OPK - OPKO Health: FDA Approval To Save The Company

2023-10-20 13:30:50 ET

Summary

- OPK and PFE received FDA approval for Ngenla in June. This enables OPK to receive royalties going forward.

- OPK has continued to lose money due to its lab business. The business had sales fall off following the decline in COVID testing. OPK needs to right size the business.

- The potential royalties from Ngenla are not enough to make the company profitable.

- OPK has a good potential pipeline. Its ability to develop that pipeline is a concern with its current cash position.

I wanted to provide an update on my investment thesis for OPKO Health, Inc. ( OPK ). I n my most recent analysis from May I rated OPKO as a hold. There was enough potential at the price point to hold on to the stock, but not enough for me to want to buy more of the stock. There has been one big piece of news since my last article. OPKO and Pfizer ( PFE ) received FDA approval for Ngenla. This removes one of the large risk items for the stock. Does the approval make the company a buy? Is Ngenla the savior that OPKO and investors have been waiting for? That is what we are going to look at a bit further today.

The Approval

OPKO and PFE received FDA approval for Ngenla (Somatrogon) on June 28, 2023 . It was a bit more of a process than originally hoped but in the end the company got the approvals that it needed. This is a big deal for the company. Not only is the US the biggest market for the drug and allows it to start profit sharing, but it also triggered a $90 million payment from PFE to OPKO. As a loss making company that milestone payment does wonders for the balance sheet of the company. It provides some more wiggle room for the company to continue to develop its pipeline. It also gets some breathing room as OPKO gross profit royalties start to ramp up. Under the agreement between OPKO and PFE, OPKO is set to receive gross profit sharing on Ngenla and Pfizer’s Genotropin.

