RBA - Openlane: Looking Good Under The Hood

2023-08-24 16:25:56 ET

Summary

- OPENLANE, a used car auction marketplace, is performing well despite a decline in the used vehicle market.

- Revenue for OPENLANE has increased, but profits have decreased due to impairments and other costs.

- The outlook for the company, both today and in the longer run, looks appealing and shares are cheap enough to warrant upside.

Like most Americans, the car that I own is not new. It never was while I owned it. To save money, I have always bought a used car. Sometimes, that goes really well. Other times, it doesn't. But for the most part, I am happy with the decision to stay away from new vehicles. Given how many Americans do buy used cars each year, it stands to reason that there would be a large market opportunity for any company that can operate a marketplace centered around auction services for used vehicles. Of course, no business like this can be truly digital. For instance, OPENLANE ( KAR ), previously known as KAR Auction Services, has historically owned its own logistics center operations in various parts of North America. Recently though, even though you would think that the used car market would be hot during a time of inflationary pressures, financial performance for the business has been rather mixed. Revenue has been growing nicely, but profits have been somewhat mixed. The good news, however, is that when you dig down into the cash flow data, you find a company that is doing quite well. Add on top of this how cheap shares are, and I have no problem keeping the company rated a ‘buy’.

Doing well in tough times

This year is looking to be rather interesting when it comes to the used automotive space. According to one report published in July by Cox Automotive, the used vehicle market is facing some pain. What the company calls the Manheim Used Vehicle Value Index dropped to a value of 215.1 in June. That represents a 10.3% decline compared to the same time one year earlier. Wholesale used vehicle prices, meanwhile, dropped 4.2% in June after adjusting for mileage and issues of seasonality. On an unadjusted basis, prices were down 3.8% for the month and were down 10.1% year over year.

{kind=link}

Author - SEC EDGAR Data

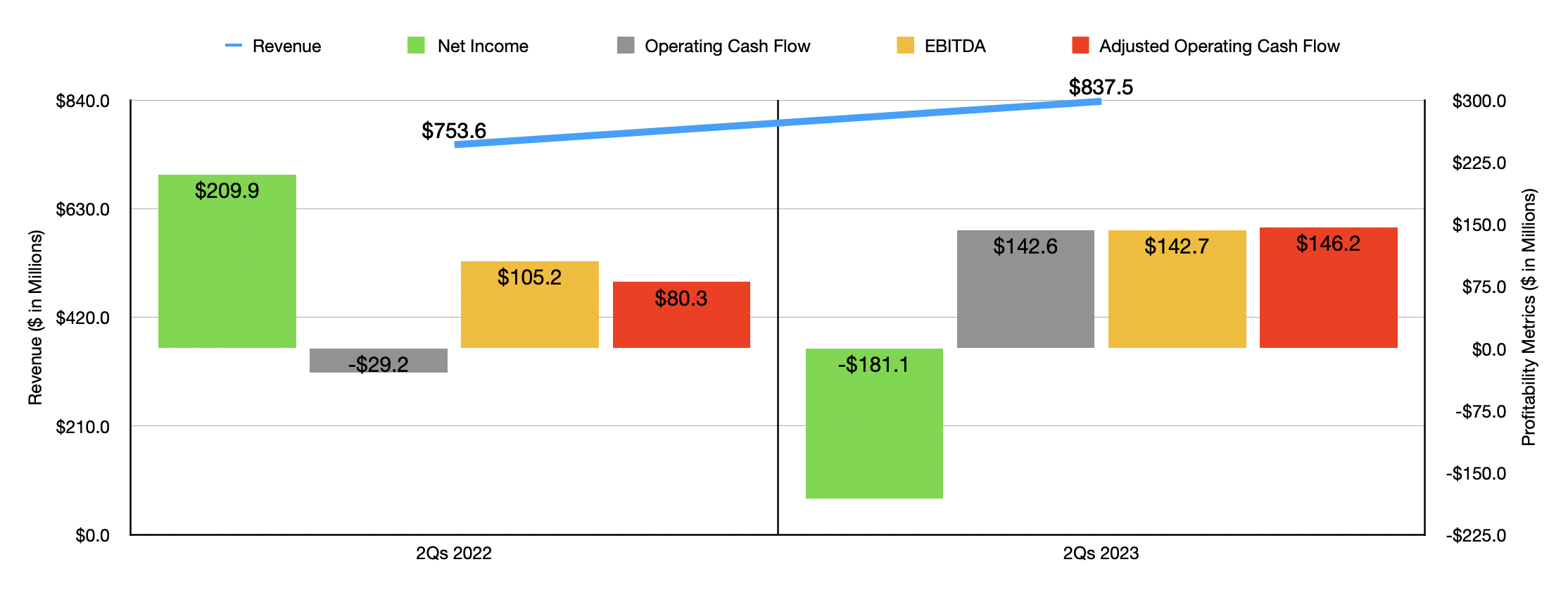

Typically, you would not expect this to bode well for a company that relies on used vehicle sales. However, OPENLANE has performed just fine. Revenue during the first half of 2023 , for instance, came in at $837.5 million. That's 11.1% higher than the $753.6 million the company reported one year earlier. The largest chunk of this sales increase came from service revenue. Sales here jumped $36.5 million, or 13% year over year, largely because of increases in repossessions and higher remarketing fees of $14 million. Third party platform fees also added $8.9 million to sales revenue, while transportation revenue and inspection service revenue also helped on this front. Purchased vehicle sales happened to be second place, with revenue jumping $23.8 million year over year. That rise, management said, was largely the result of an increase in purchased vehicles sold and average selling prices being higher for purchased vehicles sold in Europe. Higher interest rates also helped the company, with gross interest income jumping $32.8 million year over year. However, a jump in the firm’s provision for credit losses partially offset this.

