OSUR - OraSure: Valuation Upside On The Table At 16x Forward P/E

2023-05-17 05:47:01 ET

Summary

- OraSure came in with another strong quarter with upsides against the consensus at the top and bottom lines.

- The firm is concentrating heavily on capital allocation and will close its overseas InteliSwab production lines.

- The market expects strong earnings growth this year from OSUR.

- Net-net, reiterate buy.

Investment Summary

A swift repricing in the market value of OraSure Technologies, Inc. ( OSUR ) following its Q1 FY'23 has opened the gates for a very attractive buying point in my estimation. OSUR has been in my equity universe since 2021 with mixed ratings along the way, most recently revised to a buy in February. As a reminder to what changed in the investment thesis:

- Fundamental momentum building across the core portfolio with Covid-19 revenues dwindling, very important to margin mix and diversifying turnover.

- Company has its sights set on expanding core offerings and seized two new government contracts last quarter to supply its InteliSwab test.

- Record top-line of $123mm last quarter with 94% YoY growth rate pulling to 40% gross margin. With revenue growth, I believe this can stretch higher with economies of scale and other efficiencies.

- Management ploughing all Covid-19 related earnings back into the business to fund future growth initiatives.

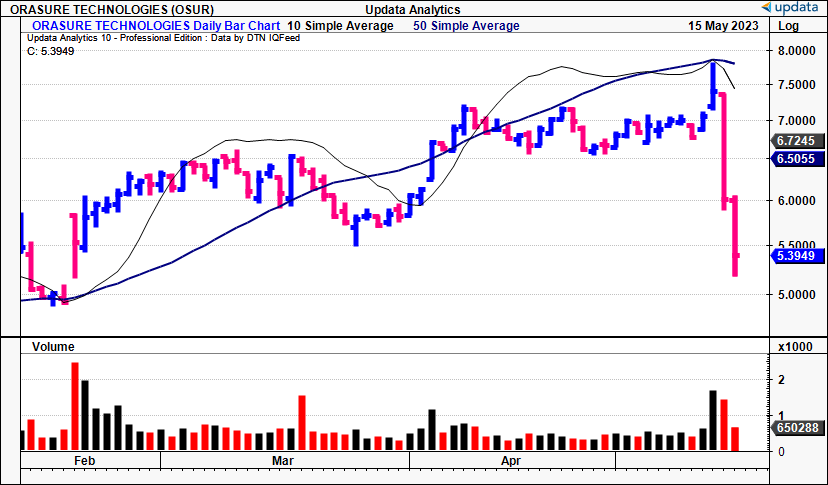

Turning to the latest set of numbers, there's numerous talking points to discuss. With post-tax earnings ratcheting higher, along with gross profitability, OSUR can now unlock risk capital on a forward basis and send off cash to its shareholders or retain earnings to reinvest for future growth. Alas, with the short-term selloff observed in Figure 1, there is now a serious dislocation in market expectations with the company now trading at 15x forward earnings and 1x book value, 45% and 58% below the sector respectively. Net-net, I continue to rate OSUR a buy and look to the $7.20-$8 marks as the next price objectives.

Fig. 1

{kind=link}

Q1 earnings disaggregation

Looking straight to the quarter the InteliSwab ("IS") segment is the first major talking point. Management note it is closing its overseas IS production lines to save margin and eliminate its overseas shipping charge from production cost. This may or may not be a beneficial saving. First, it will lower the capital charge for IS in the ex-US segment. Second, it could pull some pressure off gross margin with the reshuffled cost structure. However, it may also hamper production and therefore reduce the size of its operating line going forward. It will be a key decision to observe looking forward.

1. Income breakdown

Meanwhile, the firm booked $155mm in quarterly revenue, a tremendous 129% YoY growth schedule, also a company record. As mentioned, IS is the biggest driver of upsides at the top-line for OSUR at this point. It came in with $118mm in IS turnover versus $22mm the year prior, 434% growth for the period. This was driven by demand vs. pricing, and volumes began to taper off towards the end of Q2 apparently.

Further key observations include:

- Even with the revenue growth, OSUR saw ~150bps margin decompression to 42.5%.

