OPRA - Opera: Risk/Reward Enticing Here Options In Play

2023-10-10 09:23:34 ET

Summary

- The company's share price has dropped significantly, presenting an enticing risk/reward opportunity.

- The announcement of a secondary shelf offering is seen as positive for shareholders and will reduce control from Kunlun and the CEO.

- The company's financials are sound with a strong cash position and low debt, but improvements are needed in ROA, ROE, and ROIC.

Investment Thesis

Opera's (OPRA) share price plummeted around 60% since its highs when it surged over 600% from October ’22 lows. I wanted to take a look at the company’s financials to see if, fundamentally, the company is sound, which it looks like it is. Some improvements would be needed, however, at this price, the risk/reward seems enticing, and I will be looking to start a position via options over the next couple of months.

What happened?

So, it seems that a lot of investors got quite scared of the company’s announcement of a mixed-shelf offering of around $300m. This would usually dilute the current shareholders; however, it seems like this is going to be a secondary shelf offering, which means that no shares will be created, rather, existing parties that own a lot of shares like Kunlun Tech Ltd and Keeneyes Future Holding Inc. These two parties have 128m and 12.7m of ordinary shares, respectively. I believe that this offer is a positive for all the shareholders because it will not dilute anyone as far as I know and will relinquish some of the control from Kunlun and the CEO, Mr. Zhou.

Another thing that the investors don’t like is the company is heavily tied to China, which controls the company quite a lot, as you can see from the previous paragraph. This offer will lessen the control and should be beneficial for all. The mixed shelf offering also doesn’t mean that the parties will sell that amount right now or ever, it just means that the company won’t need to file with the SEC again in the future whenever they do intend to sell their shares. The letter here should provide a little more clarification.

Financials

As of Q2 ‘23 , the company had around $98m in cash and equivalents against zero long-term debt. This is a great position to be in. It allows for a lot of flexibility in how the management wants to use its cashflow, without much of the burden of paying annual interest expense on debt. The interest coverage ratio as of Q2 was around 58x, meaning EBIT was able to cover the interest payment 58 times over as the company still had around $450k in interest expenses. It is safe to say the company is at no risk of insolvency.

