PSEC - Opportunity: Investment Grade Bond +8% Yield From Prospect Capital

- An explanation of how traditional bonds work and how they differ from baby bonds.

- We discuss how to locate information on traditional bonds.

- A favorite traditional bond – the deeply discounted 2028 Prospect Capital investment-grade bond with an 8% yield-to-maturity.

Co-produced with Preferred Stock Trader

How Traditional Bonds differ from Baby Bonds

When speaking of “traditional” bonds, we are speaking of bonds that do not trade on the stock exchanges as baby bonds do. The differences between traditional bonds and baby bonds are as follows:

-

Traditional bonds typically have a face value or maturity value of $1,000 where baby bonds commonly have a $25 maturity value (although not always).

-

Traditional bonds all have unique CUSIP numbers, and they trade using this CUSIP number, whereas baby bonds are traded via ticker symbols.

-

Traditional bonds may or may not have call dates, whereas baby bonds are almost all callable prior to their maturity date (convertible baby bonds usually are not callable early, however those are rare).

-

Traditional bonds pro-rate the interest payment based on the purchase date. Baby bonds do not prorate, as the owner of the baby bond on the record date gets the whole interest payment, even if they purchased it just a few days ago.

-

Traditional bonds generally pay interest semi-annually and baby bonds usually pay interest quarterly.

-

Baby bond issuances are often not large, often having a face value of less than $100 million. Traditional bonds tended to be much larger issuances, but this isn’t a hard and fast rule.

-

In my experience, most traditional bonds have credit ratings from Moody’s and/or S&P, while most baby bonds are not rated.

Traditional bonds are available in various sizes, or “face value”, most frequently at $1,000. Bond brokers will express the trading “price” as a percentage of the face value. So when a $1,000 bond is quoted at 78.35 (78.35% of $1,000), then the price that you will pay is $783.50. When you see that the bid/ask on a bond is $92/$94, that means that someone is bidding $920 for the bond, while someone is looking to sell the bond at $940.

Researching Bonds

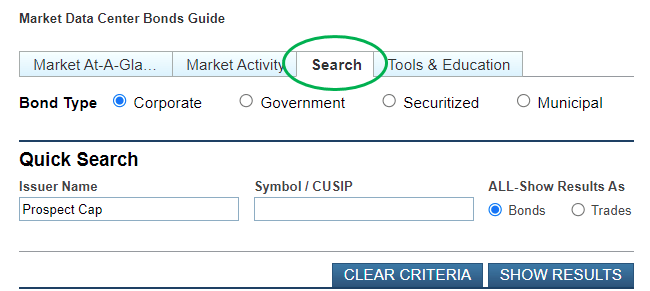

The best place for finding the CUSIP of a bond, and other information about a bond, is at FINRA (Financial Industry Regulatory Authority). When you follow this link , you then click on “Search” and this is what you see.

{kind=link}

FINRA

You can then search by company name or by CUSIP number. In the above example, I used the issuer name (Prospect Capital) and then clicked on “Show Results” and here is what came up.

{kind=link}

FINRA

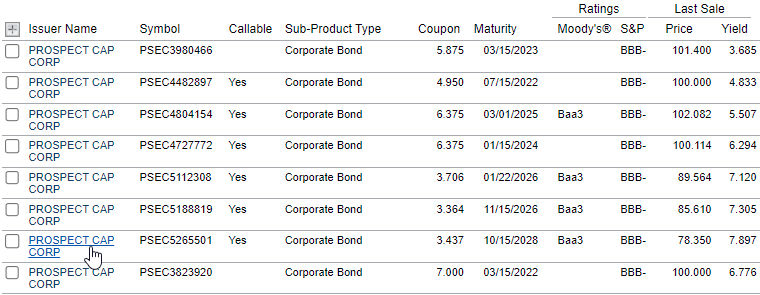

It gives you a nice summary of each bond issued – maturity date, coupon rate, credit ratings, price, and yield. Then you can click on the bond that interests you most, and this is the detail page that opens:

{kind=link}

FINRA

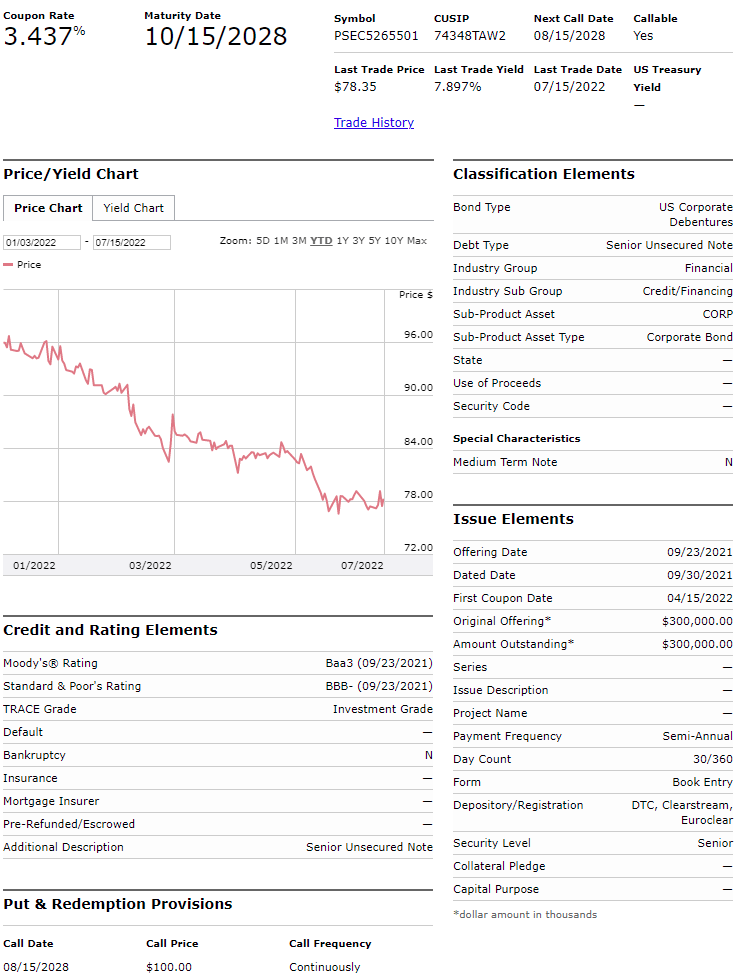

If you peruse the top of the display, you can see that the CUSIP number is provided, as well as the call date, the last price, the yield, and a historical price chart. A link to the trading history is also available. Underneath the price chart, you can see the Moody’s and S&P ratings, and further down you can see that this bond is callable on 8/15/2028 at $100.00 ($1,000.00).

Once you know a bond’s CUSIP, you can create a Watchlist at FINRA. A very useful summary about a bond is available by entering the CUSIP at Bond Facts by FINRA

Interest Payments

In terms of how the interest payments work, as stated above, they are pro-rated and traditional bonds generally pay interest semi-annually. If the payout dates for a bond are June 30th and December 30th, and you purchased this bond on September 30th, 3 months after its last payment date, you would not only pay for the bond but also pay the seller 3 months of interest. So if the bond has an 8% coupon, and thus pays $80 per year in interest, you would pay the seller $20 per bond for the 3 months of accrued interest. But 3 months later you will get compensated by receiving 6 months ($40) worth of interest for holding the bond only 3 months. And when you sell, you will be paid by the buyer for the amount of interest accrued since the last payout date.

Buying Bonds

The one variable with traditional bonds is how to place buy and sell orders, but all brokers should know which bond you are referring to by the CUSIP number. Each broker may have a different method for placing orders and some brokers may also require a minimum number of bonds be purchased in order to place an order. Some may require that you place the order over the phone while some may accept online orders that have little flexibility. Your broker may give you a price and you either accept it or reject it. They might not allow for limit orders that can stay in effect until canceled.

