LPRO - Open Lending: Downside Risks Accelerate As Auto Loans Market Stalls

2023-07-28 08:25:02 ET

Summary

- The deteriorating macro data in the US auto market, including vehicle sales and consumer loans, is yet to be reflected in the stock price.

- The company's financial results have been under pressure, with declining revenues and a compression of net income margin.

- Management insiders have been selling stock in recent months, and the options market is implying a bearish outlook.

Investment Thesis

Open Lending Corporation (LPRO) is a tech stock in the auto loans space, a sector which is starting to see rapidly deteriorating macro data in both vehicle sales and consumer loans. Whilst the stock is up over 60% year-to-date, it looks significantly overvalued and due to a correction. Both management guidance and analyst expectations are forecasting soft results for H2 2023, and this weakness is yet to be reflected in the stock price.

Company Summary & Industry Outlook

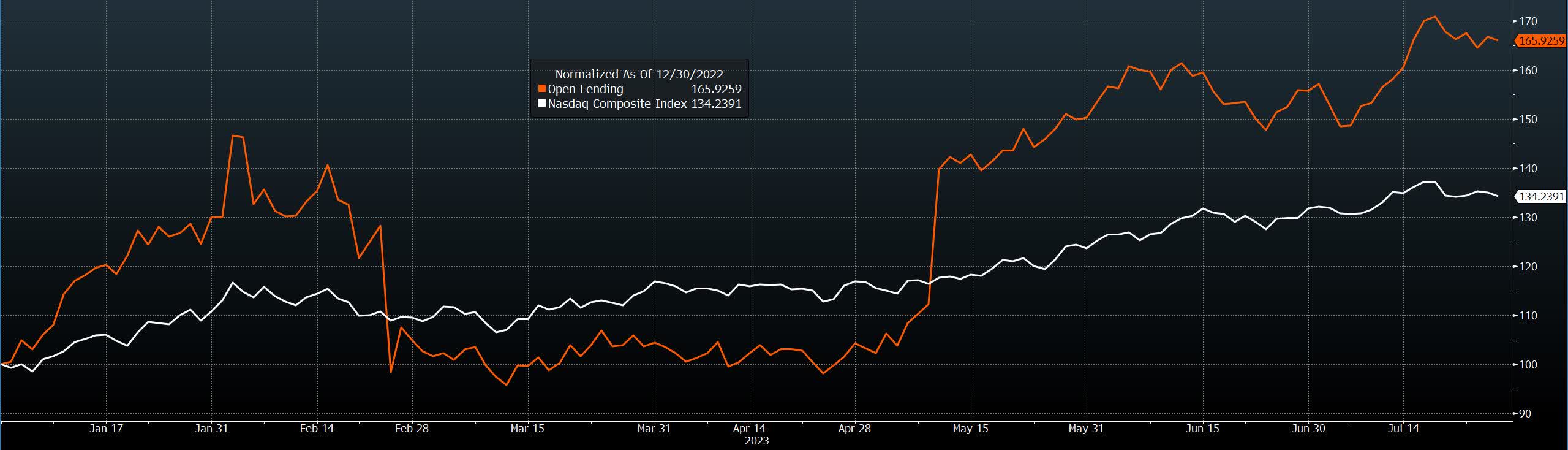

Open Lending is a financial services firm specializing in loan analytics, pricing, modeling, and automated decision technology for lending in the US automotive sector. The firm has over 20 years' worth of proprietary loan data, which helps banks and credit unions to better price and underwrite auto loans using scalable technology. The company's stock has had a phenomenal year so far, rising ~66% year-to-date, compared to the Nasdaq performance of ~34%, but the fundamentals in the auto market are deteriorating as a result of the tougher economic environment. The stock now looks to be in a dangerous, overvalued territory, and the sector and macro headwinds should drag the price down to lower levels.

Open Lending & Nasdaq 2023 (Bloomberg)

{kind=link}

Following the aggressive monetary tightening by the Federal Reserve to combat high and persistent inflation, the challenging and uncertain environment in the US is negatively impacting the consumer demand and subsequent loan originations for both new and used cars. At the same time, higher interest rates by the Fed have led to a tightening in liquidity and credit available for lenders as their own financing costs have increased substantially. We can see this negative trend in the Federal Reserve data below, consisting of auto loans held by US commercial banks. The drop in recent months is significant, which does not bode well for the future prospects and revenue generation for LPRO. Despite these growing headwinds, the stock is trading at periodic highs, which I believe is unsustainable, as the industry and market dynamics justify a drop in the stock valuation.

