OPP - OPP: Preferred Shares Offer A Safe 6.25% Yield

Summary

- OPP's preferred shares offer an excellent risk/reward ratio.

- The fund invests in high-yield debt, government and corporate debt, and CEFs.

- The asset coverage ratio is required to exceed 200% of the value of the preferred shares. If OPP fails to achieve this, it can be forced to redeem the preferreds.

- The preferred yield isn't the highest, but it is a very reliable yield.

Introduction

When I'm looking at fixed income securities like preferred shares, I don't need to have the highest yield, as that sometimes is a recipe for disaster as we, for instance, saw with Argo Blockchain ( ARBKL ) where the value of the baby bond was crushed. For me, investing in preferred shares is always a risk/reward tradeoff.

OPP's performance in FY 2022 was okay, and preferreds should be fine

RiverNorth/DoubleLine Strategic Opportunity Fund (hereafter just 'OPP' to keep it simple) is a closed-end fund focusing on creating value by focusing on a tactical income strategy and (up to 35% of the managed assets) and the opportunistic income strategy (up to 90% of the managed assets).

The portfolio mainly consists of bonds, closed-end funds and mortgage-backed securities. When I last discussed the CEF, stocks and preferred shares made up less than 16% of the assets, but the portfolio did not contain any common equity anymore while the preferred shares now still represent less than 5% of the portfolio.

{kind=link}

However, there's more than meets the eye here: OPP simply changed the description from 'common shares' to 'SPACs' as that's what the common share portfolio consists of. The combination of SPACs and preferred shares now exceeds 20%.

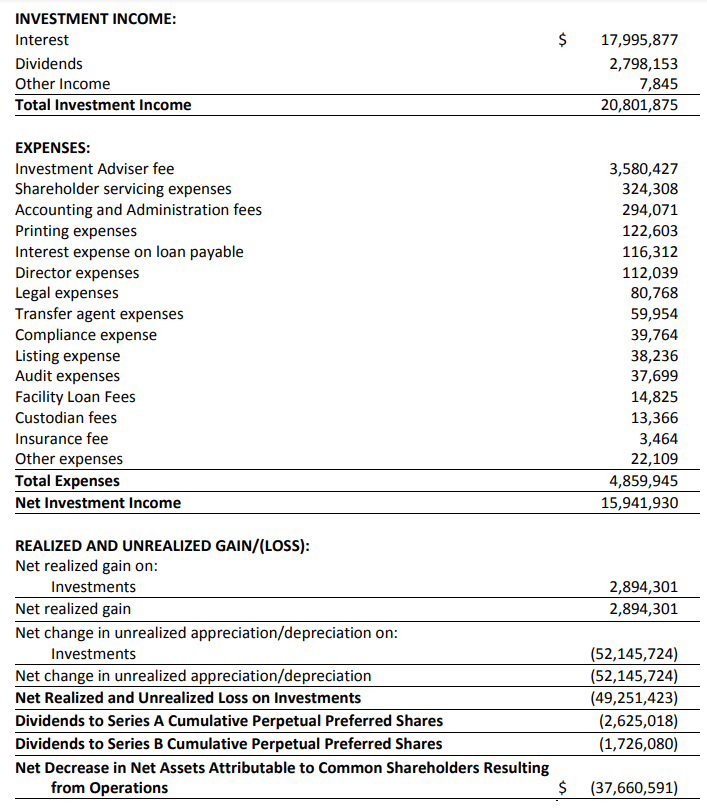

I'm mainly interested in how much interest and dividend income the OPP portfolio is generating. Looking at the income statement for FY 2022 (which ended in June), the portfolio generated about $20.8M in interest and dividend income, with almost 90% of that revenue coming from the bond and CLO portfolio.

