OTEX - Open Text Corporation's Big Challenge Is Organic Growth In Fiscal 2024

2023-10-04 14:41:43 ET

Summary

- Open Text Corporation offers digital transformation software capabilities to organizations worldwide.

- The company's main offerings include information management, content cloud, business network cloud, security cloud, experience cloud, developer cloud, AI & analytics, and process automation.

- Open Text is aiming for 1-2% organic revenue growth in fiscal 2024 and has a focus on integrating its recent acquisition of Micro Focus.

- I'm in a wait-and-see mode, so I remain Neutral [Hold] on Open Text Corporation for now.

A Quick Take On OpenText Corporation

Open Text Corporation ( OTEX ) offers a range of digital transformation software capabilities to organizations worldwide.

I previously wrote about OTEX with a Hold outlook.

With a potentially higher cost of capital environment for a longer period, Open Text Corporation management will need to avoid any missteps as the market may punish such heavily indebted companies.

I remain Neutral [Hold] on OTEX until we see organic growth for the company in fiscal 2024.

OpenText Overview And Market

Canada-based OpenText was founded to provide a range of software and services related to information management, including strategic planning, domain expertise, and customer service solutions.

The firm is headed by CEO and CTO Mark Barranechea, who has been with the firm since 2012 and was previously president and CEO of SGI and Rackable Systems.

The company’s main offerings include:

-

Information management

-

Content cloud

-

Business network cloud

-

Security cloud

-

Experience cloud

-

Developer cloud

-

AI & Analytics

-

Process automation

The firm seeks new customers through its direct sales, marketing and business development efforts and through strategic partners and solution extension partners.

According to a 2022 market research report by Grand View Research, the worldwide market for information management was estimated at $89.3 billion in 2022 and is expected to reach $223 billion by 2030.

This represents a forecast CAGR of 12.1% from 2023 to 2030.

The main drivers for this expected growth are increasing information security requirements, ongoing risk management and the rising volume of data.

The chart below shows the historical and projected future growth trajectory of the U.S. enterprise data management market:

U.S. Enterprise Data Market (Grand View Research)

Major competitive or other industry participants include:

-

International Business Corp.

-

Oracle Corp.

-

SAP SE

-

Cloudera, Inc.

-

Amazon Web Services, Inc.

-

Teradata

-

MindTree Ltd.

-

Broadcom (Symantec)

-

Informatica

OpenText’s Recent Financial Trends

Total revenue by quarter has increased sharply recently due to its acquisition of Micro Focus; Operating income by quarter has fluctuated in recent quarters:

Seeking Alpha

Gross profit margin by quarter has moved upward recently; Selling and G&A expenses as a percentage of total revenue by quarter have also trended higher in recent quarters:

Seeking Alpha

Earnings per share (Diluted) have varied sharply in recent quarters, producing negative results in Q2 2023:

Seeking Alpha

(All data in the above charts is GAAP.)

