OPK - OPKO Health: There Could Be A Chance For Upside

2023-05-10 04:20:04 ET

Summary

- OPKO Health has been a very poor performer in my portfolio. The company has had a lot of ups and downs over the last few years.

- It has taken a new go-to-market strategy as of late. It has license agreements for two of its drugs with Pfizer and Merck.

- The company is awaiting FDA approval for Somatrogon, if approved, it could drive the stock price higher.

I want to start off by saying that OPKO Health ( OPK ) is my worst performing stock in my portfolio. I have held the stock for years. I experienced some losses on the stock and then kept on buying down. It left me with an even bigger loss. In hindsight, I should have been dumping the stock. You can go back and check my track record from previous articles and see that I missed it on this stock in the past. I will review through some prior points and where things might have gone wrong. In a single sentence the company was unable to execute on much of its pipeline of products. The company did see a boom during the pandemic as it performed COVID testing. That was short lived overall. It has also left the lab business in a loss making position as it was overstaffed and not prepared for the drop off in business from COVID. The company has seen a roller coaster ride on its stock price as well. It has fluctuated all over the board, part of it coming from the COVID testing boom.

Regardless, here we are. I still own a good number of shares in the company. I held onto my shares over the years. I think there is still potential for the company. As a drug development company there is always a lot of potential that comes with a lot of risk. It is never an easy or cheap process to get a product through the FDA approval process and then also be able to sell that product profitably. It is also a longer timeline for the pipeline to reach a revenue point. As it has been awhile since I wrote an analysis on OPK I thought it was time to revisit the company. See where the company is at with some of its product pipeline and if the company is worthy of investment at this point in time.

Price Action

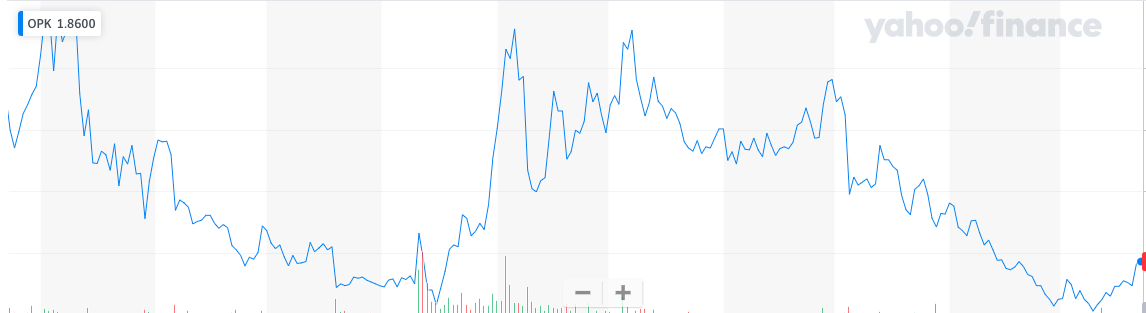

The price of OPK has been volatile to say the least. Much of this is based upon drug approval or denial. It has also been affected by COVID, which we will discuss further as well. The price chart below shows the ride that the company has been on. I will discuss further some of the reasoning for this volatility. The stock has seen highs over $6 a share and lows of under $1.

{kind=link}

The stock has seen a strong climb to start the year. It opened the year up at $1.27 a share and most recently closed at $1.86 a share. That is nearly a 50% increase for the year. I would attribute this climb to the potential approval of certain of its products by the FDA. Revenues may soon be materializing in other regions as well. I will discuss this further.

Rough History

I made my first investment in OPK many years ago. I was drawn in by the strong potential pipeline of products that the company had at the time. I also saw the experience of the founder, Dr. Frost, as a positive. Not as confident anymore if that carries true or not. They had two products that looked destined to be strong revenue drivers for the company at the time. I thought the first would help provide funding for the second and the company would be set for future revenue and growth.

The first product was the 4Kscore Test. The 4Kscore test can distinguish men with a low risk of having aggressive prostate cancer on biopsy from those with a high risk, helping to avoid unnecessary biopsies and overtreatment of indolent disease. It is non-invasive and is supposed to help reduce unnecessary biopsies and overtreatment. This seemed like a great product. It would help reduce unnecessary medical procedures as well as save hospitals and individuals money. It never was a success for the company though. It had issues getting reimbursement with insurance, it has eventually been able to get reimbursement but it started off rocky. The company still offers the test. It does not break out revenues for the product specifically. We can tell in general that it is not driving revenues higher though. It never really took off like the company expected or I hoped as well. It seemed that the company either underestimated the market demand for this product or it was not capable of taking the product to market. The latter seems a likely scenario in this case.

