OPY - Oppenheimer: Resilient Investment Bank Priced Correctly

2023-07-11 13:17:19 ET

Summary

- Oppenheimer Holdings Inc. is an investment bank and broker-dealer that operates globally.

- Revenue has grown at a CAGR of 1% in the last 10 years, but looks to be resilient during what is currently a bear market.

- On an OPM basis, the business is highly attractive but NIM is poor.

- Oppenheimer is trading in line with its peers, who are far more profitable.

Investment thesis

Our current investment thesis is:

- Oppenheimer (OPY) is a quality business, with good margins and a resilient revenue profile.

- Growth has been mediocre but with a quality advisory foothold, the business should see growth.

- Our concern is that margins are too slim. Investors are better off with other IBs we have listed below, who are trading at a similar valuation.

Company description

Oppenheimer Holdings Inc. is an investment bank and broker-dealer that operates globally. The company offers various financial services, including brokerage, wealth planning, and margin lending. It also provides asset management services, investment banking services, fixed income sales and trading, and proprietary trading and investment activities.

Share price

OPY's share price has been volatile across the last decade, gaining over 100% in the period. Most of this occurred in the last few years, driven by a rapid increase in advisory work following the pandemic.

Financial analysis

{kind=link}

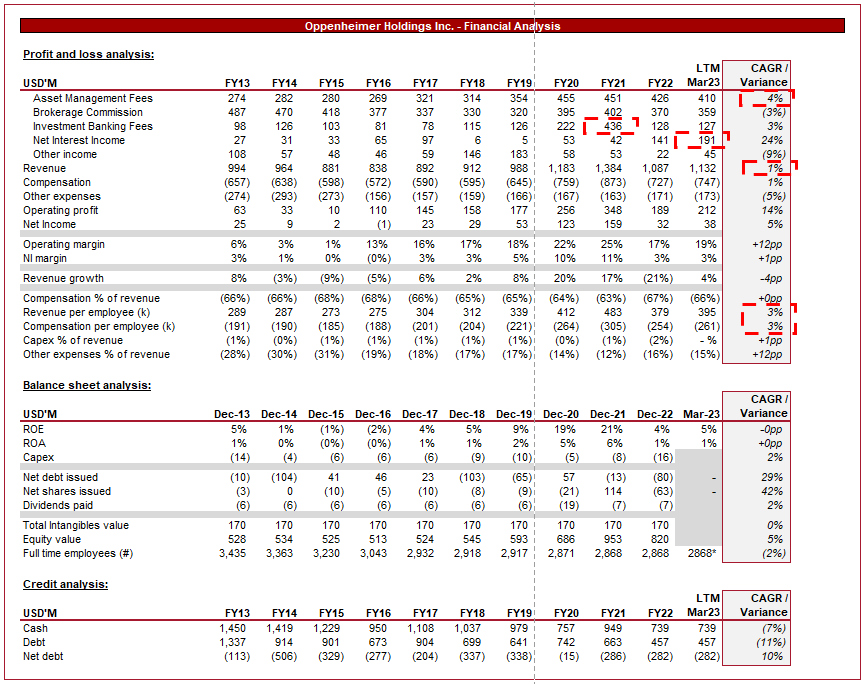

Presented above is Oppenheimer's financial performance for the last decade.

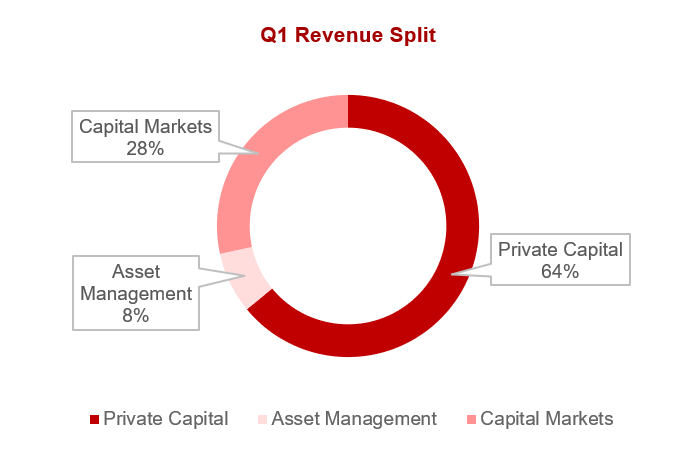

Oppenheimer currently segments its business into 3 categories, Private Client (Private wealth management), Asset Management (Traditional asset management), and Capital Markets (Investment Banking/Brokerage activities). In the most recent quarter, they contributed the following to revenue.

{kind=link}

Revenue

Oppenheimer's revenue has grown at a steady 1% across the last decade, although has seen periods of impressive gains and softening performance.

The company peaked in FY21, as did many other mid-market investment banks, due to an unprecedented boom in M&A activity. This is reflected in its IB Fees, which almost doubled in FY21 before declining 70%. This was driven by pent-up demand for investing following a decade of relaxed monetary policy.

Traditional IB services, such as M&As and IPOs, are not the primary operations of the business but are a large part of its operations. However, Oppenheimer showed an impressive ability to mobilize its workforce in FY21 to deliver on a rapidly increasing mandate. This is an important factor in our view as we are bullish for capital markets in the coming 5-10 years. The reason for this is the amount of dry powder (Uninvested capital) in the market, with Forbes estimating $2TN globally. There will be a pressure on Investment Managers to commit this capital over the coming years. Further, we are likely to see Capital market-friendly conditions return, as rates were only raised as a response to inflation, with the goal being to return to <1% levels.

