BTG - Orezone Gold Appears Undervalued After Recent Selloff Presenting A Buying Opportunity

2023-08-14 13:01:59 ET

Summary

- Orezone Gold has successfully completed its Bomboré gold mine on schedule and under budget in Burkina Faso. Commercial production generated significant net income, FCF and debt repayment.

- However, the Orezone stock was sold off lately mainly as a result of locally-observed and supposedly-transient ore under-conciliation.

- Orezone presents an opportunity for risk-tolerant investors due to its low-cost gold production and promising growth outlook.

Among all new gold producers, Orezone Gold Corp . ( ORZCF ) stands out with its on-schedule, under-budget completion of the Bomboré gold mine in an inflationary environment. Orezone poured the first gold on September 10, 2022, and declared commercial production on December 1, 2022, at its mine in Burkina Faso.

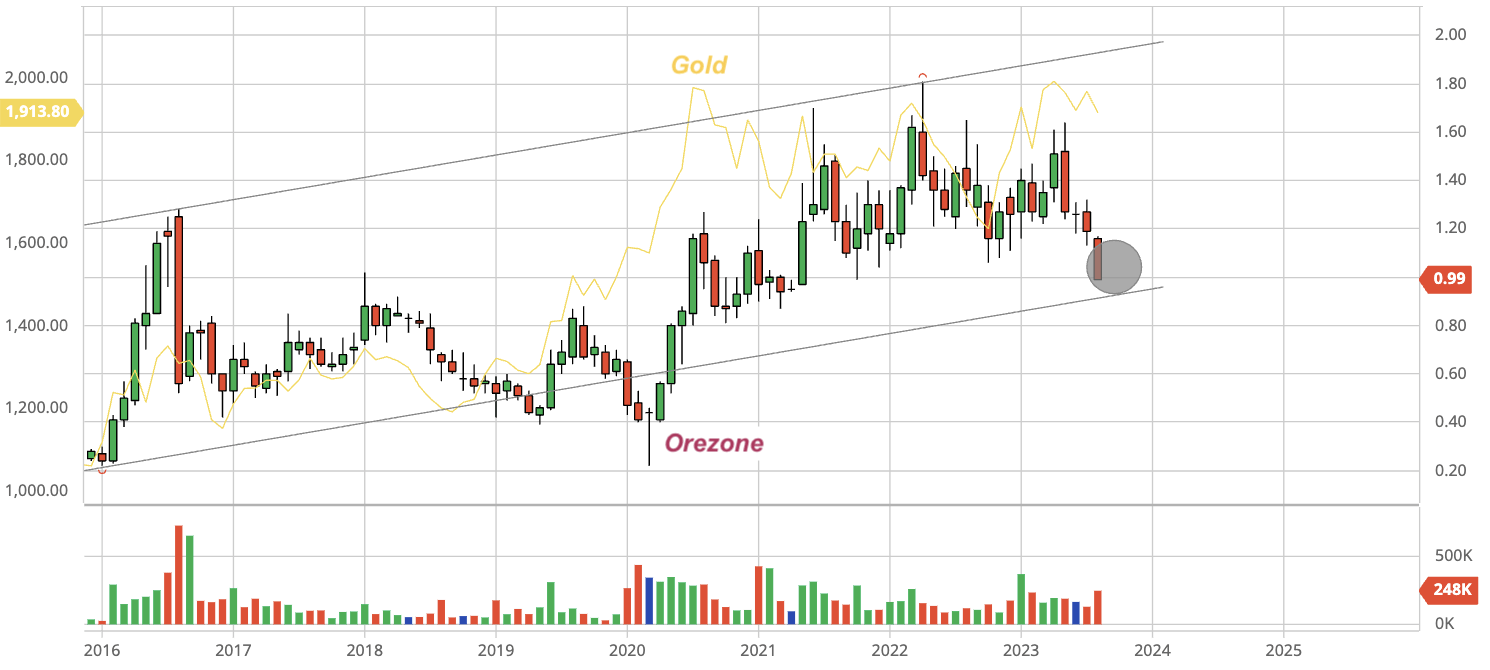

Despite these operational accomplishments, Orezone's stock did not react as positively as one would expect from its transformation from a developer to a producer, even during a period when the gold price has remained consistently strong, as shown in Figure 1.

Fig. 1. Stock chart of Orezone, as compared with the gold price (modified after Barchart and Seeking Alpha)

{kind=link}

A slew of questions arise: Is Orezone's investment thesis still valid? What are the near-term catalysts? What should a long-term investor do at this juncture?

