OTEX - Open Text: Leveraging Acquisitions For Stability And Growth

2023-05-18 18:06:18 ET

Summary

- Open Text's acquisition of Micro Focus will establish it as one of the largest software companies in the industry.

- Open Text has a track record of successful acquisition integration, but the challenging macro environment and lack of exciting Micro Focus products may present difficulties.

- Despite the challenges, Open Text's valuation, at approximately 4.8 times EV/CY24E revenue, is among the lowest in its peer group.

- I view the stock as a hold at current levels.

Investment Thesis

Open Text Corporation ( OTEX ) is a defensively positioned company in the sector, thanks to its track record of successfully integrating acquisitions and maintaining stable profit margins. The main concerns currently around the company revolve around the maturity of the markets in which OTEX operates and its limited organic growth. However, I believe Open Text's acquisition of Micro Focus will expand Open Text's portfolio, strengthening its presence in content management, cybersecurity and introducing new offerings in application modernization and IT operations. Hence, I view the stock as a hold at current levels.

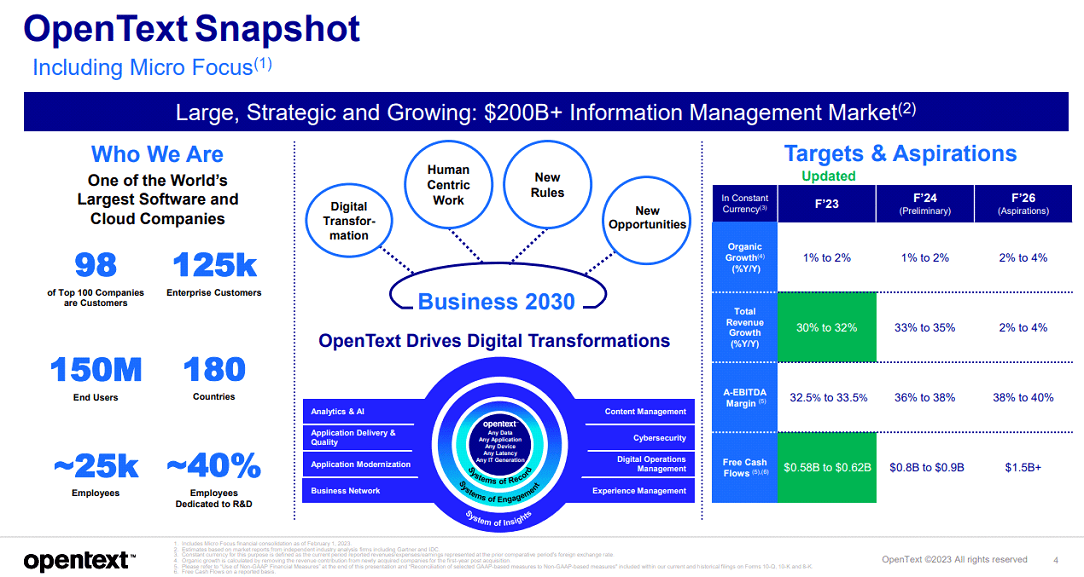

{kind=link}

Signs Of Positive Progress: Q3 Results Review

Open Text exceeded expectations in its third quarter of fiscal year 2023. Despite concerns in the market and the challenges of integrating Micro Focus, the company achieved better revenue and profitability. Looking ahead, the company forecasts cloud growth of 12-14% and total revenue growth of 30-32% for the full fiscal year 2023, both higher than market consensus. However, there will be a foreign exchange headwind on revenue amounting to $130-140 million. In terms of profitability, Open Text anticipates an adjusted EBITDA margin of 32.5-33.5%, slightly above market consensus. The company also reiterated its FY26 targets, aiming for organic revenue growth of 2-4% and an EBITDA margin of 38-40%. The standout achievement in this quarter was the contribution from the integration of Micro Focus, which exceeded company expectations at $374 million. While there is still work to be done to fully realize synergies and align Micro Focus with Open Text's margins and cash conversion, these results indicate progress in the right direction. Open Text has a track record of successful acquisition integration, but due to the scale of the Micro Focus acquisition, investors would probably like to see more data points regarding integration examples and cash conversion progress to further support positive sentiment towards the company's shares.

