OPFI - OppFi's High Debt Raises Long-Term Concerns

2023-12-18 13:21:37 ET

Summary

- OppFi is a fintech company that provides affordable lending options to individuals with limited access to traditional banking.

- The company's revenue growth rates have slowed down, creating uncertainty in the market.

- OppFi holds a significant amount of debt and may need a capital raise in the near future.

Investment Thesis

OppFi ( OPFI ) is a financial technology company that helps people with limited access to traditional banking by providing them with affordable and transparent lending options. They offer loans online, focusing on individuals who may not have a strong credit history or face challenges in obtaining loans from traditional banks.

OppFi has the makings of a potential turnaround. After all, its earnings are growing at a rapid rate higher. But I find its debt profile doesn't leave OppFi with much, or any maneuverability. Indeed, the question that looms large is how long until a capital raise takes place? I lay out my explanation for why I believe that OppFi could dilute shareholders by up to 20% in the coming six months and why I'm neutral on this stock.

Rapid Recap

In my previous analysis, nearly 2 years ago , I said:

"OppFi has seen its share price fall by 50% over the past 3 months. However, despite being a value investor, I will not be investing here and buying this dip.

The core of the issue facing OppFi is that its revenue growth rates have dramatically slowed down. And given management's own lack of visibility into the business, that creates uncertainty during a time when markets are already particularly anxious.

With that in mind, even if the multiple that investors are willing to pay for OppFi has meaningfully compressed in the past 3 months, there's no rule to say that the multiple cannot compress further.

With all that in mind, I'm giving this investment a pass."

Since that time, the share price has moved lower.

Michael Wiggins De Oliveira on OPFI

However, I now revisit this name with a fresh pair of eyes but remain neutral on the stock because I find its balance sheet restricts my upside potential. Here's why.

OppFi's Near-Term Prospects

OppFi is a fintech company, that collaborates with community banks to extend credit access to underserved Americans. Through its lending, financial inclusion, and transparent practices, OppFi aims to provide better financial health solutions for consumers who may be turned away by mainstream options.

During OppFi's recent Q3 earnings call , last month, CEO Todd Schwartz underscored OppFi's commitment to enhancing credit models with bank partners, resulting in improved credit performance, evident in key metrics such as a 23% reduction in the net charge-off rate as a percentage of total revenue. The company's strategic focus on maintaining a robust credit profile positions it well for continued credit performance and earnings growth, instilling confidence in its ability to navigate challenges in the financial landscape.

OppFi's strategy for near-term growth revolves around a disciplined approach to underwriting while prioritizing profitability over extensive portfolio expansion. Schwartz highlights the success of credit modeling enhancements and adjustments, which have generated dynamic credit models, contributing to improved early-stage delinquency metrics.

Additionally, the company's product and marketing team is actively engaged in cost-effective initiatives, including SEO and direct mail, aimed at attracting lower-risk origination volume.

Given that background, let's now discuss its financials.

