ON - onsemi: Weakness On Deck

Summary

- onsemi looks poised for further weakness after a record Q2 as macro and industry headwinds threaten vehicle production growth.

- The company noted a conservative stance in its Q3 guidance, and projected marginal sequential growth in revenues and flat growth down the line.

- Downside risk looks elevated as customers Toyota and Honda faced significant production cuts in Q3, while Conti and Aptiv pointed to weaker macro conditions.

- However, a relatively fair valuation supported by expanding margins, strong revenue and EBITDA growth could still push onsemi's shares high.

With Q3 heading into its final stretch in September, shares in onsemi (ON) look poised for further weakness after an 11% pullback from reaching new highs. Production cuts in key automotive OEMs as well as generally weak forecasts for the second half of the year paint a bleaker picture for the semi company as the year closes out. onsemi's ~40% share of revenues driven through the automotive sector leave it particularly exposed to persistent lingering challenges facing the sector.

Q2 Recap

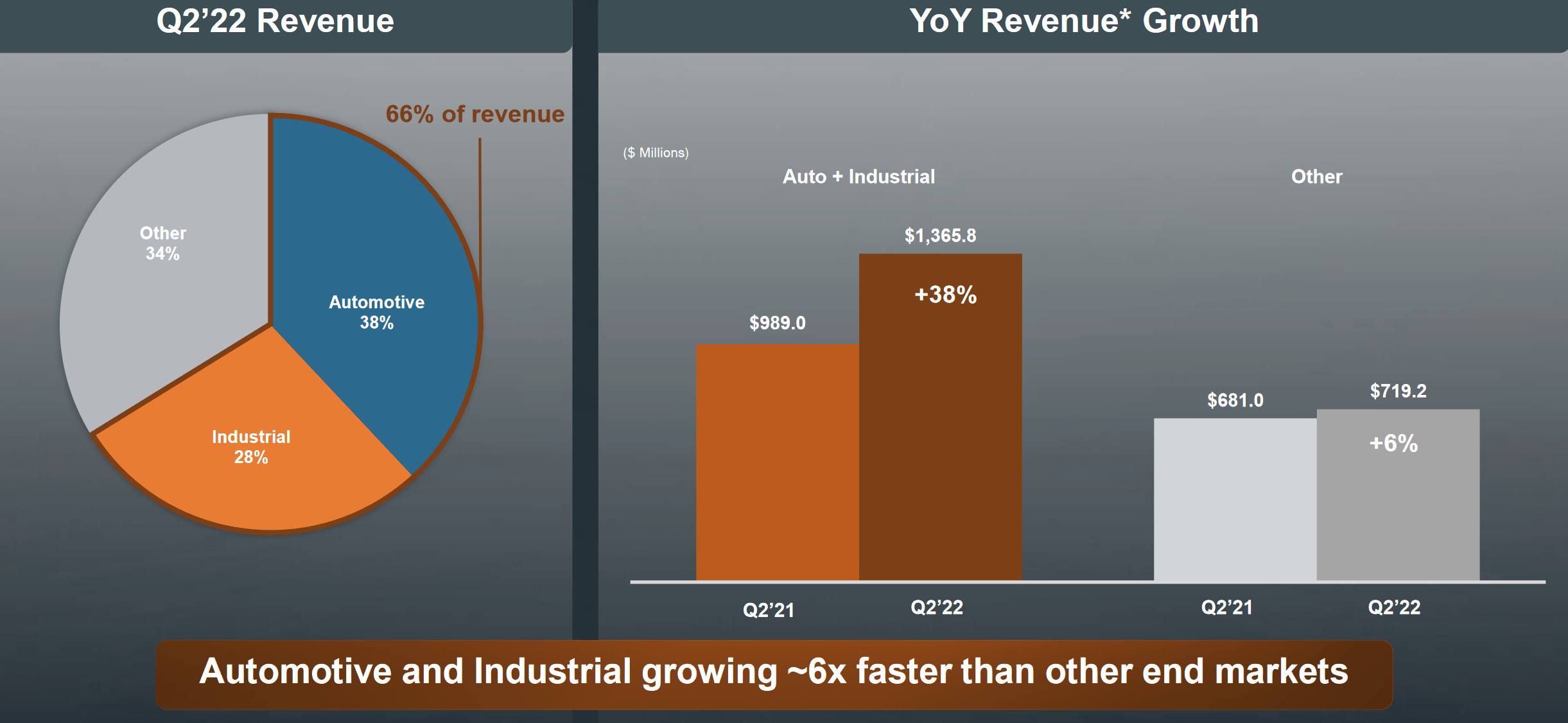

onsemi's quarterly revenues topped $2 billion for the first time, reaching a record, driven in part by ~10% sequential growth (+41% y/y) in auto revenues to $784 million. Auto revenues accounted for 37.7% of revenues during the quarter. onsemi also posted record margins and EPS which more than doubled during the quarter, further highlighting the strength of the business.