Operations

Orezone owns a 90% interest in the Bomboré gold mine, with the government of Burkina Faso retaining a 10% carried interest.

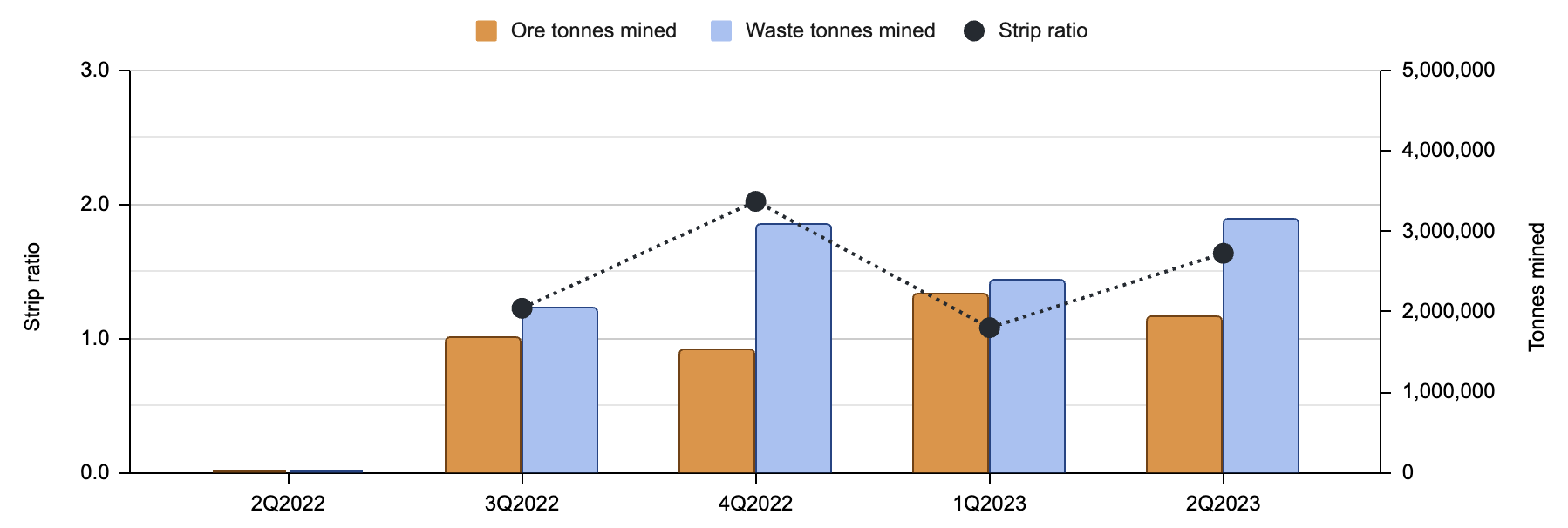

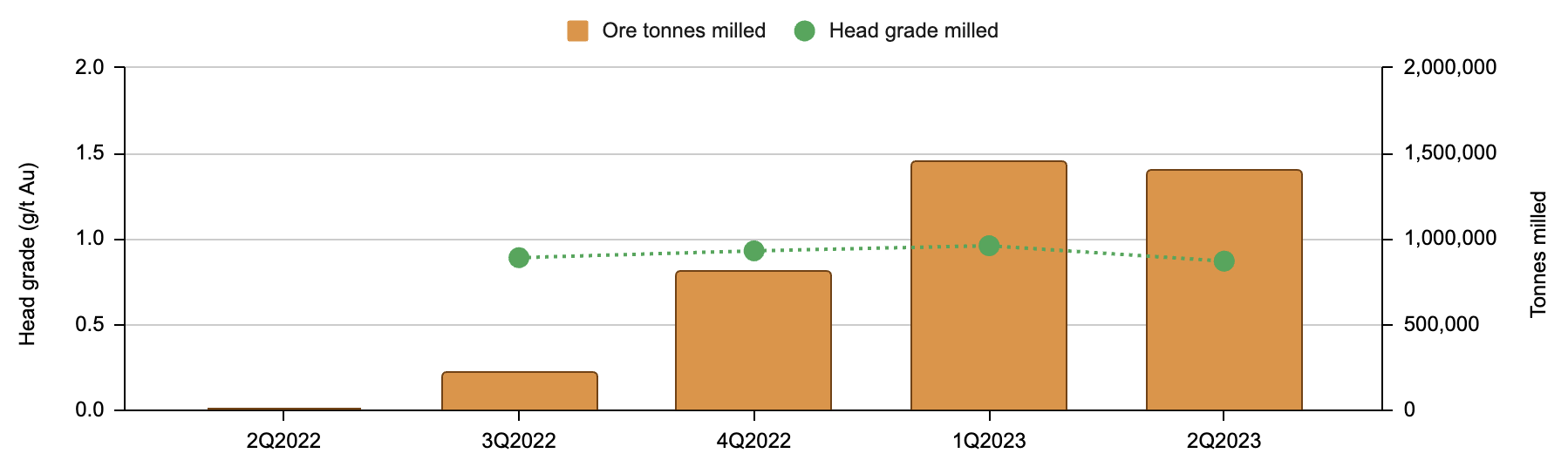

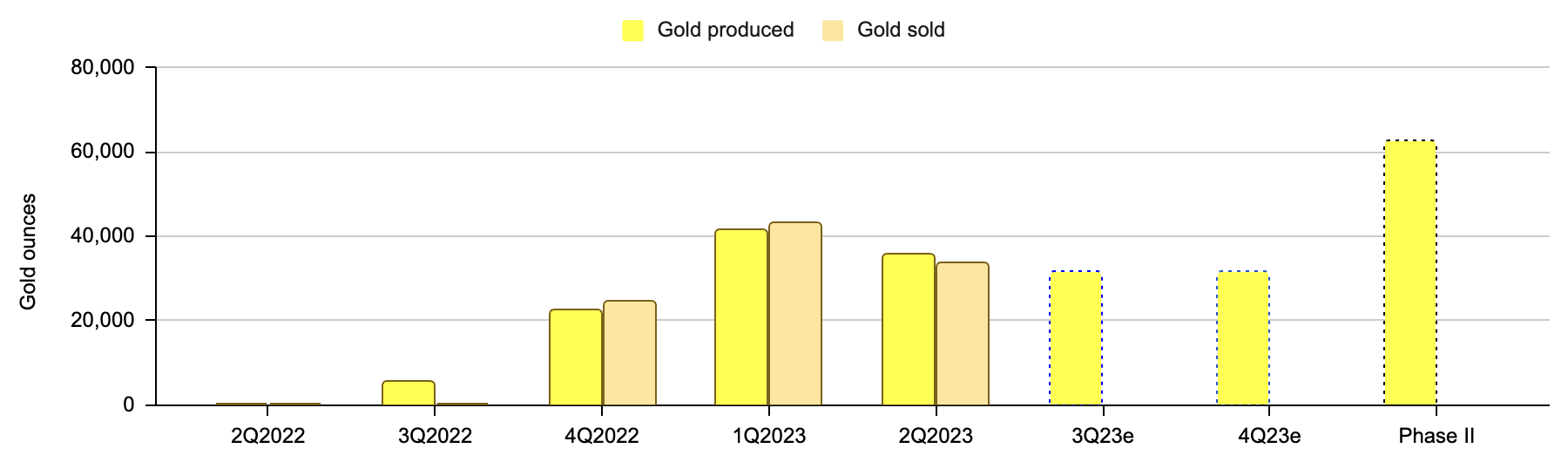

In the last four quarters since Bomboré started producing, Orezone has cumulatively mined 7.33 Mt of ore at an average strip ratio of 1.5, as illustrated in Figure 1. Additionally, Orezone has milled a total of 3.87 Mt of mined ore at average head grades ranging from 0.87 g/t to 0.96 g/t gold, as shown in Figure 2. During this period, Orezone produced 104,613 ounces of gold, including 33,608 ounces in the 2Q2023, as depicted in Figure 3. Notably, during the second quarter, the plant operated at approximately 7% above its nameplate capacity.

Fig. 1. Ore and waste mined at the Bombore gold mine, shown with the strip ratio (Laurentian Research for The Natural Resources Hub based on information gathered from Orezone and Seeking Alpha) Fig. 2. Ore milled at the Bombore plant, with the head grade of the milled ore shown (Laurentian Research for The Natural Resources Hub based on information gathered from Orezone and Seeking Alpha) Fig. 3. Gold produced and sold by quarter of Orezone (Laurentian Research for The Natural Resources Hub based on information gathered from Orezone and Seeking Alpha)

{kind=link}

{kind=link}

{kind=link}

In the 2Q2023, the all-in sustaining costs (AISC) amounted to US$1,109/oz, marking a 20% increase from the $926 reported in 1Q2023. This rise was predominantly caused by a combination of lower head grades, reduced plant throughput, decreased recovery rates, higher unit operating costs, and timing variations in sustaining capital allocation.