The second product was Rayaldee. This was supposed to be the home run drug for OPK. The company launched Rayaldee in the US market in November 2016, it is a treatment of SHPT in adults with stage 3 or 4 CKD and vitamin D insufficiency. It had a rough start as well. While most expected the company to receive approval it received a complete response letter from the FDA. This in fact was more to do with a contract manufacturer and not with the drug development. Either way it pushed the approval and release back. The company once again had difficulty getting the product to market. It has still not been a success as it continues to try and market and sell the product. Once again it still sells the product but it has never come close to achieving the market potential that was hoped for the drug. In the latest 10K the company noted the lack of success for the drug, “Sales of Rayaldee have not increased in accordance with its expected growth trajectory as a result of challenges in onboarding new patients due to several factors…”. It notes further on, “Sales of Rayaldee and our operations at Eirgen, are currently underperforming expectations and if we do not achieve our planned operating results, we may be required to incur a non-cash impairment charge”. The company has a 57-person sales and marketing team in the US dedicated to the launch and commercialization of Rayaldee. So it is not that the company is not spending effort and money, it just isn’t picking up new customers.

This lack of success can also be seen in the sales numbers. Revenue from sales for Rayaldee were basically flat year over year from 2021 to 2022. The company generated revenues of $27.3 million in 2022 and $27 million in 2021. Not only is there not any growth, it is of a small base value. Sales did see an increase in Q1 as compared to 2022. Sales grew from $5.1 million in Q1 2022 to $6.6 million in Q1 2023. This is still an annual run rate of $26.4 million. Maybe it will see an increase later in the year but overall it is still going to be an insignificant sum.

The one positive that has been coming from Rayaldee is that they have received some milestone payments as the drug begins to be sold overseas. In May 2016, the company entered into a development and license agreement with Vifor Fresenius Medical Care Renal Pharma for the development and commercialization in Europe and some other territories. This has finally started to kick back some success. The commercial launch for Germany happened in February and is now expanding into other territories. The company received payments of $10 million for the launch. The company is entitled to earn another $10 million in regulatory milestones and $207 million in milestone payments tied to the launch, pricing and sales of Rayaldee. It is also entitled to double-digit royalty payments. We will see how much of this is achieved. The company has not had the best success with the product launch so far but it is at least expanding markets and eligible to receive a good royalty if sales do increase.

The lack of success in these two FDA approved products has been disappointing. It is a long drawn out process to get products approved by the FDA. OPK did manage to get two through the process but has not been able to effectively commercialize either product. The company may have overestimated the potential of the drug, or it has just been unable to execute on the commercialization of said product. Developing a new drug and marketing that drug are very different processes. I feel that the company as a newer company was not prepared to take these drugs to market.

New Go To Market Approach

I think they learned their lesson from both of these products as they have taken a different go to market route on many of their other pipeline products. Rather than take the product to market the company works in the development stages and then licenses the rights to another party to take it to market. They have done so with a couple of large drug companies, Pfizer ( PFE ) and Merck ( MRK ). This helps ease costs for the company as oftentimes many of the expenses are borne by the partner. It also helps with the regulatory approvals process. Lastly these more experienced and larger partners have much more experience in getting a product to market. We have seen this with the last two main drugs in their pipeline, NGENLA (Somotrogon) and MDX-2201. We will quickly review these two drugs as they are the main future revenue drivers for the company.

Overall I view this as a positive for the company. They have shown a lack of ability to commercialize their portfolio. It will of course mean a lower potential return for the product. They are usually entitled to milestone payments and then also royalties on drug sales. If the drug is very successful they are only entitled to a portion of that success. I think in the end it will more than pay for itself as they can have lower costs without a sales team. Also their market partners will be able to achieve more success in the market than OPK would be able to. So their royalty payments without the costs for a commercial team will be more profitable than the company trying to commercialize these products themselves.

Somatrogon

In December 2014 OPKO and Pfizer entered into a worldwide agreement for the development and commercialization of OPKO’s long-acting hGH-CTP for the treatment of growth hormone deficiency (GHD) in adults and children, as well as for the treatment of growth failure in children born small for gestational age ((SGA)) who fail to show catch-up growth by 2 years of age. Under the terms of the agreement, OPKO received an upfront payment of $295 million and is eligible to receive up to an additional $275 million upon the achievement of certain regulatory milestones. Pfizer will receive the exclusive license to commercialize hGH-CTP worldwide. Upon the launch of hGH-CTP for Pediatric GHD the royalties will transition to gross profit sharing for both hGH-CTP and Pfizer’s Genotropin.

