OPY - Oppenheimer Holdings Remains An Undercovered Buy Opportunity

2023-04-30 04:15:21 ET

Summary

- The Private Client segment will likely benefit from an interest-rate environment.

- The Asset Management segment may benefit from rising asset valuations.

- The Capital Markets segment will likely benefit from an increase in trading.

- Downside risk could come from headwinds to the banking sector overall.

Editor's note: Seeking Alpha is proud to welcome Albert Anthony as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

The undercovered stock of Oppenheimer Holdings (OPY), a major NYC financial firm headquartered blocks from Wall Street at 85 Broad, tracing its roots back to 1881, is a Buy opportunity, as I see potential in the stock looking forward towards the rest of 2023 and into 2024.

The firm's Private Client business segment will benefit from net interest income driven by a favorable interest rate environment for most of 2023, the Asset Management segment will benefit from rising valuations of assets it manages, and the Capital Markets segment will benefit from an increase in trading & sales.

The following outlines why I believe Oppenheimer is a hidden gem that will see its stock price grow from its April levels.

Private Client Business Driven by Favorable Interest Rate Policies

When considering the firm's longer-term performance on an annualized basis rather than just quarterly, we see in this past January's FY22 full year results press release that the firm's private client business had a $89MM increase (YoY) in bank deposit sweep income revenue, and a $22.5MM increase (YoY) in interest revenue.

In that release, Oppenheimer's CEO Albert Lowenthal commented:

In particular, bank deposit sweep income and interest income on margin loans increased significantly throughout the year, as both received a benefit from the short-term interest rate increases enacted by the Federal Reserve.

FY22 full year results - private client segment - Oppenheimer (Oppenheimer press release - FY22 results)

Although the current interest rate environment could reverse course later in 2023 and we don't know for certain the Fed's decisions ahead of time, I take the position that the Fed will maintain current rates or raise them again because there is no current indication that inflation has cooled enough to warrant major rate reductions just yet, and one of the Fed's mandates is to stabilize inflation.

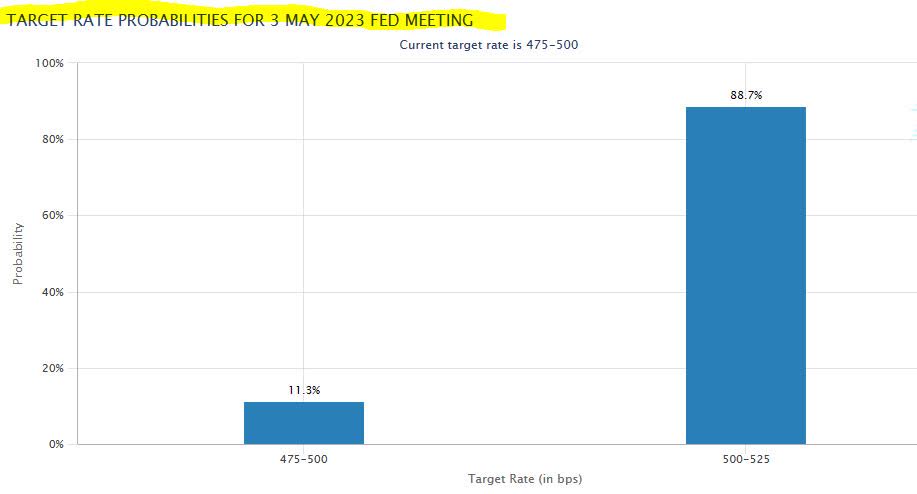

My opinion is echoed in the sentiment of ((CME)) Fedwatch below, showing the sentiment among rate traders who expect an 88.7% probability of a Fed target rate in the 500-525 basis points range, after the upcoming May 3 Fed meeting in a few weeks.

CME Fedwatch - Target Rate Probabilities (CME Fedwatch)

{kind=link}

Also agreeing with my position is a Reuters poll of economists who expect a 25-basis point hike, with rates holding steady for the rest of 2023.