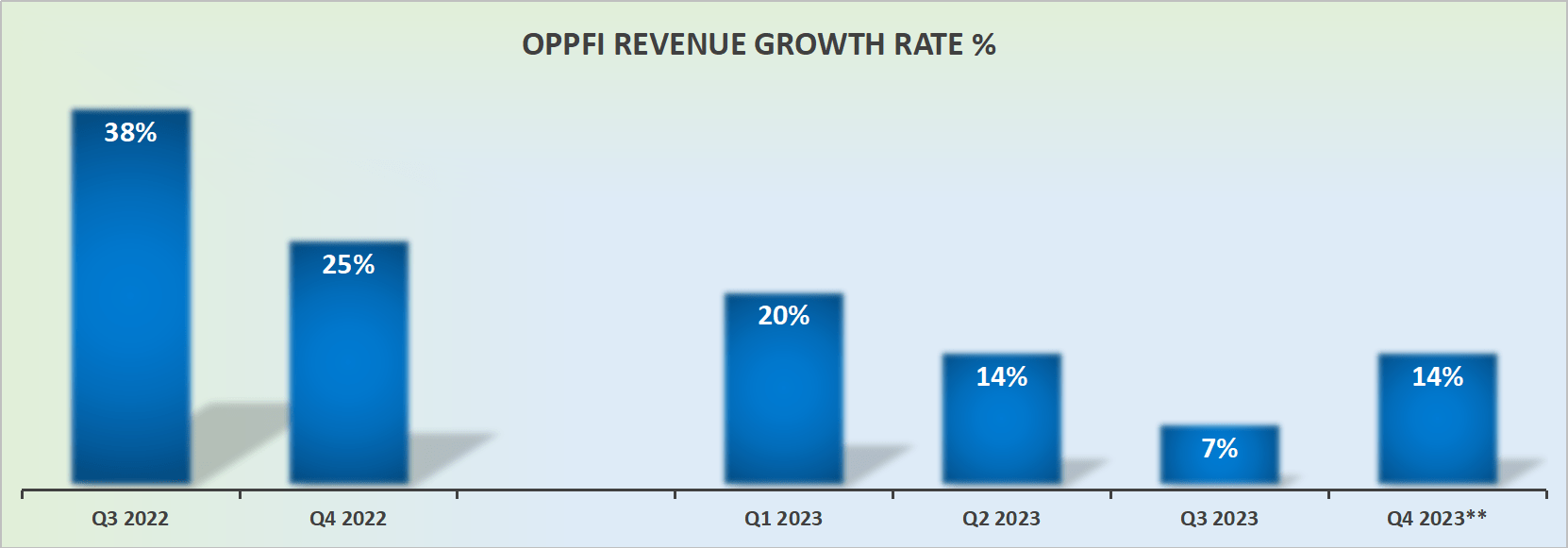

Revenue Growth Rates Are Stabilizing

{kind=link}

OppFi's Q4 guidance points to approximately 14% y/y growth rates at the high end or $140 million in revenues. Put another way, it appears clear that the period when OppFi could be counted on for impressively strong growth rates is now in the rearview mirror.

Is it possible for OppFi to reaccelerate its revenue growth rates or is this as good as it's going to get for now? That's a key question, and I'm struggling to get comfortable seeing this business returning to 20% CAGR any time soon.

And while I recognize that the business is clearly GAAP profitable, despite having approximately $50 million of interest expense payments, I remain resolute that there's more to this story. In fact, the real thesis breaker for me is found in the next section.

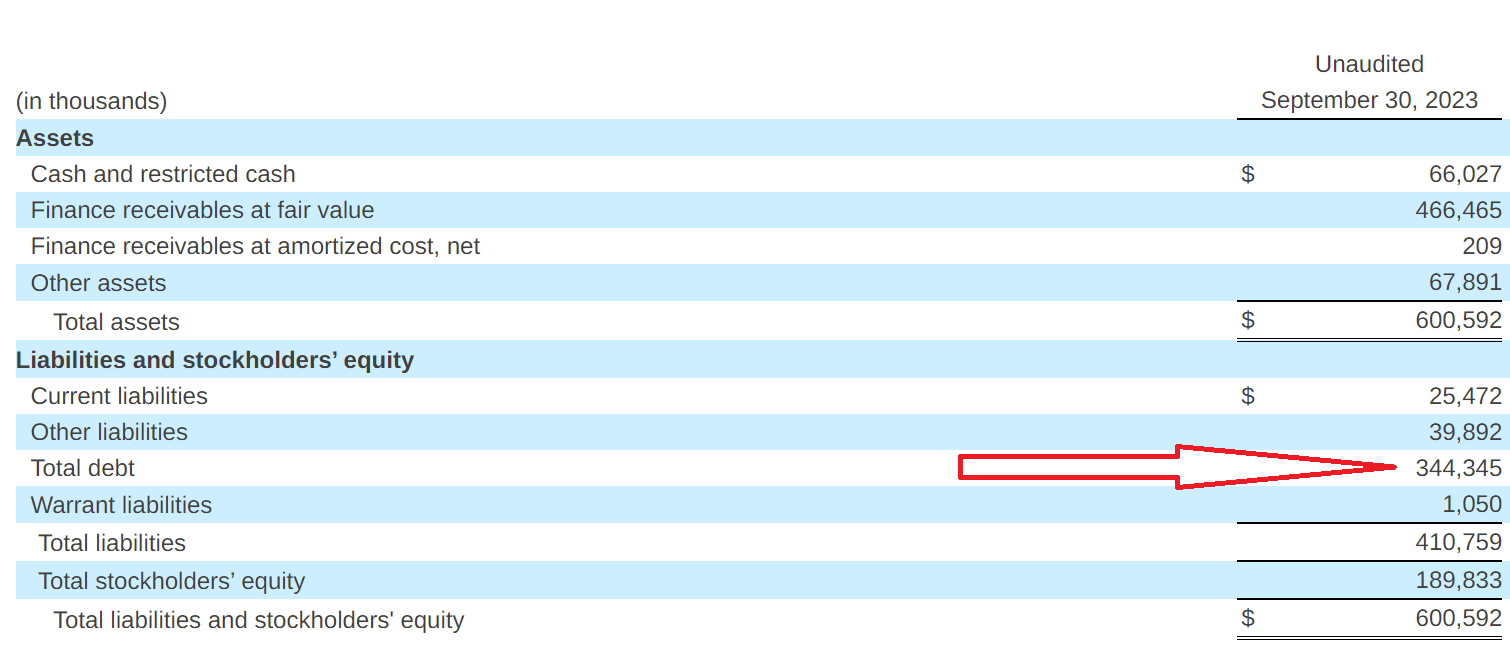

Financial Footing Looks Poor

{kind=link}

OppFi holds a lot of debt. What's more, during the earnings call, management noted that its debt has a cost of borrowing of 11% . That's really high. And although the business could survive and raise capital, it will have to work very hard to convince creditors to borrow more capital at attractive rates.