In February 2022, the European Commission granted marketing authorization in the European Union for Somatrogon (hGH-CTP) under the brand name NGENLA® to treat children and adolescents from as young as three years of age with growth disturbance due to insufficient secretion of growth hormone. Sales are underway by Pfizer for NGENLA (somatrogon) in 17 countries including Japan, Germany and the United Kingdom; NGENLA has been approved in 41 countries. Its European Union marketing authorization is valid in all EU Member States, as well as in Iceland, Norway and Liechtenstein. Pfizer expects to launch in all priority international markets by year-end.

The biggest hold up on the drug is that it did not receive approval in the US. The company submitted the initial Biologics License Application (“BLA”) with the FDA for approval of Somatrogon in the United States and Pfizer received a CRL in January 2022. Pfizer and OPKO have evaluated the FDA’s comments and are working with the agency to address their inquiries. This is a big hold up for the company. I think if it receives approval for the US, then you are likely to see much more positivity around the stock. Also OPK is due to receive a $90 million milestone payment upon approval in the US. This would do wonders for the balance sheet and help ensure that OPK does not have to raise more cash.

Regardless of the US approval, things are finally progressing with Somatrogon. The big question for me is when will revenues start to materialize for OPK. The company has spent a lot of money developing the drug, now it's time to start to see some revenues. During Q1 of 2023, the European region shifted to a gross profit share and going forward, both the European and Japanese regions will share in gross profit for the HTH franchise consisting of GENOTROPIN and NGENLA. When asked about revenues and breaking it out in financial reporting the company stated the following:

“I would expect that once it becomes individually material, we break it out in some of the disclosures. You would expect that perhaps, and once we have a U.S. region in the gross profit share, it will become more significant, but it could be later this year or into next year.”

While things are moving along for Somatrogon it appears that the company does not expect that to happen during this year. This was a little disappointing, I was hoping to start to see some positive income coming from the drug in the second half of the year. Rolling out a drug can take some time. You have to jump through a lot of insurance and approval hurdles. Also the US is expected to be the biggest market for the drug. So the holdup there is also a cause for the problems.

Overall it is good to see the progress on Somatrogon. It has finally reached the revenue stage for the company. While it does not expect significant revenue this year that should change in future years going forward. The one big question is the FDA approval. If it can achieve that then the company would be in a good position for a revenue jump. I think the company will get approval for the drug in the US. I think a big part of that will be due to Pfizer. They have the charge with approvals and commercialization. Due to their experience, I think they will be able to get approval in the US.

The other really important part for the Somatrogon approval in the US is that OPK is in line to receive a $90 million milestone payment from Pfizer upon approval. This is important to help shore up the balance sheet for OPK before it begins to generate revenues from its pipeline.

MDX-2201

OPKO Health’s ModeX Therapeutics, Inc. entered into an exclusive worldwide license and collaboration agreement with Merck to develop MDX-2201 for Epstein-Barr virus. Under the terms of the agreement, OPKO received a $50.0 million upfront payment and is eligible to receive up to an additional $872.5 million upon the achievement of prespecified development and commercial milestones. In addition, upon commercial launch of MDX-2201, OPKO is eligible to receive royalties on global net sales. Merck will be responsible for clinical and regulatory costs and activities, as well as product commercialization.

This is still early on in the approval process. From the announcement of the agreement, “ModeX and Merck will jointly advance MDX-2201 to an Investigational New Drug ((IND)) application filing, after which Merck will be responsible for clinical and regulatory activities, as well as product commercialization. Pre-IND filing activity will be guided by a joint steering committee comprised of representatives from both companies.”

It is still early on in the process. It still hasn’t filed an IND and cannot start clinical trials until that happens. Then it has to go through the 3 phases of clinical trials. It is not an easy process to get drug approval and this one is just getting started. So do not plan on seeing revenue from this drug for quite some time, if ever. That being said, the dollar amount for the milestone payments is a very large number and shows the potential that Merck thinks the drug has.

The thing I like most about this deal is that it will not cost OPK as much on the cash flow side. As part of the deal, Merck will fund the development of the drug. The company clarified on this point during the conference call.

“But currently, all expenses incurred by OPKO are reimbursed by Merck. And the reason is very simple is that because we have advanced the products so much that we are close to IND, and we need to really continue that without disruption…. And in terms of beyond the IND, it's really in the control of Merck. We may or may not be asked to continue to do certain things. But at this point, I can't comment. So fundamentally, the cost to us ModeX until IND is pretty much assumed by Merck on that time.”

Merck will reimburse all the costs for the drug at the moment and then going forward Merck will decide if it takes over the development and clinical trials or if it will have OPK run those. Either way the costs will not be borne by OPK. They already bore the costs to get the drug to this point and now are offloading the costs to Merck as part of the agreement. This is a great positive for OPK. If the drug gets through approvals, it is line to receive payments as well as receive royalties and at this point there are no, or minimal, additional costs for that potential revenue generation.