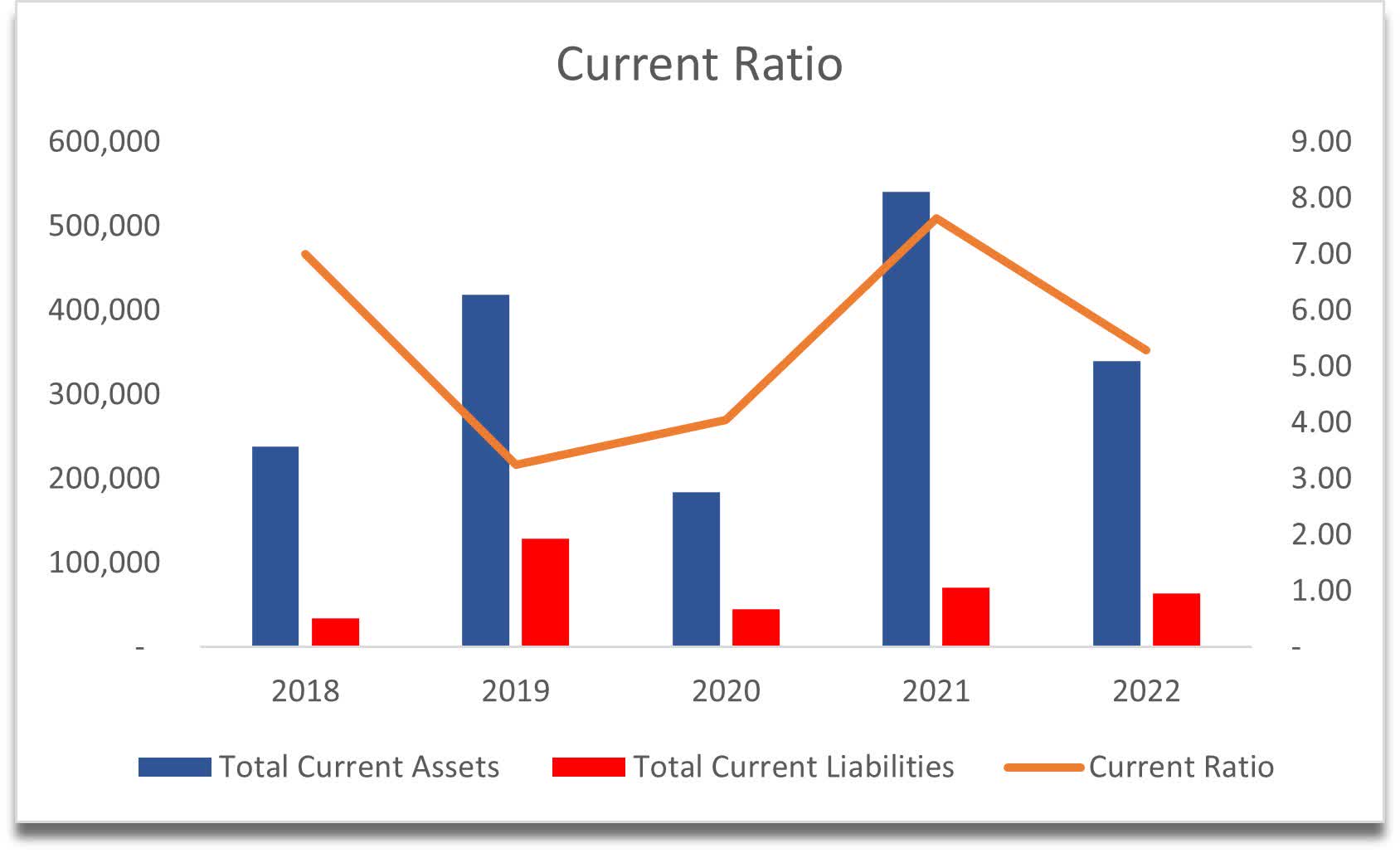

OPRA’s current ratio has been very strong over the years. I believe that it’s a bit too strong, which makes it inefficient. What I deem to be an efficient ratio is in the range of 1.5-2.0. I believe this range offers a perfect balance between the ability to pay off short-term obligations and still have liquidity for whatever the company wants to do with it. Anything over that range, I consider opportunity lost because the company is hoarding cash that could be used to further the company’s growth.

