FNCTF - Orange: Normalizing CapEx To Finally Spur Dividend Growth

2023-07-14 15:27:06 ET

Summary

- Despite not raising the dividend as I had expected, Orange has nonetheless done well since my initial piece on the stock back in 2021.

- Performance in France has been a little soft on account of declining Wholesale revenues, and that will continue, albeit with a diminishing effect over time.

- Africa & Middle East performance continues to be strong, and with comparatively high EBITDA margins and growth prospects, this remains a bright spot for the company.

- CapEx is now materially declining following the rollout of full fiber in France, and along with modest EBITDA growth this will finally support a growing dividend.

French telecom giant Orange S.A. ( ORAN ) has largely performed as I imagined when I first covered the company two-and-a-half years ago, if not for the exact reasons I envisioned. These shares have returned around 27-28% in that time in local currency terms, mapping to the circa 10% annualized rate I was looking for, but those returns have been a bit less dividend-led than expected. Indeed, at €0.70 per share, the annual payout remains where it was back then. Note that dollar-denominated ADR performance has been slightly weaker on account of USD/EUR currency movements:

While dividend growth has fell short of even my modest low single-digit expectations, the main drivers identified back then remain in place. Chief among them is the normalizing level of CapEx, which will boost free cash flow and result in modest dividend growth in the coming years. With the dividend yield still a fairly substantial 6.7% and with growth finally set to come from FY23 onwards, these shares still offer at least high single-digit annualized returns potential. Buy.

France A Little Soft, Offset By Growth In Africa & Middle East

Orange's composite French business and its principally mobile operations in Africa & the Middle East are the most important aspects of its business. In terms of the former, France accounts for a little over 40% of group revenue, but the region's comparatively high EBITDAaL (EBITDA after leases) margin (37% in FY22) lift's its share of group EBITDAaL to over 50%. In terms of Orange's African & Middle Eastern operations, on a revenue basis these are cumulatively still smaller than its combined non-French European operations in Spain, Poland & the CEE area (€6.9B vs €11.0B in FY22), but with much higher organic growth prospects and EBITDAaL margins (37.3% in FY22 vs 25.3% for the combined non-French European operations).

With that, the domestic French business has been a little soft in the period since my first piece. Q1 FY23 French revenue of €4.307B was around 2.25% lower than at prior coverage in Q1 FY21 (€4.404B), and that has been driven by declines in the Wholesale business as legacy copper lines are retired. French Wholesale revenues have thus fallen from €1.286B (Q1 FY21) to €1.1B (Q1 FY23) in that time.

Data Source: Orange Quarterly Results

{kind=link}

This decline is structural in nature, and so I do see it continuing out over the medium term, however it will be offset to some extent by low growth in the Retail line. Furthermore, as Wholesale's revenue continues to fall, its share of the top line will likewise carry on dwindling, having already fallen from over 29% (Q1 FY21) to 25% (Q1 FY23). As a result, its effect on revenue will gradually fade too. Note that French EBITAaL has been supported by cost cuts, leading to flatter performance in spite of revenue declines.

Orange's African & Middle Eastern operations have continued to grow strongly. Q1 FY23 revenue attributable to this division was €1.7B, up almost 10% YoY and 15% higher than Q1 FY21. Organic growth prospects remain strong here, driven by both demographics (mobile customers increased from 130.9m to 143.9m over the same period) and economic growth (more demand for mobile data; 4G customers increased from 36.1m to 54m over that two-year period). Furthermore, this growth is also relatively high quality given that EBITDAaL margins land in the high-30s region as per above.

Data Source: Orange Quarterly Results

{kind=link}

The above dynamics also mean that EBITDAaL growth should outpace revenue growth for the group as a whole. With flat-ish annual revenues in France and mid-to-high single-digit growth in Africa & Middle East, group sales should grow at around 1-1.5% or so per annum, which in turn would support around 2.5% per annum EBITDAaL growth.