Quotes on bonds will vary among brokers, depending on which bonds they have in their inventory or have access to. Compare quotes if you have multiple brokerage accounts. A “depth of book” listing for a bond will show the various bid/ask prices and quantities.

Your trade confirmation might be confusing, at first look. A purchase of ten $1,000 bonds, for example, may read as 10,000 @ 78.35, meaning that you paid 78.45% of 10,000 total face value = $7,835. The settlement will also include the accrued interest that is paid to the seller. It is not unusual for brokers to also include a commission fee or markup of $1 or $2 per bond in the transaction.

There may be other brokers that have very good online trading platforms, but I am most familiar with Interactive Brokers. Their bond trading platform is superb. You can set up a screen of bonds that you follow and see in real-time the current bid/offer prices of each. And you place your orders very easily online. They accept limit orders, day orders, and good-till-canceled orders. It is just like trading a stock. In fact, you don’t even need to know the CUSIP number, as you can simply type in the name or ticker symbol of the company that issued the bond and it will bring up all bonds issued by that company, and you can add whichever of those bonds you want to your trading screen and follow them regularly like you would a stock.

I own no stock in Interactive Brokers, so I have no financial incentive to say this, but if you think you will be buying traditional bonds, I do recommend an account at Interactive Brokers. Additionally, for most bonds they do not have a minimum purchase requirement, so if all you want to buy is two bonds, you can do that.

Prospect Capital Bond Due 8/15/2028

CUSIP 74348TAW2

I have noticed that the bonds trading in the bond market are now more attractive than baby bonds. In the past, baby bonds generally provided higher yields than equivalent traditional bonds, but for some reason this bear market has changed that.

In the past, there were a large number of baby bonds from BDCs (Business Development Companies). These were excellent bonds because BDCs are restricted in how much leverage they can take, and thus no BDC bond has ever defaulted. But most BDC baby bonds have been called in recent years making it much more difficult to find high-yielding and safe baby bonds.

But there are a lot of traditional bonds that trade by CUSIP that look like good values. One stands out to us, not just because of its high yield relative to equivalently rated bonds, but also because it is liquid with a narrow spread between the bid and offer price. This bond is from Prospect Capital ( PSEC ).

As can be seen in our examples above, this PSEC bond (CUSIP 74348TAW2) has a coupon of 3.437% but trades well below the $100 par value at around $77.60. Amazingly, this bond came out just 10 months ago with a YTM (yield-to-maturity) of 3.437% but now can be purchased with a YTM of 8%. This shows you just how much damage has been done in the fixed-income market in a short period of time.

PSEC is a BDC with an investment-grade credit rating from Moody's (Baa3) and S&P (BBB-), so this current 8% YTM looks very attractive, especially for a bond that matures in only 6 years. Because it is a BDC, PSEC must keep leverage below 67% (liabilities cannot exceed 67% of assets). This makes PSEC bonds quite safe. And better yet, PSEC’s leverage is currently at a mere 36% in terms of its bonds. No doubt, this is a primary reason that PSEC bonds are considered investment grade. And as I stated above, no BDC bond has ever defaulted.

Another interesting thing about PSEC is that they have issued hundreds of small bonds. Whereas most companies might have issued 2 or 3 large bonds, and face large refinancing risk when they come due, PSEC only has small bonds coming due that they have to deal with. They have basically laddered their bonds with huge numbers of maturity dates going out many years. This provides extra safety that I don’t see in any other company that I follow. Refinancing risk is one of the larger risks for companies that have issued bonds, and PSEC has done a great job of mitigating that risk.