{kind=link}

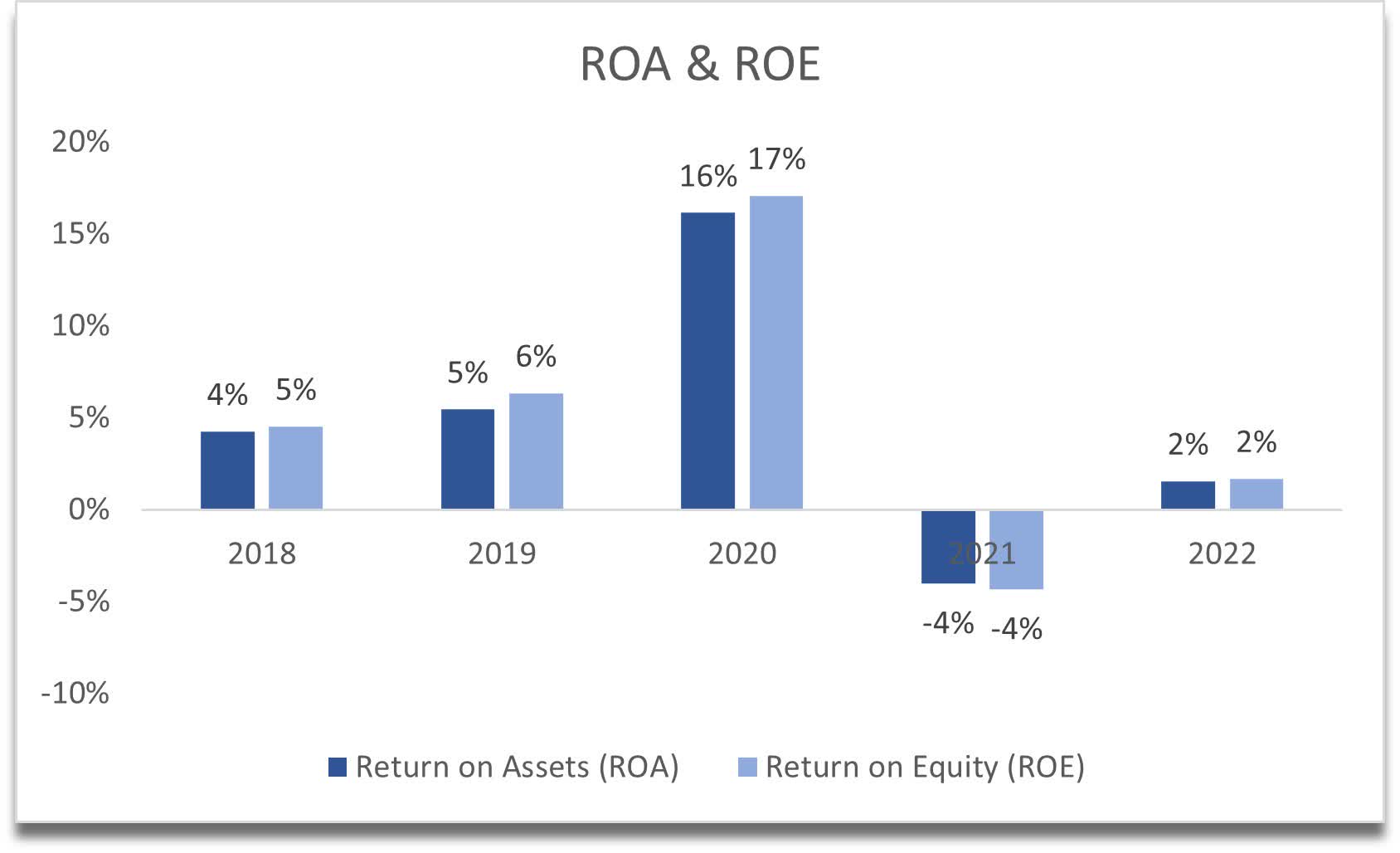

The company's ROA and ROE have fallen quite a bit from the pandemic highs in '20. I look for companies that can achieve at least 5% for ROA and 10% for ROE, which the company managed in FY20 ( due to gains from discontinued operations); however, it lost it all in the following years and is slightly below the historical averages.