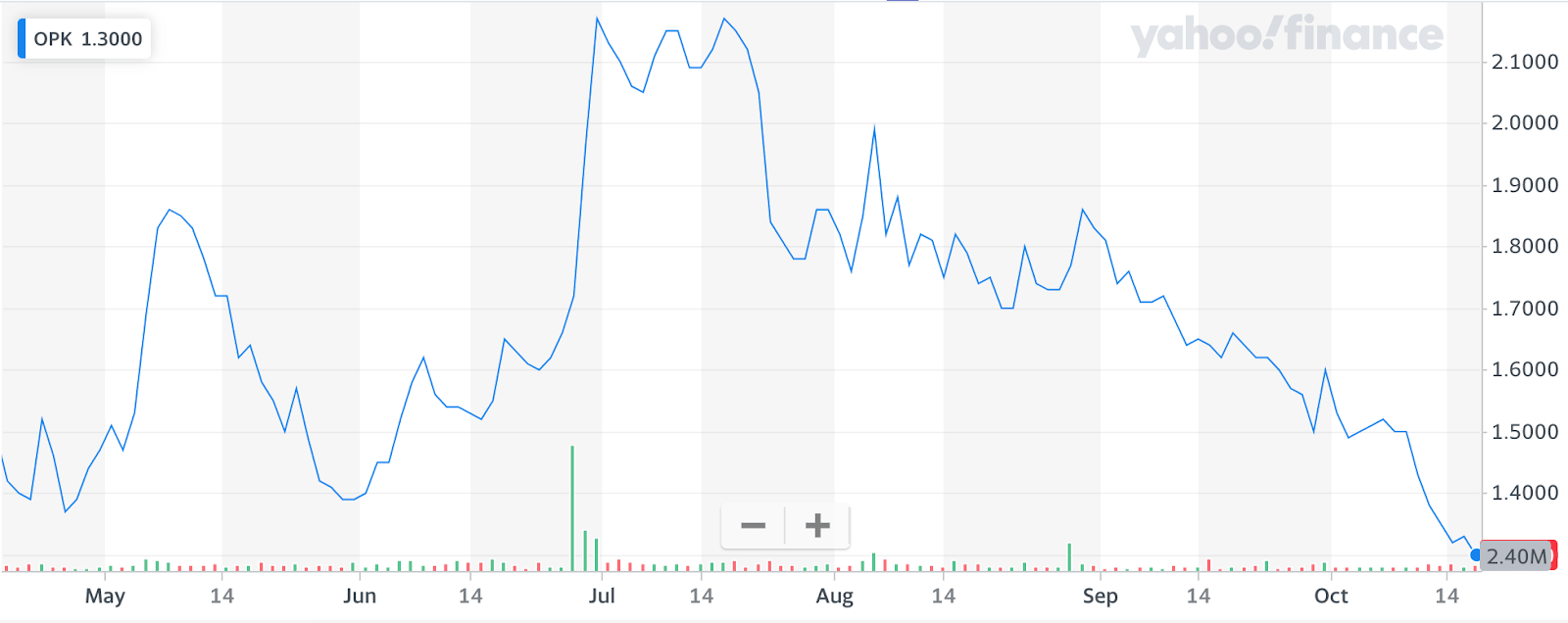

While investors have been awaiting approval so they can start to see some profits flow from the drug, is it enough to bring the company and the stock from its current lows? The initial approval news drove the stock higher. The stock started to climb a bit before the approval as I think many were expecting it. It spiked on the news of FDA approval. This euphoria quickly wore off. You can see the spike and then decline in the chart below.

{kind=link}

The stock reached a high of $2.17 a share following the approval at the end of June. It has since fallen 40% to $1.30 a share. That is a pretty rough price drop in three and a half months. It is the lowest the stock has been since March 2023. I am sure there was also some profit taking. Many took advantage of the price jump to take a quick gain and get out of the stock. Or longer term investors were happy to see some increase in the stock price and sold some of their position off.

This price drop is also a reality check from investors. The company had over $1 billion in revenue last year. Ngenla is in line to bring in revenue and profit for the company but how much and is it enough to move the needle on a company that size is part of the question.

Ngenla the savior?

Many investors, myself included, were very excited about the approval of Ngenla. As we should be since it will drive profits for the company. I think many investors got caught up in this excitement and bought the stock. Then they started to do a bit more research and digging and have decided that the company still has a lot of issues. While the approval is a big deal for the company, the drug is not going to save the company on its own. The company needs to see a lot of other areas of improvement before it can become profitable.

We can take a look at the revenue and potential from the drug approval and see what it looks like for OPK. The agreement with Pfizer states, “Upon the launch of hGH-CTP for Pediatric GHD (Ngenla), which is subject to regulatory approval, the royalties will transition to gross profit sharing for both hGH-CTP (Ngenla) and Pfizer’s Genotropin”. The company has stated that this royalty is a double digit royalty. From the latest quarterly earnings call: “OPKO will be entitled to a profit sharing arrangement with Pfizer on a worldwide basis, which is based on regional tiered gross profit on both NGENLA and Genotropin, Pfizer's daily human growth hormone.”

In 2022, Pfizer had sales of $360 million from Genotropin. This is down from $389 million in 2021. These sales have seen an increase in the first 6 months of 2023 as sales reached $222 million. That is an increase from $171 million in the first 6 months of 2022. Good for an almost 30% increase in sales. If we can assume that sales will continue at that same rate then Pfizer will see revenues of close to $450 million from Genotropin. This would be a pretty solid win for Pfizer in general, but we can operate off this assumption as there is no indication that sales will drop off in the second half of the year. Now we start to get into the assumptions. OPK will receive royalties on gross profit. Drugs usually have a very high gross profit, we will look at a range of 85%-95% gross profit. The other assumption is what is the double digit royalty that OPK is set to receive. We will use a range of 10% to 20%. The table below lays out the potential returns.