CEO Hassane El-Khoury said onsemi's leadership in the accelerating megatrends of vehicle electrification, ADAS, energy infrastructure and factory automation have enabled us to extend long term supply agreements and increase demand visibility." Again, this is evident within auto's strong 41% y/y growth rate, as ADAS adoption ticks higher with manufacturers adding active safety assistance features to a growing number of models, along with established ADAS systems such as GM's ( GM ) Super Cruise and Ford's ( F ) BlueCruise actively expanding.

{kind=link}

However, auto & industrial are the main drivers of onsemi's growth - with the segment expected to reach ~75% of revenues by 2025, with growth rates >30%, weakness in the segment does not signal positively for the business. El-Khoury noted that while onsemi is " optimistic about our outlook, we remain sensitive to dynamic market conditions." For Q3, onsemi forecast minor sequential growth, +4% at the high end, with margins and EPS remaining practically flat. Growth rates are expected to cool to 21% y/y for Q3, 11 pp lower than the ~32% y/y rate seen in Q3 2021.

Q3 Outlook

Deteriorating conditions in automotive production from major OEMs as well as lingering headwinds to the broader market are challenging onsemi's growth, and a picture for slight sequential gains to another record quarter of revenue could underestimate the negative impacts of these developments.

onsemi noted in its Q2 call that for Q3, "Demand continues to outpace supply in our targeted automotive and industrial end markets while there are pockets of softness in our non-core markets. Given the uncertainty in the macro environment, we are taking a conservative stance in judging down demand in our guidance for the third quarter." onsemi's conservative guidance may not be conservative enough, given the underlying trends in key customers.