{kind=link}

We also see the total amount of expenses is just $4.9M, resulting in a net investment income of $15.9M. As I am mainly interested in the preferred shares, I will ignore the $52M in unrealized depreciation on investments. While that has a negative impact on the NAV of the common units, it is an irrelevant factor to decide how safe the preferred shares are: ultimately the debt will be repaid to OPP and mark-to-market differences won't make a difference here: either the borrower repays OPP, or it defaults. And, of course, the lower portfolio value will be discussed when I look at the asset coverage ratio.

We still need to look at the preferred dividend payments. We see there was a $2.6M payment on the Series A preferred shares and $1.7M on the Series B. Keep in mind the Series B were only issued during the financial year and considering there are 2.4M preferred shares outstanding, the normalized preferred dividends on the Series B will be just over $2.8M. On a combined basis, the preferred dividends will cost OPP about $5.5M per year. With a net investment income of almost $16M based on the FY 2022 results, the coverage ratio of the preferred dividends is almost 300%. Not spectacularly high, but good enough for me.

A closer look at the two issues of preferred shares

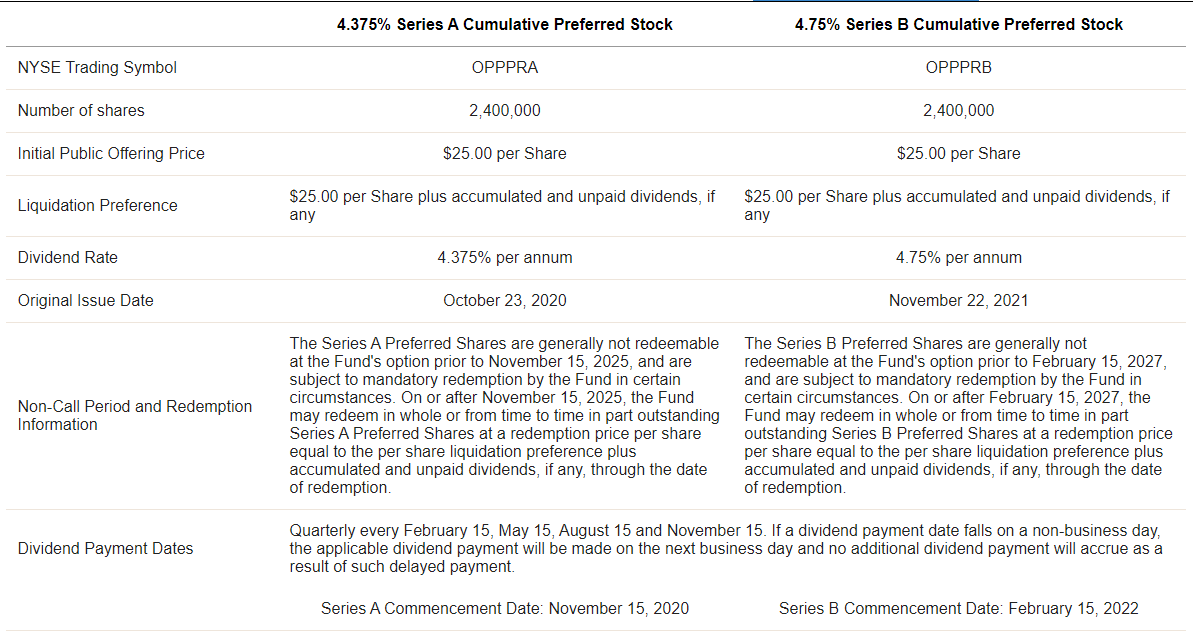

As explained in my previous article , OPP now has two series of preferred shares outstanding.

The Series A preferred shares are trading with ( OPP.PA ) as ticker symbol and offer a cumulative dividend of $1.09375 per share per year, which works out to a preferred dividend yield of 4.375% based on the par value of $25/share. These securities can be called from November 15th, 2025 on. And to be clear, the preferred dividend does not have a reset function: the $1.09375 remains unchanged until OPP decides to call the preferred shares.