The general weakness in FY22 onward has been driven by the increase in rates. This impacts all of Oppenheimer's services, not just IB. Rate increases result in:

- Future cash flows are discounted at a greater level as the cost of capital rises. This reduces buy-side valuations.

- The cost to financing investments through any portion of debt increases but disproportionately, as we usually see debt markets become more difficult to access.

- Consumers' cost of living increasing, leading to a slowdown in demand, which impacts businesses.

- Businesses find it more difficult to secure attractive financing, contributing to weakening performance.

This is why the business has seen its IB, Asset Management, and Brokerage fees decline. We are currently in a bear market where investment banks generally do not perform well.

For this reason, we place value in IBs who have some exposure to interest-bearing assets, as part of our ongoing analysis of boutique investment banks (See profile for other writing). This will allow for offsetting interest income, which acts in a countercyclical way. This is the case with Oppenheimer, with the business experiencing a 235% increase in FY22, with this continuing into the LTM. The net impact is an increase in revenue during the LTM, despite markets continuing to remain uncertain.

The question then becomes what is our outlook? Currently, US inflation, which rates are currently combatting, sits at 5%. This is heading down and its current trajectory suggests rates may have peaked. This being said, rates cannot begin a decline until inflation is reined in, which could mean a rate decline begins in late Q3 or Q4 2023. This would mean another year of heightened interest rates for Oppenheimer, partially (if not wholly) offsetting any market weakness.

Margin

Oppenheimer's OPM is quite attractive, having rapidly improved across the historical period. NIM has been less impressive.

Compensation is the largest cost to the business, having fluctuated around 66-68% of revenue. Our view is that a <65% level is good but 66% is not overly problematic. Compensation per employee has grown in line with revenue, suggesting incentives are aligned.

The big concern for us is the poor NIM, which is driven by a consistent non-trading expense. This eliminates value for investors in our view.

Q1 results

Private capital (Oppenheimer)

Oppenheimer's Private Capital segment has seen a bounce bank in performance, driven wholly by bank deposit sweeps and interest. If we exclude this, performance has continued to decline, as AUM falls. This said, once again interest income has shown itself as countercyclical during the current conditions, allowing the business to be resilient.

Capital Markets (Oppenheimer)

Banking activities have improved, driven by an increase in advisory fees. Management has done well to win work in what is still difficult trading conditions.

Underwriting has rapidly declined due to lower deal volumes and a slowdown in IPOs/SPACs.

Asset Management (Oppenheimer)

Finally, Asset Management fees have moved in line with Private capital, for the same reason, without the offsetting impact of cash sweeps.

Distributions

Management's distribution method of choice is dividends and buybacks, which have remained relatively mild throughout the historical period.

Peer analysis

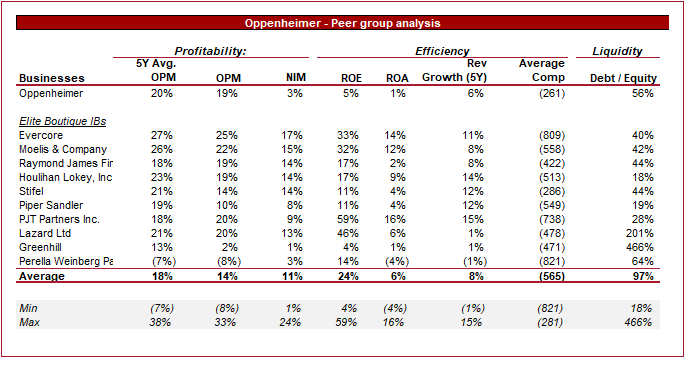

{kind=link}

Presented above is a comparison of Oppenheimer to a cohort of mid-market investment banks. It should be noted that these businesses do differ in operations, as some are boutiques (Wholly advisory work), while some are more diversified in services offered.

Oppenheimer's resilience is in full effect here, with its OPM decline in the most recent period being far below the peer group average. Further, if we exclude the weak members in the group, the company's OPM is in line with the top performs.

The problem is that Oppenheimer is far less profitable from a NIM perspective. This restricts the ability for distributions to shareholders.

Valuation

Valuation (Capital IQ)

Oppenheimer is currently trading in line with its peer group. The positives are that the business should be more resilient than the average should market conditions continue to be difficult. However, the issue is that on a NIM level, the business is significantly worse.

Key risks with our thesis

The risk to our current thesis is primarily on the downside. This would occur if market/economic conditions deteriorate further, which is not out of the question given the banking issues with have seen with SVB and others. This could cause short-term underperformance.

Upside potential would come from greater growth, which would offset the NIM underperformance.

Final thoughts

Oppenheimer is a good business, with a strong track record in asset management. The leading position in this segment allows the business to earn consistent, strong margins. The advisory segment of the business will allow Oppenheimer to partake in what we think will be the key growth area, and should hopefully allow the business to outperform relative to the poor growth it achieved in the last decade.

Our issue with the business, and why its valuation does not suggest enough upside for us currently, is its poor NIM. This does not allow investors to share in the rewards of growth.

For further details see:

Oppenheimer: Resilient Investment Bank Priced Correctly