During the 2Q2023 earnings report, Orezone highlighted that processed head grades in the first half of 2023 were lower than initially projected. This was attributed to a more significant historical artisanal depletion in specific near-surface, higher-grade ore zones being mined. The company adjusted its 2023 guidance accordingly, saying that gold production for the year is likely to lean towards the lower end of the guidance range (140,000 to 155,000 oz), accompanied by an upward revision in AISC guidance (US$1,100-1,180/oz, up from US$1,010-1,110/oz Au).

This adjustment to the 2023 guidance is likely a contributing factor to the recent sharp decline in Orezone's share price, falling below C$1.20 (Figure 1). However, it is believed that the aforementioned issue will have limited impact moving forward:

"Significant artisanal workings were encountered in H1-2023 but evidence of artisanal activity has diminished as the Company mines towards lower pit benches. As a result, the Company expects historical artisanal activity to have less influence on the modeled mined grades in H2-2023."

It is worth noting that, as planned, Orezone processed its last remaining stockpiles of higher-grade ore accumulated during construction in June 2023. Therefore, even though greater mining volumes and lower artisanal depletion are expected, gold production is projected to decline in the second half of 2023, as depicted in Figure 3.

Financials

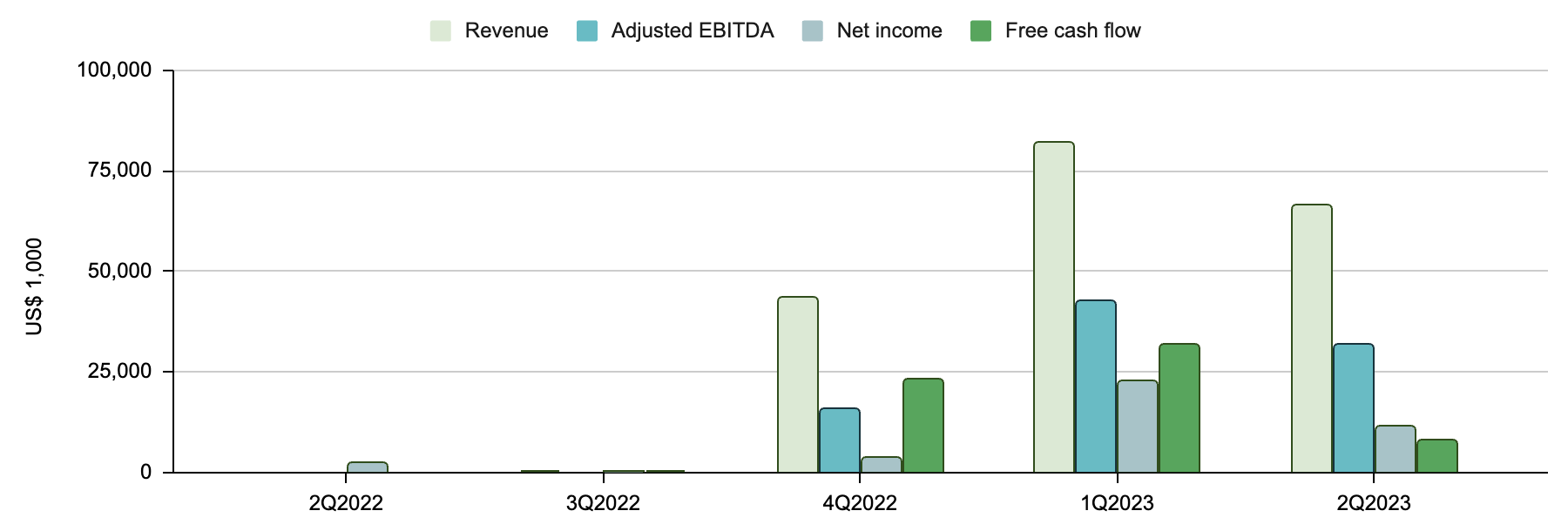

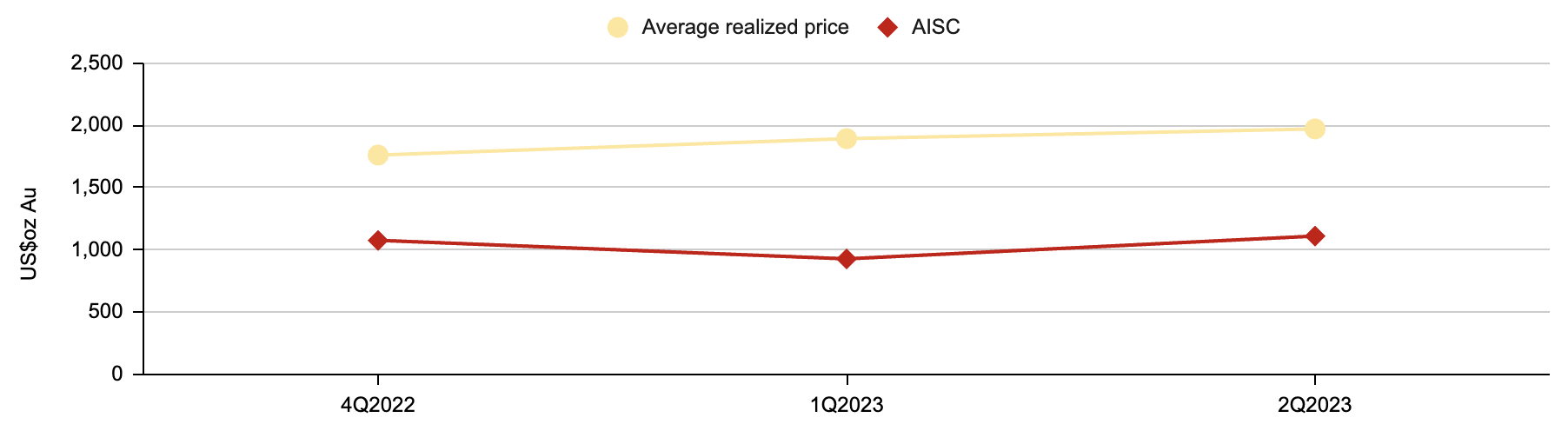

Orezone has sold 101,423 ounces of gold since its first gold pour, generating revenue of US$191.54 million, as illustrated in Figure 4. The company has maintained its AISC between US$926 and US$1,109 per ounce of gold, with realized gold prices ranging from US$1,760 to US$1,970 per ounce, as depicted in Figure 5. Consequently, Orezone has achieved a cumulative net income of US$39.92 million and generated US$62.75 million in free cash flow during that time.

