OPCH - Option Care Health Inc.: Terminated Merger Leaves Some Potential Still

2023-08-04 19:10:20 ET

Summary

- Option Care Health Inc received a $106 million termination fee after the agreement to merge with Amedisys Inc was terminated.

- Despite the termination, Option Care Health has shown strong financial growth and consistent revenue growth.

- The company's valuation is currently high, making it a hold until the valuation becomes more reasonable.

Investment Outline

Earlier in 2023 there was the proposal that Option Care Health Inc ( OPCH ) and Amedisys Inc (AMED). This agreement was quite recently terminated and OPCH received $106 million as a termination fee which is bolstering the financial state of the business somewhat. Looking at OPCH by itself and not from what it could have been with AMED I think it still has some potential. The company is trading at a valuation above the sector and this is keeping me from rating it a buy right now. But I think investors who stick with their investment and don’t sell will see decent returns over the long term.

OPCH operates in the healthcare services industry where it has made a strong name for itself and grown the valuation to over $6 billion. In the industry, it provides home and alternate site infusion services in the United States. The company has been growing steadily and despite the Covid-19 pandemic it hasn't slipped up and reported anything but a revenue YoY growth since at least 2018. This is showcasing very well the steps that OPCH has taken to grow investor sentiment and grow its capital allocation program. To reiterate my stance on OPCH right now, I see them as a hold until the valuation comes down to more reasonable levels.

Recent Developments

Significant news that came out recently was the termination of the agreement to merge or combine with AMED. The termination left OPCH with an additional $106 million which will have helped grow the cash position by nearly 20%. This deal was supposed to offer investors a decent arbitrage play with a premium of around 7 - 9%.

But even without the deal, I think that OPCH has a lot to offer still seeing as the last report showcased strong FCF growth and EBITDA growth too. The deal would have put two very competent companies together, but without it, OPCH still has potential as a growth opportunity, when the price is right that is.

The CEP of John C. Rademacher of OPCH was disappointed in the outcome of the deal but also followed up and made some reassuring comments about the future of the business.

-

“ We remain confident in our growth trajectory, which is underpinned by current industry trends and market forces as well as our strong financial position. Our team is committed to serving all our stakeholders by providing unsurpassed care and superior clinical outcomes in the home or ambulatory setting, and we will continue to identify ways to increase the value we can deliver ”.

Going forward I don’t think this news will have an impact on the performance the Q2 report posted recently showcased the strength of the business. Net revenues grew by 9% YoY to over $1 billion in total. Margins also expanded and the gross margins reached 23.5%. This is especially great to see as it's above the TTM average for the business. This highlights that OPCH is heading in the right direction for margins. Moving over to the FCF for the quarter it landed at $169 million and this is an impressive improvement from the prior year's result of $104 million. Concluding my opinions on the quarter I think that OPCH made great progress and is set up very well to benefit from industry trends and growing demand.

Margins

Margin Profile (Seeking Alpha)

As mentioned earlier OPCH has made some solid progress in terms of growing its margins the last quarter showcased the fact they are generating gross margins above their 5-year average of 22.28%. This is supporting the long-term outlook for the business as doing this in a high-interest environment is impressive. Looking at the FCF margins of OPCH we have another highlight. The 5.4% FCF is solid and I think this has helped OPCH in significantly reducing the need to dilute shares to raise capital YoY the shares outstanding barely increased by 0.3%.

Valuation

DCF Model (My Own Model)

Looking at the DCF model above here it highlights the fact that OPCH is trading at a pretty rich valuation in comparison to its intrinsic value. I think we are best to be rating OPCH a hold now as paying a premium like this and also not getting a dividend doesn't seem like the best possible scenario in my view. The model assumes that FCF will be growing by a terminal 10% and with an 8% discount rate we are covering some of our basis and getting a good margin of safety. The cash flows are strong and I think a higher margin might be possible in the future, but for now, the share price doesn't offer enough of an immediate upside potential to make it a buy.

Comparing the current valuation of OPCH to the sector it does look expensive on some remarks, like the EV/EBITDA where it has a multiple of 16, or 18% higher than the sector. But with the predictions for 2023, the p/e would be at 25 which is a quite big premium to the sector of around 25%. I would have preferred getting a better discount at OPCH if I were to make it a buy here honestly. Given that OPCH hasn't had a long enough track record of profitability we cant measure it to historical standards, but we can see that it's trading around 18% above its EV/sales average over the last 5 years. This further highlights that maybe OPCH isn't in such a good investment place right now.

Financials Of OPCH

Viewing the financials of OPCH I can see some decent improvements.

