ORTX - Orchard Therapeutics: MLD Opportunity Could Be Larger Than Initial Estimates

2023-04-24 17:38:49 ET

Summary

- Shares have lost a third of their value over the past year.

- HSC-based gene therapy Libmeldy is approved in the EU for MLD with a ~$3.5M price tag. Incidence could be higher than initial estimates.

- Cash position was bolstered with March financing, burn rate is coming down, and there are multiple shots on goal in the pipeline.

- Bear thesis boils down to poor prior execution, regulatory setbacks (obstacles raised by FDA), and slow launch out of the gate.

- ORTX is a Buy and I suggest accumulating shares below $6. I see a pathway to value creation via accelerating sales growth in the medium term.

Shares of Orchard Therapeutics ( ORTX ) have lost a whopping 96% of their value since my initial foray into this gene therapy pioneer in 2019. Over the last year, they've lost roughly a third of their value.

When I look at my old article, I see that quite a few of their HSC-based gene therapy programs were discontinued (whether due to competitive concerns like beta-thalassemia, data or perhaps clinical feasibility issues like WAS or X-CGD). With all of that pipeline attrition, not to mention regulatory hurdles faced for lead program Libmeldy in metachromatic leukodystrophy (MLD), the name had fallen off my radar.

This changed with March's strategic financing, providing the company with up to $188M of funding (at successively higher valuations). I was also persuaded to reenter by Q4 call nuggets, two of which were the increasingly efficient cost structure leading to narrowing burn rate as well as higher than expected incidence of MLD in initial screening efforts (hinting at larger market opportunity than initially projected).

With the above providing some context for why I prioritized this name for our Core Biotech (commercial-stage) portfolio, I look forward to providing a more complete overview for readers.

Chart

{kind=link}

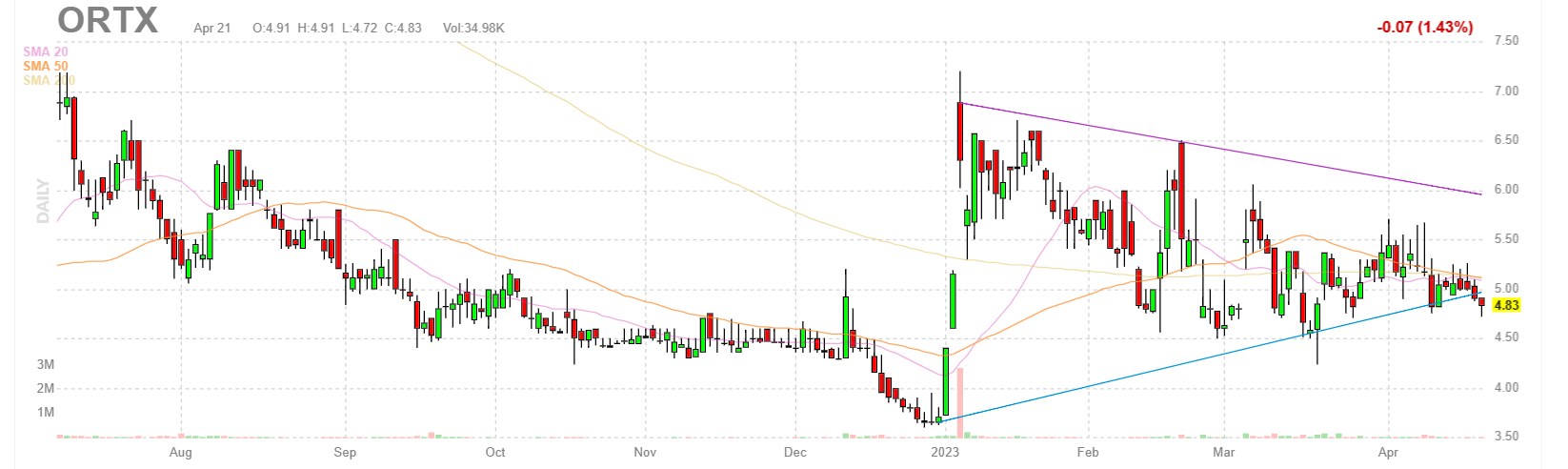

Figure 1: ORTX daily chart (Source: Finviz)