With this rate environment expected, I am bullish on Oppenheimer since its private client division has proven to do well in 2022 after the continued Fed rate hikes, as we see in their results vs 2021, which was a much lower rate environment.

First-quarter results from some of its much larger peers in the banking sector, such as JPMorgan Chase (JPM) Q1 2023 results , already have shown a 49% increase in net interest income ((NII)) vs the same quarter in the prior year.

Asset Management Business Driven by Increase in Asset Values

Taking a look at the FY2022 results for the firm's Asset Management segment, we see a decline YoY in both advisory fees and ((AUM)), or assets under management.

FY2022 results - Oppenheimer - asset management segment (Oppenheimer - FY22 results press release)

Based on the firm's commentary in the release, the decrease in ((AUM)) was due to lower asset values but also due to net distributions. Advisory fee revenue decreased 5.1% from the prior year primarily due to lower management fees from advisory programs.

I think this trend will reverse in 2023 and early 2024, bringing this business unit at least back in line with 2021 performance, because in my opinion the values of equities in particular will rise throughout the rest of the year and next, bringing up with them the values of portfolios under management, and the associated management fees that firms like Oppenheimer make to manage money.

This trend was also predicted a few months ago in a market insights brief from JP Morgan called The Investment Outlook for 2023 :

By 2024, the U.S. economy may well be back on a path that looks much like that of the late 2010s - slow growth, low inflation, moderate interest rates and strong corporate margins. While this may not represent an exciting prospect for the average American worker or consumer, it is an environment that could be very positive for financial markets.

With that said, it is also important to note the larger sector, financial & banking, that Oppenheimer is in. So far in 2023, we have seen several large financial firms blow past analyst expectations for Q1 results, showing that the overall financial sector is still very strong despite the headwinds of the recent failures of Silicon Valley Bank & Signature Bank (SBNY), and the takeover by UBS (UBS) of rival Credit Suisse (CS).

In a piece this March in Kiplinger , certified financial planner ((CFP)) Don Calcagni predicted a market tailwind in 2023, which I concur with. According to Calcagni:

"Historically, market returns following relatively sharp declines have been quite good. Since 1926, stocks have averaged 12.5% returns in years following declines of 10%, while average returns increase to 22.2% in years following declines of 20%. The S&P 500 fell 18% in 2022."

Along those lines, I believe this will boost the asset valuations that Oppenheimer manages for clients, and boost its fees in this segment as well, so I am not overly concerned about last year's decline in this business unit, when looking forward into 2023 and 2024.

Capital Markets Business Driven by Increase in Trading/Sales

In its capital markets segment, the FY22 full year results actually showed an increased revenue vs 2021, as shown in the table:

FY 2022 - Oppenheimer results - capital markets segment (Press release - FY22 results - Oppenheimer)

In its full year 2022 results for its capital markets segment, equities sales and trading increased 1.9% compared with the prior year. Fixed income sales and trading increased 2.1% compared with the prior year, driven by higher trading income from U.S. government securities.

In my opinion, this direction going forward will increase in 2023 and 2024, driven by higher trading volume in the financial markets overall.

As someone who has lived through the trading frenzy of 2021, and taken part in it personally as a retail trader, but also having worked at a top 10 bank in the US and seeing the sheer volume of trading during the "meme-stock" frenzy, I believe that retail traders will make a strong comeback this year and be the market catalyst to drive the S&P back up to 2021 levels.

Consider the following from an article in Forbes just this past February:

The percentage of total trading volume coming from retail investors was about 23% from January 25 to February 1, JPMorgan's Peng Cheng wrote in a note to clients this week, narrowly edging out the record retail share of 22% in the pandemic-fueled trading frenzy and a massive increase in retail volumes since late last year, when it hovered at about 15%.

In fact, this increase in trading volume starting in February of this year was echoed by major trading platform Tradeweb as well, in a recent press release , stating that "total trading volume for February 2023 of $27.4 trillion. Average daily volume ((ADV)) for the month was a record $1.43 trillion, an increase of 21.5% year-over-year (YoY)."

