally sell online or through other non-store channels, rather than traditional brick-and-mortar retailers and "seeks investment results, before fees and expenses, that track the performance of the ProShares Online Retail Index".

I used to own the retail sector in a variety of ways - ONLN being one of them. But over time I had shed this exposure while keeping the fund on my radar looking for a chance to get back in. A year ago, I still saw a clouded backdrop, leading me to a cautious stance on the fund. In hindsight, I was spot-on with this assessment :

Fund Performance (Seeking Alpha)

With a fast-changing market, I thought after a year had passed that I should give ONLN another look. After all, the holiday season is coming up, the US (and most of the developed world) has avoided recession, and the jobs market has been resilient. All these factors could add up to a bullish case for retail.

Unfortunately, after digging in to the sector, I see continued merit for caution. The flare-up in violence in the Middle East, while tragic for so many reasons, is also a major headwind for discretionary areas. Rising oil prices, dampened consumer confidence, and elevated interest rates are all forces that will make gains in this sector difficult to come by in my opinion. As a result, I am maintaining my "hold" rating on ONLN, and will explain why below.

Rising Oil Prices A Major Consumer Headwind

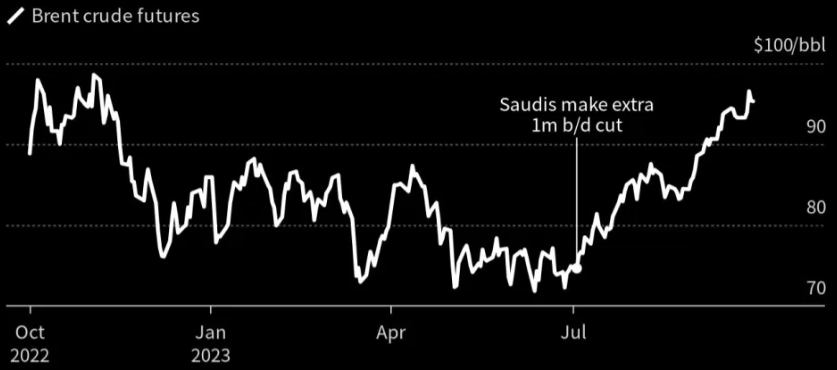

My first topic is one that is very recent and relevant. This concerns the surge in oil prices on the backdrop of a fresh wave of violence in the Middle East. Specifically, this refers to the escalating conflict between Israel and a number of terrorist groups, with no real end in sight. This is a terrible human tragedy, and one that is already causing volatility in financial markets. A "beneficiary" of geo-political unrest is often crude oil - and we are seeing that play out now as well:

Oil News on Monday's Open (CNBC)

It is always a little uncomfortable to discuss investment implications during a tragic event like this, but we are investors here. The reality is that violence and unrest often combine with higher energy bills, and that is likely going to play out this time as well. While the direct impact on the American household from this conflict is minor - we could feel the sting of higher oil prices at the pump and in our monthly heating bills.

While some expect the rise to be fleeting, I would not be so sure. Israel has declared war and the oil market has been tight in the second half of 2023 to begin with. OPEC+ has committed to balancing out the demand-supply dynamic, and this suggests to me that higher prices are here to stay:

{kind=link}

To tie this back to ONLN, we need to recognize this is a more "discretionary" fund. ONLN - and the underlying companies that make up the ETF - rely on consumers to buy things they want, as opposed to "need" (for the most part):

ONLN's Top Holdings (ProShares)

These companies depend on consumers buying online, of course, but also buying non-staple related goods. A look at the list suggests that if consumers/households are feeling a pinch in other areas - such as energy prices - they can probably cut back on their discretionary spend within these categories. That is central to why I cannot place a "buy" rating on this particular investment right now.

Future Confidence Taking A Big Hit

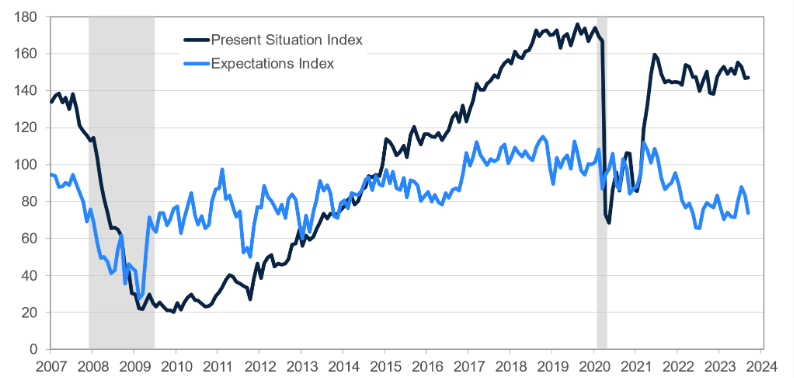

Another major concern I have is consumer confidence regarding the future. This was before the recent headlines, so I can only imagine we will see further dips from here. While consumer confidence on the "present" situation is not exactly strong, it's not overly weak either. But on the forward-looking "expectations" index, we see that American households are anticipating a more challenging environment ahead:

Present & Expectations Index (The Conference Board)

{kind=link}

This will likely cause some belt-tightening around the country and, again, this doesn't bode well for companies that sell "nice to have" items. In this type of backdrop I want to focus on companies that have pricing power and sell more "staple" related goods (or that avoid the retail consumer for the most part).

The bottom-line is that if Americans are worried about what their future will bring, they will likely cut back now . This is a net negative for short-term profits in the retail sector, and weighs heavily on my investment outlook for ONLN by extension.

Expense Ratio Not Justifiable

My next gripe with this ETF is one I have had for a while. It concerns the fund's expense ratio, which clocks in at .58 basis points:

Fund Metrics (ProShares)

The simple truth is that this is too high for this type of sector fund. Other options such as the SPDR S&P Retail Sector ETF ( XRT ), Consumer Discretionary Select Sector SPDR ETF ( XLY ), or the VanEck Retail ETF ( RTH ) all charge lower amounts for the privilege of owning them. (i.e. XRT and RTH have .35 basis point expense ratios, while XLY has a .10 basis point expense ratio).

This has been the case for ONLN for a long time (since its inception), but I had incorrectly surmised that the fund would cut what it charges down to a level that more definitively competes with its peers.

Alas, I have been wrong, so it stands to reason why ONLN is an "avoid". Even if one wants to play the online or broader retail space - why choose ONLN when similar options exist that charge lower fees? Seems like a no-brainer for me, so it will be difficult for me to merit an upgrade on this fund until ProShares makes a fundamental change here.

Higher Borrowing Costs A Consumer Drag

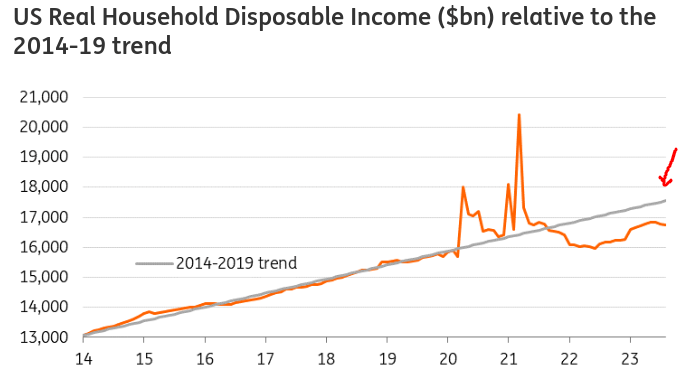

My final point looks at interest rates and the impact on the US consumer. Similar to rising oil prices, higher interest rates act like a tax in that they suck money out of the consumer-oriented economy as households have less discretionary spend. The more Americans are forced to spend filling up their tanks or managing their borrowing costs, the less they have to buy or goods and services elsewhere that they want.

This is a reality of life that readers are probably very familiar with. As the Fed has maintained a "higher for longer" mantra, yields are up in the market and that is prompting higher interest rates for everything consumer credit related. This includes mortgages, auto loans, credit cards - you name it. The net result is that American households are seeing more of their after-tax money go toward servicing debt, and less is left over for disposable income. This bucks a multi-year trend that established itself during the pandemic:

{kind=link}

Now this is not caused completely by higher rates - inflation is also to blame. But there-in lies the problem. Americans are being punished by higher prices and higher borrowing costs to pay for those prices. With the resumption of student loan obligations as well, I just can't see a bullish thesis materializing for the American consumer. Yes, job numbers and wages have been resilient, but there are a host of other headwinds that mitigate those forces. Ultimately, this pressures the outlook for ONLN.

Bottom-line

Retail has been in a tough spot over the past year and that has limited the opportunity for ONLN. Looking ahead to the end of 2023 and the start of 2024, I don't see much changing. Consumers face higher prices, large debt burdens, and geo-political unrest is sending energy costs soaring in the immediate term. ONLN does not have any bullish momentum to get excited about, and I'm not seeing an environment that suggests consumers will lead the way in the months ahead. Therefore, I am maintaining a cautious view on ONLN, and suggest to my followers that they approach any new positions very selectively at this time.

For further details see:

ONLN: A Year Later, Outlook Still Very Mixed