When looking at charts, clarity often comes from taking a look at distinct time frames in order to determine important technical levels and get a feel for what's going on. In the daily chart above, we can see share price spike to $7 after January's progress report showed that a turnaround was potentially in place (growing Libmeldy sales, reduced burn rate and Type B meeting with FDA). From there, shares have bounced around in the $4.50 to $5.50 range and are in a holding pattern ahead of expected news on regulatory progress with the FDA. My initial suggestion is that readers interested in this name would do well to acquire a position in the current range (below $6).

Overview

Founded in 2015 with headquarters in London (166 employees), Orchard Therapeutics currently sports enterprise value of ~$550M (fully diluted) and Q4 cash position of $175M providing them operational runway for ~3 years. I should point out the company also has $32.4M of debt outstanding.

When discussing share structure, I must first highlight terms of March's financing with key institutional investors (led by RA Capital Management, participation from Deep Track Capital and others). On March 10th closing, Orchard received $34M (shares and warrants, total issuance of 56.7M shares). Investors committed to purchase additional units at $8 per unit (successively higher share price) for $34M (issuance of 42.5M shares). Total of 109.M warrants are being sold in the offering at exercise price of $1.10 per share if Libmeldy is approved by the FDA in 2024 (and exercise price of $0.95 per share if approved after 2024). As if that weren't confusing enough, throw in a 1:10 reverse split into the mix that occurred March 10th. 10-K report currently shows 128M shares outstanding (fully diluted), equating to $700M market capitalization at current share price.

Orchard can be described as a global gene therapy company with the chosen approach of utilizing ex vivo autologous hematopoietic stem cells ( HSC ) to "harness the power of genetically modified blood stem cells and correct the underlying cause of disease" ( 10-K filing ). This stands in stark contrast to other companies I've profiled like Rocket Pharmaceuticals ( RCKT ), which is modality agnostic, and 4D Molecular Therapeutics ( FDMT ) which utilizes customized vectors for AAV gene therapy. To date, over 170 patients have been treated by Orchard's current and former product candidates across seven different diseases with follow-up periods of over 11 years following single administration.