Auto Consumer Loans (Bloomberg, Federal Reserve)

{kind=link}

An additional industry dynamic to consider is the seasonality of US vehicle purchases. Using data from the Bureau of Economic Analysis on US total vehicle sales, we can analyze a seasonality heat map to identify persistent trends in the monthly selling patterns of the last 10 years' worth of data. From the below, Q2 and Q3 have historically not been strong periods of significant sales growth. The month of April has seen negative change every year over the sample period, and there is a similar trend in June, July, and September. Another highlight is the non-existent growth in April, May, and June 2023 data, which demonstrates how tough the current environment has become on auto sales.

US Vehicle Sales - Seasonality Chart (Bloomberg)

{kind=link}

Financial Results Under Pressure

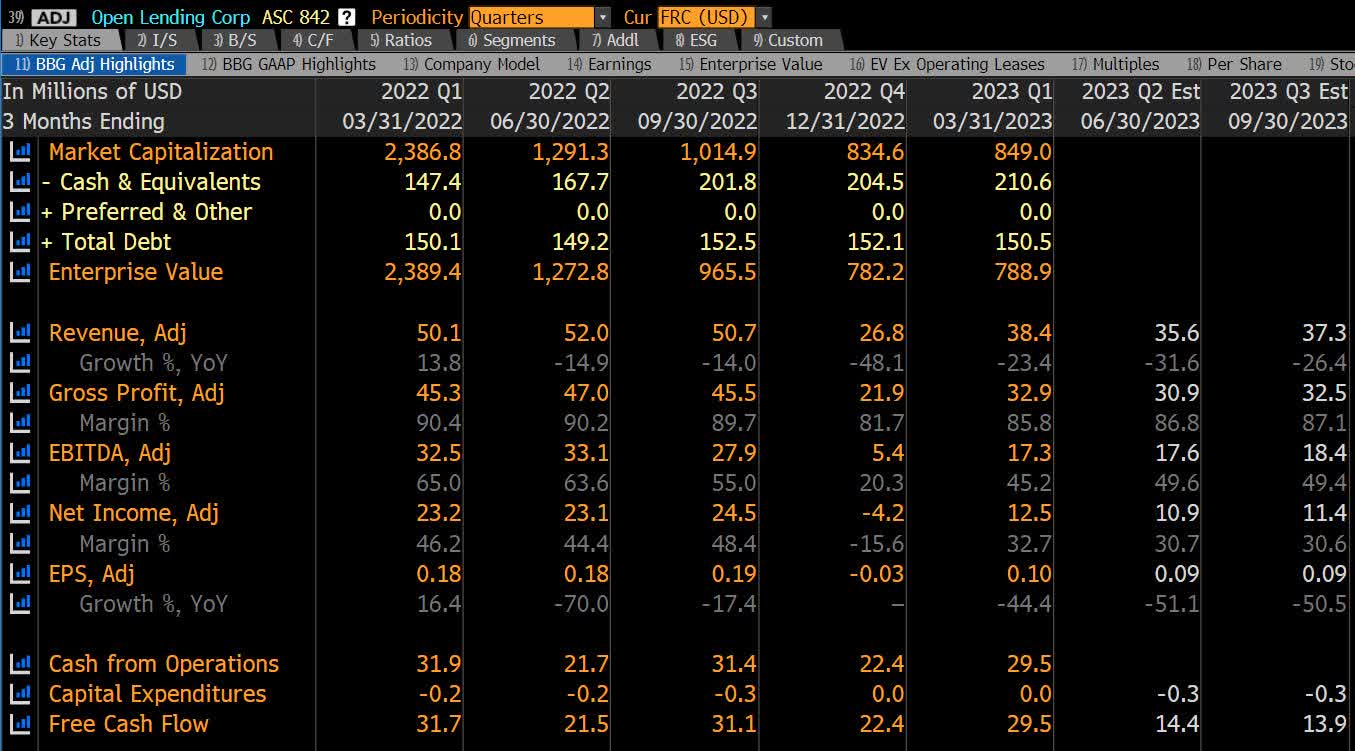

Despite the firm's scalable technology and favorable fundamentals around the low capex and high profit margin nature of their business, we can clearly see their struggles in top line financial performance, starting from the end of last year. As per the Bloomberg Financial Analysis Summary (below), in Q4 22, Revenues were down ~48% year-on-year, whilst Net Income was negative. More recently in Q1 23, Revenues rose marginally to $38.4 million, but are still down ~23% from the prior year. Looking at the analyst consensus for the next two quarters, further challenges are expected regarding lack of revenue growth, as well as a worrying compression of Net Income margin.