Even though revenue for the company increased nicely, profits tanked, with net income of $209.9 million turning into a net loss of $181.1 million. It is important to note, however, that the bulk of this increase came from impairments totaling $261.8 million. The real story is on the cash flow side. Operating cash flow for the company went from negative $29.2 million to positive $142.6 million. If we adjust for changes in working capital, we get an increase from $80.3 million to $146.2 million. And finally, EBITDA for the firm expanded from $105.2 million to $142.7 million.

{kind=link}

Author - SEC EDGAR Data

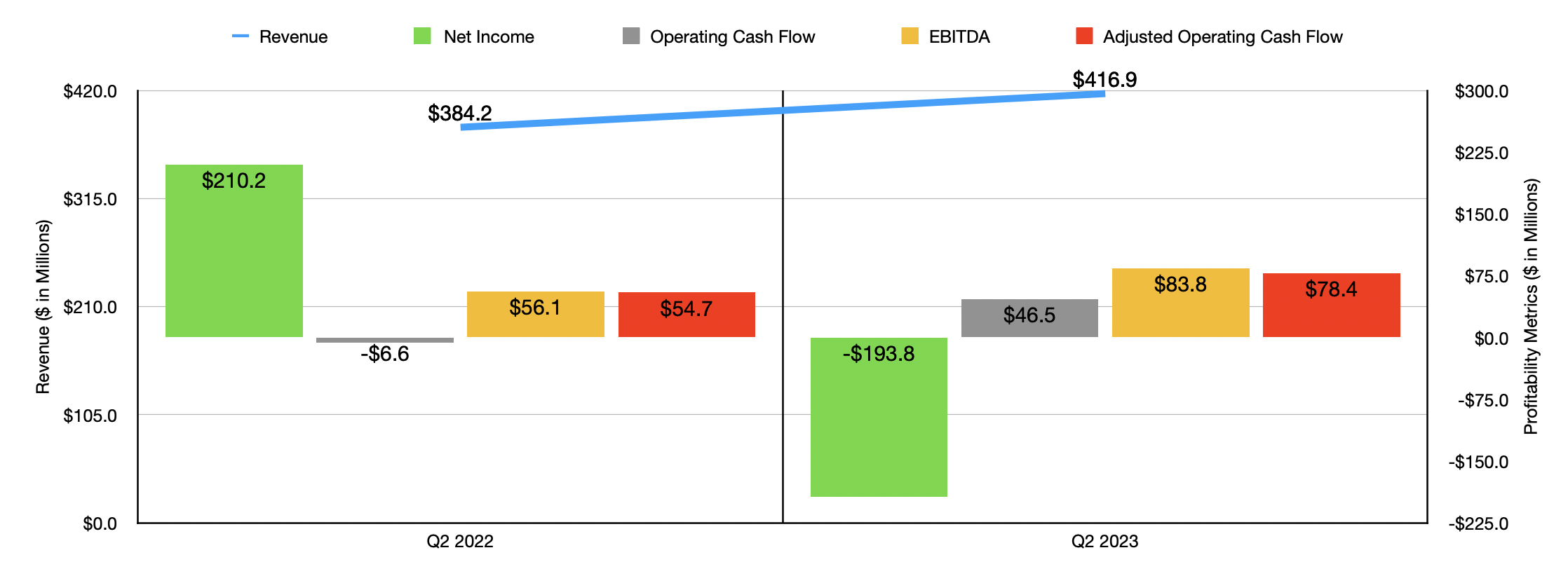

The financial picture for the company in the second quarter of 2023 alone looked very similar to what it was for the first half of the year in its entirety. In the chart above, you can see that revenue increased. Net profits tanked because of the timing of the aforementioned impairments. However, cash flows came in strong year over year. This is absolutely great to see for any company, especially one that's operating in an industry that is not doing particularly well right now.

I would make the case that, while the past is absolutely important, we also should be paying attention to what the future holds. We have both the long term and short-term picture here. In the long run, for instance, management remains very optimistic about the market potential. They see the addressable market for used vehicles being around 60 million units per year. About 40 million of these should be under the retail side, while 20 million should be under the wholesale side. To put this in perspective, in 2022, the company transacted 1.3 million vehicles online with $23 billion in gross merchandise value. So the potential to scale from here is significant. This massive market should be supported by 100,000 participants that largely consists of dealers and other commercial sellers and buyers. And as recent financial performance has shown, the company plans to cater not only to the digital marketplace side of things, but also to the physical side. The repossessions are one such example of the latter.