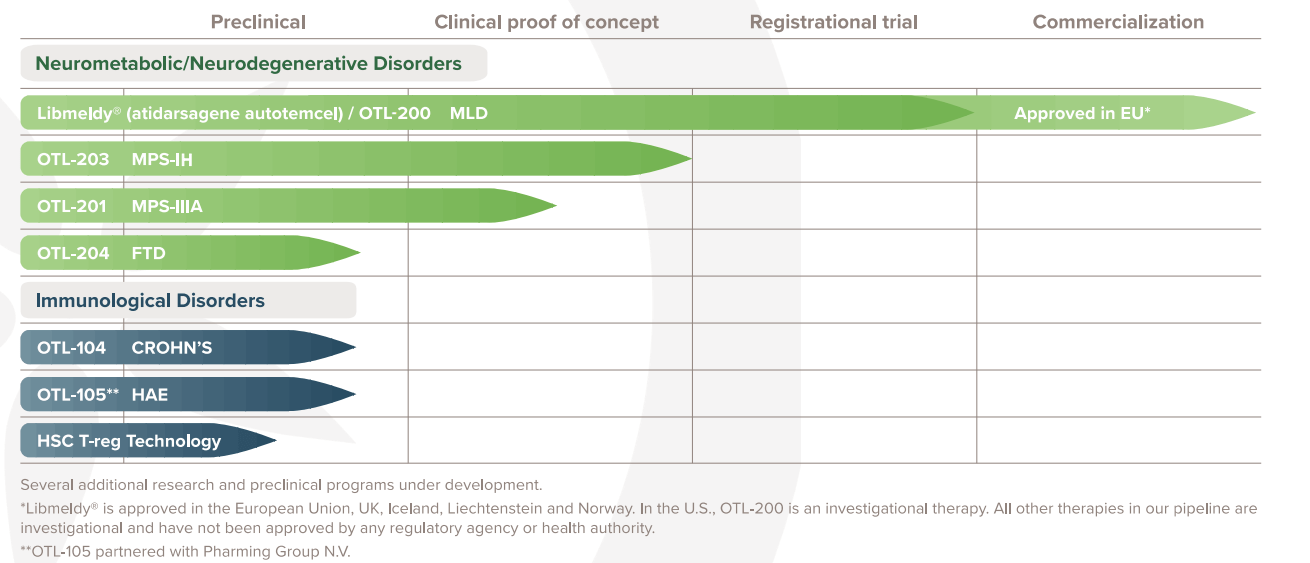

Pipeline is divided into two franchises, neurometabolic/neurodegenerative disorders and immunological disorders. Of the former, OTL-200 (Libmeldy) is approved in the EU and a few other countries (UK, Sweden, etc) for eligible MLD patients. Pre-BLA meeting with the FDA should take place this quarter with BLA submission to follow midyear.

{kind=link}

Figure 2: Pipeline (Source: corporate presentation )

Management believes their HSC-based approach has broad applicability to a large number of indications. This is because of "the ability of HSCs to differentiate into multiple cell types allows them to deliver gene-modified cells to multiple physiological systems, including the central nervous system ( CNS ), immune system and red blood cell and platelet lineage" ( per 10-K filing ). The company further notes that HSCs "have a unique, innate self-renewing capability as they are engrafted in the bone marrow and additionally can achieve stable integration of a modified gene into the chromosomes of HSCs".

It's worth mentioning that Orchard is utilizing existing network of CDMOs for drug manufacturing along with development capabilities in London. This came as part of March 2022 cost-cutting efforts where the company was forced to lay off 30% of its workforce and ceased work on manufacturing facility in Fremont, California two years prior to that. I recall from a few years back that the company was having to do bridging studies from "fresh" cell to cryopreserved formulation with all trials going forward expected to use the latter (greatly facilitates logistics). Outside of HAE, Orchard owns global rights to all drug candidates in the pipeline, with the next up after Libmeldy being MPS-IH set to move into pivotal trials.