{kind=link}

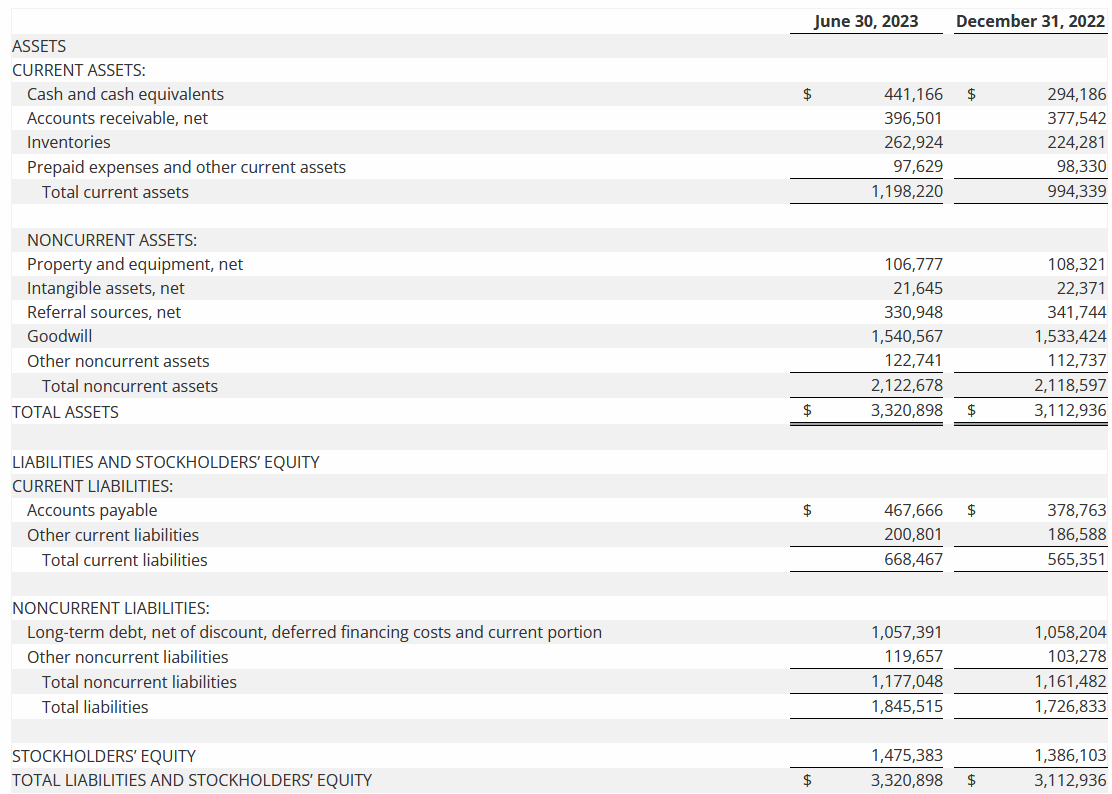

The balance sheet looks healthy as the cash position continues to grow and makes OPCH sit in a far better position to make investments right now without the worry of significant amounts of debt. Speaking of debt, it hasn't changed much on this front and still sits at just over $1 billion. The cash position could cover over 40% of it which I dont think will be necessary as the maturity is further out. By that point, OPCH will have also been able to grow margins and FCF too.

Comparing the assets to the liabilities as well we can see that it has a ratio of 1.79 which is very healthy, indicating that OPCH has a solid asset base it can tap into to cover any necessary liabilities in the future.

Risks

A pivotal aspect to consider is the potential for heightened competition within the industry. Although Option Care Health occupies a niche market, it's essential to recognize that other companies also provide similar services. The escalation of competition could introduce challenges such as pricing pressure or even a potential erosion of market share for Option Care Health.

Furthermore, the threat of losing market share is a significant concern. If competitors manage to offer comparable services at more attractive terms, Option Care Health could face the risk of customers switching to alternative providers. This can impact the company's revenue stream and hinder its growth prospects.

Looking at more imminent risks that are facing OPCH right now I think the valuation is the primary one sitting at a p/e of over 25. This is significantly higher than the industry and I don’t think the growth we have seen is necessarily enough to justify it. All it takes is one tough quarter or an increase in interest rates to send the share price down to where the rest of the sector is trading at.

Investor Takeaway

OPCH has been in the healthcare services industry for quite some time and gained a solid reputation. The company focuses on providing anti-infective therapies and home infusion services. This has led to consistent YoY revenue growth and I don’t see them slowing down. But the fact of the matter is that the share price is quite high at a p/e of 25 and this doesn't present enough of a beneficial risk/reward profile for an investment. This leads me to instead rate OPCH as a hold until better entry points are revealed.

For further details see:

Option Care Health Inc.: Terminated Merger Leaves Some Potential Still