OPRA - Opera Stock: Consider Buying This Dip

2023-11-10 11:54:59 ET

Summary

- Opera Limited has experienced a dip in stock price, making it a potential buy for medium-term holding. Read on.

- The company's Q3 FY2023 results exceeded expectations, with strong revenue growth and improved user metrics.

- Opera's shareholder policy has changed in recent months, and now the company should reward its shareholders much more generously than before while maintaining a strong FCF generation.

- OPRA's valuation suggests significant upside potential, with a projected 44% increase in equity value by the end of next year.

- I therefore recommend that investors consider buying OPRA stock's dip.

Introduction

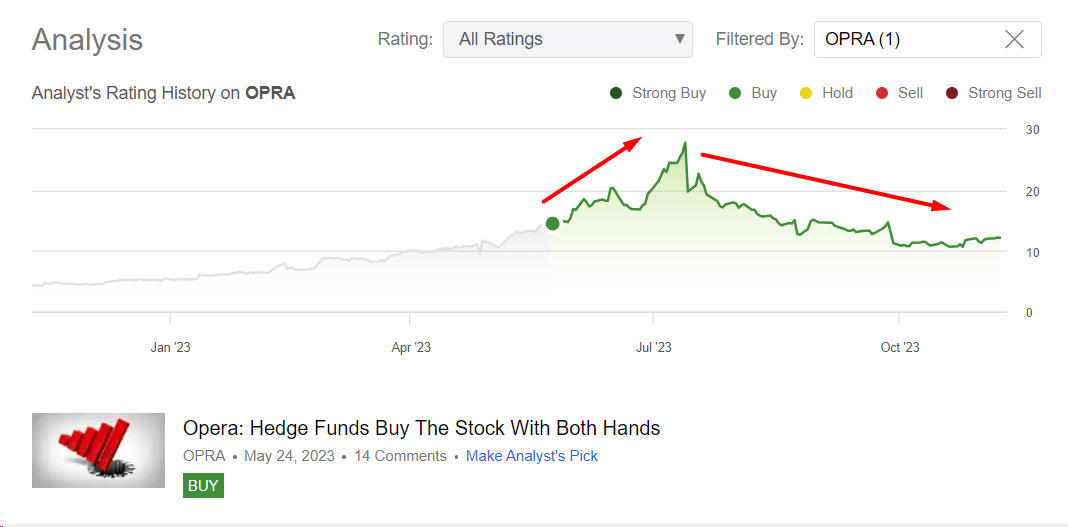

The last and only time I wrote about Opera Limited ( OPRA ) stock was in May 2023 , when the company was enjoying an unprecedented growth rate in the wake of the AI hype in the market. At the time, I noted that hedge funds and institutional market participants had just started to buy into OPRA, meaning that the stock had a very good chance of continuing its rally at the time. That was largely my thesis, which ultimately proved to be correct, as OPRA doubled in price before entering a protracted consolidation and falling sharply.

{kind=link}

Today, after OPRA fell below the publication price of my last article, I decided to take another look at the company to understand whether this dip is worth buying for a medium-term holding and how much of the AI hype has actually translated into operational improvements.

