OPBK - OP Bancorp: Californian Economy Interest Rates To Drive Earnings

Summary

- Loan growth will likely slow down from the first half’s level. However, strong regional markets will keep loan growth at a moderate level.

- The margin is moderately rate sensitive.

- The December 2022 target price suggests a high upside from the current market price. Further, OPBK is offering a good dividend yield.

Earnings of OP Bancorp ( OPBK ) will likely increase this year thanks to moderate loan growth, which will, in turn, be driven by strong regional economies. Further, the margin will benefit from rising interest rates. Overall, I'm expecting OP Bancorp to report earnings of $2.25 per share for 2022, up 19% year-over-year. Compared to my last report on the company, I've barely changed my earnings estimate. For 2023, I'm expecting OP Bancorp to report earnings of $2.39 per share, up 6% year-over-year. The year-end target price suggests a high upside from the current market price. Therefore, I'm maintaining a buy rating on OP Bancorp.

California’s Economic Factors to Sustain Loan Growth

OP Bancorp’s loan growth slowed to 3.9% in the second quarter from 8.8% in the first quarter of 2022. Going forward, loan growth will likely decelerate even further as the increasing interest rates will tone down credit demand.

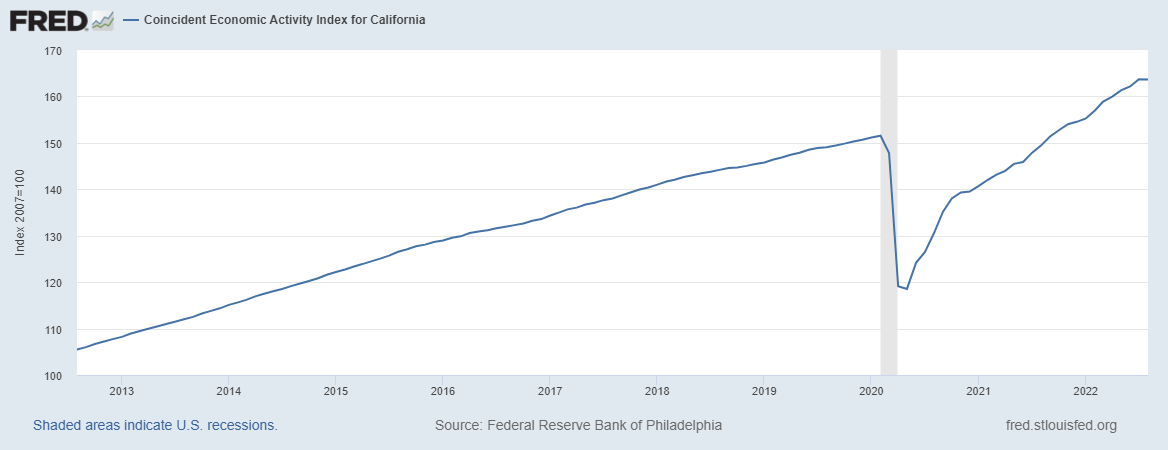

On the plus side, regional economic strength will likely continue to support loan growth. OP Bancorp mostly operates in California, with a concentration in Los Angeles. The company also has some presence in Atlanta GA, Aurora CO, Lynnwood WA, Seattle WA, and Carrollton TX. OP Bancorp focuses on Korean Americans, but it's not limited to them alone. The coincident economic activity index for California paints a promising picture, which should keep loan growth elevated in that region.

{kind=link}

Further, the unemployment rate for the state has improved considerably, as shown below.

Considering these factors, I'm expecting the loan portfolio to grow by 3% every quarter till the end of 2023. This will lead to loan growth of 19.9% for 2022. In my last report on OP Bancorp, I projected a loan growth of 18.9% for 2022. I’ve slightly increased my loan growth estimate because the second quarter’s performance beat my previous expectation.

Meanwhile, I'm expecting deposits and other balance sheet items to grow somewhat in line with loans. The following table shows my balance sheet estimates.

| FY18 |

| FY19 |

| FY20 |

| FY21 |

| FY22E |

| FY23E |

| Income Statement |

| Net interest income |

| 41 |

| 44 |

| 45 |

| 61 |

| 78 |

| 92 |

| Provision for loan losses |

| 1 |

| 1 |

| 6 |

| 1 |

| 3 |

| 4 |

| Non-interest income |

| 9 |

| 11 |

| 11 |

| 16 |

| 19 |

| 18 |

| Non-interest expense |

| 30 |

| 33 |

| 32 |

| 36 |

| 45 |

| 50 |

| Net income - Common Sh. |

| 14 |

| 16 |

| 13 |

| 29 |

| 34 |

| 36 |

| EPS - Diluted ($) |

| 0.89 |

| 1.03 |

| 0.85 |

| 1.88 |

| 2.25 |

| 2.39 |

| Source: SEC Filings, Earnings Releases, Author's Estimates (In USD million unless otherwise specified) |

Although I have increased my net interest income estimate, my updated full-year earnings estimate for 2022 is lower than my previous estimate of $2.28 per share given in my last report on the company. My earnings estimate has slightly declined because of the substantial jump in non-interest expenses.

Actual earnings may differ materially from estimates because of the risks and uncertainties related to inflation, and consequently the timing and magnitude of interest rate hikes. Further, a stronger or longer-than-anticipated recession can increase the provisioning for expected loan losses beyond my estimates.

Maintaining a Buy Rating

OP Bancorp is offering a dividend yield of 4.3% at the current quarterly dividend rate of $0.12 per share. The earnings and dividend estimates suggest a payout ratio of 20% for 2023, which is below the last three-year average of 23%. Therefore, there is room for a dividend hike next year. However, to remain on the safe side, I’m not assuming an increase in the dividend level.

I’m using the historical price-to-tangible book (“P/TB”) and price-to-earnings (“P/E”) multiples to value OP Bancorp. The stock has traded at an average P/TB ratio of 0.94 in the past, as shown below.

| FY19 |

| FY20 |

| FY21 |

| Average |

| TBVPS - Dec 2022 ($) |

| 12.1 |

| 12.1 |

| 12.1 |

| 12.1 |

| 12.1 |

| Target Price ($) |

| 8.9 |

| 10.1 |

| 11.4 |

| 12.6 |

| 13.8 |

| Market Price ($) |

| 11.2 |

| 11.2 |

| 11.2 |

| 11.2 |

| 11.2 |

| Upside/(Downside) |

| (20.1)% |

| (9.3)% |

| 1.5% |

| 12.4% |

| 23.2% |

| Source: Author's Estimates |

The stock has traded at an average P/E ratio of around 7.8x in the past, as shown below.

| FY19 |

| FY20 |

| FY21 |

| Average |

| EPS 2022 ($) |

| 2.25 |

| 2.25 |

| 2.25 |

| 2.25 |

| 2.25 |

| Target Price ($) |

| 13.0 |

| 15.3 |

| 17.5 |

| 19.8 |

| 22.0 |

| Market Price ($) |

| 11.2 |

| 11.2 |

| 11.2 |

| 11.2 |

| 11.2 |

| Upside/(Downside) |

| 16.5% |

| 36.6% |

| 56.7% |

| 76.8% |

| 96.9% |

| Source: Author's Estimates |

Equally weighting the target prices from the two valuation methods gives a combined target price of $14.4 , which implies a 29.1% upside from the current market price. Adding the forward dividend yield gives a total expected return of 33.4%. Hence, I’m maintaining a buy rating on OP Bancorp.

For further details see:

OP Bancorp: Californian Economy, Interest Rates To Drive Earnings