| (millions USD) |

| High |

| Med |

| Low |

| High |

| Med |

| Low |

| High |

| Med |

| Low |

| Annual Sales |

| $450 |

| $450 |

| $450 |

| $450 |

| $450 |

| $450 |

| $450 |

| $450 |

| $450 |

| Gross Margin |

| 95% |

| 95% |

| 95% |

| 90% |

| 90% |

| 90% |

| 85% |

| 85% |

| 85% |

| Gross Profit |

| $428 |

| $428 |

| $428 |

| $405 |

| $405 |

| $405 |

| $383 |

| $383 |

| $383 |

| Royalty |

| 20% |

| 15% |

| 10% |

| 20% |

| 15% |

| 10% |

| 20% |

| 15% |

| 10% |

| Revenue |

| $86 |

| $64 |

| $43 |

| $81 |

| $61 |

| $41 |

| $77 |

| $57 |

| $38 |

There is a large range at play here. This largely depends on the royalty rate that the company is receiving. The company could be looking at $86 million on the high end to $38 million on the lowest end. There are a lot of factors here, from revenue, to gross profit, to royalty percentage. This gives us a general idea of where revenues might fall for OPK. The company will only be profit sharing for the month of September in Q3 so we will probably have to wait until the end of Q4 before we have much visibility into the revenues being received by OPK. The other good part here is that this will be almost entirely profit for the company. OPK is still winding down some of its clinical operations for Ngenla but hopes to wind that down by Q1 2024. At that point it will almost be entirely profit.

Taking these estimates we can see the effect they will have on the financials for OPK. The table below shows the revenue, expenses, and operating profit for the last three years.

| (In millions) |

| 2022 |

| 2021 |

| 2020 |

| Revenue |

| $1,004.2 |

| $1,774.7 |

| $1,435.4 |

| Total Costs and Expenses |

| $1,230.4 |

| $1,756.0 |

| $1,377.7 |

| Operating Income/(loss) |

| -$226.20 |

| $18.70 |

| $57.70 |

The company had an operating loss of $226 million in 2022. Even with the highest estimate of $86 million the company would still be at a large operating loss. The company did have $87 million in amortization in 2022. When this is backed out the company is still not cash flow positive with the gross profit share from Ngenla. Now this is not taking into account any future growth in the sales of Ngenla. Going forward they could see growth in revenues but even if the sales were to double to almost $1 billion the company would still be at an operating loss in its current status.

So in short, Ngenla is a great positive for the company but it is not going to be the savior of the company, at least not on its own. It is good to see a win for the company but it needs more. The company needs to see other parts of the company become more efficient and profitable.

BioReference Lab

This large loss is mostly due to the operations of their lab unit. I discussed this operation more in depth in my last article . Basically it has turned into a massive loss making segment for the company. During COVID the unit was making a lot of money but also added a lot of costs. COVID testing all but stopped and the company still has a bloated cost structure and is now hemorrhaging money. The company has cut costs and is working to turn the segment around. We have another quarter of results since I last reviewed the company so I want to see if their turnaround is starting to come to fruition.

| (In thousands USD) |

| Q2 2023 |

| Q1 2023 |

| 2022 |

| 2021 |

| 2020 |

| Revenue from Services |

| 127,052 |

| 132,368 |

| 755,630 |

| 1,607,106 |

| 1,262,242 |

| Cost of Services |

| 113,028 |

| 114,061 |

| 627,548 |

| 1,102,172 |

| 823,899 |

| Gross Margin |

| 11.0% |

| 13.8% |

| 17.0% |

| 31.4% |

| 34.7% |

| SG&A |

| 52,617 |

| 52,576 |

| Operating Income/(loss) |

| -44,258 |

| -40,007 |

| -173,652 |

| 98,067 |

| 138,922 |

It does not look like the company has made much progress. In terms of revenue the company is looking at a decline in revenues in 2023 vs 2022. The gross margin has continued to decline. The SG&A also stayed consistent with Q1. I would have expected to see a decline in SG&A. If it was experiencing growth in revenues then the flat SG&A would not be as big of a deal as it would continue to become a smaller percentage of revenue. That is not the case though as revenues are not growing. The company did decrease SG&A by approximately $70 million through the first half of the year in 2023 vs 2022. Going from $170 million to $100 million is a significant decline. This is a positive, but seeing as they are still at a large operating loss I would expect that to continue to decline and not flatline. I personally have not seen the “turnaround” or “right sizing” of the labs business happening at a fast enough pace. The entity is trending for a slight decline in the operating loss but still a large loss for the year. This is the largest revenue driver and also loss maker for the company. The other segments are EBITDA positive. The labs business continues to drag the company down and the sooner it gets fixed the better.