As per the recent company guidance , management are also expecting sequential declines in all of their key metrics (loan certifications, total revenues, adjusted EBITDA) in the Q2 23 results due to be released on August 08. The firm has also declined to give guidance for the rest of the 2023 fiscal year. Considering the rapid drop-off in the auto loans data recently, I believe both management and analyst forecasts run the risk of needing to be revised lower in upcoming periods, as the crunch in the auto loans market is only starting to materialize in the sector data. This warrants a downward correction in the stock price.

{kind=link}

Expensive Valuation

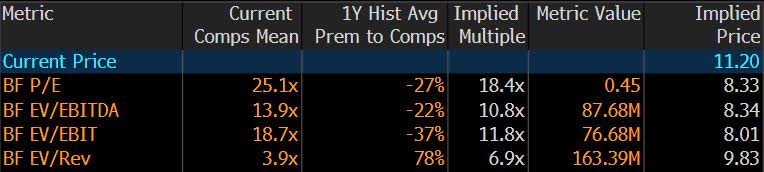

Using the Seeking Alpha valuation data relative to LPRO's peers, we can observe a clear overvaluation both using trailing twelve months data and forward-looking data. P/E GAAP ((TTM)) is currently 25.18x, significantly higher than the sector median of 10.15x, whilst P/E GAAP ((FWD)) is at a ~180% premium to the sector median.

This overvaluation view is reinforced by Bloomberg data that uses the 1-year average historical premium for LPRO to its comparables and applies this adjustment to calculate an implied multiple and implied price. Blended Forward (BF) data is a time weighted average of fiscal year 1 and year 2 forward estimates. Using this methodology and metrics, the target prices imply a ~25% drop from the current price.

Relative Valuation (Bloomberg)

{kind=link}

Management Sell Transactions

It is important to analyze recent management transactions to see if any buying or selling trends can be spotted to strengthen the fundamental thesis. In LPRO's case, within the Bloomberg Insider Transactions page, we can see significant selling activity in the last couple of months at the recent high prices. This is an ominous and bearish sign on the company prospects, as it indicates that the executive team view their stock as either fairly valued or overvalued at these levels, and they are taking advantage to offload a portion of their shareholdings. This reinforces my belief that a correction is due in the stock, as these insiders would arguably not be selling if they predicted significant upside in the second half of the year.

LPRO Management Transactions (Bloomberg)

{kind=link}

Negative Skew In Options Market

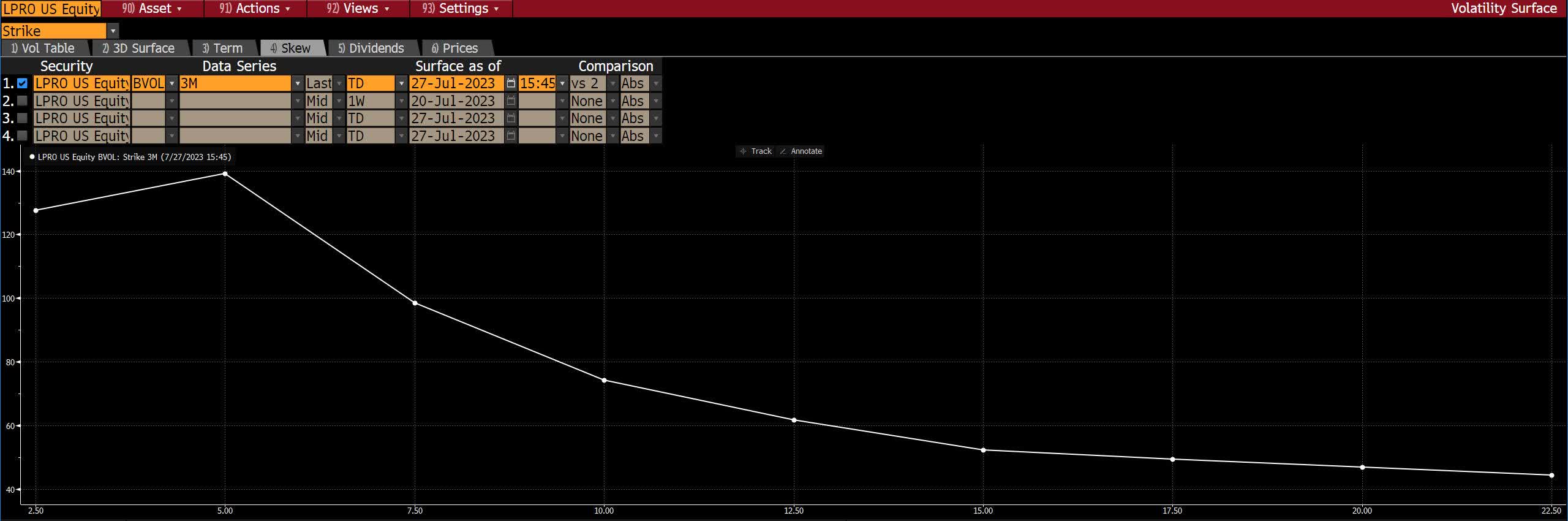

From a technical perspective, when looking at the current options market on LPRO, we can see a significant negative skew to the downside in the current implied volatility and demand for puts.