- This will be helped by the cost savings plan (discussed later) where it hopes to save $0.50 per test in gross.

- The gross number is below the sector margin but has pushed back to FY'20-'21 range as seen in Figure 2. Here, the gross margin is illustrated as a function of revenue on a rolling TTM basis.

- Treating gross profit as a function of capital productivity, you'll see the gross profitability has curled up from 2-year lows with sequential upsides since June 2022. Here, gross profits are scaled by total assets. It shows that OSUR now produces $0.55 for every $1 in assets.

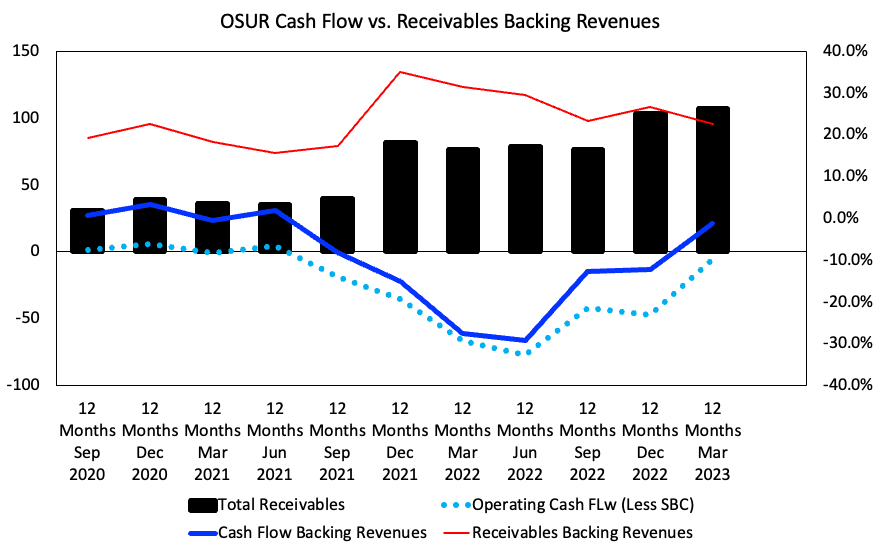

Considering these points, revenue quality is paramount. Naturally, given the revenue growth, total receivables backing the revenue stipulated growth has increased markedly above 2-year highs at the time of writing. It remains at ~20-25% of turnover. It is therefore pleasing to see operating cash flow trends curl back towards long-term range [Figure 3]. Here, you can see that OSUR is generating more OCF per unit of revenue in the last 3 quarters, on a rolling TTM basis. Convergence of the amount of receivables to OCF backing turnover will be a positive trend to look out for in FY'23 in my opinion.

As an additional tailwind, the firm is set to collect net $40mm in milestone payment under its government tenders by the end of this year. Added benefit here is the credibility from fulfilling all the deliverables under the government's contract. Should it hit those targets successfully, there's scope for additional fixed contract work down the line I would estimate.

Fig. 2

Data: OSUR 10-K's

Fig. 3

{kind=link}

2. Cost savings

The second talking point, taken over from its last quarter (and discussed in the last publication), is the cost savings plan. Part of this is the shut-down of its manual overseas IS lines, where it can focus entirely on production in the U.S. With this, it hopes to hit breakeven operating cash flow by FY'24. This follows the IS repackaging design that was completed in March. OSUR did this to free up gross margin and drive scale down the P&L. As mentioned, it hopes to achieve $0.50 cost saving per unit from doing this, which could amount to a large saving over time.

Further, with these actions, is reduced its non-production workforce by 11%. Net-net, it hopes to free up ~$15mm in additional liquidity from these cost savings measures and I'd suggest to track this closely looking forward.

Looking to capital productivity, the following points are relevant to the discussion:

- NWC density increased by ~$38mm for the quarter ($152mm annualized) as a result of the IS demand experienced.

- This will create a tailwind as it converts to cash over the coming periods, aiding profitability.