Financials And Prospects

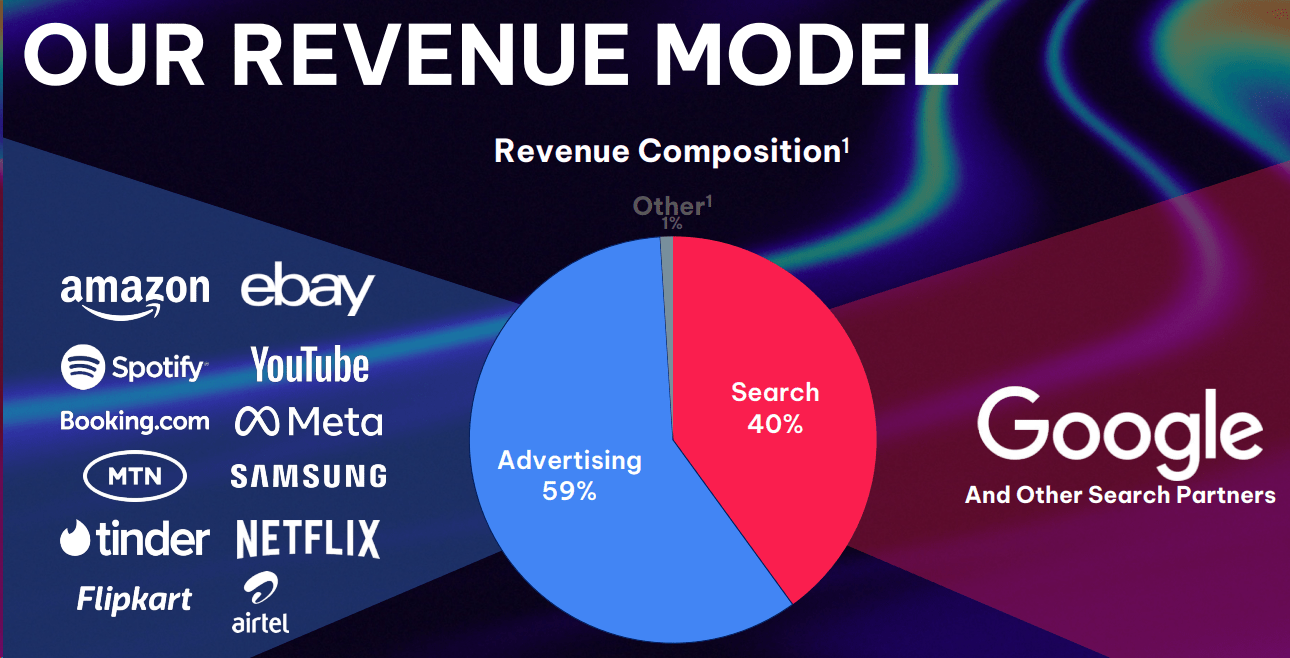

In case you hear about Opera for the first time, it's a small-cap [~$1 billion market cap] firm that offers web browsers for mobile and PC devices. They have 2 main segments: Browser and News [99.2% of total revenue], and Other [0.8%], according to the most recent 20-F filing . But looking at the revenue composition, OPRA's revenue model looks way more diversified with 59% of sales coming from advertising and the other 4% coming from search activity.

{kind=link}

The company provides various mobile browser products like Opera Mini, Opera for Android and iOS, Opera GX Mobile, and Opera Touch. They also offer PC browsers such as Opera for Computers and Opera GX. Additionally, Opera Limited has Apex Football, Opera VPN Pro, and Opera News, which is a personalized news discovery and aggregation service powered by artificial intelligence. They also have Opera Crypto Browser for PCs and mobile devices, a browser-based cashback rewards program, and their own GameMaker Studio, a platform for developing 2D games. Opera Limited operates the gaming portal GXC and the online advertising platform Opera Ads. They have operations in several countries including Nigeria, Ireland, France, Germany, Spain, England, South Africa, and Kenya, as well as internationally. The company was founded in 1995 and is headquartered in Oslo, Norway. Opera Limited is a subsidiary of Kunlun Tech Limited.

{kind=link}

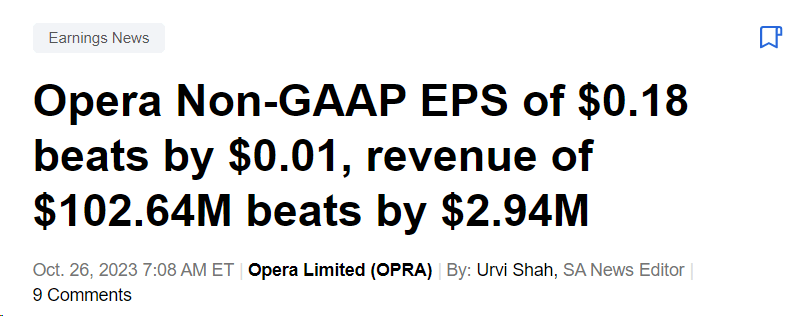

On October 26, 2023 , The company released Q3 FY2023 results, surpassing revenue and earnings estimates (not by much though):

{kind=link}

In Q3 FY2023 , OPRA delivered impressive financial results, marking its 11th consecutive quarter of >20% revenue growth. Advertising revenue, comprising 59% of the total, grew by 24% year-over-year, benefiting from both the trajectory of browser monetization and the expansion of the Opera Ads platform. Search revenue also exhibited strong growth at 15% YoY, driven by a targeted focus on users with high monetization potential in Western markets.

