OPRA - Opera: It's Time To Be Greedy As Its Bubble Imploded (Rating Upgrade)

2023-12-12 12:30:00 ET

Summary

- The Opera stock has imploded since I tagged it with a Sell rating in July. Late buyers who chased were hammered, learning an expensive lesson.

- Opera has continued to deliver on its operating performance, although its surging growth rates have likely peaked. As a result, a growth normalization phase could follow.

- Opera's focus on improving monetization drivers and its niche in the gaming market could present more robust opportunities to reignite growth in 2024.

- I argue why I've decided to upgrade my thesis on OPRA, as over-optimism in the stock seems to have been deflated.

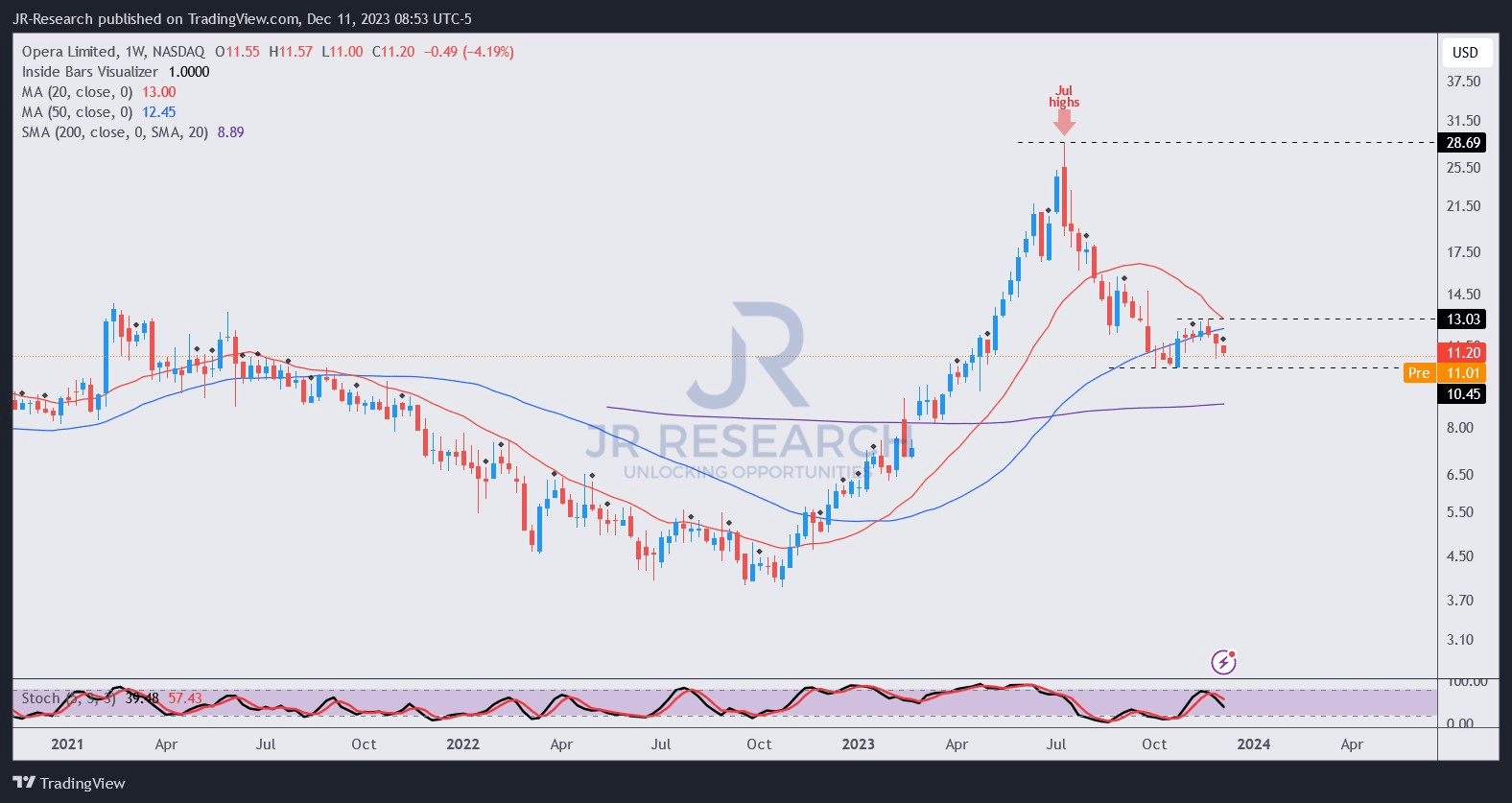

Opera Limited (OPRA) investors have been teetering on the edge over the past few months since I downgraded OPRA to a Sell/Underperform rating in July 2023 to the chagrin of the overly-optimistic OPRA Bulls (OPRA is down almost 45% since my July update). I updated investors that the mixed shelf offering by the company shouldn't be understated, as OPRA surged to its top in the same month. I then upgraded OPRA to a Hold/Neutral rating in September 2023, anticipating that the downward momentum could continue, but the risk/reward had turned more balanced. Even that upgrade proved too early, as OPRA fell another 11% since then, underperforming the S&P 500 ( SP500 ) significantly, as the market posted a 7% uptick.

As a result, late OPRA investors who chased its unsustainable upside have likely learned an expensive lesson. Given OPRA's recent developments and Opera's third-quarter or FQ3 earnings release since my last update, I believe it's an appropriate time to help investors decide whether to return to the battered stock.

Interestingly, OPRA posted a double-beat on revenue and adjusted EPS in FQ3, suggesting that the company has continued to execute well. Seeking Alpha's Quant "A+" earnings revisions grade corroborates my observation. It also led to an initial surge in OPRA in late October 2023, but the upward recovery faced a stumbling block at the $13 level as sellers returned. As a result, I believe investors were likely concerned about whether the best days in its incredible growth phase could be over.

Management provided a better-than-expected guidance for Q4 and FY23. As a result, analysts' estimates have also been upgraded, expecting Opera to post revenue growth of 16.6% in Q4. While Wall Street projects full-year revenue growth of 19.7% for FY23, it's clear that Opera's surging run could end.

