NEE - Opportunities Abound In These Dividend Stalwarts

2023-09-29 08:15:00 ET

Summary

- Market timers come out in force when stocks are soaring or plummeting, but often miss out on long-term investment opportunities by waiting to make sure stocks have definitively bottomed.

- I like to keep it simple by buying high-quality dividend growth companies at discounted prices during bear markets. If they get cheaper, I buy more.

- I highlight a handful of high-quality, investment grade-rated dividend growth stalwarts to consider for your portfolio.

You make most of your money in a bear market. You just don't realize it at the time.

--Shelby Cullom Davis

The market timers are out in force right now.

They thrive in market environments where stocks (or certain types of stocks) are either soaring higher at a rapid clip or plummeting with no bottom in sight.

The former was the case in 2021, when market timers proclaimed fellow investors foolish for looking askance at the unprofitable tech startups trading at 100x sales (no profits available yet upon which to base valuations). FOMO and YOLO prevailed.

Today, the market timers are back, but they're in a decidedly more pessimistic mood, proclaiming foolish all those investors who are trying to catch falling knives.

A stock drops from $200 to $100, from a price/earnings ratio of 20x to 10x, and the long-term fundamentals for the company and its industry still look good.

I would argue, as I did in " REIT Crash: The More They Drop, The More I Buy ," that the hypothetical stock above has become attractively valued for long-term buy-and-hold investors. During bull markets, we always wish we'd bought more during bear markets. Well, now is our chance!

But in the market timer's mind, it's obviously a terrible idea to buy a stock while it's still falling.

The market timer looks at that hypothetical stock that has fallen from $200 to $100 and says, "I'm not buying until it hits $50." (They usually pick a nice, round number that has nothing to do with any fundamental valuation.) Sometimes, the market timer gets their wish and is able to buy the stock at $50. This makes them feel smart for a moment, until the stock keeps dropping and they realize they've joined the ranks of the existing shareholders who are now being ridiculed by the next batch of market timers, saying, "I won't touch it until it hits $25."

Notice that both when stocks are soaring and when they're plummeting, the market timer doesn't have time (pardon the pun) for valuations or fundamental analysis. Their calls are based on the stock price, which itself is largely being moved by other market timers (including computers and algorithmic traders).

For a little while, the shrewdness of market timers always feels more exciting and alluring than the boring wisdom of the buy-and-holders.

Here's my strategy:

- Buy high-quality companies

- that pay a growing dividend

- at a discount to fair value (and thus an attractive dividend yield )

- and wait patiently as they compound over time .

Rinse and repeat.

Bear markets simply offer deeper discounts and more of them. They are not a good excuse to deviate from the strategy. Quite the opposite. They're the perfect time to double down on it!