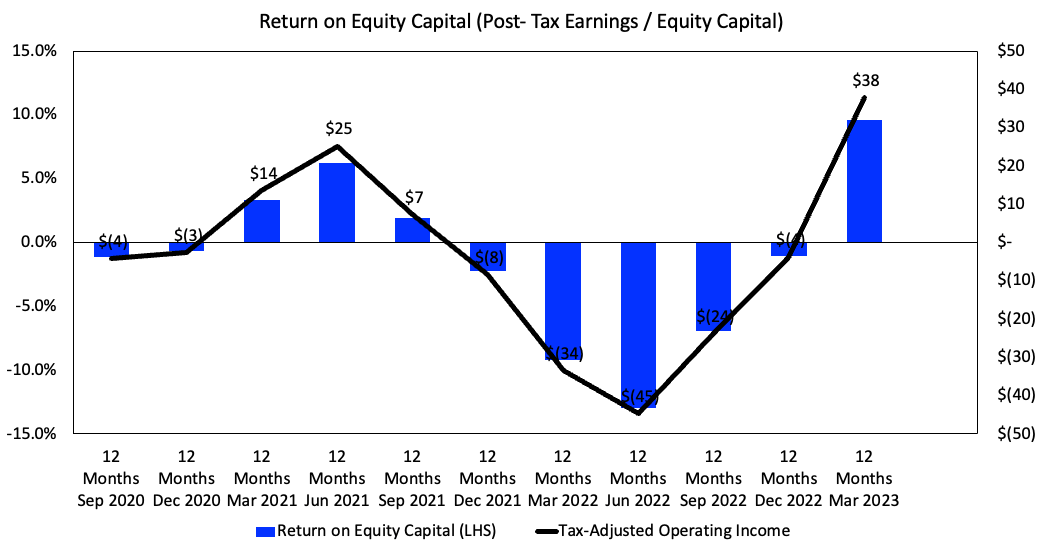

- With no debt, equity holders are the sole providers of capital. The TTM tax-adjusted operating income OSUR produced since Q3 FY'20 are observed in Figure 3. This is shown against the return on equity capital, calculated as the TTM post-tax earnings generated each quarter divided by book value of equity each quarter. You can see the rapid liftoff from June FY'22, corresponding with the reversal in share price. This turnaround in profitability shouldn't be discounted. It produced $38mm in tailing after-tax earnings last quarter which is a 2-year high.

Fig. 3

{kind=link}

3. Capital budgeting

On the capital it has put to work, the jump in NOPAT has pushed OSUR's return on investments back above the hurdle rate. The cyclicality in its return on existing capital at risk is observed in Figure 4. The firm's TTM NOPAT is shown against entire capital invested, including R&D adjustments, goodwill and intangible investments, each period. This is compared to a 10% hurdle rate to observe the change in economic earnings OSUR produced each quarter, up until Q1 FY'23.

Notably, investors were treated to economic profitability last quarter. The firm created ~230bps of economic profit above the 8% hurdle rate shown. This is integral to OSUR creating value for shareholders in future periods. The value of $1 must be more profitable in the company's hands versus the investors. The only way in which this can truly happen is if the returns on invested capital rest above the hurdle rate (10% in this instance).

Fig. 4

Data: Author, OSUR SEC FIlings

Finally on the capital budgeting front, I'd point out that OSUR completed 3 new commercial partnerships in Q1. These follow the Quest Diagnostics and Grifols announcements posted recently (check my Quest publication from February here ).

One, the Enriched DX deal, which is actually a co-promotion of the company's Colli-Pee device. It will develop various liquid biopsy solutions using first-void urine ("FVU"). FVU has been known to produce more potent biomarkers for various assays.

Two, it also signed papers with Ziwig to help commercialize Ziwig Endotes. This is a breakthrough innovation to diagnose endometriosis, touted by the French Ziwig to use salivary microRNA. There's importance here, because it can typically take eight years to diagnose endometriosis, so there's high unmet need on the diagnostics front within this disease, that has many variations by the way.

Three, the deal with Novozymes to support clinical development of their BiomeFx line. This is a microbiome assay that uses gut and vaginal microbiome in order to promote health. I'd keep a close eye on this one. In my opinion, this is fairly broad from OSUR's core offerings, and could broaden exposure to alternative assay menus that squeeze the company into various adjacent markets.

