FIBK - Open Letter To First Interstate Bank Board Of Directors After 11% Drop On Friday

Summary

- First Interstate reported 4Q 2022 earnings on January 27. Shares promptly fell 11% from the prior day close.

- An 11% one day decline can be a wakeup call to directors. It should be occasion to say: What is the market telling us?

- While the bank's 5.5% dividend yield is enticing on the surface, it tells directors that First Interstate is risky, another signal something is not right at the bank.

- As a long-term investor (since 2015), I have five questions for the board's independent directors.

- Holding First Interstate shares pending expected First Interstate response to Friday's double-digit loss.

February 1, 2022

I last wrote about First Interstate BancSystem , Inc. ( FIBK ) a year ago. At the time I expressed concern with the Great Western acquisition. I also expressed the view that the subsequent 16% decline in share price was evidence of FIBK being oversold.

At the time of the article being published, I doubled my position in FIBK at $36.85. I subsequently sold half of the newly acquired shares when FIBK's share price hit $40.

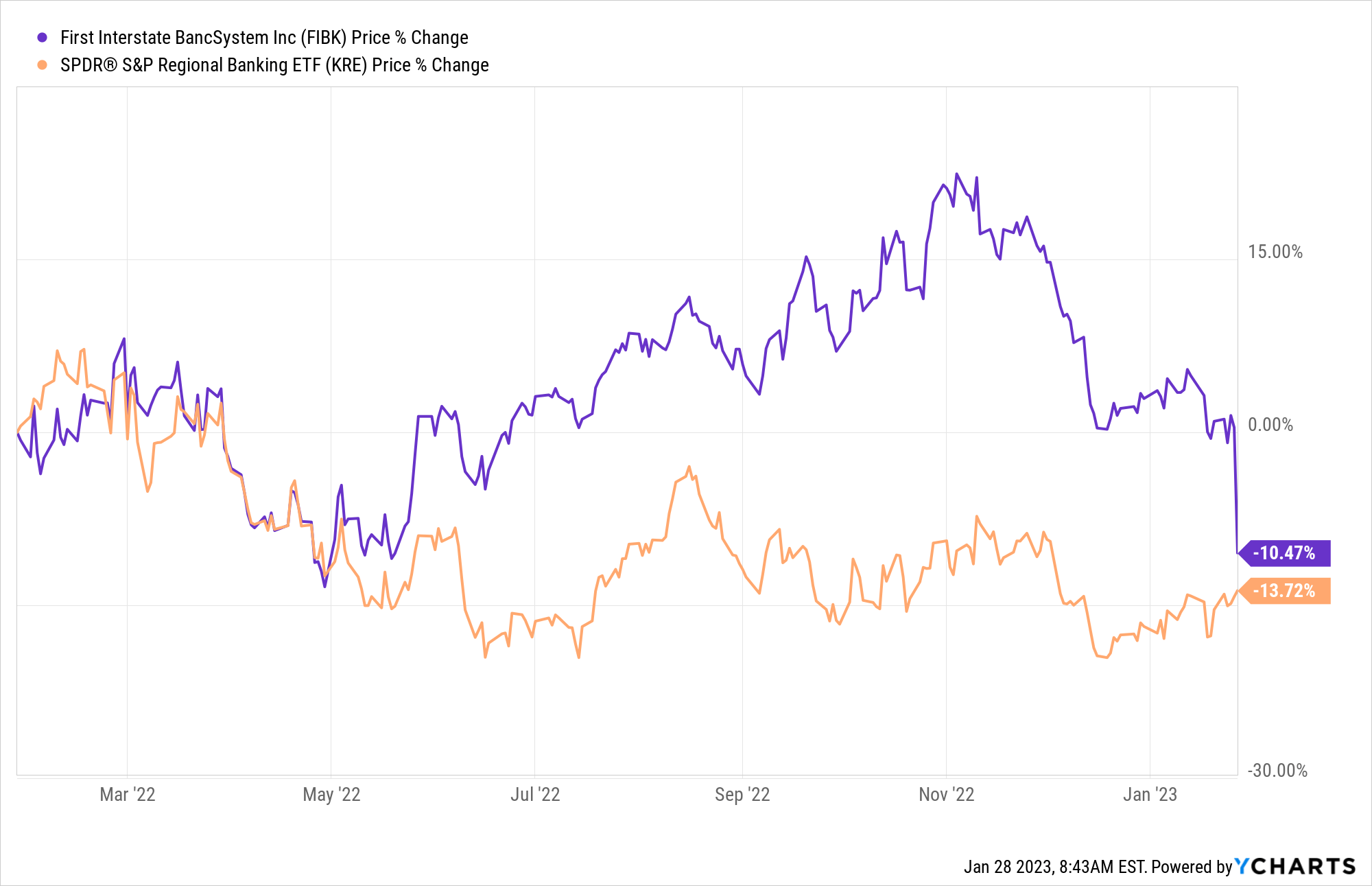

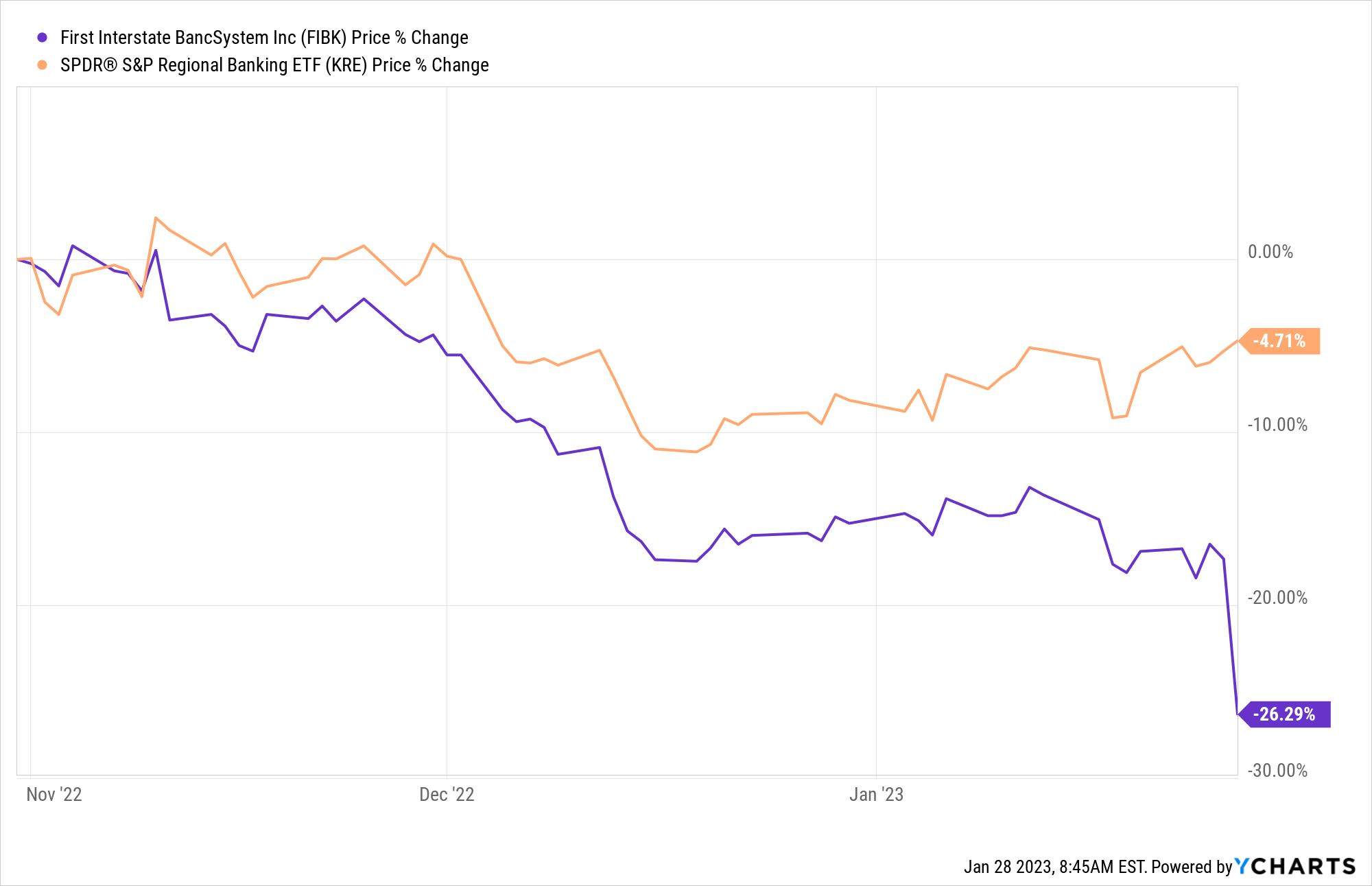

Share Price Action Past Year and since Oct. 31

Over the past year FIBK trails the SPDR S&P Regional Banking ETF ( KRE ) modestly as the chart below shows. The chart also shows that FIBK shares were up a bullish 20% as of late October. The second chart shows share price action since October 31: FIBK down -26%+ compared to a -4.7% decline for KRE.

{kind=link}

Share price FIBK (Ycharts)

{kind=link}

Share Price FIBK (Ycharts)

What Happened?

The obvious answer for why FIBK's shares have dropped -26% over the past 90 days is because the bank missed analyst earnings expectations. 4Q earnings came in at $0.82/share versus expectations of $1.03 .