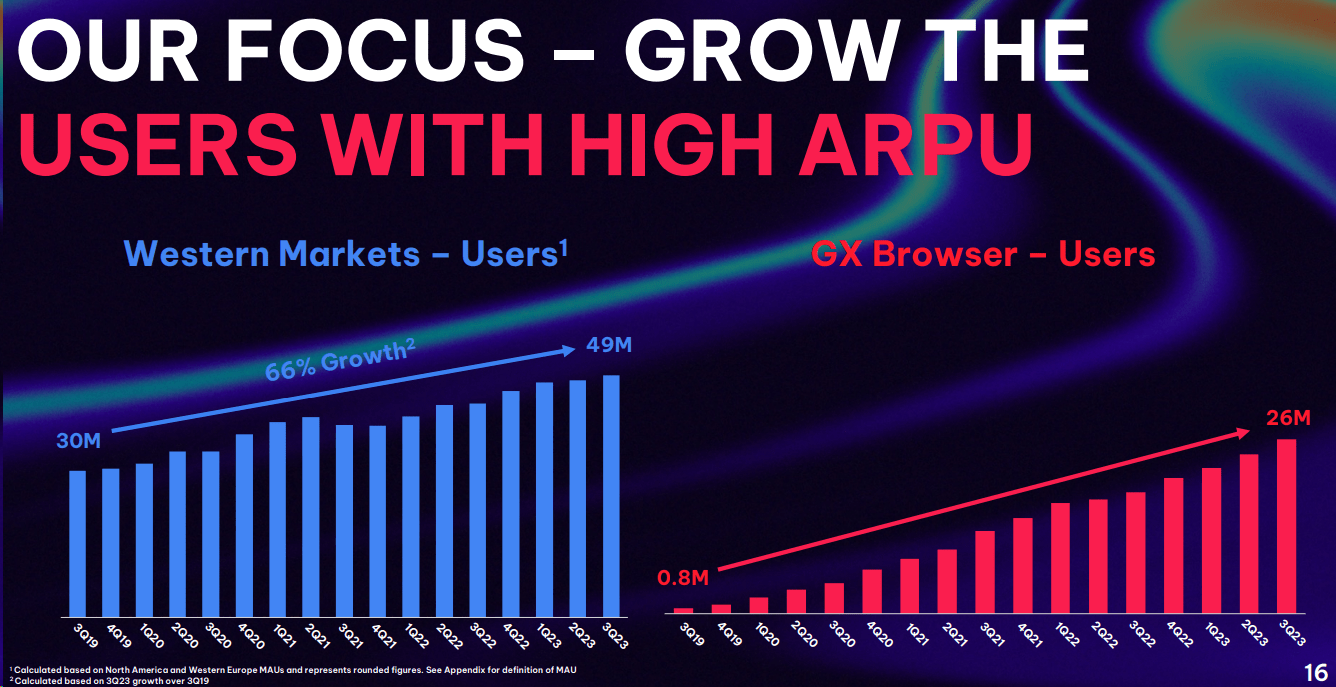

Speaking of unit economic metrics, it's worth noting that OPRA's user metrics showed resilience and strategic focus. Despite a reduction in low-average revenue per user ((ARPU)) in emerging markets, the company reported 311 million monthly active users (MAUs) in Q3 2023. Additionally, the annualized ARPU increased by 24% to reach $1.31 compared to the same period in FY2022. The Opera GX gaming browser, designed for the gaming community, also experienced robust growth, with 26.1 million MAUs across PC and mobile, reflecting a 10% increase from the previous quarter.