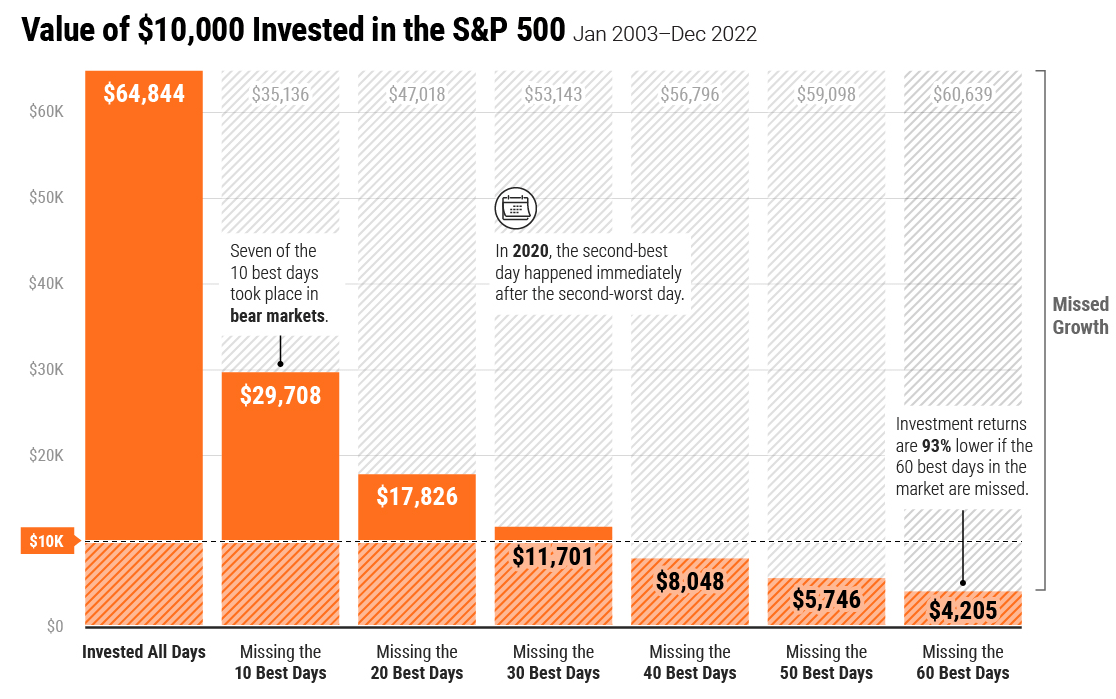

The strategy of the market timer seems to be to wait to buy stocks until they are definitively in an uptrend. But that risks missing the best days in the market!

{kind=link}

Notice that in 2022, the second best day in the market happened the following trading day after the second worst day in the market.

I am sure during that second worst trading day, the market timers were out saying, "Don't try to catch a falling knife!"

But this catchy phrase implies either that:

- One will be able to buy at the exact bottom, which requires about as much luck as winning the lottery

- One will wait until the market is in a confirmed uptrend before buying, which most likely means that they will miss many of the best days in the market

Contrary to this, my plan is to keep accumulating shares of high-quality, dividend-paying companies at opportunistic valuations and above-average yields.

What if their stock prices keep falling? I'll accumulate shares at lower prices and higher yields.

I find that focusing on fundamental analysis and dividend income helps me stay calm and remain invested when I'm tempted to listen to the market timers' siren song.

After all, for me, successful investing is defined not by continuously rising stock prices but rather continuously rising total dividend income from my portfolio.

Research by the famous economist Robert Shiller found that since 1957, stock prices have been twice as volatile as their dividends.

And perhaps even more importantly, dividend growth over long periods of time has significantly outpaced inflation. Take my two favorite dividend ETFs -- Schwab US Dividend Equity ETF ( SCHD ) and iShares Core High Dividend ETF ( HDV ) -- as examples:

Over the past decade or so, their dividends have grown significantly faster than the consumer price index ("CPI"), the primary measurement of consumer inflation.

You could of course wait to buy until the Fed starts cutting rates, or a recession is confirmed, or we are definitively emerging out of a recession.

But with the incredible buying opportunities available right now -- not just among the low-quality dividend payers with heavy debt burdens but also among the high-quality dividend stalwarts -- waiting seems to me like letting a fat pitch come right down the pipe into the strike zone, assuring yourself that the next pitch will even be better.

What dividend stalwarts do I have in mind? I'm so glad you asked. I'll highlight a handful.

Alexandria Real Estate Equities ( ARE )

- Dividend Yield: 5.0%

- 5-Year Average Dividend Growth: 6%

- Price/AFFO: 11.1x

Incredibly, this owner and developer of world-class life science real estate properties now trades at a price to adjusted funds from operations ("AFFO") of 11.1x, its lowest level since the Great Recession of 2008-2009. This despite projecting 6.4% AFFO per share growth this year, having no debt maturities until 2025, and boasting an incredible weighted average remaining debt maturity over 13 years.

The market is worried about the size of the life science development pipeline in place today. Roughly 1/3rd of all office space currently under development is life science buildings. Moreover, conversions of traditional office space into other uses has roughly doubled this year from last year, with nearly 1/5th of this space being redeveloped into life science.

Amid this wave of new supply, there are two important points to keep in mind:

- Location and quality matter. The world's leading biotech companies generally do not seek out the lowest priced life science space but rather the highest quality and best located space. That's what gives ARE's state-of-the-art facilities located in leading innovation clusters a competitive advantage.

- Newcomers to life science property development face significant challenges. Not only have construction costs gone up, the length of time it takes to obtain certain equipment, materials, or skilled labor in order to complete projects stretches from 4 weeks to 2 years. Thus, many of these announced projects will be canceled, and those that are completed will likely take a lot longer than the market thinks.

Cushman & Wakefield

At a 5% dividend yield, ARE looks like a steal.

Brookfield Infrastructure Partners ( BIP )

- Dividend Yield: 5.25%

- 5-Year Average Dividend Growth: 6%

- Price/FFO: 9.7x

This flagship infrastructure fund from parent/sponsor company Brookfield Asset Management ( BAM ) boasts a global presence, wide diversification across asset types from energy to transportation to data centers, and enjoys an investment grade credit rating of BBB+.