But I do not think the big miss explains the big drop in price.

While missing analyst earnings expectations is a factor, five other factors also contribute meaningfully to why FIBK shares are falling. Those five factors form five questions for the board.

Five Questions for First Interstate Independent Directors

1. What is the bank's strategy for CAPITAL MANAGEMENT?

My sense is that the board is not treating the bank's capital as a precious resource. Too many moving parts. Trying to please too many factions?

Over the past year the bank has:

- Acquired Great Western , taking share count from 62 million shares to 109 million shares when buying an undistinguished banking franchise for a 25% premium.

- Increased the dividend from $0.41 per quarter to $0.47, a 14.6% increase.

- Repurchased five million shares.

- And as recently as the bank's most recent earnings call, expressed an interest in doing more M&A activity as soon as this year.

I urge capital caution. A dividend payout greater than 50% and talk of more M&A is a risky brew. Capital management discipline is not appreciated until problems (e.g., economy, unexpected losses, regulatory issues, political pressures, etc.) erupt.

2. Is it true that the Board is considering more M&A activity in 2023?

Here is a comment from CEO Riley's earnings call that I believe contributed significantly to the bank's -11% decline on Friday:

"But, as you probably know, there's a lot of banks out there for sale, but we're not interested in all the ones that are out there for sale. So, we're just, we're going to stick to our knitting and, and make sure this bank is, is, is performing at the ultimate level of performance. And then if something comes up that's, that we believe will increase the franchise value, we'll go to it. But nothing is right currently on the horizon."

The market hammers banks that do large M&A (large is compared to bolt-on acquisitions where the acquired bank is less than 20% the asset size of the acquirer). The market especially hammers banks that are serial acquirers. Why?

The market has a lot of history showing that acquirers suffer from three problems: 1) Over-optimism. 2) That leads to over-paying for acquisitions. 3) And the discovery of too many "one-time" expense surprises that linger on long past when the merger dust settles.

The $3.9 million one-time 4Q merger expense appears to be a surprise. This comes after management implied that the GWB merger was wrapped up in 3Q. Here are two quotes from the 3Q earnings call:

"It's worth noting that a lot of the positive momentum we have right now is the result of the successful execution of the integration of Great Western, which has worked out exceptionally well.

I would say that the cost saves at Great Western are done. The way we do acquisitions, we pretty much get rid of those right away, we don't have a linger on, that doesn't get any better over time. So, all the cost saves that we saw with the acquisition of Great Western are behind us."

First Interstate investors need the board to articulate publicly its plans for M&A in 2023-2024.

3. Is First Interstate now chasing deposits?

I have long appreciated First Interstate's strong core deposits and low loan-to-deposit ratio. In fact, it was this competitive advantage in the Mountain States that first attracted me to the bank.

CEO Riley articulated this competitive advantage in October:

"... strong, loyal, low-cost base that serves as a foundation of our franchise..."

The combination of the GWB acquisition with a rising interest rate environment is putting at risk FIBK's hard-earned reputation as a low-cost of deposit funding bank.

Evidence can be seen in the bank's big jump in deposit costs in 4Q. Comparisons to deposit cost trends at Glacier Bancorp, Inc. ( GBCI ) are not only appropriate, but reason for the board to assess its current view of loan growth, target loan-to-deposit ratios, and deposit pricing.

4. Back to M&A: Why not focus exclusively on Mountain State markets?

I am not a fan of the bank's decision to enter non-Mountain State markets where FIBK seems to lack competitive advantage. Deposit share in several of the non-Mountain states, per the most recent FDIC reports, is so small as to suggest the need for the bank re-examine its strategies for these markets.

It might be a very good idea to study the bank's current and future ROE in non-Mountain state markets. Markets that fail to meet a 10% ROE hurdle should be on the chopping block. It may be instructive to learn more about how the bank tracks direct costs and allocates indirect costs by state.

A board articulation of its geographic strategy is appropriate.

5. Can the board put in place a policy that prevents insider sales of FIBK shares when the bank is actively buying back shares?

I like share buybacks as much as any shareholder, but I am not a fan of insiders selling shares while the company is buying back shares. I recommend that the board put in place a policy that addresses what can be viewed as a conflict of interest.

Final Thoughts

My favorite comment from CEO Riley during the 4Q earnings call is this one:

"... we're going to stick to our knitting and, and make sure this bank is performing at the ultimate level of performance."

Clearly FIBK is one of the nation's premier banks which is why I remain a long-time investor. You "knit" well. Stay the course that put the bank in the enviable position of being a top-tier Mountain State bank.

Respectfully submitted,

Richard J. Parsons, shareholder

For further details see:

Open Letter To First Interstate Bank Board Of Directors After 11% Drop On Friday