{kind=link}

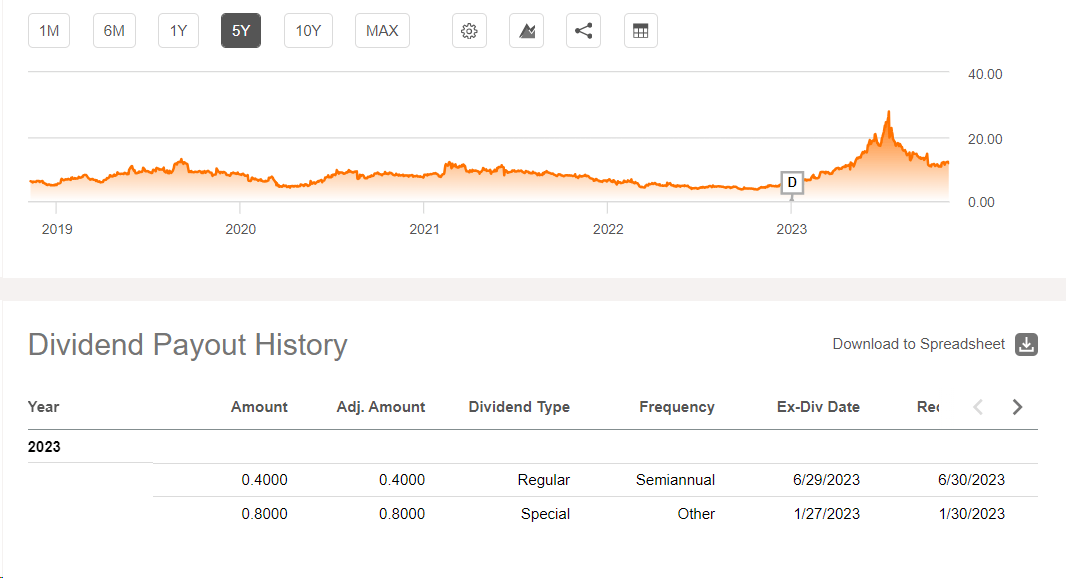

Financially, OPRA demonstrated its commitment to shareholder value by returning $53 million through dividends and share repurchases during the quarter ( that's over 5% of the market cap in just 3 months ). The company paid its first recurring semi-annual dividend of $0.40 per ADS in July and repurchased 1.2 million ADS at $17.2 million in Q3.

{kind=link}

With quarterly revenue reaching $103 million and an impressive adjusted EBITDA margin of 23%, OPRA not only surpassed its previous guidance but also raised projections for both revenue and adjusted EBITDA, underscoring its positive growth outlook and effective financial management.

For the full year, Opera has raised its revenue guidance to a range of $394 - $397 million, up from the previously issued range of $380 - $390 million. The adjusted EBITDA is now guided to be in the range of $88 - $90 million, representing a 23% margin at the midpoints, up from the previous guidance of $80 - $84 million. Looking specifically at Q4 FY2023, Opera anticipates revenue between $110 - $113 million, reflecting a 16% year-over-year growth at the midpoint, and adjusted EBITDA is guided to be $22 - $24 million, with a 21% margin at the midpoint.

As far as I can see, despite its phenomenal growth, OPRA still has a very robust balance sheet with a current ratio of well over 1 and a debt-to-equity ratio of almost zero.

The company continues to generate enormous free cash flow, which fell slightly in the third quarter compared to the previous year (mainly due to working capital) but increased YTD by ~121%:

| Three Months Ended September 30, |

| Nine Months Ended September 30, |

| 2022 |

| 2023 |

| 2022 |

| 2023 |

| Net cash flow from operating activities |

| $ |

| 18,032 |

| $ |

| 16,233 |

| $ |

| 33,120 |

| $ |

| 57,477 |

| Deduct: |

| Purchase of equipment |

| (165) |

| (741) |

| (2,758) |

| (1,279) |

| Development expenditure |

| (1,988) |

| (1,189) |

| (4,911) |

| (3,304) |

| Payment of lease liabilities |

| (848) |

| (884) |

| (2,884) |

| (2,943) |

| Free cash flow from operations |

| $ |

| 15,031 |

| $ |

| 13,418 |

| $ |

| 22,567 |

| $ |

| 49,951 |

Source: OPRA's press release

I like the pace at which the company is developing and how its margins are growing. Apparently, the introduction and monetization of AI in a company is having an even more positive impact on financials than many expected, including the management itself.

But what about OPRA's valuation?

OPRA's Valuation

I mentioned above that Opera's FCF has risen quite sharply this year. If we look at the FCF yield, we see that the recent correction in the stock has caused this type of yield to rise to the level of previous lows such as early 2021 or late 2022:

Let me remind you that the company is now paying a dividend of over 3% per annum while actively using FCF to buy back its ADS from the market. In my opinion, this makes OPRA a more attractive company today than in early 2023, if we're talking about "shareholder friendliness". Imagine: If the total shareholder return (buybacks + dividend) remains at the same level as in the third quarter of fiscal 2023, then OPRA should theoretically return >20% of its market capitalization to its investors over the next 12 months. That's a lot, especially for a fast-growing IT company.