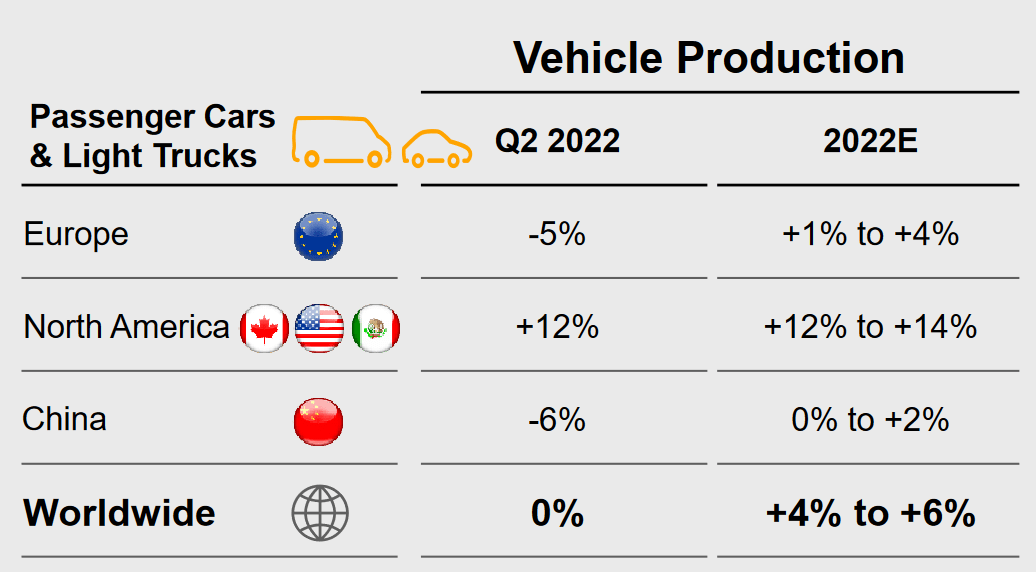

Even though August light-vehicle sales are shaping up for the "first year-over-year gain for new light-vehicle sales for the trailing year," per estimates from S&P Global Mobility's analysts, the industry is not in the clear. The "overall August results are unlikely to signal an easing of challenges facing the beleaguered automotive industry. Constrained inventories, stemming from continued supply disruptions, preventing sales from rebounding more aggressively."

As such, a majority of onsemi's fiscal Q3 (July-Sept.) coincides with a period of weakness for major OEMs, even as the industry could eke out a slight gain in sales. Major firms and onsemi customers Continental AG (CTTAY), Aptiv (APTV), Honda (HMC) and Toyota (TM) have pointed to production cuts and more cautious outlooks, highlighting the potential weakness for onsemi closing out the year.

Broader Weakness Evident In Customers' Production & Outlooks

A handful of onsemi's customers in the automotive segment have expressed caution towards full-year outlooks, especially in the second half, as well as significant vehicle production cuts, suggesting a higher risk to onsemi's sales coming below targets.

Continental

Unlike some of the other firms listed here, Conti maintained its outlook for the fiscal year during its earnings report in early August, anticipating a "a rise in automotive production" and cost measures to take effect. However, the Tier 1 supplier noted an "extremely challenging" market for auto suppliers as current headwinds "will not subside any time soon."

Conti's reasoning supporting its maintained outlook is a "stabilization of global supply chains, a slight improvement in the availability of semiconductors and continued stable energy supplies in Europe, and particularly in Germany."

As August comes to a close, Conti's assumptions are already challenged - UK supply chains are in a rut following a strike at the crucial Port of Felixstowe, Russia halted gas flows to Europe again on the 31st, lasting at least until September 3, while low river levels on the Rhine and Yangtze have been adding pressure to shipping and logistics.

While these factors do not directly apply to onsemi, they represent a deterioration, or downside risk, to the three key factors serving as the foundation for Conti's "optimistic" outlook. The challenges to those three factors place doubt on other targets from Conti, such as a recovery in China and European vehicle production at a high enough degree to see growth this year.

{kind=link}

For onsemi, lower production volumes as a whole could weigh on revenues, even if other parts/chips are holding up production. onsemi's long-term contracts provide it stability and visibility, but ultimately, onsemi could feel effects stemming from lowered production volume caused by other suppliers.

Aptiv

Aptiv " lowered its annual forecasts for profit and revenue, blaming production cuts by major automakers in Europe as the region braces for a disruption in gas supplies from Russia." Aptiv cut its full-year revenue forecast by ~4.5% to $17.15 billion at midpoint, and its earnings forecast by ~24% to $3.30 at midpoint.

Aptiv has seen "continued adverse impacts from global inflationary pressures and the worldwide semiconductor shortage," which do not show signs of easing anytime soon. Persistent impacts from inflation and chip shortages lasting through 2023 pressure Aptiv's already-lowered forecast, again leading to more trouble ahead for one of onsemi's customers.

Aptiv also shed a light on the power solutions and signals market - power solutions is onsemi's most important segment, generating ~50% of the firm's revenues during Q2. Aptiv saw 14% growth in Q2, and forecasts ~15% growth for the full-year; Aptiv also saw lower volume and supply chain challenges from China. In addition to a 12% guide down in European vehicle production units to a project a 5% decline for the full-year, Aptiv's results also point to a higher risk of weakness moving forward in key market segments for onsemi.

Honda

Major OEM Honda has seen its fair share of production impacts arise this year, with some more substantial impacts arising during calendar Q3.

