OPRA - Opera Q2 Earnings: A Silver Lining - Rewarding Dividend At 5%

2023-08-24 14:42:57 ET

Summary

- Opera's stock price has been affected by concerns about major shareholders selling their holdings, but the company remains highly profitable.

- The recent flattening in Opera's user growth raises questions about its growth trajectory, but the company's revenue guidance suggests ongoing stability.

- Opera's profitability profile, attractive dividend yield, low valuation, and strong balance sheet make it an appealing investment option.

Investment Thesis

Opera ( OPRA ) the web browser delivered results that didn't appease bears. As readers will know, the stock has been on the back foot since it renewed its shelf filing last month , noting that its biggest shareholders may look to exit a portion of their holding.

Meanwhile, the business remains highly profitable. And by my estimates, the stock is priced at 14x next year's EBITDA. Ultimately, there's a lot to be attracted to Opera, particularly given that this tech company is now paying out a +5% dividend yield on its stock or $0.80 per share .

Why Opera? Why Now?

As we headed into the earnings print, I wrote up an earnings preview earlier this week as to what sort of elements I was looking for.

{kind=link}

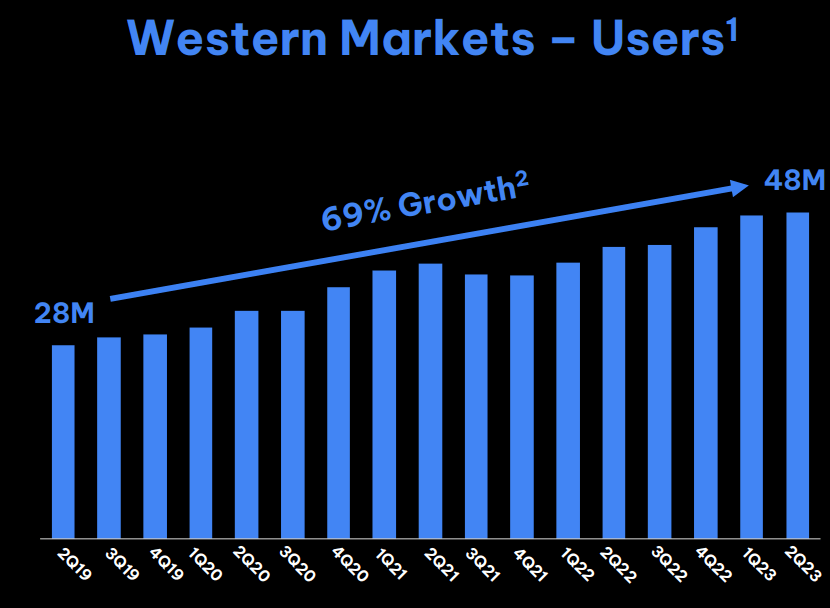

As the title of that analysis remarks (Focusing On User Base Stability) I was eager to see if Opera's Western user base, its higher value users, could continue to grow.

As it turns out, it appears that sequentially, there's been a flattening in Opera's user growth from Q1 2023 into Q2 2023.

While this doesn't destroy my bull case, I have to admit that it does make my bull thesis slightly less enticing. To be clear, this in and of itself, isn't such a dealbreaker, and there are other worthwhile bullish considerations that keep me bullish on the back of this report, but there is a partial denture to a super tight bull thesis from Opera.