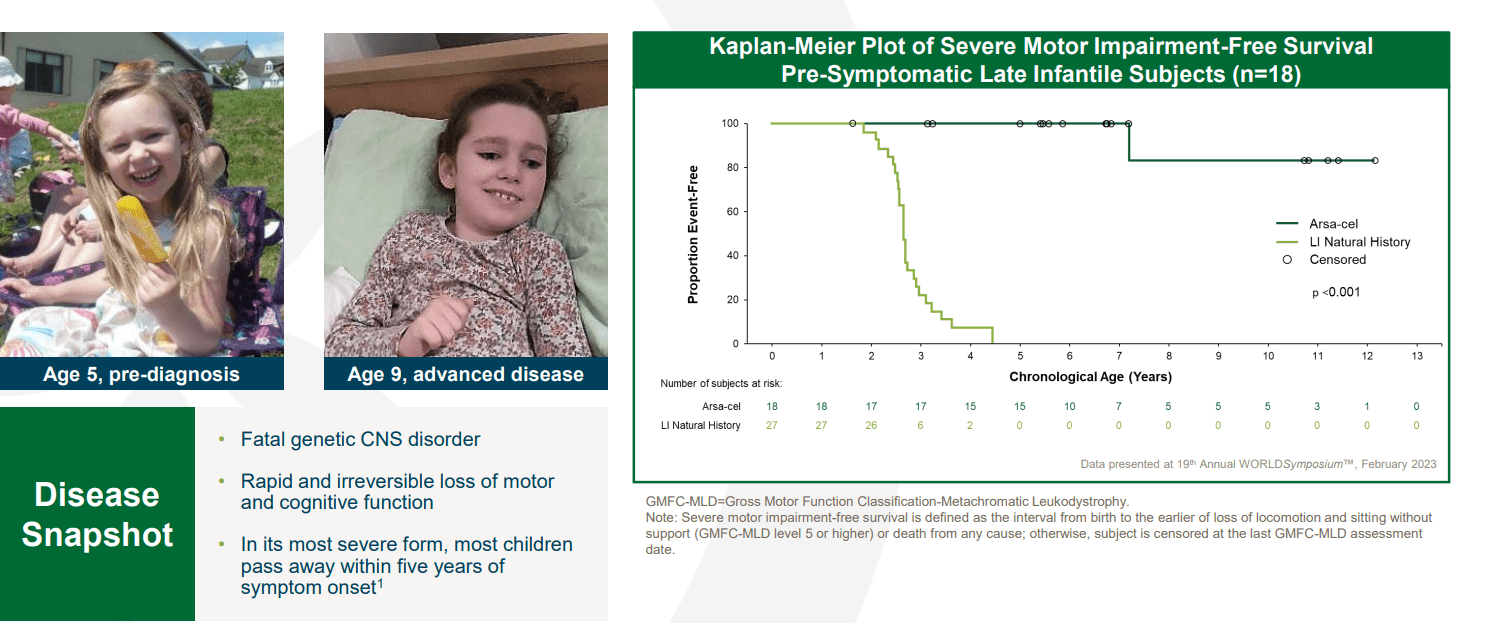

Focusing on Libmeldy in MLD, this is a life-threatening disease occurring in 1 in every 100,000 live births in most regions of the world (could be higher as recent screening efforts are showing). Higher incidence rates have already been reported in the Middle East. MLD is caused by a mutation in the arylsulfatase-A (ARSA) gene that results in accumulation of sulfatides in the brain and other areas of the body. Over time, the nervous system is damaged and this leads to neurological problems (motor, behavioral, seizures, etc). Late infantile form of MLD has 5-year mortality of ~50% (juvenile is somewhat less severe but still results in early mortality).

{kind=link}

Figure 3: Libmeldy's highly convincing survival benefit in 18 MLD patients (Source: corporate presentation )

MLD is clear-cut example of one that is ideal for gene therapy, as apart from Libmeldy there are no effective treatments and only palliative care is offered. Libmeldy provides the potential for a long-term cure, though again the jury is still out on this one (waiting for longer follow up). Rights to the program were obtained via asset purchase from GSK back in 2018.

European Commission granted full (standard) marketing authorization for Libmeldy in December 2020 for the treatment of early-onset MLD in children with either late infantile or early juvenile forms of the disease. As one can imagine, the company has committed to follow patients for the long term (up to 15 years) as a post-marketing commitment. Approval was granted based on results from 29 MLD patients, 20 of which were pre-symptomatic (9 were early-symptomatic). Digging into the most important nuggets, I see that patients treated with Libmeldy experienced significantly less deterioration in motor function at 2 and 3 years post-treatment (measured by GMFM total score, high statistical significance at p?0.008). The most telling part is that ALL late infantile treated patients were alive with follow-up post-treatment of up to 7.5 years and 10 of 13 early juvenile patients were alive with follow-up of up to 6.5 years.

Delving a bit more into motor development, by 4 years post-disease onset 62.5% of early juvenile MLD patients survived (compared with just 26.3% of untreated), clearly showing delay of disease progression. Likewise with cognition and language abilities, 12 out of 15 assessed patients had IQ/DQ within the normal range. All but two of these patients remained above the threshold of severe mental disability whereas ALL 14 untreated comparator LI patients showed evidence of severe cognitive impairment. This is quite convincing to my eyes.