According to its SEC filings , the business holds about $30 million in unrestricted cash against more than $300 million of debt. These numbers don't inspire much hope for the long-term prospects of this business.

Could A Capital Raise Take Place?

As it stands right now, approximately 60% of OppFi's market cap is made up of debt. That's not a compelling investment opportunity.

On top of that, for 2023 as a whole, its non-GAAP adjusted operating profits stood at $40 million. Think about this figure. Even if we presume that in 2024, its non-GAAP adjusted operating profits increase by 20% y/y to $50 million, this would still mean that at the present run-rate, it will take more than 5 years of future non-GAAP operating profits to be diverted toward improving its balance sheet.

{kind=link}

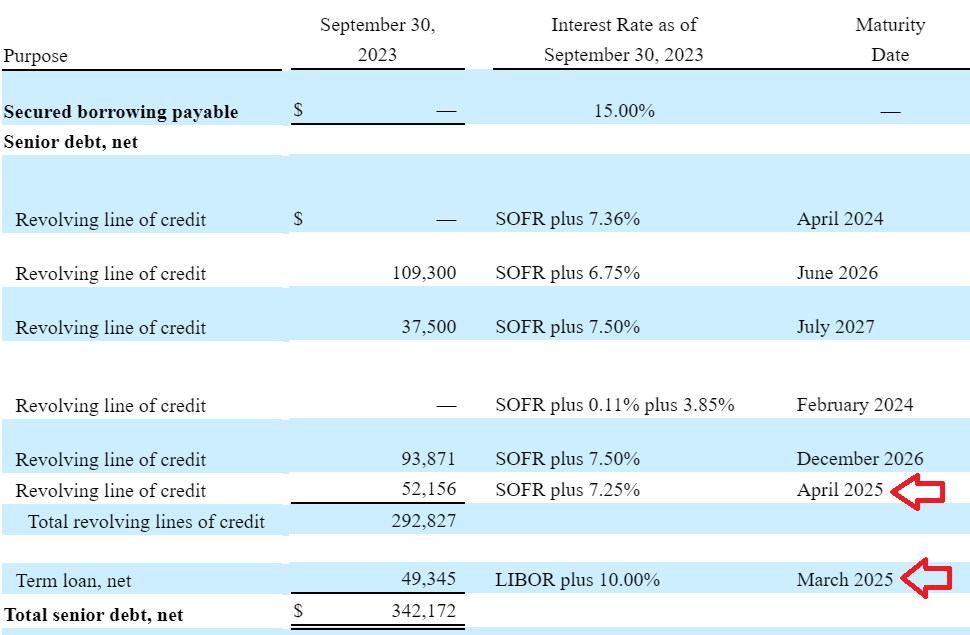

And if that wasn't sufficiently unappetizing, think about this, in 2025, OppFi will have to pay back or refinance approximately $100 million worth of debt.

Naturally, OppFi will want to tackle this debt, before it becomes current, meaning due in less than 12 months.

This means that OppFi will have to take the full cash sum on its balance sheet, plus whatever other free cash flows it can generate in the coming twelve months, to meaningfully chip away at its debt.

For my part, I believe that with so much debt on its balance sheet, and its share price recently showing significant strength, I believe that management could look towards some sort of capital raise within the next 6 months. Although, I suspect this raise will not be more than 20% of its market cap or $100 million of funds.

OPFI Stock Valuation - 9x Forward Non-GAAP Operating Profits

For my valuation estimates, I presume that in 2024, OppFi could deliver $50 to $55 million of non-GAAP operating profits. This is approximately a 25% increase from 2023's guided non-GAAP operating profits of $42 million.

My estimate here presumes that OppFi continues to grow its topline at about 20% CAGR, in line with the current forward revenue growth rate estimate.

On top of that, I have assumed that there's some level of cost savings taking place, given that OppFi's organic investments in operations have started to deliver decreasing returns on investment since we can see that its revenue growth rates have generally decelerated relative to 2022.

Altogether, this leaves this stock priced at 9x forward non-GAAP operating profits. A figure that bulls will be quick to remark is a bargain entry point into this stock.

However, I maintain that with so much debt on its balance sheet, investors are getting a stock that looks cheap on the surface, but in time, unless its debt gets tackled in a satisfactory manner, will in time look even cheaper.

The Bottom Line

In evaluating OppFi's current standing, I am confronted with a sense of uncertainty and doubt, particularly concerning its considerable debt relative to the cash on its balance sheet.

Despite the apparent turnaround potential highlighted by the growing earnings and improved credit performance, the question of how long OppFi can navigate its debt profile without a capital raise looms large.

The unease is palpable, given the observation that the business is left with limited maneuverability, and the need for a capital infusion could surface.

Altogether, I remain neutral on this stock.

For further details see:

OppFi's High Debt Raises Long-Term Concerns