The Series B preferred shares are trading with ( OPP.PB ) as ticker symbol and are also cumulative in nature. This series was issued in Q2 FY2022 (Q4 calendar year 2021) and OPP had to offer a higher preferred dividend to get the deal done, and these preferred shares are paying a preferred dividend of $1.1875 per share and can be called from February 15, 2027 on.

{kind=link}

What's interesting is that due to the increasing interest rates, both preferred shares are now trading substantially below par. OPP.PA closed at $17.96 on Monday night, while OPP.PB closed at $18.97, for a yield of respectively 6.09% and 6.26%. Needless to say that - as both series rank equally - I am favoring the OPP.PB series now, given the higher yield and higher likelihood the securities will be called (note: those odds are still pretty slim at 4.75% is pretty cheap for perpetual equity so although they are more likely to be called, I don't think a call is likely).

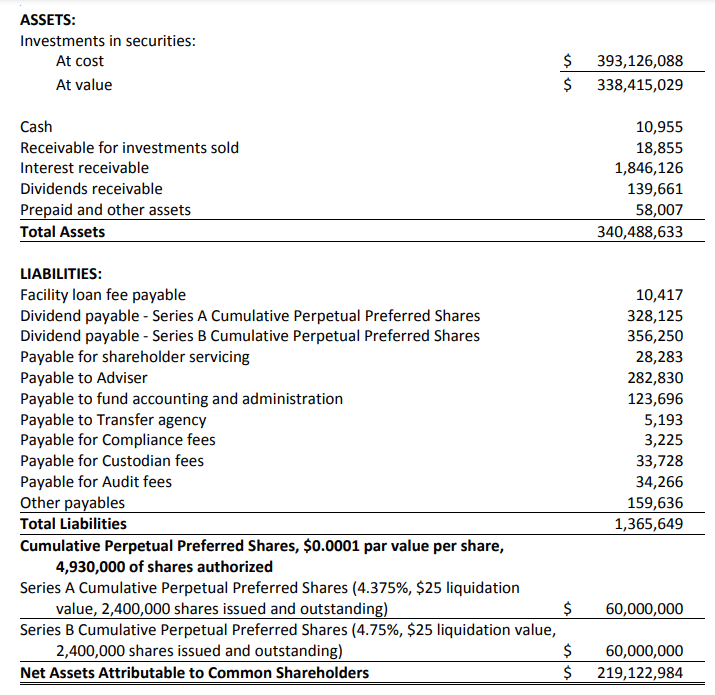

What I like most about these types of investments is the lack of debt on the balance sheet. As you can see below, the total amount of liabilities is less than $1.4M, which is less than half the total amount of assets.

{kind=link}

This means the preferred shares are pretty much first in line to be paid out should something go wrong. This also makes the asset coverage ratio interesting as the total amount of assets versus the $120M in preferred equity came in at 283%. So even if the value of the portfolio drops by 50%, the preferred shareholders can still be made whole.

The preferred shares have an additional interesting feature: if the asset coverage level drops below 200% (in this case, the total amount of assets would have to drop below $240M), OPP will either have to issue new common units to shore up the assets position, or will be forced to redeem the preferred shares at par value. And that's why I am not too worried about the unrealized losses. It hits the common unitholders harder, and the preferred shareholders are protected by the 200% rule. And keep in mind that subsequent to the end of the financial year, OPP raised about $34M in common equity through a rights issue. This makes the preferred shares safer.

Investment thesis

I currently still don't have a position in the preferred shares of OPP, but I am planning to go long in the next few weeks. At the current share prices, buying the B-series would make more sense as the yield is higher.

While the preferred dividend yield of 6.1-6.25% is definitely not the highest yield on the street, it is a 'sleep well at night' type of yield and the (standard) protection related to the required 200% asset coverage ratio adds an additional layer of safety.

For further details see:

OPP: Preferred Shares Offer A Safe 6.25% Yield