Drug Pipeline

The other positive with the company, as with most biopharma companies, is the potential of the pipeline. While the company has received FDA approval for a few different drugs at this point, most have not panned out as expected. That is always the inherent risk with the industry. It is still too early to tell if their future pipeline will generate revenue or when, but there is a lot of potential with MDX-2201. It signed a license agreement with Merck to develop this drug. It followed a similar strategy as with Ngenla to partner and take it to market. The company has potential to receive some large milestone payments, up to $872 million, and also royalties on global sales. This is the biggest potential product in the pipeline. I covered this more in my last article and you can reference that for more information.

The key here for me is that there is a lot of potential revenue, but it costs to develop that pipeline. I would like the company to get to a positive cash flow position with its current business. The company should be able to achieve this with the license of Ngenla. Then it will be able to continue to advance its pipeline and achieve the potential without raising more money. While there is value in the pipeline I don’t want to see that value diluted.

Cash Position

The company is basically at the same cash position as it was last quarter. The company had approximately $110 million on the books to end Q1 and at the end of Q2 had $108 million in cash. It had a very large cash burn quarter, minus the $90 million payment for Ngenla. They in essence burned through benefits of the $90 million payment in one quarter. If the company continues at the current rate of cash burn it only has enough cash on the books for two or three more quarters. The company has received some very large milestone payments recently. Due to mismanagement of the company as a whole these have been burned through very quickly. This was a big waste for the company. These milestone payments should have provided the cash needed to continue to develop the pipeline and provide a buffer while the company starts to receive royalties.

I do think the cash flow position will improve. The company will start to see revenues from the royalties. These are almost straight profit to the company. I also expect the company to continue to cut costs. This combination will improve the cash flow for the company. My concern is that it is not happening fast enough. The company is not in a strong cash position, and it should be with the recent payments received.

The company needs to cut costs and do so fast, it also needs to see some growth within the labs business. The company does not have the benefit of large milestone payments upcoming, at least not anytime too soon. This means the company will have to better manage its cash flow to avoid raising more money or taking on more debt.

Risks

There are positives to OPK, but there are plenty of risks. The approval of Ngenla removes one of the big risks for the company. The company is still going to be a loss making company, despite the approval of Ngenla. The losses are coming from their lab business. The company is in the process of a turnaround in that business. It seems that the turnaround process still has a long way to go. These losses are burning through the cash position of the company. If it is not able to improve the profitability of the business within the next few quarters then it will need to raise more money or take on more debt.

The company has good potential in the pipeline. As with any drug in the development process, there is a lot of risk. Getting a drug through FDA approval is expensive and difficult to do. Also there is no guarantee that the drug will be a success even if it does get through the approval process. As can be seen with the company’s other drug approval, Rayaldee.

Conclusion

The company has finally received approval for Ngenla. This will start to bring in royalty revenues and will be a large boost on getting the company to profitability. It unfortunately will not be the savior for the company. Even with the royalties the company is still going to be losing money. It needs to turn around the losses within the labs business in order to get to profitability. This business has been losing a lot of money. While the company has started cutting costs and attempting to right size the ship it still has a long way to go.

The company still has plenty of potential. It has an approved drug in the market that will generate royalties. It has a strong potential pipeline. With the recent price drop it has a market cap of $1 billion. That is right in line with 2022 sales. The company is being valued conservatively as there are some risks for the company.

I rated the company a hold in May. I will keep that same rating on the stock. The company removed a large risk with the approval of Ngenla. The stock also has plenty of potential in its drug pipeline. The company has experienced a recent price drop as well. I want to see more of a turnaround in the Bioreference business and get a better idea on the future cash position of the business. The company is getting into a cash crunch quickly. I don’t want to get diluted or see the company take on more debt in the current high interest rate environment. Both options will eat at any potential return. This one is worth holding for the potential but a risk to buy due to the losses and cash concerns.

For further details see:

OPKO Health: FDA Approval To Save The Company