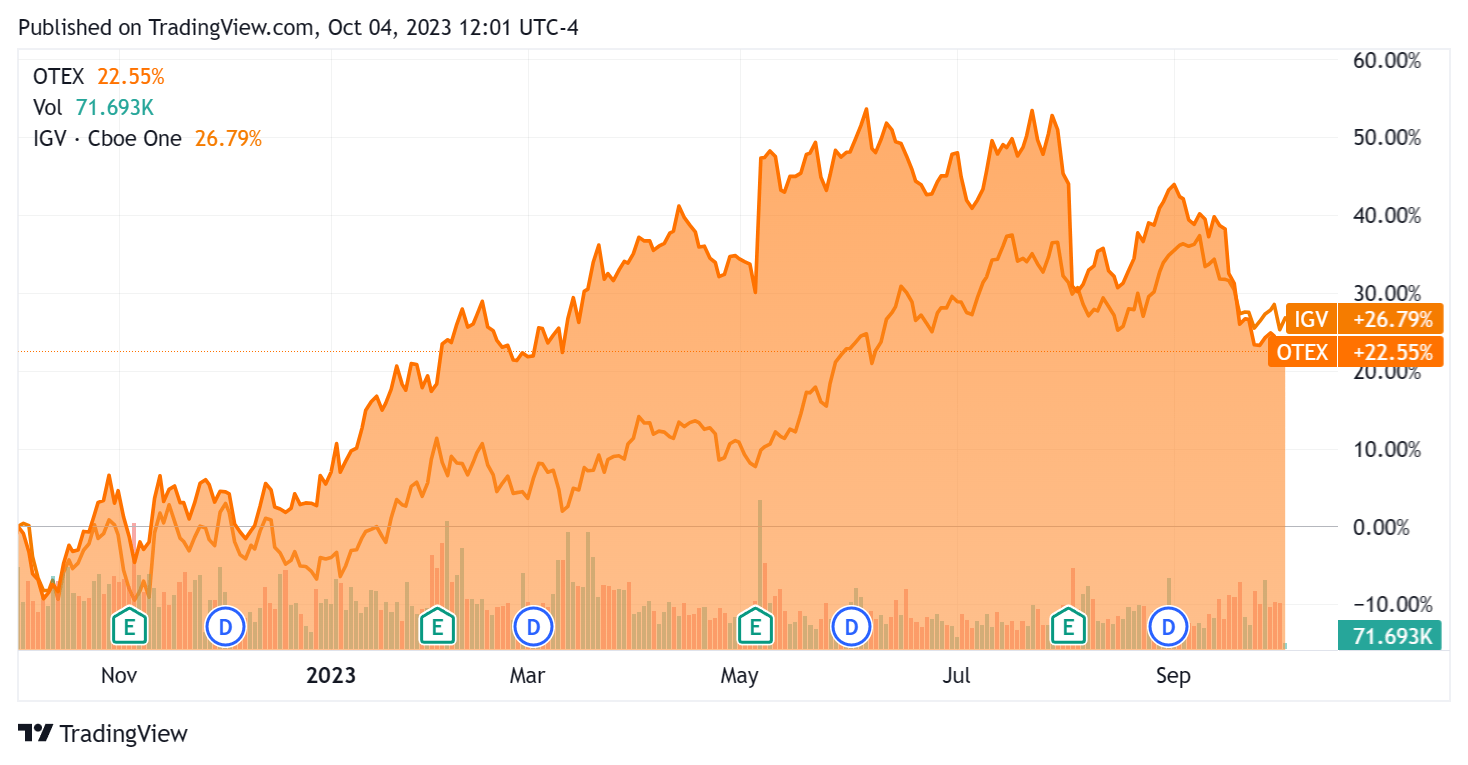

In the past 12 months, OTEX’s stock price has risen 22.55% vs. that of the iShares Expanded Technology-Software ETF’s ( IGV ) rise of 26.79%:

{kind=link}

For balance sheet results, the firm ended the quarter with $1.234 billion in cash, equivalents and short-term investments and $8.88 billion in total debt, of which $320.9 million was categorized as the current portion due within 12 months.

Over the trailing twelve months, free cash flow was $655.4 million, during which capital expenditures were $123.8 million. The company paid $130.3 million in stock-based compensation in the last four quarters, the highest trailing twelve-month figure in the past eleven quarters.

Valuation And Other Metrics For OpenText

Below is a table of relevant capitalization and valuation figures for the company:

| Measure [TTM] |

| Amount |

| Enterprise Value / Sales |

| 3.9 |

| Enterprise Value / EBITDA |

| 15.7 |

| Price / Sales |

| 2.1 |

| Revenue Growth Rate |

| 28.4% |

| Net Income Margin |

| 3.4% |

| EBITDA % |

| 24.8% |

| Market Capitalization |

| $9,400,000,000 |

| Enterprise Value |

| $17,410,000,000 |

| Operating Cash Flow |

| $779,200,000 |

| Earnings Per Share (Fully Diluted) |

| $0.56 |

| Free Cash Flow Per Share |

| $2.42 |

(Source - Seeking Alpha.)

OTEX’s most recent unadjusted Rule of 40 calculation rose to 53.2% as of FQ4 2023’s results, so the firm has performed well in this regard due to its Micro Focus acquisition, per the table below:

| Rule of 40 Performance (Unadjusted) |

| FQ3 2023 |

| FQ4 2023 |

| Revenue Growth % |

| 11.8% |

| 28.4% |

| EBITDA % |

| 26.1% |

| 24.8% |

| Total |

| 37.9% |

| 53.2% |

(Source - Seeking Alpha.)

Sentiment Analysis

The chart below shows the frequency of various keywords in management’s most recent earnings conference call with analysts:

Seeking Alpha

The firm faces foreign exchange headwinds with a strong dollar and is subject to many of the same macroeconomic risks as other software companies.

Analysts asked leadership about its M&A plans, best-performing areas and its Aviator system.

Management said that it is focused on integrating its recent major acquisition of Micro Focus and is not contemplating acquisitions in the near term.

It views AI as a future best-performing area and is building out its AI capabilities within its Aviator system, which is used by customers to automate tasks across numerous business functions.

Commentary On OpenText

In its last earnings call (Source - Seeking Alpha ), covering FQ4 2023’s results, management’s prepared remarks and presentation highlighted its goal of 1% to 2% organic revenue growth in fiscal 2024.

