OPFI - OPFI: Too Much Risk At Today's Price

2023-04-27 11:38:48 ET

Summary

- OppFi came public in the midst of the SPAC mania of 2021 and shares are down 80% from their high.

- Busted IPOs and SPACs are good hunting grounds for a growth and value convergence, but you have to cherry-pick for quality.

- OPFI is too pricey right now, and the future is still relatively uncertain versus the price.

Opportunity Financial, AKA OppFi,( OPFI ) is a disruptive fintech company that came public via SPAC in the midst of the mania of 2021. Their core business helps provide personal loans to individuals with very low or no credit scores, who are employed full time.

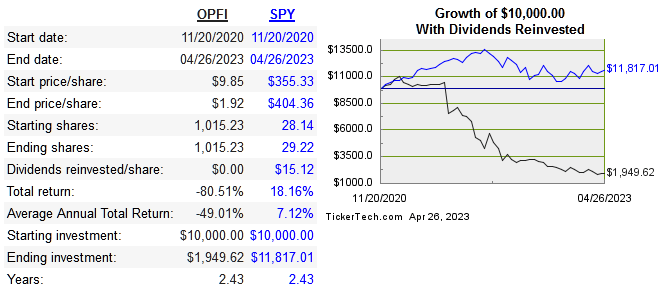

Below is the share price performance since the IPO in 2021:

{kind=link}

dividend channel

SOFI is definitely a competitor, but they have a slightly different business model and serve a different segment of consumers.

| Company |

| Revenue 5-Year CAGR |

| Operating Margin |

| Net Margin |

| ROIC |

| OPFI |

| 45% |

| -0.9% |

| 1.6% |

| 1.1% |

| 1.3% |

| -1.2% |

| -18% |

| 5.8% |

| 34.2% |

| 18.6% |

| 8.3% |

| 77.7% |

| -12% |

| -12% |

Risk

The most obvious short-term risk is the $100 million USD lawsuit the company is facing. I’m afraid I don’t have much to add in order to know the probability of OPFI beating this suit. All I can say is that the very nature of this business model attracts negative attention, and this is something I consider to be a risk factor going forward even if this lawsuit is beaten.

This lawsuit can definitely lead those who give it a superficial glance to the conclusion that they are simply a usurious, payday lender type wrapped up in new tech veneer. There could be legal limits put on the APRs, which would weaken the business model considerably.

The next biggest risk is simply producing poor underwriting results. One of the main features of OPFI is the vast amount of data they use to make underwriting decisions algorithmically. I don’t have insight into their prosperity methods, but the consistent profitability along with reasonable growth of the top line shows that the business model works for now. The problem is, we haven't seen if this profitability can last through a full cycle.

The company itself is mission-driven, and while many consider the subprime market murky waters no matter what, I don’t see this company as a bad actor in the industry. I think management is decent, and the insider ownership level of 71% is definitely a positive.

Valuation

The value investor in me loves the idea of busted IPOs, and this case a busted SPAC, as hunting grounds for an investment. The growthier side of me likes the idea of cherry-picking an above average business from that distressed cohort and holding it for the long run. High-flyers are often priced at near full optimism when they go public during a bull market, but I would argue that this effect was exaggerated in 2021.

One of the most appealing aspects of this young company is the fact that it has been profitable for a while now, which can't be said for most newer tech companies.

Clearly, OPFI got caught up in the SPAC mania of 2021, however. The bad news is that those who got in at the peak in 2021 are now down over 80%. The overvaluation is clear to us all in hindsight, but what matters most is the valuation going forward.

Below we look at the multiples comp:

| Company |

| P/E |

| P/S |

| P/FCF |

| OPFI |

| 29.8 |

| 0.5 |

| 0.9 |

| SOFI |

| -16/.5 |

| 3.4 |

| UPST |

| -11.2 |

| 1.4 |

| -2 |

| ENVA |

| 6.4 |

| 2 |

| 1.5 |

| CURO |

| -0.3 |

| 0.1 |

| 0.2 |

I like to also look at historical multiples over at least a 10-year period, but these companies are newer to the public markets, so

it doesn’t help quite as much.

On a multiple's basis, I think the stock is overpriced. The potential growth rate of earnings doesn’t justify such a high P/E. The future cash flows are much more uncertain, and the level of risk I see outweighs the price today. Being down 80% from the 2021 high isn’t enough to warrant actual undervaluation. There is too much uncertainty at this still early stage of the company’s journey as a disrupter. A DCF model is less effective with a company this young, so the multiples are a better guide.

There is still more time to see how this story plays out before jumping in, so this stock is a hold for me right now.

Conclusion

I think it's fair to say that OPFI was overhyped, just like most other SPACs. Now that the dust has settled from that type of market, is the price appropriate for the quality of these businesses and the risk that comes with it?

The quality of the company is ultimately yet to be seen, but there is far too much uncertainty of future earnings versus the potential upside if everything goes right for OPFI over the next decade. This is definitely a busted SPAC, but the stock comes with a lot of risk in exchange for limited upside.

For further details see:

OPFI: Too Much Risk At Today's Price