Stock Price Outlook

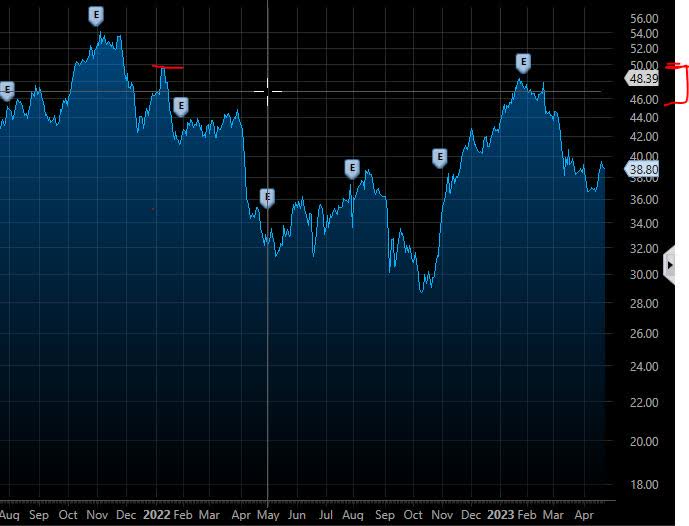

I am anticipating a forward-looking January 2024 price range in line with the December 2021 price range of $46 to $50, as shown in the chart below, based on my opinion & evidence shown that 2023 will be a rebound year, with financial stocks bouncing back from the 2022 market shocks & headwinds, the same as they bounced back from the 2020 pandemic shock.

While one may argue that a recession could also be looming in 2023 and that could dampen equities, I will side with economists from Goldman Sachs (GS) who only predict a 35% likelihood of a recession, in a January insights article .

This smaller likelihood of a recession, along with the other points highlighted, makes Oppenheimer worth considering as a good value if it remains in the $38 to $40 range well into May.

Chart of OPY price 2021 - 2023 (StreetSmartEdge trading platform)

{kind=link}

A Closer Look at Downside Risk Potential

It is also worth commenting on any potential downside risk that OPY could face as well, which could create headwinds to this stock price outlook.

Essentially, I believe the downside ironically is also tied to what the Fed ends up deciding, which we do not know with 100% certainty.

If the Fed continues with rate hikes, it could also impact the larger banking sector in the following ways: there could be a flight of deposits out of checking & savings accounts and into higher-yielding products. It could also impact banks that are holding a large amount of older Treasuries on their books, causing "paper losses" on mark-to-market bonds.

The issue of interest rate risk is not anything new, and in fact the St. Louis Fed remarked on the issue as far back as 1994, saying, "Interest rate risk can be significant for banks, especially for those banks with large securities holdings."

While OPY does not deal in consumer banking like traditional deposit accounts, which I think in their case is now a good thing, at the same time if several more banks in this sector run into trouble, investors themselves may ignore Oppenheimer's solid fundamentals and sell off shares in the financial sector stocks in general, concerned about sector contagion.

In late April, we have seen shares of First Republic Bank ( FRC ) drop as much as 50% over two trading days, after reports of deposit flight, echoed by the Wall Street Journal who highlighted, "First Republic's deposits fell by $100 billion over the course of the period ended March 31."

So, while I still think that OPY has solid fundamentals and is a good value, it is always possible that it gets caught up in another wave of bearish sentiment by investors selling off bank stocks, affecting the entire sector it is in, and therefore affecting OPY stock as well. What could be in Oppenheimer's favor in such a scenario is its size, brand strength, and the fact that it is not considered a smaller, riskier regional bank but essentially among the big players in money management.

Conclusion - A Bullish Rating

In conclusion, to reiterate the key points, I remain bullish on OPY stock due to expected continued strong interest income this year, continued strong trading revenue, and a rebound in asset valuations under management, driving up the firm's fees in the process.

I am maintaining a Buy Rating on OPY stock for the end of April and all of May 2023, with a forward looking sentiment of Hold afterwards.

For further details see:

Oppenheimer Holdings Remains An Undercovered Buy Opportunity