{kind=link}

Author - SEC EDGAR Data

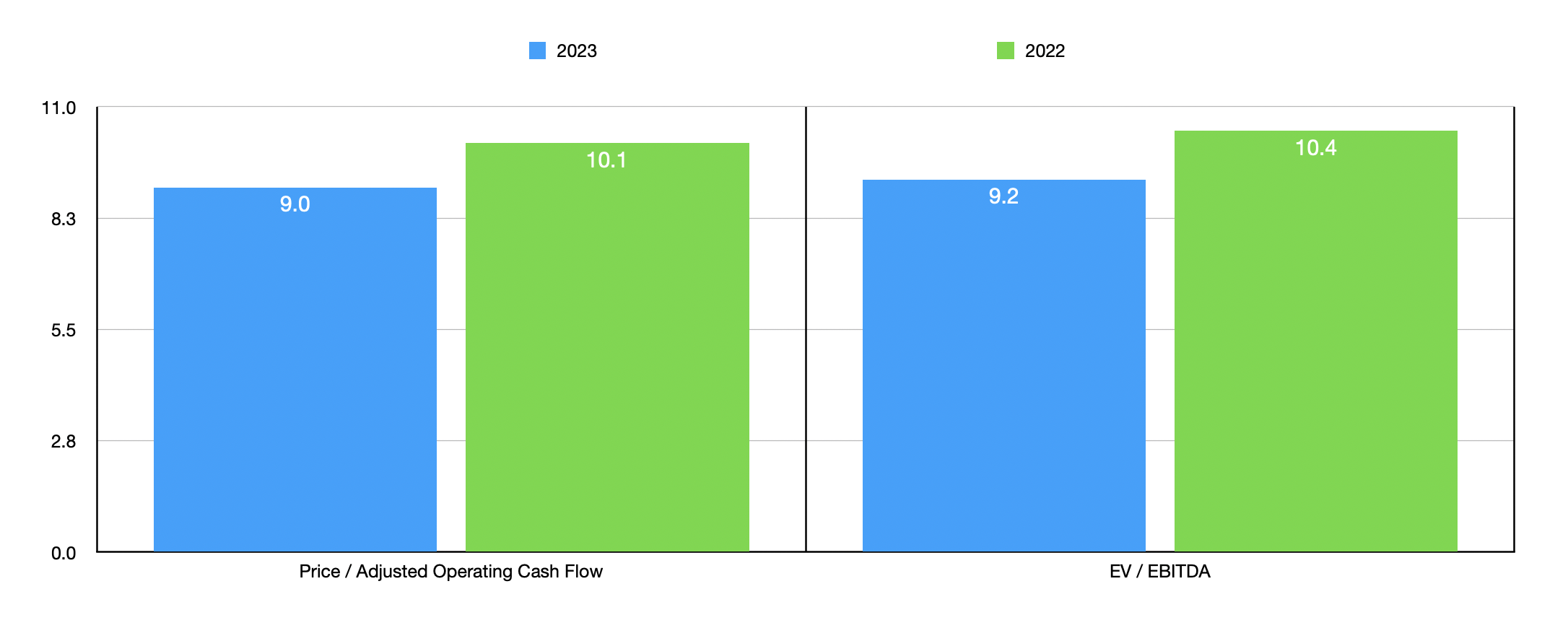

In the nearer term, we do have a financial outlook provided by management. The current expectation is for EBITDA this year to be between $250 million and $270 million. No guidance was given when it came to adjusted operating cash flow. But if we assume that it will increase at the same rate that EBITDA is forecasted to at the midpoint, we would get a reading of $183.6 million. Using these figures, I created the chart above. As you can see, the stock does look a bit cheaper on a forward basis compared to what we would get using data from 2022. But, I would argue, shares look attractively priced in either scenario. Of course, shares are not just attractive on an absolute basis. They are also attractive relative to similar firms. In the table below, you can see the company compared to three similar firms. On a price to operating cash flow basis, only one of the three companies was cheaper than KAR . And when it comes to the EV to EBITDA basis, it was the cheapest of the three firms that had positive results.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| OPENLANE |

| 9.0 |

| 9.2 |

| ACV Auctions ( ACVA ) |

| 118.7 |

| N/A |

| RB Global ( RBA ) |

| 23.9 |

| 24.7 |

| CarParts.com ( PRTS ) |

| 3.1 |

| 14.3 |

Takeaway

Fundamentally speaking, financial performance may have been somewhat mixed recently. But for the most part, things are looking good under the hood. Cash flows are improving and shares look cheap on both an absolute basis and relative to similar enterprises. It is true that the industry itself is facing some challenges. And I fully expect that this will weigh on the near-term potential for the company. But when you focus on the long haul, the picture looks undeniably attractive. Given these facts put together, I have no problem rating the company a ‘buy’ at this time.

For further details see:

Openlane: Looking Good Under The Hood