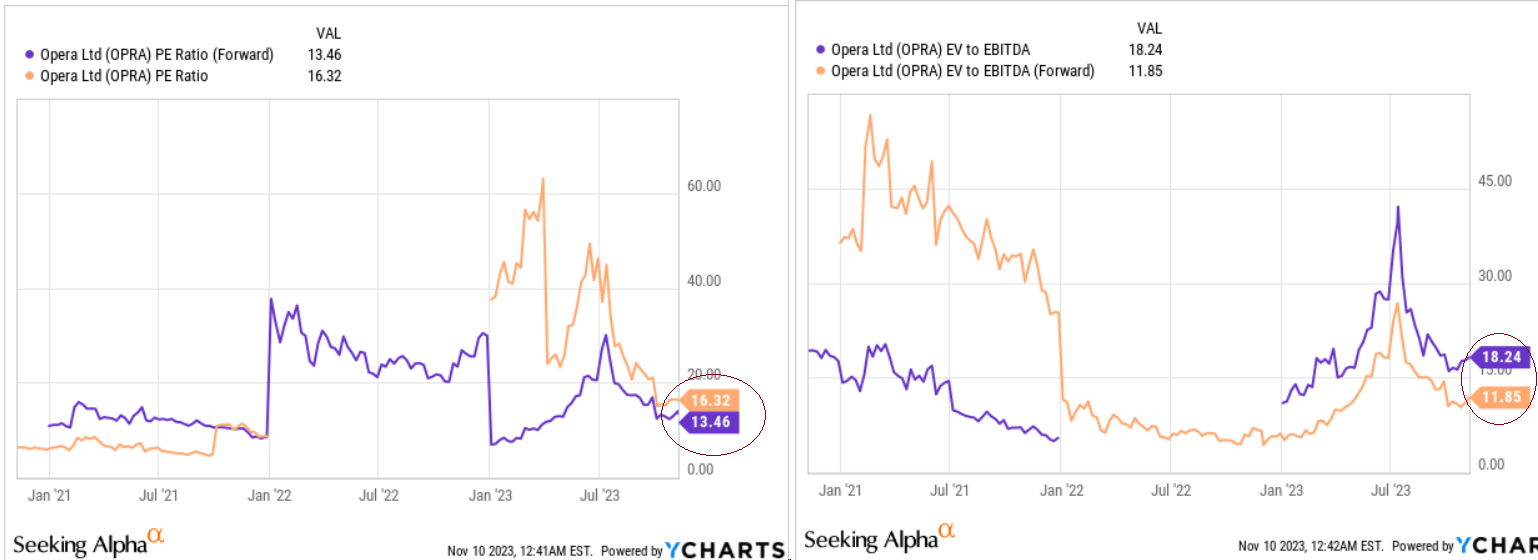

At the same time, absolute price/earnings ratios and EV/EBITDA ratios are set to fall significantly next year, as they are already quite low for the information technology sector .

{kind=link}

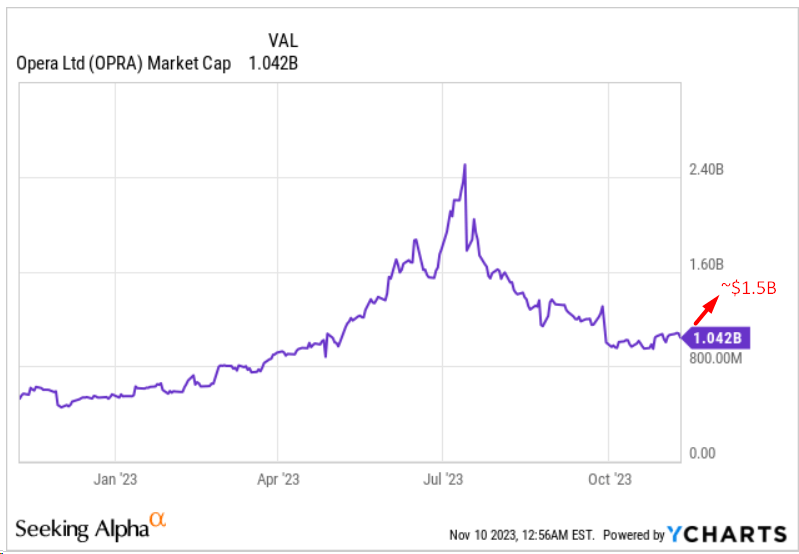

As we know from the new guidance, OPRA's adjusted EBITDA for FY2023 is going to be in the range of $88 - $90 million (at a margin of 23%). At the midpoint of this range, and assuming a modest EV/EBITDA ratio of 15x, OPRA's enterprise value should be $1.335 billion by the end of 2023. However, this is too short a timeframe. Let's assume that the forecast EBITDA margin at the end of FY2024 remains unchanged. With consensus revenue of $396.12 million , we get an adjusted EBITDA of $95.1 million. Using the same expected EV/EBITDA multiple of 15x, we arrive at an enterprise value of $1.426 billion.