And though the share price has taken a dive recently, it's a comfort to know that BIP has no further funding needs for its growth program this year. It has already raised all funds necessary through capital recycling and issuance of BIP's corporate equivalent, Brookfield Infrastructure Corporation ( BIPC ), which trades at a premium to BIP.

(Those wishing to avoid K-1 forms should stick with BIPC, although the LP is cheaper and higher yielding.)

Around 70% of BIP's cash flows come from long-term contracts or regulated utilities, and 70-75% enjoys inflation-linked fee escalators, both of which provide high stability. And the company has been using those cash flows from stable industries like utilities, oil & gas pipelines, and toll roads to invest in fast-growing sectors of the economy like data centers. BIP expects to more than triple its global data center capacity over the next three years.

Even amid the current high interest rate environment, management projects FFO per share growth averaging 10-12% over the next three years, which should easily support its 5-9% annual distribution growth target. Given the 68% AFFO payout ratio expected for 2023, the dividend also has plenty of buffer while providing some retained cash flow.

Perhaps most importantly, BIP's return on invested capital is consistently around 12-13% and has been slowly rising over time. Those Brookfield folks are darn good capital allocators.

Medtronic Plc ( MDT )

- Dividend Yield: 3.5%

- 5-Year Average Dividend Growth: 7.4%

- Price/Earnings: 15.1x

This global medical devices giant suffered a hit from COVID-19 due to foregone or postponed elective surgeries, and since then supply chain difficulties and foreign exchange headwinds have caused some stagnation. But MDT has drastically improved its supply chain and growth outlook. In addition, the company boasts multiple competitive advantages:

- A strong history and culture of innovation, exemplified by its >45,000 patents and record of investing ~7% of sales into research & development (which management plans to increase to 8-9%). They are investing in new products for surgical robotics, diabetes monitoring, blood pressure monitoring, cardiac catheters, and so on.

- Recession-resistant product offerings, as a result of being tied to necessity-based medical procedures and paid for by third-party insurers. During the GFC in 2008-2009, revenue grew right through the recession.

- Strong, investment grade balance sheet with low leverage at a debt to EBITDA ratio of 1.8x.

The market seems to worry that new, popular weight-loss drugs like Novo Nordisk's ( NVO ) Ozempic, which have seen a huge surge in prescriptions recently, will hurt MDT's product sales, especially for diabetes devices. But management insists that MDT's automated delivery system products should continue to be in demand among both Type 1 and Type 2 diabetics.

As the world population ages and MDT expands into emerging markets, I believe the company will be able to rejuvenate its high single-digit growth rate going forward. As a result, the 45-year dividend growth track record should continue indefinitely.

NextEra Energy Inc. ( NEE )

- Dividend Yield: 3.1%

- 5-Year Average Dividend Growth: 12%

- Price/Earnings: 18.5x

NEE is the largest and arguably best managed regulated utility in the United States, being the parent company of Florida Power & Light. It is also the largest developer of renewable power generation assets in the nation as the parent company of Energy Resources.

The company's consistency of earnings and dividend growth speak for itself:

NEE September 2023 Presentation

Even after recently halving the distribution growth outlook for NEE's renewable energy YieldCo, NextEra Energy Partners ( NEP ), from 12% to 6%, NEE's projected EPS growth remains unchanged. Management says NEE will achieve 6-8% annual EPS growth through 2026 and 10% dividend growth through at least next year.

Given the ~20% selloff in NEP after this announcement, the market seems to think that NEP will no longer be equipped to support NEE's growth plans by buying its stabilized assets. The very worst case scenario seems to be that NEP gets rolled up by NEE, and NEP shareholders get bought out at an unfavorable unit price.

I highly doubt that will be the case. It is in NEE's interest to ensure NEP survives and regains an adequate equity valuation to continue issuing units in order to buy assets from NEE. Plus, given management's plans to sell gas pipelines in NEP's portfolio in order to eliminate convertible equity in the coming years, NEP has no need to issue equity for growth investments through 2027.

The team at NEE have proven themselves capable capital allocators over the years, resulting in a 27-year dividend growth record. I'm confident they can manage through the current storm as well.

Bottom Line

Opportunities abound in high-quality dividend stalwarts like the four mentioned above. You could certainly try to time the market by waiting to see if you can get them cheaper, but I'd rather stick to my strategy of continuously accumulating shares for as long as they remain cheap.

Whether or not the stock prices of these blue-chip dividend growers decline further, I think patient investors will be richly rewarded for buying them in the long run.

For further details see:

Opportunities Abound In These Dividend Stalwarts