CapEx Normalization Means A Return To Dividend Growth

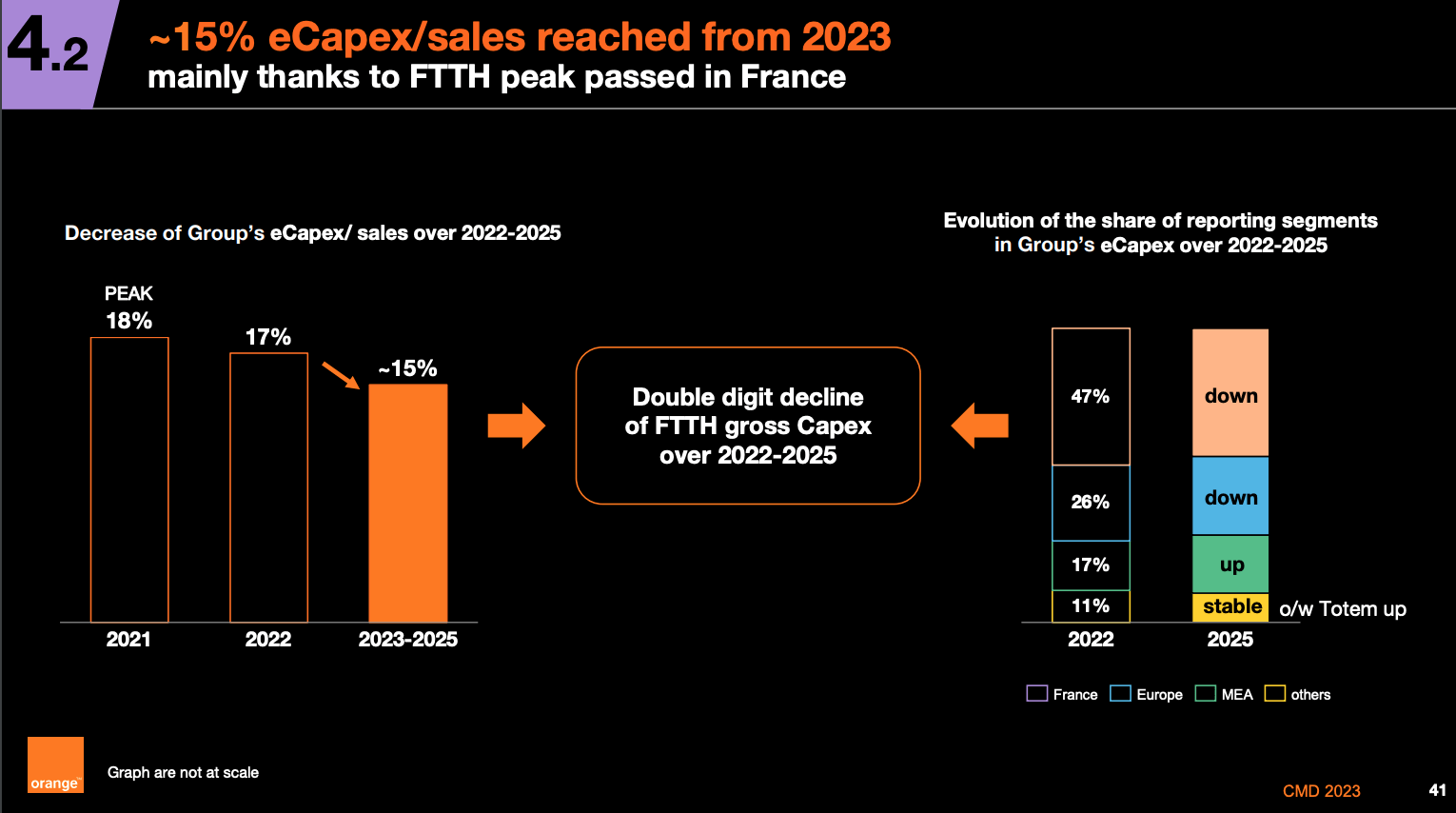

The biggest catalyst for near-term dividend growth is a return to more normal levels of capital expenditure. At initial coverage, economic CapEx (i.e., excluding telecommunications licenses) had risen to 18% of sales as the firm was expanding full fiber access across France. Free cash flow was barely enough to cover the existing dividend after including spending on telecommunications licenses.

2021 represented the cycle peak for CapEx, both in absolute terms and as a portion of revenue. CapEx fell last year, and Management further expects a "strong decrease" in CapEx this year. Guidance of a circa 15% CapEx/sales ratio implies around €6.7-€6.8B in FY23 CapEx, equivalent to a roughly €500m YoY decrease and €900m lower than the FY21 peak. That ~15% ratio is then seen steady over the next couple of years.

Source: Capital Market Day 2023 Presentation

{kind=link}

With that, management is guiding for at least €3.5B in free cash flow this year. That more than covers the current level of dividend spending (€1.9B) with enough cash left over for telecommunications licenses (a circa €1B annual expense over the 2020-2022 period). That is why management have already guided for a 2.85% dividend hike in respect of FY23 (from €0.70 to €0.72). EBITDAaL growth of 2.5% should then be good for a commensurate level of annual dividend hikes.

With the current dividend yield still at 6.8%, 2.5% per annum growth should enough to drive 9%-plus annualized returns, which I consider acceptable given the defensive nature of Orange's operations. Buy.

For further details see:

Orange: Normalizing CapEx To Finally Spur Dividend Growth