{kind=link}

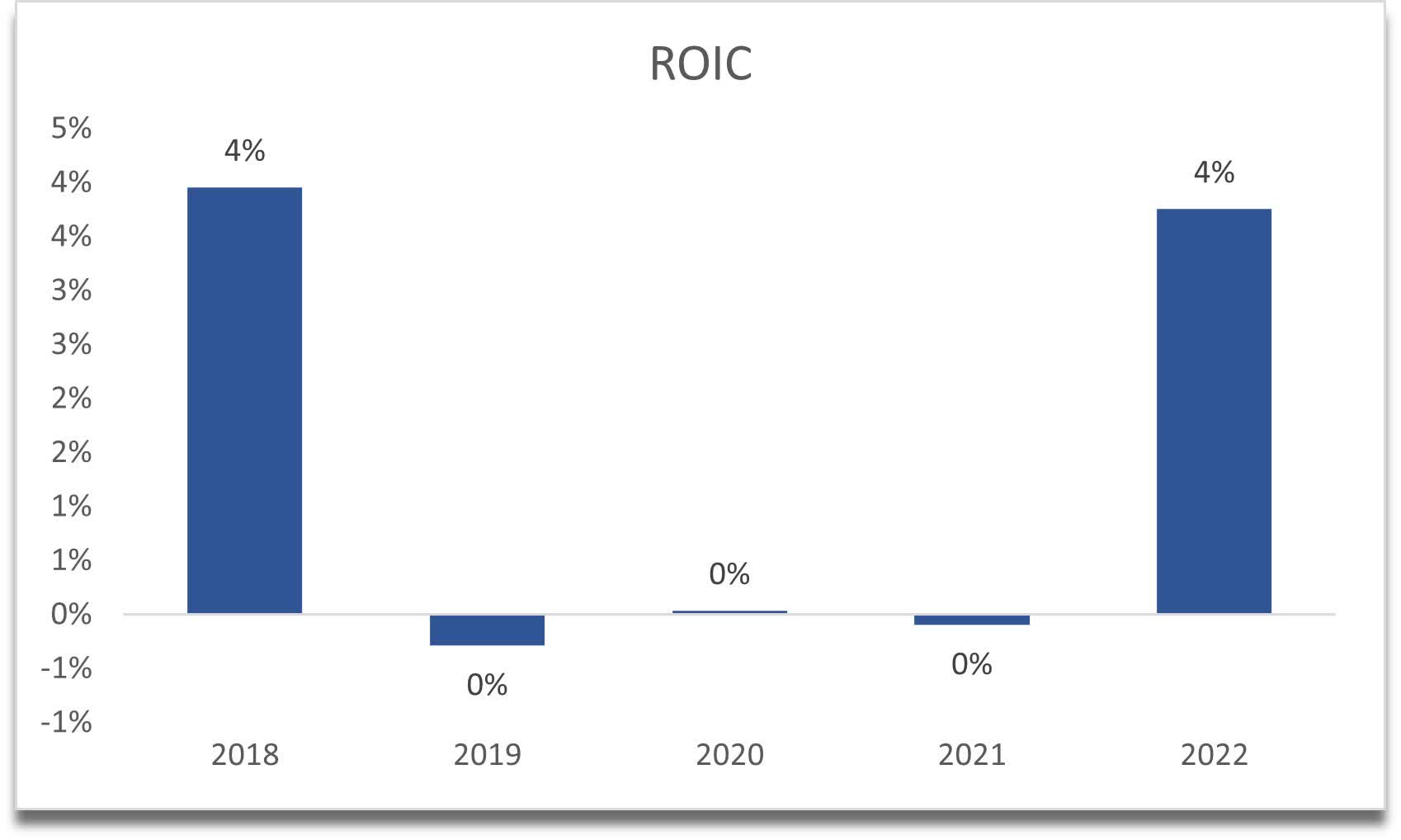

The company’s return on invested capital is also nothing to write home about. It is well below my 10% minimum; however, the company is still very new, and this may improve over time. For now, though, I will require a higher margin of safety for the lack of moat and competitive edge.