Guidance Didn't Astound Investors

{kind=link}

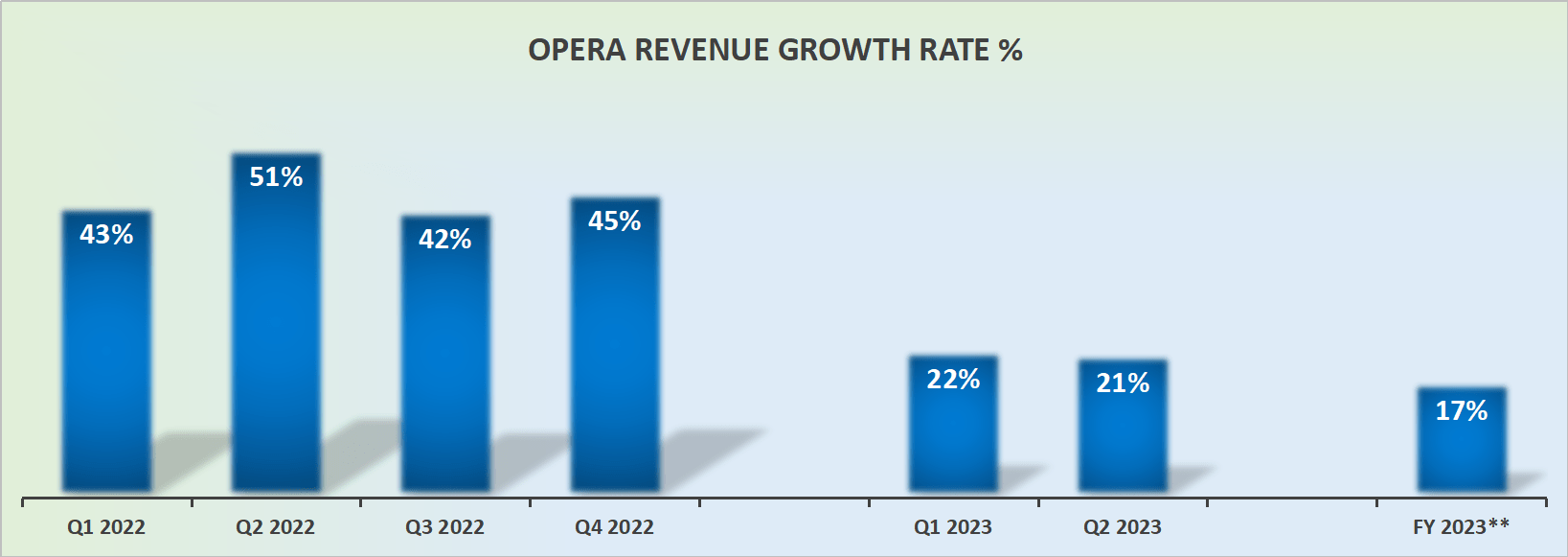

Opera slightly raised its full-year outlook. Or perhaps, a better way to put it is to state that Opera increased the lower end of its 2023 revenue guidance, but left its top end unchanged.

This is yet another of those pesky matters that I've already noted surfaced in this earnings report.

In practice, this means that the outlook for the remainder of 2023 is likely to see Opera's revenue growth rates dip into the mid to high-teens. Why is this a problem?

It tells me that Opera's strong growth rates, over the past 10 quarters, when Opera could be counted on to deliver premium revenue growth rates of more than 20% are now in the rearview mirror.

For investors who were eager to buy into Opera's turnaround growth story as one that was taking market share away from the search giant Goliath, I have to declare, that this is not a great setup.

Profitability Profile is Still the Bull Case

Moving on, the reason why I'm bullish on Opera has less to do with its growth trajectory and more to do with the underlying fact that this stock is cheaply valued.

OPRA Q2 2023

As you can see above, with the passage of time, Opera has succeeded in increasing its underlying profitability.

Case in point, Opera's diluted earnings per ADS (you can think of this as EPS), went from negative $0.05 in last quarter's Q2 2023 to positive $0.15 per diluted ADS this time around. Unquestionably a strong improvement, which lead to a $0.03 beat per ADS.

That being said, given that H1 2023 saw Opera's adjusted EBITDA reach just over 23%, the fact that H2 2023 is pointed towards around 19% to 20%, implies a significant step-down in profitability relative to the first 6 months of the year.

Accordingly, this reinforces my argument here, that Opera was shinning very strongly in H1 2023, but that the outlook for H2 2024 doesn't appear as enticing.

Nevertheless, Opera has announced an attractive semi-annual dividend that reaches $0.80 per ADS (per American Depositary Share). Accordingly, investors right now are getting around a 5% dividend, on top of any progress the company is making to grow its intrinsic value. And this I believe helps support its overall market valuation. After all, who doesn't like a nice dividend on a growth tech stock? I know I do.

For my part, I estimate that Opera is priced at 17x EBITDA. A multiple that makes an investment in Opera right now than satisfactory, despite all the blemishes to the bull case that I've already noted here.

Indeed, if we presume that into next year, Opera's EBITDA will grow by 15% y/y to $100 million, this implies that investors are being asked to pay 14x next year's EBITDA.

Further, Opera has no debt on its balance sheet and ample cash. Also, Opera has a 9.5% stake in OPay, valued on the balance sheet at around $220 million.

In sum, the dividend, plus strong cash flows, plus clean balance sheet, make this an attractive investment.

The Bottom Line

The recent dip in its stock price due to concerns about major shareholders exiting some of their holdings has piqued my interest. Despite this uncertainty, Opera continues to demonstrate strong profitability, with a current valuation of 14x next year's estimated EBITDA. What's particularly appealing is that Opera is now offering a dividend yield of +5%, translating to $0.80 per share.

While the recent flattening in Opera's Western user growth from Q1 to Q2 2023 raises questions about its growth trajectory, the company's revised revenue guidance for 2023, while not astounding, suggests ongoing stability.

Opera's profitability profile remains a key attraction, with a consistent increase in underlying profitability over time. Although H2 2023 might witness a slight dip in profitability compared to the first half of the year, Opera's enticing semi-annual dividend, combined with a low valuation at around 17 times EBITDA, makes it a compelling proposition. With a debt-free balance sheet and a significant stake in OPay, valued at approximately $220 million, Opera seems worthy of consideration for investors seeking value and a nice dividend.

For further details see:

Opera Q2 Earnings: A Silver Lining - Rewarding Dividend At 5%