Free cash flow generation is targeted at $850 million at the midpoint of the range for fiscal 2024.

The firm also announced its OpenText.ai initiative, or "expanded AI strategy and road map," along with its Aviator generative AI system.

Management said that AI and analytics were currently about 5% of its revenue. Once leadership sees "clear revenue signals," it will communicate those to analysts and investors.

Total revenue for FQ4 2023 rose 65.2% YoY due to the Micro Focus acquisition, and gross profit margin increased by 1.2%.

Management didn’t disclose any customer or revenue retention rate data.

Selling and G&A expenses as a percentage of revenue grew by 1.6% YoY, and operating income was 14.3% higher than the same period in 2022.

The company's financial position is marked by nearly $9 billion in debt, ample short-term liquidity and strong free cash flow.

Looking ahead, management’s primary goal is to integrate Micro Focus into the company's operations and show that it can produce organic growth.

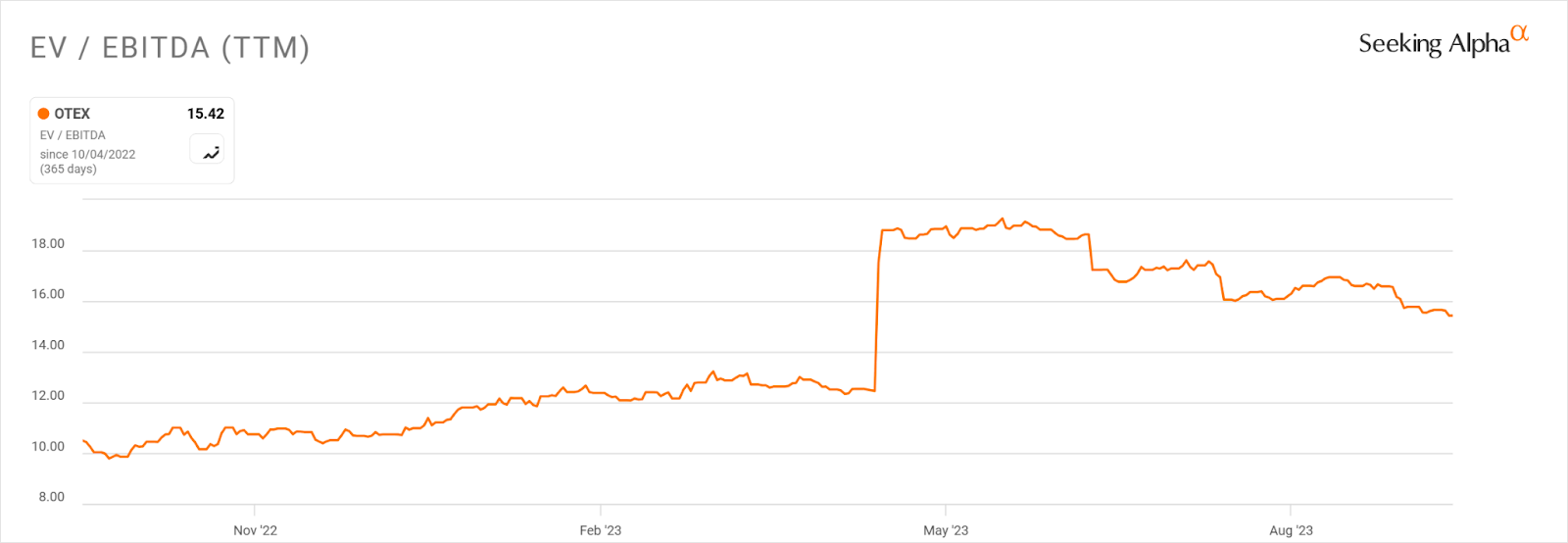

In the past twelve months, the firm's EV/EBITDA valuation multiple has risen 47%, as the chart from Seeking Alpha shows below:

EV/EBITDA Multiple History (Seeking Alpha)

{kind=link}

A potential upside catalyst to the stock could include strong client uptake of its new AI initiatives, although any revenue improvement will likely be minimal.

While management appears to be making the right noises about focusing on the Micro Focus integration, organic growth and increasing efforts for AI-enabled capabilities, I’m in a "show me" mode with the stock.

Also, with the market appearing to expect a higher cost of capital for a longer period, heavily indebted companies like OTEX may be disproportionately punished for any missteps.

Accordingly, I remain Neutral [Hold] on Open Text Corporation stock until management can prove it can grow the new combined entity organically.

For further details see:

Open Text Corporation's Big Challenge Is Organic Growth In Fiscal 2024