When I look at the few BDC baby bonds that still exist, this PSEC bond just looks like a very good value. For example, Saratoga (SAR) has a baby bond ( SAT ) that matures in 2027 with a YTM that is only 6.8%. Another BDC baby bond is OFS Capital ( OFSSH ) which matures in the same year as this PSEC bond, so it makes for a great comparison. Its YTM is only 6.2% versus PSEC’s 8%. And both SAT and OFSSH are unrated versus the investment-grade rating that PSEC carries.

{kind=link}

Interactive Brokers

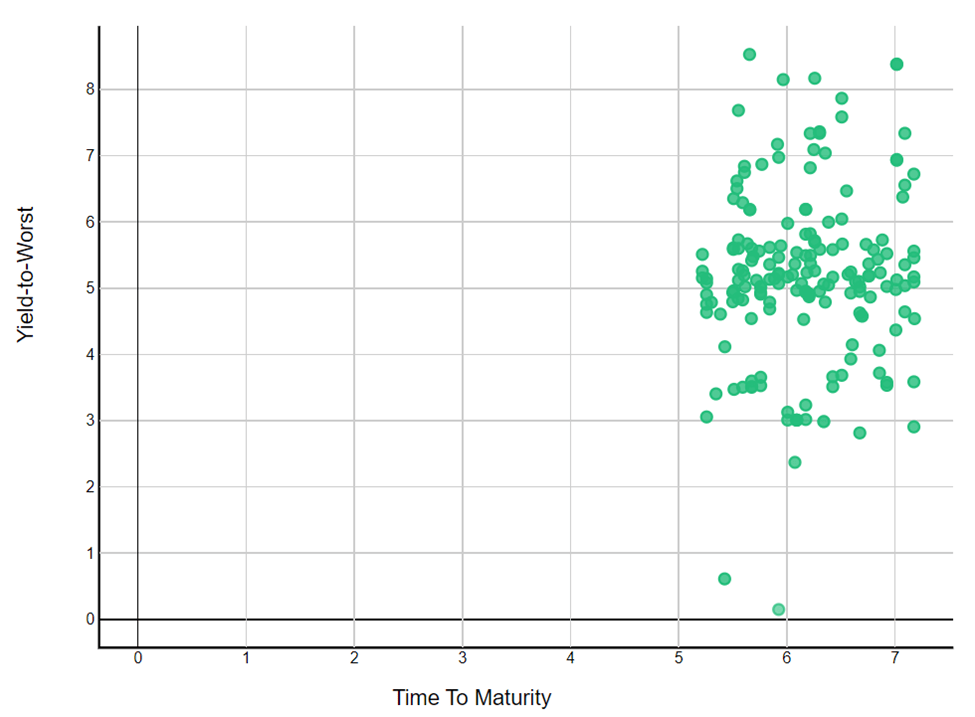

Above is a scatter plot of the yields of all bonds that have the same Baa3 Moody’s rating as our PSEC bond. As can be seen, the average yield-to-worst is around 5.6% on a Baa3 bond with around 6 to 7 years until maturity. So the 8% YTM on the PSEC bond, CUSIP 74348TAW2, is extremely good relative to its Baa3-rated peers.

Summary/Conclusion

Given the wreckage in fixed-income of late, the traditional bond market is now offering some great values. Whereas we used to concentrate on baby bonds, there just are not a lot of high-quality baby bonds with high yields to choose from. Thus, we are now focusing on finding strong values in the traditional bond market.

The PSEC bond that we highlighted (CUSIP 74348TAW2) is one very good example. Its 8% YTM is better than any safe BDC baby bond and much better than other traditional bonds with the same credit rating.

We consider this PSEC bond safe because:

- No BDC bond has ever defaulted.

- PSEC is restricted in how much leverage it can take on.

- PSEC operates at an extremely low leverage of 36%.

- PSEC issues a huge number of smaller bonds, greatly reducing refinancing risk on their bonds.

- PSEC has an investment-grade credit rating from both Moody's and S&P.

For further details see:

Opportunity: Investment Grade Bond, +8% Yield From Prospect Capital