As ROTY member Osmium. Research has pointed out (in colorful language as always), development in the US has been much slower and much of that can be placed at the feet of the FDA. Rare Pediatric Disease designation has been granted (potential for a Priority Review Voucher, which could be sold for $100M+), along with RMAT designation (allows for continuous communication). BLA filing could come as soon as midyear after feedback from Q2 meeting.

Moving on to MPS-IH, incidence is thought to be similar to MLD at 1 in 100,000 live births (60% of children born with MPS-I have MPS-IH). Mucopolysaccharidosis type I is a lysosomal storage disease caused by a deficiency of the lysosomal enzyme alpha-L-iduronidase (IDUA). Median diagnosis is 12 months and most affected children are diagnosed before 18 months of age. They may appear normal at birth but develop symptoms in the first 6 months. Allogeneic-HSCT is commonly accompanied by enzyme replacement therapy ( ERT ) from diagnosis and is the standard of care. 203 has orphan drug and PRIME designation from the EMA as well as orphan drug and rare pediatric disease designation from the FDA.

Moving on to MPS-IIIA (Sanfilippo syndrome type A), I think of this one as a somewhat crowded indication being used for POC by a variety of gene therapy companies (though to be fair, nothing has been approved yet). Within the first years after birth, MPS-IIIA and MPS-IIIB patients begin to experience progressive neurodevelopmental delay and decline. Ultimately, they progress to vegetative state and life expectancy is between 10 to 25 years. Early findings for OTL-201 include observation of supraphysiological levels of SGSH enzyme and early neurocognitive outcomes also indicate that since receiving 201, 4 of 5 patients showed gain of cognitive skills (in line with development of healthy children).

There is high optionality with this story (one reason that makes it attractive to me as an investor) via pursuit of more prevalent indications with the first of these being NOD2-Crohn's disease. NOD2 is the most common genetic factor in Crohn's (20% of 40% of Crohn's patients carry mutations causing defective NOD2 activity). This subset of Crohn's patients have more severe symptoms and are more refractory to existing therapies. There are up to 200,000 patients in the US and EU with two NOD2 mutated alleles. OTL-104 is still in preclinical development and I look forward to seeing what this program can do in human studies (IND submission expected in 2024).