In July , Honda "said it would slash production by up to 30% in Japan next month [August] against original plans due to persistent supply chain and logistical issues." Japan accounted for ~18% of Honda's global production during July, so these production cuts will have an impact on the OEM's sales figures.

For September , Honda "will scale back its production plans by as much as 40% at its Japanese plants,...signifying that their ongoing production woes aren't close to being over." Honda is blaming persistent supply chain woes and the semiconductor shortage for these production cuts.

Off the bat, Honda is looking at ~50,000 units of lost production in Japan alone; other production impacts in North America could further stress the OEM's production volumes.

As a customer for onsemi, Honda's production cuts cast further doubt on global production volumes across onsemi's customer cohort, with Q3 volume declines possible for onsemi's customer. Honda's cuts also illuminate a geographic risk stemming from Japan, which accounts for ~7% of onsemi's revenues.

Toyota

Similar to Honda, Toyota is facing production impacts during Q3. Toyota initially cut its July output plans by 50,000 vehicles, but a recent release of July production volumes saw the OEM produce 706,547 vehicles, an 8.6% y/y decline and around 12% below its 800,000 unit target. Thus, production impacts likely worsened during the month, considering the wide miss in production output, much wider than the initial 50,000 unit forecast. Toyota said domestic production fell 28.2%, approximately in line with Honda's cuts.

Looking forward, Toyota has maintained an air of optimism - the OEM still is holding steady with an 850,000 unit target for September, up nearly 20% from July's and August's targeted production levels of approximately 700,000 units. During August, Toyota is forecasting about 18 days of suspension at its Motomachi plant, for bZ4X EV production, with smaller suspensions at other plants. It's unlikely that production issues will magically resolve for September, and further output cuts are likely.

Given the state of supply chains and chips, Toyota's high production is questionable, along with its forecast for a record 9.7 million units of production this fiscal year.

Valuation & Risks

On a valuation basis, onsemi's downside looks more concentrated in macro headwinds and deteriorating sentiment, rather than something more fundamentally-driven.

Shares look relatively fairly valued given underlying fundaments, even near all-time-highs: rapid triple-digit EBITDA growth, nearly 80% EPS growth, and strong free cash flow combined with a 15x PE, below a historical 20x average, and a 4x EV/revenues, above a 2.5x average. Above average EV/revenue multiples are justified by a ~30% revenue growth rate and expanding margins.

However, this forecast for persisting weakness hanging over shares does face some risks, which could see onsemi's shares find more upside.

Strength in BEV sales supports onsemi's revenues and end-markets - the firm highlighted that EVs "require up to $700 of incremental onsemi content for drivetrain and onboard charging as compared to an internal combustion engine car." Thus, S&P Global's expectation that "the rising BEV sales trend will continue" supports a positive outlook for onsemi's key markets as EV sales are seeing longer-term tailwinds .

onsemi also expects to "triple last year's silicon carbide revenue in 2022 and exceed $1 billion in revenue in 2023." SiC chips are key in developing more powerful EV drivetrains, extending range, and allowing for faster charging, among other things. The long-term tailwinds for SiC applications in EVs supports solid long-term growth for onsemi.

Outlook

onsemi potentially faces a string of weakness closing out the year, just after reaching record revenues above $2 billion and projecting revenues to grow marginally in Q3. Broader industry factors such as supply chain chaos from port strikes and shipping impingements from droughts, along with persistent chip shortages, are pressuring OEM production volumes and pose a downside risk to onsemi as customers feel adverse impacts.

Honda and Toyota have seen struggles producing vehicles during Q3, with some significant production cuts; Toyota is guiding for 850,000 units volume in September, a ~20% jump from August's targeted 700,000 volume. More cuts are probable given macro conditions. Tier 1 suppliers Aptiv and Continental also are forecasting for some weakness in vehicle production and in the power and sensing market.

However, onsemi's long-term supply contracts and presence in a high-growing SiC chip segment, along with a relative fair valuation supported by high revenue growth, expanding margins, and rapid growth in EBITDA and EPS could support onsemi's shares, should the chipmaker shrug off possible weakness in Q3.

For further details see:

onsemi: Weakness On Deck