{kind=link}

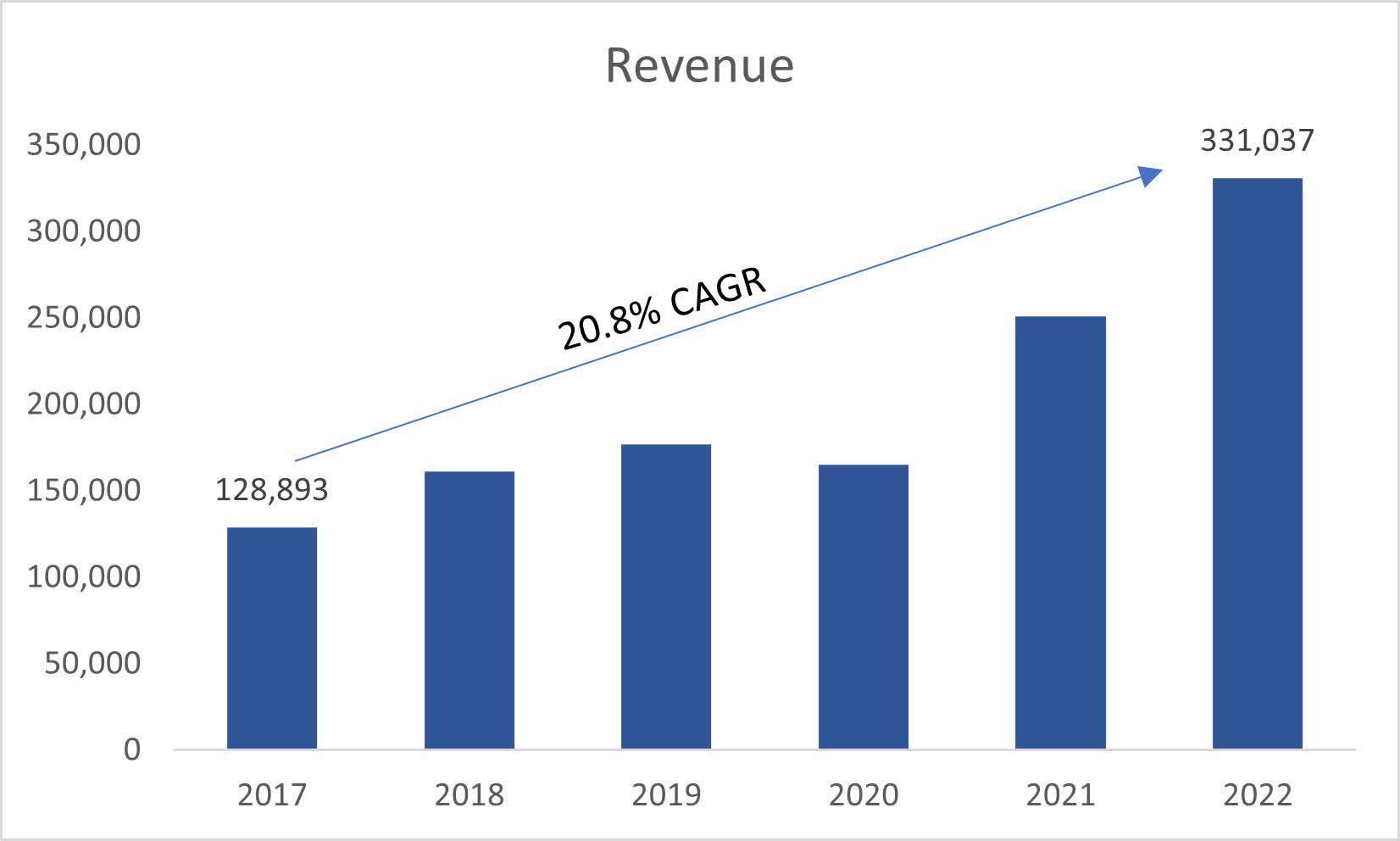

In terms of revenues, the company managed to grow at around 20% CAGR, which is quite impressive. The latest quarter showed around the same growth as the company's historical average, while the analysts estimate the company will grow at around 15.6% a year for the next 3 years, which is still decent.