The company has negative debt on its balance sheet (-$75 million), so the equity value should be ~$1.5 billion. This gives OPRA an upside potential of 44% by the end of next year.

{kind=link}

The Bottom Line

Of course, investing in OPRA stock involves some very important risks that every investor should consider before purchasing the stock. First off, Opera company faces formidable competition from well-established web browsers like Google Chrome and Microsoft Edge. The firm's heavy reliance on advertising revenue exposes it to economic downturns and shifts in consumer behavior. The concentration of revenue in specific markets makes Opera susceptible to economic and political instability in those regions. Regulatory changes in the web browser industry could impact Opera's business model. Data privacy concerns arise from Opera's extensive user data collection, which, if breached or misused, may lead to reputational damage and financial losses. Also, the technology-centric nature of Opera's business poses risks related to cyberattacks and other disruptions.

Despite all the existing risks, Opera seems to me to be an interesting buy candidate after the severe dip. Firstly , the latest financial results show that Opera isn't just talking big about AI, but is actually using the new technology to drive its growth. Second , Opera's shareholder policy has changed in recent months, and now the company should reward its shareholders much more generously than before while maintaining a strong FCF generation. I expect this to attract even more institutional investors. Incidentally, contrary to my expectation that there has been an outflow of institutional investors in recent months (which would explain the fall in the share price), their ownership has, on the contrary, continued to rise despite the fall in the share price.

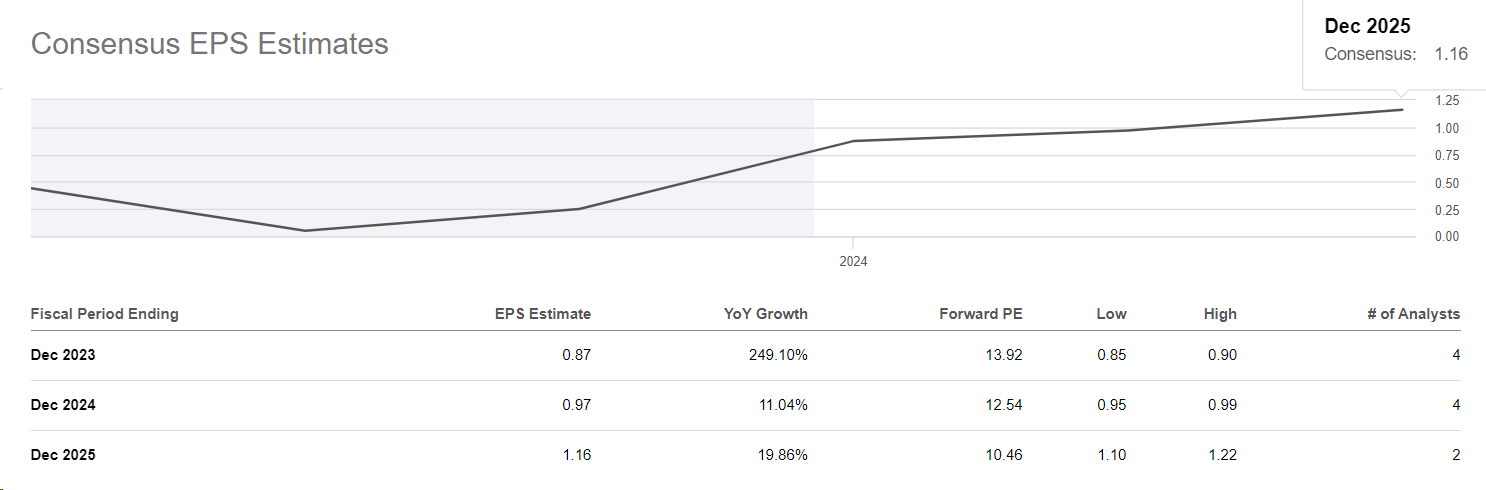

Third, the share remains very cheap given the growth rates it is expected to achieve in the coming years:

{kind=link}

The 12-month upside of 44% I calculated above leads me to the conclusion that the rating should be set to "Buy" again.

Thanks for reading!

For further details see:

Opera Stock: Consider Buying This Dip