Other Information

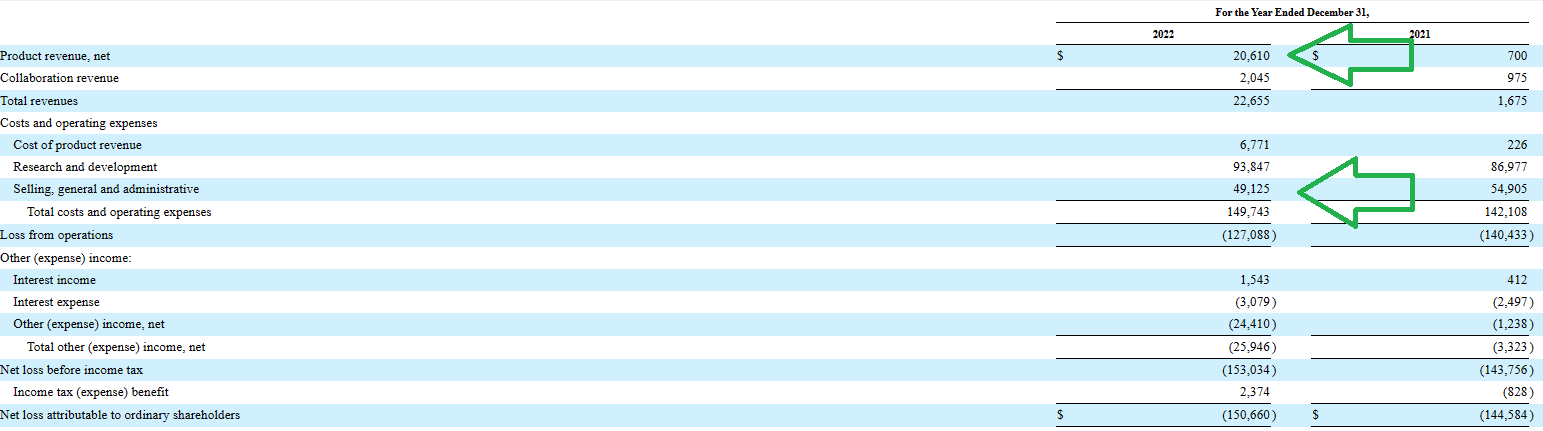

For the fourth quarter of 2022 , the company reported cash and equivalents of $143M (does not include proceeds from March financing). Keep in mind the company also had $32.4M of debt. Net loss was $7.9M but excluding one-time offsets would have been $23.4M for the quarter. Libmeldy revenue rose to $5.8M (cost of product sales was just $2.4M). Research and development expenses rose slightly to $25.5M, while SG&A fell by 22% to $10.6M.

{kind=link}

Figure 4: Financials improving over the past year (Source: 10-K filing )

For Libmeldy commercialization in the EU, management notes that 3 genetically confirmed cases of LMLD were identified after screening 96,000 newborns globally to date (suggests incidence is higher than initially thought). One of these cases was assessed clinically and referred for treatment with Libmeldy (other two are pending clinical assessment). 6 studies are actively screening newborns in EU, Middle East and US. Libmeldy received the strongest possible recommendation for use by the New Therapies Council following completion of health economic evaluation by FINOSE (consortium between Finland, Norway and Sweden). Additional reimbursement discussions are ongoing including in Spain, France and Beneluxa region. Moving on to anticipated 2023 milestones, the big one of course is Libmeldy's BLA submission midyear. For ongoing commercialization efforts, reimbursement agreements in at least one additional market in Europe will be secured along with expansion of newborn screening activities throughout the US, EU and Middle East. Pivotal trial for OTL-203 in MPS-IH will get underway 2H 23 and additional clinical data for OTL-201 in MPS-IIIA is expected. For OTL-104 in NOD2-Crohn's, further preclinical data is expected in the near term with IND filing to follow in 2024. Other preclinical programs will move forward (including Pharming-funded OTL-105 for HAE (Orchard stands to receive up to $189M in milestone payments plus mid-single to low-double digit royalties).

On the conference call , management highlighted the fact that Libmeldy did $20M of sales in its first year on the market despite having few reimbursement agreements in place. Significant acceleration is expected as they expand access and reimbursement to other markets and implement additional newborn screening studies. For financials, management notes that cash burn has been reduced by 38% for Q4 2022 versus Q1 2022.

Looking specifically at MLD market opportunity, Libmeldy is the most expensive ever approved drug by the NHS in UK at £2.875M ($3.5M). Conservative estimates for sales mentioned in my Trade Post were $100M-$300M in US with similar in EU.

{kind=link}

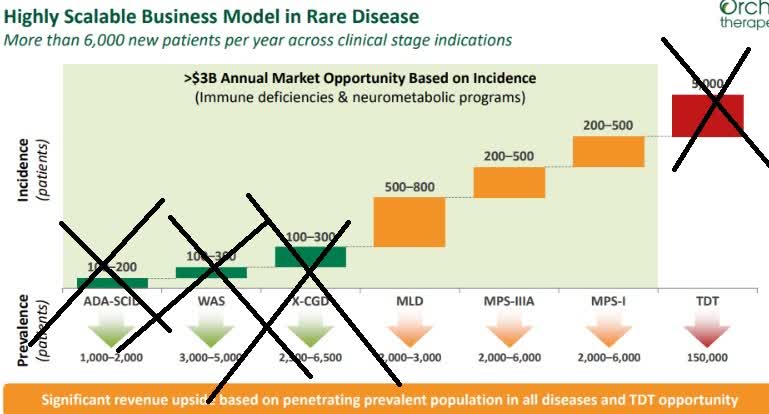

Figure 5: Sizeable opportunity in MLD, optionality with MPS-IIIA and MPS-I (source: old slides)