{kind=link}

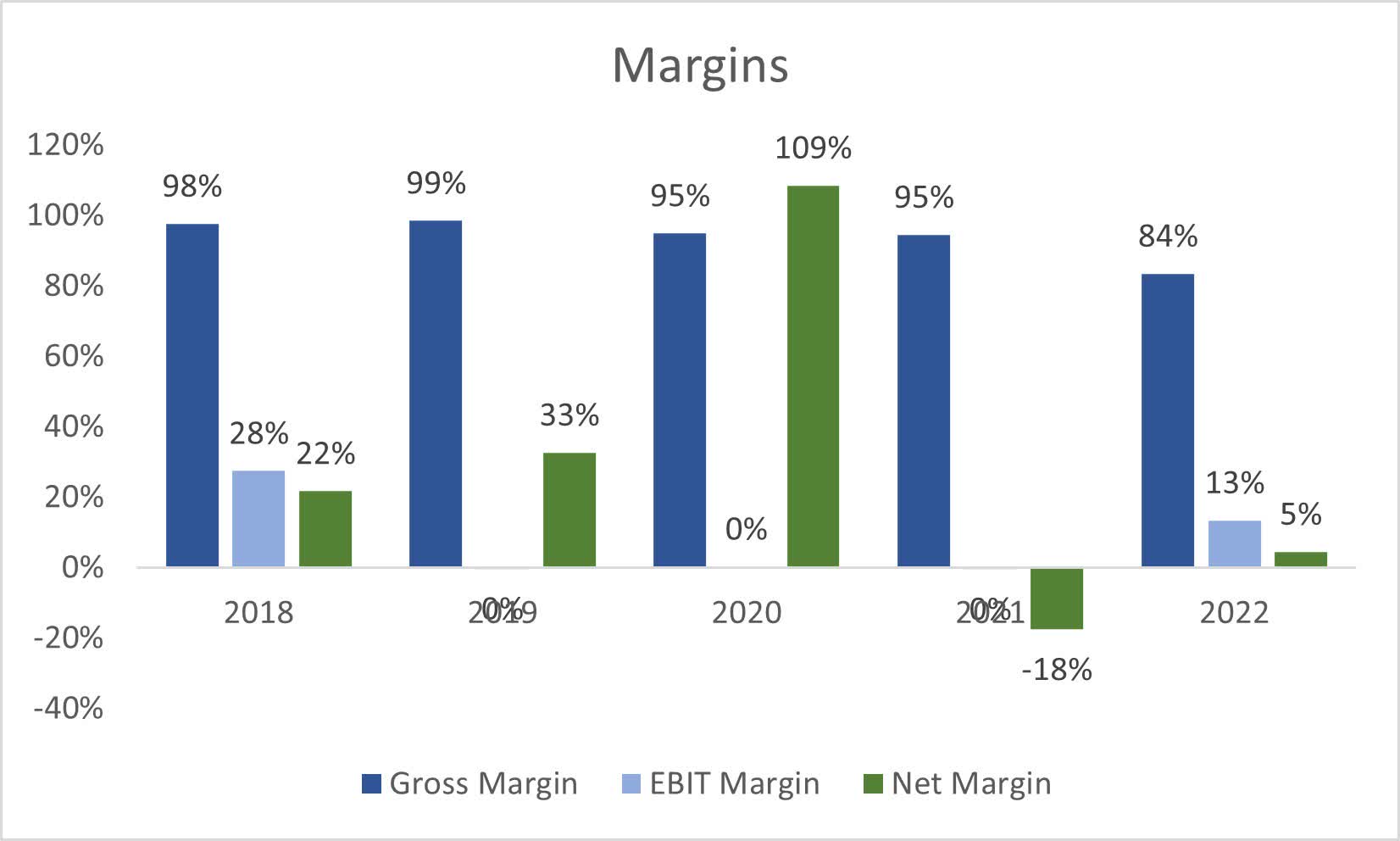

In terms of margins, these have been quite volatile over the years, which is understandable given the company’s short life. As of Q2, the company's net margin stood at around 16%, which is an improvement of around 10% from FY22. Due to how volatile the margins have been, I will add slightly more margin of safety to my calculations in the next section.

{kind=link}

Valuation

For the revenue growth, I decided to take the analysts’ estimates for my base case scenario for the first three years of the model. After that, the company will see around 10% CAGR through FY32. For the whole model, the company will see an 11% CAGR from FY22 to FY32. So, it is on the conservative end of calculations because I like to have an extra margin of safety that way, and it is better to be safe than sorry. For the optimistic case, I went with a 13% CAGR, while for the conservative case, I went with a 9% CAGR.

In terms of margins/EPS, I also went for a conservative route for the base case, compared to what the analysts see the company grow. Analysts see .75, .85, and 1.01 cents of EPS for '23, '24, and '25, respectively. I went with .43, .45, and .50 for the same years. After that, the company will see EPS growth of around 14% CAGR through FY32. For the optimistic case, I went with a 15% CAGR of EPS growth, while for the conservative case, I went with a 12% CAGR.

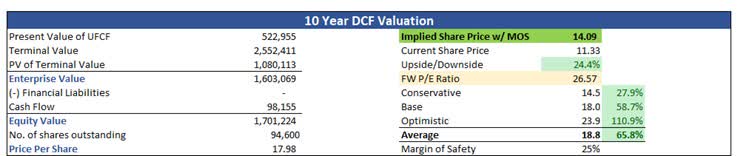

On top of these estimates, I decided to add another 25% margin of safety to the final intrinsic value calculation. It seems that I’ve beaten down the estimates quite a bit, so I think 25% is more than sufficient. With that said, OPRA’s intrinsic value is $14.05 a share, implying that the company is trading at a discount to its fair value.

{kind=link}

Closing Comments

It seems that the company is a good buy at these prices right now. The company’s massive pullback from its highs is presenting an enticing risk/reward at these levels. The company’s fundamentals and financial metrics are decent with a lot of growth still ahead for the company, which I believe will improve over the next couple of years. I would like to see the company’s moat and competitive advantage increase over time and would like to see ROIC go above 10% in the future, the same goes for ROA and ROE.

I think the mixed-shelf offering is still a good idea, as this will bring more power to individual investors, rather than the two controlling entities. The company will see its traded volume improve and become much more liquid to trade, making it easier to get in and out of a position. The company’s shares change hands around 1.5m times per day, so it is not like it’s very low, but it could be improved.

In terms of volatility, I could see further price drops due to the macroeconomic headwinds and the investors' negative sentiment towards the owners of the company. Since the company's share price isn't very high, I would be opening a couple of option contracts. I will be selling a couple of cash-secured puts at around 30-40 days out at a $10 strike price, which will net me a decent amount of premium. If it doesn't come down to $10 by then, I will rinse and repeat. This way I will be getting paid while I wait for the shares to come to me, in turn lowering my cost basis too.

For further details see:

Opera: Risk/Reward Enticing Here, Options In Play