Despite that, Opera is still assigned a best-in-class "A+" growth grade by Seeking Alpha's Quant, further bolstered by an attractive "B+" valuation grade. In other words, I believe it's possible that OPRA could be bottoming out, as management highlighted several opportunities in 2024 that could pan out.

Accordingly, Opera is working on improving its monetization drivers to improve ARPU further. Management updated that it experienced an increasing share of " Western users " in its active user base, which monetized more attractively. As a result, the company posted an 11% QoQ growth in ARPU, "reaching a new high of $1.31."

Furthermore, Opera also sees its niche focus on gaming users playing out nicely in Q3, notching a "10% sequential increase to 26M MAUs during the third quarter." As a result, it helped improve its GX-based ARPU to an annualized $3 rate, sustaining its growth inflection in GX. Opera presented to investors that its GX efforts are still nascent, achieving a penetration rate of just 7%. As a result, it sees a substantial opportunity in this segment, predicated on its AI and gaming expertise, coupled with the improvement in its advertising growth drivers.

Opera has proved its mettle in the browser market, notwithstanding its smaller scale. As a result, I believe the company has provided sufficient confidence to continue to scale profitably. Therefore, it should undergird its ability to continue improving operating leverage and develop a sustainable long-term network effect moat, which Google ( GOOGL ) ( GOOG ) has exploited to become a core market leader.

{kind=link}

As seen above, OPRA dip buyers have attempted to support its consolidation at the $11 level. However, the upward momentum failed at the $13 level as the post-earnings recovery dissipated.

Despite that, I see constructive price action as long as OPRA's $11 level isn't decisively broken down by intense selling pressure. Therefore, I assessed that the risk/reward profile has improved, with the $11 level as a critical support zone to add more aggressively if re-tested successfully.

Rating: Upgrade to Buy.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Please always apply independent thinking and note that the rating is not intended to time a specific entry/exit at the point of writing unless otherwise specified.

We Want To Hear From You

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn't? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!

For further details see:

Opera: It's Time To Be Greedy As Its Bubble Imploded (Rating Upgrade)