However, as per recent conference call nugget, if incidence of MLD were higher than initial projections at 3 cases per 100,000 live births, that puts them closer to SMA (spinal muscular atrophy) which has incidence of 4 to 10 cases per 100k live births. Biogen/Ionis' ( BIIB ) Spinraza did $2.5B in peak sales and Novartis' ( NVS ) gene therapy Zolgensma is currently doing a $1.4B run rate after logging $368M in Q4 2022 sales (+18%). Thus, if Libmeldy ends up on the higher end ($800M+ global sales), that alone could spike substantial appreciation in share price/valuation without even taking other pipeline indications into account.

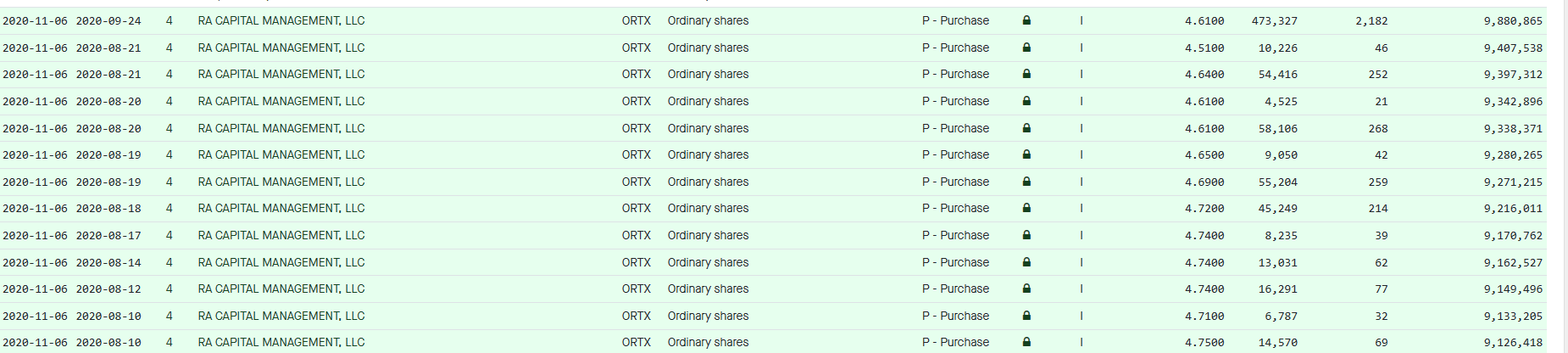

As for institutional investors of note , after March financing Deep Track Capital owns a 9.99% stake as does RA Capital (in addition to right to purchase more stock via warrants). Recently on April 1st and 5th, I see insiders made small purchases on the open market (CEO Bobby Gaspar now owns 366,000 shares). Interestingly, RA Capital recorded quite a few open market purchases in late 2020 (multiple those cost averages by 10 to account for 1:10 reverse split!).

{kind=link}

Figure 6: RA Capital purchases (Source: Fintel )

As for relevant leadership experience, President and COO Frank Thomas served prior in the same role at AMAG Pharmaceuticals (acquired in 2020 for $650M). Chief Technical Officer Nicoletta Loggia hails from Novartis (led teams in AAV and CAR-T space including Avexis' technical capabilities). Chief Scientific Officer Fulvio Mavilio served prior as SVP Translational Science at Audentes Therapeutics (bought out by Astellas for $3B). Chief Commercial Officer Braden Parker commercialized several rare oncolytic and genetic disorder products at Celgene, NPS Pharma (acquired by Shire for $5.2B) and PTC Therapeutics.

Moving on to compensation, cash portion of salary for CEO seems on the high side (for a small cap company looking to turn itself around) at $600k but certainly is not a red flag in and of itself. Options awards likewise are on the high side (though not necessarily excessive).