BioReference Lab

They also acquired BioReference Labs which at the time looked to be a profitable business that could also help fund R&D on the drug pipeline. It also seemed like a good fit since OPK develops lab test products such as the 4Kscore test. There were some potential synergies between the two companies that OPK hoped would drive revenues. This acquisition did not quite pan out like expected, at least not at first. It was not able to perform as profitably as hoped and was mismanaged. COVID changed that narrative as BioReference became a major COVID test provider. The Diagnostics or Services Business was unprofitable as well as the company as a whole. COVID changed that and the segment became profitable in 2020 and 2021. It even drove a profit for the company as a whole in 2020. Once COVID testing dropped off during 2022 the BioReference business dropped back into a loss making entity. The financials for the last 4 years are outlined in the table below.

| (In thousands) |

| 2022 |

| 2021 |

| 2020 |

| 2019 |

| Revenue from Services |

| 755,630 |

| 1,607,106 |

| 1,262,242 |

| 716,434 |

| Cost of Services Revenue |

| 627,548 |

| 1,102,172 |

| 823,899 |

| 511,206 |

| Gross Margin |

| 17.0% |

| 31.4% |

| 34.7% |

| 28.6% |

| Operating Income/(loss) |

| -173,652 |

| 98,067 |

| 138,922 |

| -123,359 |

As you can see the expectation of having the BioReference business be a profitable business to help drive drug development did not work out as well as hoped. COVID saved the business for two years as it became profitable due to COVID testing. They are now working on cost cutting as the slowdown in testing caught them in a position of being overstaffed. The services business lost a lot of money last year. In Q1 the metrics improved but still do not look good as the segment reported a loss of $40 million. I would expect these metrics to continue to improve as it cuts costs and looks for growth outside of COVID. It will still be a loss making business for the year.

Cash Flow Position

This is always a big question for a biopharma company. Pipeline products are not revenue generating and they have development costs. The income is out in the future so at what point does that revenue come in and do they have enough cash on hand to make it to the point of profitability. OPK does have some products in the market but as we have discussed there has been muted success with those products. BioReference labs continue to be unprofitable so it is not going to improve the cash position of the company either.

MDX-2201 is a long way from revenue generation. It is not going to be a factor in terms of cash for some time. Luckily Merck is paying the costs for the development so it is unlikely to be a large cash drain. The one question is for milestone payments. We do not know what the payment schedule looks like but there is a chance for certain milestone payments upon achieving clinical studies and different steps along the approval process.

Somatrogon is the main potential revenue driver for the company. It is also entitled to a $90 million milestone payment if Somatrogon receives approval in the US. That would do wonders for the balance sheet as sales begin to ramp up throughout the world. That approval or denial is likely to come soon. The question is, does the company have enough money on hand to avoid further dilution before royalty payments begin to be collected. Also there is a question if those revenues will be enough to make the company profitable. Much of this depends on the approval in the US.

The company currently has $110 million on its balance sheet. That is down from $153 million to end the year. Part of that decrease was due to repayments of credit lines. The company did burn through $22 million during the first quarter of the year. At that rate, the company only has 4 quarters of cash left on the books. The company provided estimates that were much worse for Q2 as it estimates a loss of closer to $80 million for the quarter. If we increase to that rate, the company will be in a cash crunch after next quarter.

The cash position is not looking good for the company. I think the company’s cash flow will trend up as the year goes on. They will continue to become more profitable with the Services business as they continue to cut costs and right size that business. They do have credit available, but they really need to see the approval for Somatrogon in the US. It will receive $90 million in payments which will buy another quarter or two in cash to the company. This can go a long way as they are entitled to double digit royalties.

Risks

The risks are very apparent with OPK. It is a loss making company. Much of its potential success as a company rests on FDA approval of Somatrogon. This is always a large risk as we do not know if the company will receive approval. Without the approval the company could find itself in a situation where it needs to raise more cash as well.

Conclusion

The company has not been able to commercialize its product portfolio. It has been able to receive FDA approval for a few of the products in its pipeline but not been able to take those products to market in a profitable way. The company has begun to partner with other companies for some of its pipeline. The hope is that those companies will have more success taking those products to market. There is less risk and less reward for OPK but overall I think it is a winning strategy.

I think there is still potential for the company as Somatrogon is being marketed in Europe and a few other countries. The big question is whether or not the company is going to get approval in the US. The stock has seen a strong increase to start the year. I think this is a bet by many that the drug will receive approval in the US. If the company is able to achieve approval then I think you will see the stock continue its climb. OPK stock is not without its risks. I do think there are potential future rewards for the company as well. I will continue to hold my position.

For further details see:

OPKO Health: There Could Be A Chance For Upside