The skew below plots the implied volatility, a key input in the pricing of options, across strike prices both below and above the current stock price. The implied volatility, and thus option price, for the lower strikes (OTM puts) is significantly higher than those of the higher strikes (OTM calls). This indicates that market makers are charging higher option premiums for downside protection, which is generally driven as a result of higher demand for put options that will perform favorably if the stock price were to fall from the current high levels.

{kind=link}

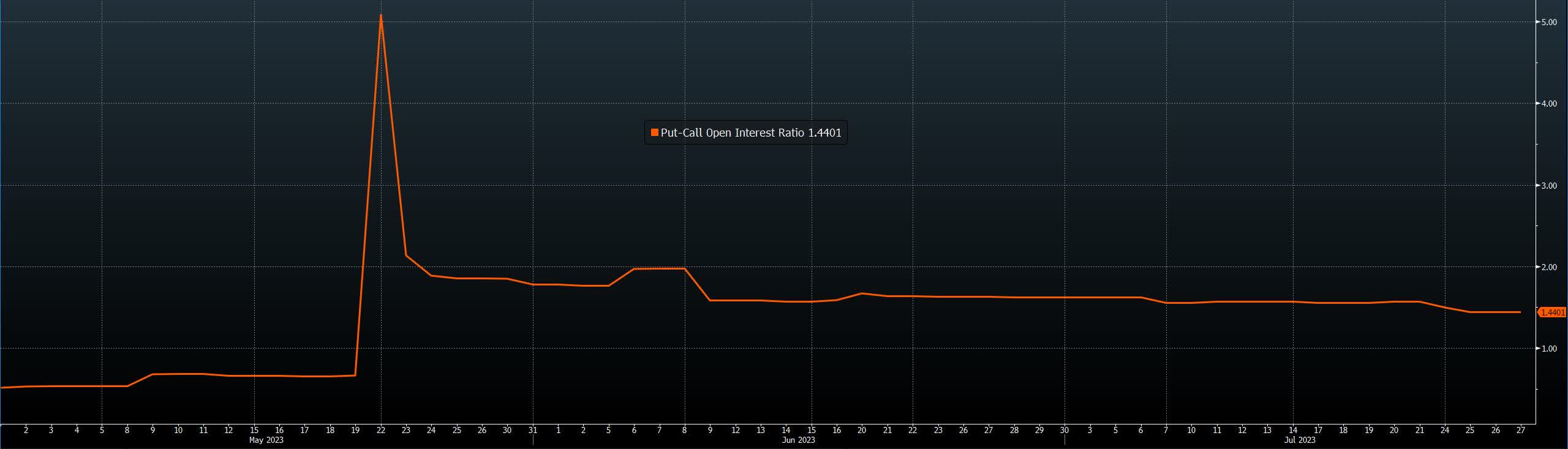

This view is further strengthened by the Put/Call ratio, which compares the current open interest for put options versus call options. A ratio value above 1 indicates greater demand and positioning in puts over calls, which implies investors are either protecting or preparing themselves to take advantage of a drop in the stock. We can see how the ratio spiked in May and has remained elevated since.

{kind=link}

Risks

The main risk to this thesis is that the macro concerns regarding the US consumer and the credit and liquidity of lenders in this segment are overstated, and that a drop in loans origination and demand recovers quickly from recent difficulties. This view could be supported by optimism that the Federal Reserve has likely reached their peak interest rate and that inflation has been dropping in recent months, whilst US unemployment and GDP data has remained resilient. A firm such as LPRO with a strong and scalable tech solution within this lending market would then face more optimistic prospects regarding a recovery in their top line revenue growth. However, due to the lagged nature of monetary policy and the seasonal consumer demands for auto purchases, I believe LPRO has a difficult second half of the year ahead.

In Conclusion

Overall, Open Lending is an interesting tech-driven company in the financial services segment of the auto sector, and the stock's recent performance show there is significant belief in their story. However, the firm's financials results and data from the auto sector have recently started telling a different tale, as the US macro environment and headwinds in auto demand and lending start to weigh down on the stock. At the same time, recent management sell transactions and pricing dynamics in the options market also fail to deliver confidence on the stock's outlook.

For further details see:

Open Lending: Downside Risks Accelerate As Auto Loans Market Stalls