OSUR - OraSure: Revising To Buy Following Extensive Growth Route

Summary

- OraSure has robust growth throughout the P&L, cash flows and balance sheet.

- Core business exhibiting remarkable upsides without Covid-19 revenues.

- Valuations supportive with 25x forward P/E implying $10 target.

- Net-net, re-rate to buy.

Investment summary

Shares of OraSure Technologies, Inc. (OSUR) have become increasingly attractive on a number of fronts leading into the new year. Following the company's Q4 FY22' numbers I believe there is enough margin of safety and growth potential yet to be priced in in order to warrant an upgrade to my previous hold rating. In the last publication back in November titled " Concentration Risk From Covid Revenue " it was noted the continued reliance on Covid-19 revenue to drive top-line growth, with negligent divisional growth when excluding this from the picture. Turning to the present day, management has engaged liquidity preservation measures and embarked on a restructuring route to potentially amount to $15mm p.a. in cost savings. Management now guides to a forward run-rate of $130mm in Q1 FY23' at the upper bound, calling for 92% YoY growth at the top line. To the point on reliance on Covid-revenues, we've observed that OSUR has managed to plow all of its Covid-related earnings back into the business, reinvesting at tremendously high rates of return to fund its future growth initiatives, leading to a strong economic profit and incremental return on invested capital ("ROIC").

Putting it all together, I feel there's enough fundamental momentum building across its core portfolio in order to re-rate the stock to a buy. Here, I'm searching for an initial target above $10 based on supportive valuations and a 4% forward earnings yield. Check out my last 3 publications on OSUR here:

- OraSure: Revenue Mix Continues To Present Risk .

- OraSure: Not So Sure With Softening Fundamentals, Fairly Priced At $2.54 .

- OraSure: Well Positioned Ex-Covid, Sell Side Missing The Organic Growth Drivers .

OSUR Q4 numbers - unpacking the growth drivers

The first major inflection point that needs discussing is the company's restructuring plans to drive growth in the coming periods. It recently began to restructure its portfolio to increase liquidity preservation and drive profitability in its core businesses. To begin with, 2 business units were consolidated into a single entity [named OraSure]. This tied with an 11% reduction in the company's non-production workforce. Investors typically like headcount reductions in my experience given the greater focus on efficiencies and profits, and this was reflected in the market's price response since last week with the stock up >24% at the time of writing. I'd note the more linear cost structure could potentially drive more revenue synergies and potentially feed more income down the P&L. Honing in on ORUR's manufacturing, R&D and operational performance, this could also reflect a more efficient allocation of capital into high-growth investment opportunities to drive operating leverage down the line. As mentioned earlier, the restructuring is expected to generate ~$15mm in annualized OpEx savings when fully implemented at the end of Q1 this year.

It's also worth noting that OSUR has set its sights on expanding its respiratory assay portfolio. This follows a reasonable period of growth with its Covid-19 lateral flow testing. Though specific details remain undisclosed, my opinion is that OSUR looks set on augmenting the commercial expansion of its respiratory portfolio. For evidence on this, look at the latest InteliSwab developments in Q4 - overwhelmingly positive by estimation. Notably, it secured 2 new contracts from the U.S. Government. The first, estimated to be around 18mm tests of InteliSwab for Covid-19, includes a maximum award of 36mm tests, and a guaranteed minimum award of 3.6mm tests, running from November 2022 through to November 2023. Notably, these awards are concurrent with the existing government contract supporting the school testing program, and the company has already shipped approximately 46mm tests as of the end of Q4 under these agreements. Specifically, the procurement came from the U.S. Defence Logistics Agency ("DLA").

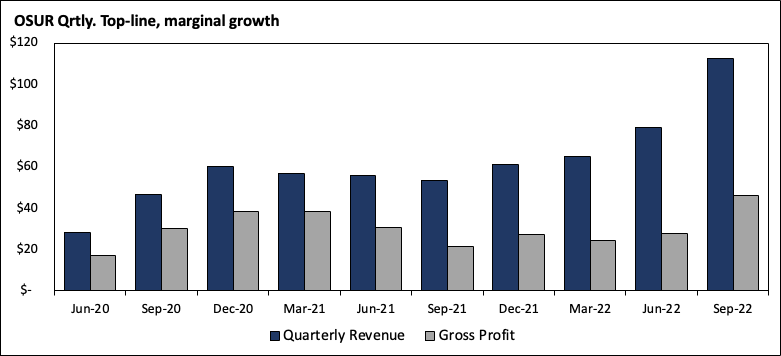

Fig. (1)

Data: Author, using data from OSUR SEC Filings

{kind=link}

Turning now to the quarterly numbers, and my observations are broken down into performance across the company's core business divisions. In no particular order:

- OSUR achieved a record for its top-line revenue at $123.1mm, representing a YoY growth of 94%. The diagnostics business unit delivered $107.3mm in revenue, expanding 228% YoY, with InteliSwab leading the way as expected. Excluding this, the core diagnostics business was up 3% in the quarter, but it's also worth pointing out that growth was negatively impacted by the timing of various international orders.

