OPP - OPP: Too Many Cooks In The Kitchen Sour 17% Yield

Summary

- OPP is a fixed income CEF that allocates its cash between two principal strategies.

- The two strategies are run by different asset managers, namely RiverNorth and DoubleLine.

- The CEF is currently overweight non-agency MBS bonds and has significantly underperformed in 2022 as duration has increased.

- The fund has an unsupported 17% dividend yield and we expect a cut this year.

- This article covers CEFs from our suite of products - we focus on CEFs and yield-generating options strategies, targeting overall yearly portfolio returns of 9%+.

Thesis

It is not often that we see funds with negative Sharpe ratios. But RiverNorth/DoubleLine Strategic Opportunity Fund ( OPP ) is one of them. With a negative 3- and 5- year Sharpe ratio OPP takes significant risk with virtually no gains on a long-term basis: the fund's 3-year total returns are negative while the 5-year total returns are flat. Yes, you read that correctly. If you had bought OPP a while back you would have nothing to show for today, and when adjusting for inflation you would actually be losing money. For a buy-and-hold investor OPP is something to run from, not walk away, but run.

OPP markets itself on the notion that having two investment managers could somehow create some "magic":

RiverNorth allocates the Fund’s Managed Assets among two principal strategies: Tactical Closed End Fund Income Strategy (managed by RiverNorth) and Opportunistic Income Strategy (managed by DoubleLine). RiverNorth determines which portion of the Fund’s assets is allocated to each strategy based on market conditions. The Fund may allocate between 10% to 35% of its Managed Assets to the Tactical CEF Income Strategy and 65% to 90% of its Managed Assets to the Opportunistic Income Strategy

Source: Fund Fact Sheet

The allocation is dynamic which results in an ever-changing risk factoring and weighting. We generally do not like these types of funds because they rely too much on the manager's timing abilities rather than assets' alpha generating capabilities. These types of funds also tend to lack a proper benchmark due to their "unique" investment set-up. From that angle OPP does not fail in not delivering total returns. The market is aware of this as well with the fund trading at a -5% discount to NAV.

The fund currently displays a 17% dividend yield:

{kind=link}

This is unsupported and it will likely be cut, as the fund has done before in January 2022. The fund is fairly new, having IPO-ed in September 2016. Since the IPO, the CEF has managed to lose half its NAV and given the unsupported yield it will continue to do so in the future. We tend to see this type of behavior from fund managers which lack performance - when a CEF is not able to generate healthy long term returns they navigate towards the very high dividend yield angle to generate interest in the fund. Long term this strategy erodes the NAV, hence the recent fund rights offering .