Declining Revenue Remains A Concern

The past few years have been difficult for Micro Focus, as evidenced by declining revenue in its major product categories. However, there are some areas of overlap between Micro Focus and Open Text's portfolio, particularly in content management and security. This presents an opportunity for cross-selling to the existing customer base. Open Text is relatively new in areas such as application modernization, application delivery management, and IT operations, and there is potential for improvement by reducing the emphasis on legacy assets. However, further clarity from management is needed on this matter. It is worth mentioning that Open Text successfully integrated Documentum, its second-largest acquisition prior to Micro Focus, to strengthen its core content management offering. Nonetheless, there are still reservations as Micro Focus is a larger and more complex entity to integrate.

IFRS to GAAP Conversion

Micro Focus has maintained a healthy adjusted EBITDA margin of approximately 35% over the past few years. However, the conversion from International Financial Reporting Standards ((IFRS)) to Generally Accepted Accounting Principles ((GAAP)) has posed a challenge, leading to a decline in adjusted EBITDA margins (29.3% in Q3). Despite this short-term setback, management guidance suggests a relatively rapid recovery, aiming for an adjusted EBITDA margin of 36-38% in FY24. This reversal is considered plausible due to Open Text's successful track record of increasing margins following the acquisitions of Documentum and Carbonite.

Micro Focus Acquisition Creates Execution Risk

Open Text's acquisition of Micro Focus for $6 billion, financed through approximately $1.4 billion in cash and $4.6 billion in debt, will make OTEX one of the largest software companies in the sector, with an estimated revenue of around $5.5 billion in the next twelve months. This acquisition expands Open Text's portfolio by adding a broader range of assets, increasing its presence in content management, cybersecurity, and introducing new offerings in application modernization and IT operations.

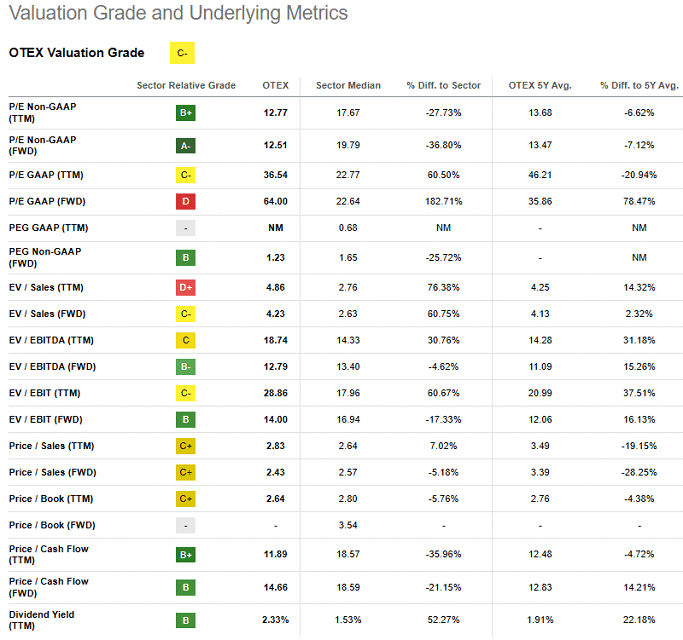

The integration of Micro Focus will be a complex and lengthy process to improve the company's revenue and free cash flow structure. Although Open Text has a solid track record of successfully integrating acquisitions, the challenging macro environment and the absence of a clear Micro Focus product that generates excitement will pose difficulties. I remain concerned about Micro Focus's declining revenue in recent years and the internal execution challenges that became more significant after its acquisition of HPE software. However, Open Text's valuation, at around 4.8 times EV/CY24E revenue, is one of the lowest among its peer group. I believe this lower valuation partly reflects the perceived risks associated with the acquisition, thereby setting lower performance expectations for Open Text.

{kind=link}

Conclusion

With a track record of successful integration of acquisitions and a consistent margin profile, I consider Open Text to be one of the more resilient companies in the sector. Over the medium to long term, I anticipate that Open Text will perform better than the market and increase its market share due to its strengthened product portfolio. While there are some execution concerns regarding the acquisition, I believe those are currently reflected in the company's valuation; hence, I view the stock as a hold at current levels.

For further details see:

Open Text: Leveraging Acquisitions For Stability And Growth