Collectively, these deals highlight OSUR's move focus on aligning with precision instruments, a currently underserved market in my opinion. Hence, there's scope for these deals to add value down the line.

4. Outlook

Speaking of the forward-estimates, management project $25-$30mm in IS revenues in Q2 FY'23. Note, this is well back from the $118mm observed in Q1, but very much expected. Annualized, this could hit $75-$100mm for the year (excluding the first quarter result). It also projects $67mm in Q2 revenue at the upper end of range, $268mm annualized.

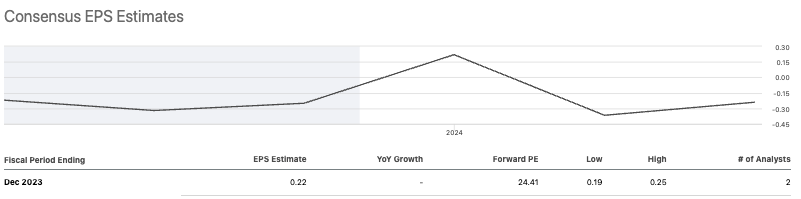

Fig. 5 - OSUR Consensus EPS Estimates

{kind=link}

I am in-line with these numbers and believe the company can do $320-$330mm in turnover this year, and pull this down to $0.20-$0.25 in EPS. Note consensus' project a similar trajectory [Figure 5] leading me to question what is already in the expected in the OSUR share price. That is, what is expected at the current price, and, if anything, what could be missing from these expectations.

5. Valuation

Shares are priced at 16x forward earnings, a 17% discount to the sector's 19.5x multiple. You'd also be pleased to see OSUR priced at 1x book value, making the 7-8% trailing ROE look more attractive as an investor ROE at that multiple. We've also got the company at 6x forward EBITDA and that's a steal in my opinion, not to mention 24% discount to the sector as well. On these grounds, it is unsurprising to see the company rated in the top bracket for valuation in the quant factor grades.

Fig. 6 - OSUR Quant factor gradings

Data: Seeking Alpha

I'd be comfortable with a 12% discount rate in pricing OSUR given the long-term averages in the market and a factor of risk from giving up the current 3-4% yield at the risk free rate to invest here instead. I'd make a few inferences from this, to gauge what the market expects:

- Assuming no growth, at the 12% hurdle rate, the market expects ~$50mm in pre-tax earnings from OSUR this year, getting you to the $400-$415mm market valuation range ($49 / 0.12 = $408). There would be some deviation both ways on this.

- This presumes a 42% growth in annual EBIT from FY'22-'23, indicating the market has very high growth expectations for the company.

- I believe there's scope for OSUR to outperform these expectations and my numbers call for c.$60mm in FY'23 pre-tax income valuing the company closer to $500mm in FY'23.

- Looking forward, I'd call for an 8% CAGR on this EBIT number into FY'25. That calls for a $629mm market value for OSUR ($8.30/share) and is potentially what the market is missing. Even a 3% CAGR over the next 2-years has the company valued at $546mm market value (60x1.03^3)/0.12 = $546).

In any sense, if OSUR does in fact generate the earnings growth outlined above, the NPV of its future market value is higher than it is currently, presuming the 12% discount rate. Even with conservative 3% annual earnings growth estimates, I am getting to 34% upside potential at the time of writing ($546/$407-1 = 0.34). This is supportive of a buy.

Conclusion

In summation, there are multiple inflection points that add bullish weight to the OSUR investment debate in my opinion. Chief among these, are gross profitability trends and highly supportive valuations. I would be calling for a market cap if $630mm ($8.30/share) if OSUR can hit $60mm in pre-tax income this year and compound these earnings at 8% per year into 2025, a 54% return objective ($7.20/share). Even with conservative figures, I'd be looking to 30-35% upside, presuming the market is an accurate judge of fair value over time, and a 12% discount rate. In that vein, there is ample evidence in my investment psyche to continue the buy rating on OSUR.

For further details see:

OraSure: Valuation Upside On The Table At 16x Forward P/E