- The molecular solutions business incurred a 49% YoY decline to $15.8mm. Again, backing out Covid-19 revenue, the business declined 32%. As was expected in my prior observations, the pullback stemmed from the work down of excessive inventory numbers within some of their large consumer-oriented accounts, notwithstanding the cycling against a significant research study the company purchased in FY21. Despite the expected volatility, the company remains optimistic about its genetic testing growth, which it will have to achieve through establishing partnerships in my estimation

- Looking at the Q4 adj. gross margin, it pulled to 40.7%, showing meaningful positive progress on a sequential basis. Although, the sizeable shift in revenue mix towards the diagnostic business unit mentioned above continues to create some margin headwind here. The company plans to boost its gross margin off the top by transitioning to a new packaging configuration for InteliSwab toward the back end of Q1 this year. Management said it expects to save ~$0.40 per test following these moves. However, it's also worth noting that, due to lower pricing under new requests for proposal ("RFPs") is expected to create some pricing headwinds through the first quarter, which could improve towards the back end of the year. This could also ramp up given the focus on manufacturing and cost efficiencies listed earlier. Moreover, adj. OpEx in the quarter came to $31.8mm, an overall decrease of $3.5mm. Reiterating what was mentioned above, the company expects to achieve $15mm in savings to annualized expenditures, and I'd also add that the tapering of its InteliSwab test costings could improve operating margin further.

- Looking at its liquidity and delta in cash flows, OSUR left the quarter with on-balance sheet cash of $111mm, after accumulating ~$9mm last quarter. Important points to note here:

- Management project to generate positive cash flow from the company's $109mm DOD contract to build out its InteliSwab capacity.

- The majority of the cash allocated to this has now been put to work, and it is now set to be cash flow as it surpasses contract milestones going forward.

- Excluding InteliSwab revenue , the company targets to be cash flow breakeven in the base business, by the end of FY24. I would go as far to estimate management will re-route the OpEx savings listed earlier into selective investments to garner ongoing returns on capital.

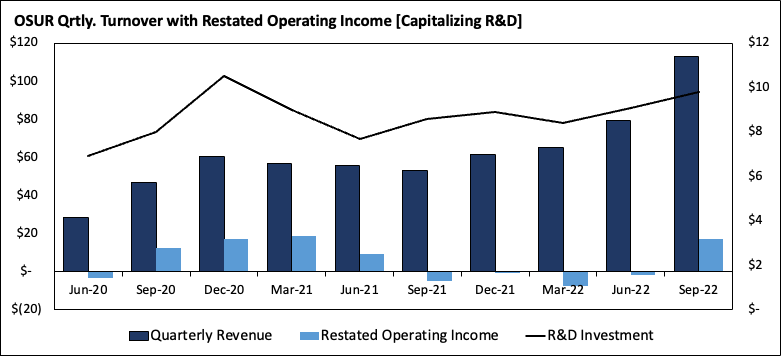

Finally, I mentioned in the introduction that OSUR has managed to plow earnings from its Covid-base back into growing the business. To exemplify this, I've made reconciliations to its GAAP reported numbers to accurately show where the company has invested its money and what its tax-adjusted operating income looks like on an annual basis from FY20-'22. This more accurately states the operating performance of the company, per Mauboussin ( April 2022 and July 2022 ). To do this, we capitalize R&D as an intangible investment onto the balance sheet, restate operating income [excluding R&D investment], and amortize the new R&D figure at 10% per year.

Fig. (2)

Data: Author, using data from OSUR SEC Filings

{kind=link}

You will see that the company accumulated $62.7mm in NOPAT, on an additional growth of $16.7mm. However, it only needed to invest a net $8.4mm to achieve this growth rate, therefore reinvesting 13.4% of NOPAT at a 198% incremental ROIC over the 2-years to FY22. The annual ROIC has also crept up from 4.3% to 8.4% in FY22, exhibiting this momentum. Alas, the company grew at a rate of 26.6% per year over this time. These numbers are evidenced clearly throughout the growth percentages shown in its financial statements.

Fig. (3)

Data: Author, using data from OSUR SEC Filings

Risks to thesis

There are several risks that must be noted to the buy thesis. First the risks around its Covid-19 segment, in that if these pare back substantially this could hurt top-line growth and therefore impact the buy thesis. Not only that, the company faces obvious competition from a number of large names in same industry, and we've seen this in the less benign pricing environment that have lowered its RFPs as mentioned earlier. If the pricing environment for procurement becomes more competitive, this could make it difficult for OSUR to secure contractual revenues. There's also the obvious market risks with the stock being a small-cap name that is susceptible to volatility, and technicals can become wildly disconnected from the fundamental thesis presented here. It is essential for investors to recognize these risks in full before making any investment decisions.

Valuation and conclusion

Trading at 25x forward P/E I'd suggest OSUR is still attractively priced given it also attracts a 1.2x P/Book value multiple as well, and trades at just 10x forward EBITDA. The latter two multiples are discounted versus the industry and with the high forward P/E we're looking at a 4% forward earnings yield - not far off the S&P 500's 4.8% forward earnings yield. Further, looking to the forward earnings multiple this is a market implied $0.64 EPS and assigning the 25x P/E to this derives a price target of $10.32, another 63% upside on today's market value. Subsequently I rate OSUR a buy, in-line with the quant rating system.

Fig. (4)

Data: Seeking Alpha, OSUR, see: "Ratings"

Net-net, there's now sufficient evidence to suggest OSUR is a buy, having overcome the main tension points raised in my prior publications on the stock. I am searching for an initial upside target above $10 and look forward to further coverage.

For further details see:

OraSure: Revising To Buy Following Extensive Growth Route