ORAN - Orange: Growth Rate Questionable

2023-12-19 00:00:06 ET

Summary

- Orange S.A. is a leading telecommunications company that offers a wide range of digital services and networking solutions.

- The company has a solid dividend yield and price growth, making it an attractive investment for existing shareholders.

- ORAN is lagging behind the industry in terms of growth and faces challenges in key areas such as wholesale and enterprise. Investors should approach with caution.

Orange S.A. ( ORAN ), a leading telecommunications company, operates with a business model that integrates digital services and networking. Their unique expertise as both a network operator and digital services integrator allows them to offer their customers a wide range of skills. Orange also designs innovative, secure mobile financial services through Orange Money and Orange Bank, tailored to meet people's needs in each of their markets.

Orange is a solid player in the telecom space with a 6%+ dividend yield and 16% price growth across the past year.

{kind=link}

I have no doubt that Orange will continue to cash flow and continue to pay a strong dividend and investors who previously entered the stock will be well rewarded. However, I am concerned about price appreciation for investors entering the stock today.

From a growth standpoint, Orange is doing just okay and is lagging the industry in key areas. With a large cost base, the business is highly sensitive to revenue growth rate. My DCF-generated price target of $13 doesn't provide a sufficient premium to enter today, given the state of the bond market. With that in mind, I rate Orange a hold pending improvement in long-term growth prospects.

Orange Is Lagging The Industry In Growth

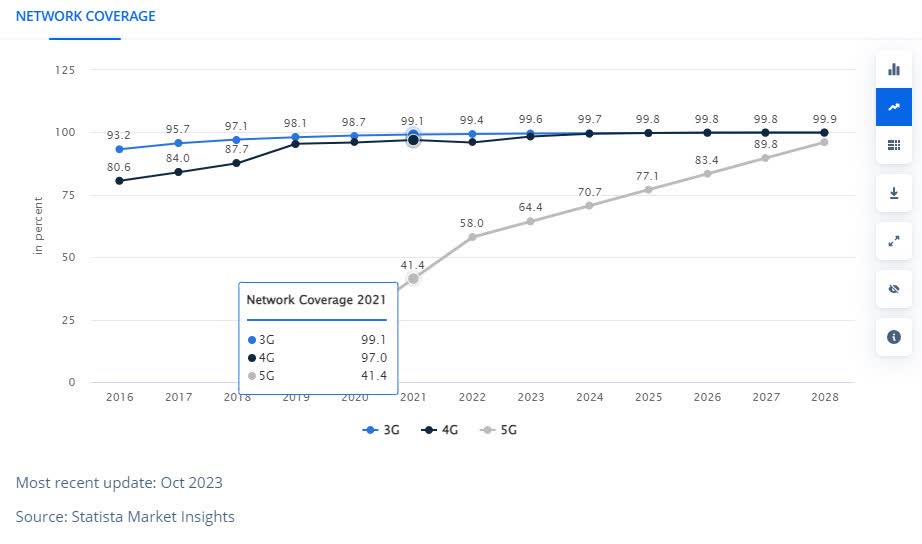

It almost goes without saying that telecom in Europe, much like North America, is a mature industry. In 2023, 99% of Europe has 3G, 97% has 4G and 41% has 5G. By 2028, 5G is expected to cover 96% of the population.

{kind=link}

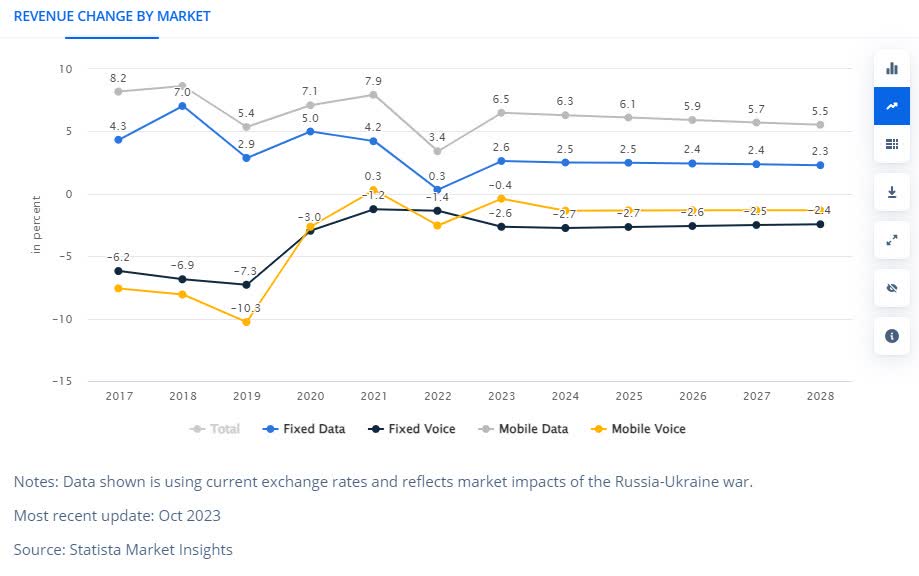

In mature regions, I look for telecoms to be at or above market growth rate in key businesses to ensure the business is executing well and can continue covering costs. Here are the expected overall growth rates based on the most recent European telecom analysis from Statista:

{kind=link}

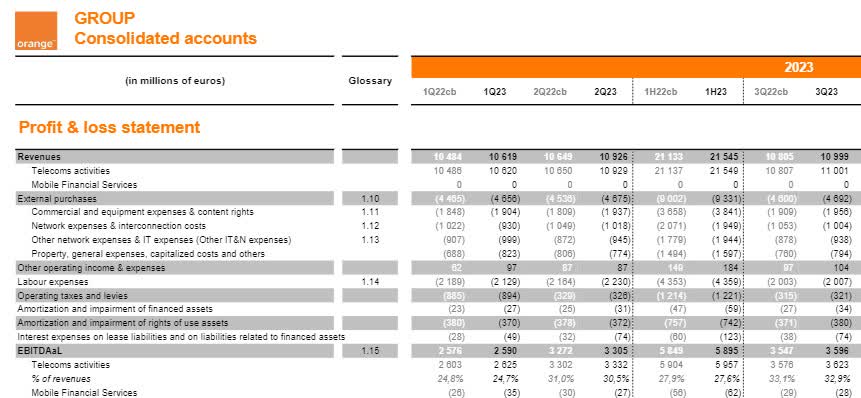

It is also important to note, per the same analysis , that the overall growth rate from 2023 - 2028 is expected to be 2.65%. Unfortunately, Orange doesn't stack up to the industry. Overall revenue growth was 1.8% (1.9% for year-to-date)

Orange Q3 Summary (Orange Investor Relations)

Using France as an example, no individual service kept up with overall growth rates.

France financials (Orange Investor Relations)

Even more concerning, the high-margin Wholesale business was down 6.7% in Q3 and struggled in nearly every region.

A lot of telecoms, such as competitor Vodafone , have been leaning heavily into the enterprise space to drive growth. Unfortunately Orange had a mixed quarter in enterprise as well.

Enterprise financials (Orange Investor Relations)

The business is by no means falling off a cliff, but I am concerned that growth expectations are higher than what Orange can deliver.

Revenue Growth Falling Behind Costs

As shown in the financial summary above, revenue in Q3 grew by 1.8% outpacing EBITDA growth of 1.4%. Orange has a significant cost base to consider.

{kind=link}

Here are the average inflation rates impacting Orange:

- Labour is up 4.5%

- Core Inflation is up 3.4%

Management did go into detail in the earnings release on an efficiency plan.

{kind=link}

However, there is only so much to cut when cost growth from inflation outpaces revenue growth by 1-2ppt. Given the state of revenue growth, especially in high-margin businesses like wholesale, I am concerned about the margin deteriorating over the next few years.

Stock Price Fairly Valued Given Growth

I ran a simplified discounted cash flow analysis with the following assumptions:

- Management guidance is achieved for 2023

- Revenue growth at 2% based on current trend

- Expense growth at 3% based on current trend

- 9% discount rate based on low risk premium for an established, large-scale telecom

- 2% long-run growth rate based on current trends and market expectations

I generated a price target of $13 or 16% upside from today's pricing.

ORAN DCF (Data: SA; Analysis: Mike Dion)

Wall Street analysts get a slightly higher price target at $14.59 and recommend a strong buy. Also worth noting that the quant rating is giving a strong buy as well.

{kind=link}

Here is why I am not recommending a buy, despite the concurrence of the three ratings above.

- DCF analysis in this case is highly sensitive to revenue growth rate. 10 basis points on the growth rate is +/- $0.50 on the stock price. I used a 2% growth rate based on the overall trend, but the Q3 growth rate of 1.8% drops the price target to $12.

- Growth is challenged in the overall European telecom market and there is only so much growth that can be priced in for any one company.

- Orange needs to stabilize declines in areas like wholesale for a few quarters.

Upside Potential And Downside Risk

On the upside, Orange could exceed industry growth targets through its "disciplined value" strategy in addition to stabilizing cost growth. Alternatively, Orange could drive additional value from businesses like Enterprise or financial services to offset core challenges.

On the downside, costs could grow faster than expected if inflation does not continue to mitigate. In addition, businesses like wholesale or fixed access could decline faster than expected, or retail growth could slow down.

Overall, I feel that the upside and downside are well balanced, especially given the inertia of such a large company.

Verdict

In conclusion, while my DCF shows a price target of $13, a potential upside of 16% from today's pricing, and finds strong buy recommendations from both Wall Street analysts and quantitative ratings, it's crucial to approach this with caution. The company's valuation is highly sensitive to revenue growth rate adjustments - a reduction of the projected growth rate from 2% to 1.8% results in a price target drop to $12. Furthermore, the European telecom market poses growth challenges, and Orange is grappling with the need to halt declines in sectors such as wholesale.

Potential growth avenues for Orange include exceeding industry growth targets via its "disciplined value" strategy and deriving additional value from sectors like Enterprise or financial services. However, the risks include a potential increase in costs if inflation does not persist in mitigating them or a faster-than-expected decline in businesses like wholesale or fixed access. Given these factors, I rate Orange a hold with a well-balanced upside and downside from the inertia of such a large company like Orange.

For further details see:

Orange: Growth Rate Questionable