{kind=link}

Figure 7: Compensation table (Source: Proxy filing )

Moving onto useful nuggets shared in our Live Chat by members of ROTY Biotech Community, Osmium. Research points out the following:

"I actually looked at this company despite my reluctance to consider early stage drug companies and I liked it. 1st off, treating a storage disease is just a wonderful thing and their data here looks very good. Typical that children in Europe can now benefit while the idiots at FDA let their kids suffer. It's a differentiated approach to gene therapy. Revenues are growing. Valuation is reasonable"

I consider that high praise, given Osmium's usually high degree of skepticism and narrow universe of quality names he actually likes.

As for intellectual property and barriers to entry, Orchard does not own any patents or patent applications that cover Libmeldy or any of their lead product candidates (potentially concerning). They rely on regulatory protection based on orphan drug and other designations or exclusivities provided by the agency. They also rely on know-how and trade secrets.

As for other useful nuggets from the 10-K filing(you should always scan these because investors may not get the complete picture from press releases), the company came by its assets via 2018 purchase agreement with GSK. Orchard remains on the hook for up to £90M milestones and tiered royalty rate that is definitely on the high side (mid-teens to low-twenties). There is an element of uncertainty in the area of manufacturing given the fact that the company does not have in-house facilities (relies on CDMOs). This could make it harder to meet regulatory deadlines, requirements and also result in supply disruptions or delays.

As for competition, in MLD there are no other effective treatment options and as noted prior HSCT has demonstrated limited efficacy in halting disease progression. Other gene therapy companies such as Passage Bio and Affinia have AAV gene therapy programs but they are still preclinical. Takeda is investigating an ERT for biweekly intrathecal infusion as well. For MPS-IH indication, current standard of care is HSCT before the age of 30 months and REGENXBIO ( RGNX ) has a phase 1 program (delivered intracisternally). Standard of care treatment involves regular IV injections of Aldurazyme from BioMarin and Sanofi Genzyme. For MPS-IIIA, there are 3 gene therapy candidates in development including Lysogene's (collaboration with Sarepta terminated in July 2022) and Abeona's ABO-102 (outlicensed to Ultragenyx Pharmaceuticals with regulatory discussions taking place this year ahead of potential BLA submission to follow). For NOD2-Crohn's, there are no approved treatment options specifically for this form of the disease and keep in mind many patients have uncontrolled symptoms despite evolving standard of care (biologics, surgical interventions, etc).

Final Thoughts

To conclude, one could argue that current valuation is backstopped by EU approval of Libmeldy alone. Investors obtain significant optionality via possible US approval in 2024, potential for higher incidence of MLD than initial estimates, MPS-IH & MPS-IIIA moving into late-stage studies and higher incidence indications such as NOD2-Crohn's later on down the line. The benefits of Orchard's HSC-based approach are clearly evident in the MLD data (convincing improvements and benefits observed in survival, motor skills, cognition and other relevant areas).

For readers who are interested in the story and have done their due diligence, ORTX is a Buy in the current range and I suggest accumulating exposure below $6.

Speaking of which, key risk factors in the near term include any hiccups in pre-BLA meeting with FDA as well as setbacks/delays in the clinic with MPS-IH and MPS-IIIA programs. If commercialization efforts for Libmeldy were to slow or experience setbacks (lower incidence of patients turning up or trouble with expanding footprint & screening efforts), that would weigh on share price and valuation as well.

While as an investor I leave price targets to the analysts, I do look at a blend of technicals, enterprise value, upcoming catalysts and future prospects to provide a realistic guess of potential upside in the medium term. I think a return to mid-2022 highs of $10-$12 (100% upside) is certainly possible if Libmeldy sales take off in the medium term (2023-2024 period).

OTHER LINKS OF INTEREST

UK's most expensive drug Libmeldy saved Teddi Shaw, but is too late for her sister

Libmeldy: World's 'most expensive' drug recommended for NHS use

Gene therapy offers new hope for children with metachromatic leukodystrophy

For further details see:

Orchard Therapeutics: MLD Opportunity Could Be Larger Than Initial Estimates