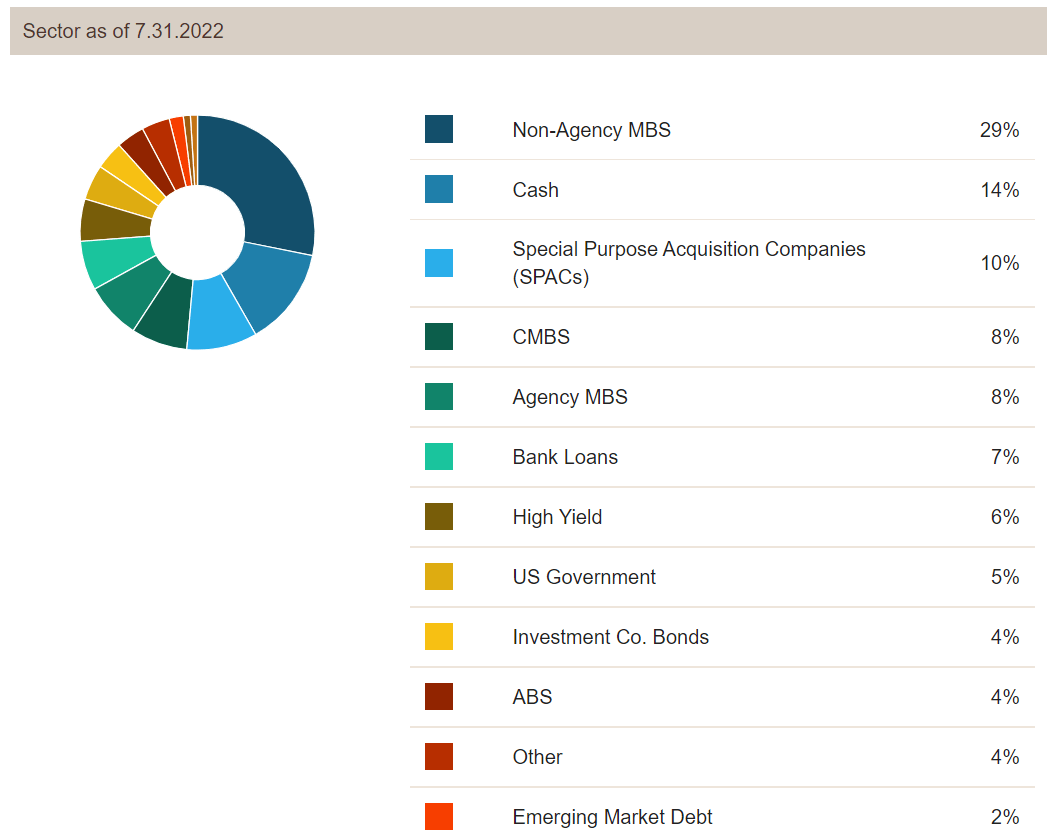

The fund holds a large allocation to MBSs (over 37%), with most of them being non-agency. A large portion of the non-agency MBS paper is also below investment grade. As mortgage rates have risen this year the duration has increased on MBS bonds due to lower pre-payment from homeowners (lower refinancings) which has resulted in lower prices and a lower NAV for OPP.

There is not much to like about this fund. Could you buy it after a significant sell-off and make a profit? Sure. Are there much, much better alternatives in the CEF space to do that? You bet. We do not like the sliding risk-factoring set-up for the fund, nor do we like the significant allocation to non-agency MBS bonds. The current tightening of financial conditions will continue and we have not seen the wides in mortgage rates. That will keep pressure on MBS bonds and increase duration via lower CPRs for many of them. We feel OPP is a great example of having too many cooks in the kitchen which results in a sour soup. New money and buy and hold investors should steer away from OPP - it offers very poor rewards for the risk taken. Existing stakeholders might want to Hold until late next year in order to recuperate some of the 2022 drawdown.

Holdings

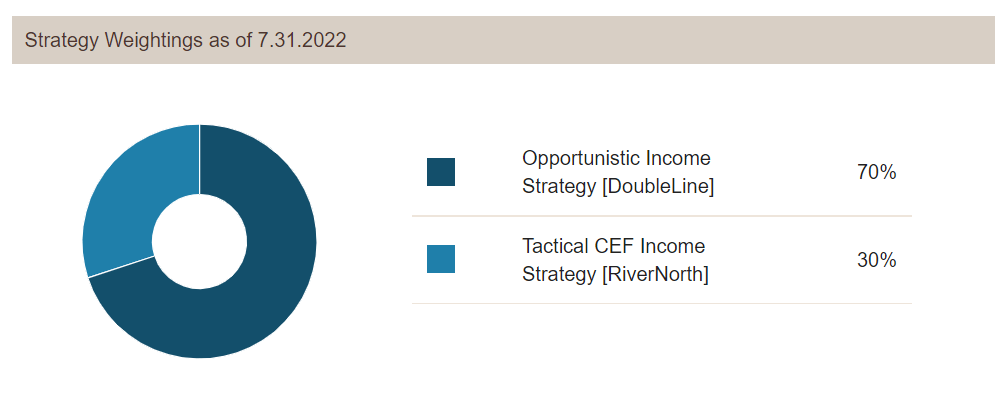

Currently the fund is overweight the Opportunistic Income Strategy:

{kind=link}

That set-up has resulted in a large portfolio allocation to non-agency MBS:

{kind=link}

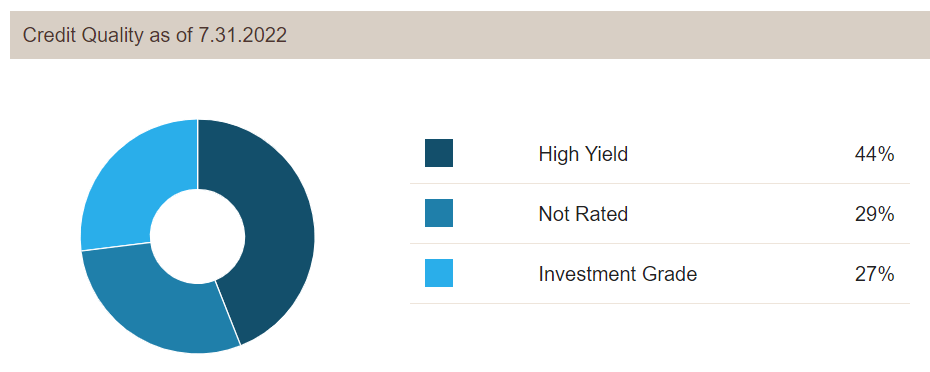

Many of the non-agency MBSs are below investment grade:

{kind=link}

We can see from the above graph that more than 44% of the fund has a rating that falls in the high yield category. Parsing through the assets we can infer that a significant proportion of the Non-Agency bucket falls in the below investment grade category.

Performance

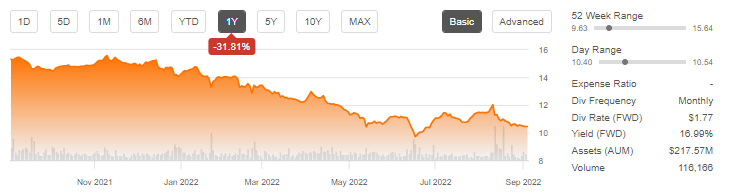

The fund is down almost -20% on a total return basis in 2022:

{kind=link}

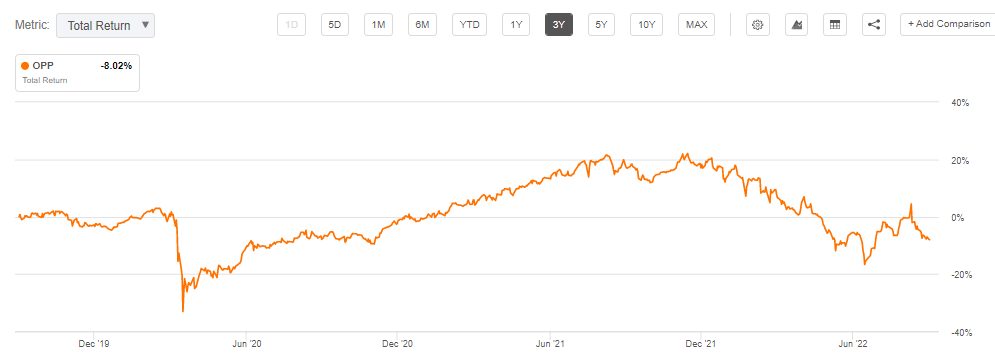

The fund has a negative 3-year performance:

{kind=link}

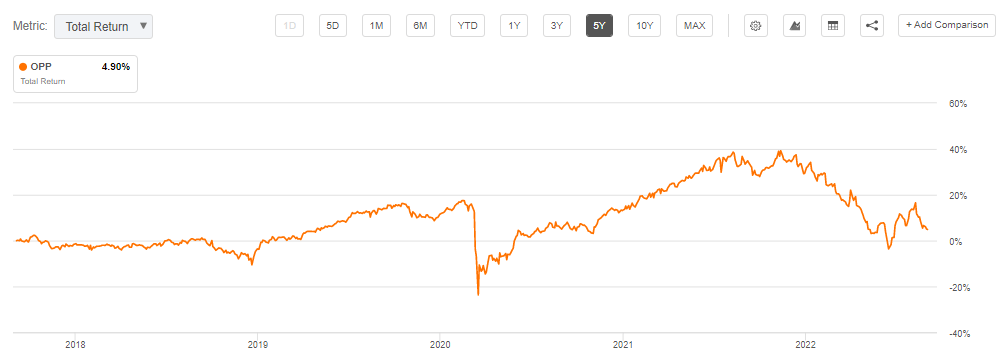

OPP has very poor 5-year total return metrics as well:

{kind=link}

Distributions

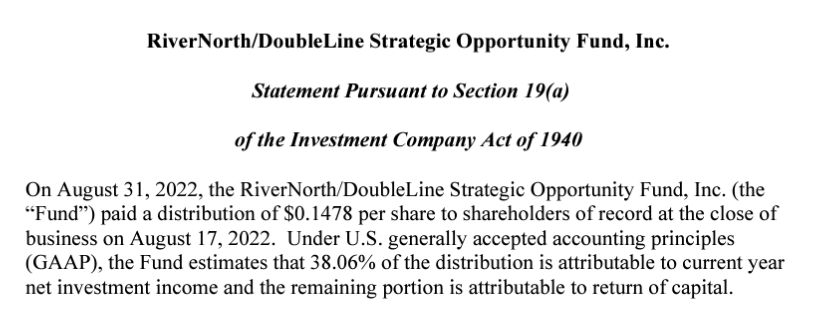

Over 60% of the current dividend consists of return of capital:

{kind=link}

We expect this to persist in 2022 as the fund underperforms from a NAV standpoint. If the assets do not generate enough cash-flow to pay the dividend yield then that money comes from investor "principal".

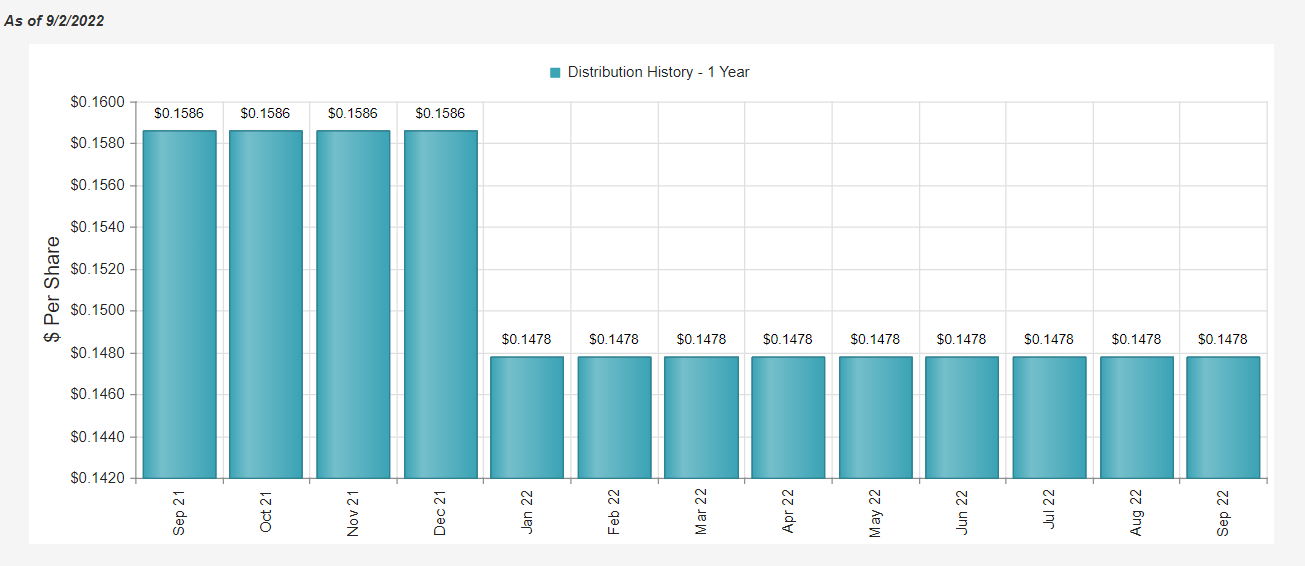

The CEF has cut its distribution before and we expect to see another cut this year:

{kind=link}

Conclusion

OPP is a fixed income CEF that allocates its cash between two principal strategies. The two strategies are run by different asset managers, namely RiverNorth and DoubleLine. This set-up provides for a sliding risk factoring and a dynamic portfolio allocation. The current holdings are overweight the DoubleLine strategy and non-agency MBSs. Due to the violent mortgage rate re-pricing this year the underlying MBS bonds have seen their duration increase and their pricing moving down, resulting in OPP being down almost -20% in 2022 on a total return basis. The fund has an unsupported 17% dividend yield and we expect the distribution to be cut this year. With a negative 3- and 5- year Sharpe ratio OPP takes significant risk with virtually no gains on a long-term basis: the fund's 3-year total returns are negative while the 5-year total returns are flat. New money and buy and hold investors should steer away from OPP - it offers very poor rewards for the risk taken. Existing stakeholders might want to Hold until late next year in order to recuperate some of the 2022 drawdown.

For further details see:

OPP: Too Many Cooks In The Kitchen, Sour 17% Yield