Fig. 4. Revenue, adjusted EBITDA, net income and free cash flow of Orezone (Laurentian Research for The Natural Resources Hub based on information gathered from Orezone and Seeking Alpha) Fig. 5. Realized gold price and AISC of Orezone (Laurentian Research for The Natural Resources Hub based on information gathered from Orezone and Seeking Alpha)

{kind=link}

{kind=link}

The cash flow enabled Orezone to repay XOF 11.5 billion (or US$19.1 million) under the Coris Bank International senior loan facility in the second quarter of 2023, resulting in principal repayments of XOF 17.5 billion (US$28.8 million) in the first half of 2023 and the extinguishment of the Coris Bank short-term loan. As of end-June 2023, debt principal stood at US$101.6 million, consisting of XOF 40.0 billion (US$66.6 million) on the senior loan facility and US$35.0 million on the convertible debentures.

Growth initiatives

Over the next few years, a series of growth initiatives are anticipated to drive substantial expansion of the Bomboré operation. I expect that this expansion will more than offset any mining under-conciliation resulting from the greater-than-anticipated historical artisanal depletion encountered in certain near-surface, higher-grade ore zones, as observed in the 2Q2023 report.

Grid power tie-in

Orezone anticipates completing the project to link the Bomboré operation to the national grid by the end of 2023. This project, with an estimated cost of US$15-$18 million, is expected to significantly decrease the power costs associated with ROM processing.

Orezone entered into an agreement with Genser Energy Burkina S.A. to procure low-cost power from an LNG-fired power plant that Genser was set to construct. Unfortunately, Genser experienced substantial delays and was unable to deliver a functional power plant as planned. Consequently, Orezone had to terminate the agreement. Orezone is now preparing to initiate a claim against Genser through binding arbitration, seeking financial compensation for both past and projected losses.

RAP Phase II and III

The Resettlement Action Plan (or RAP) involves the establishment of four new resettlement villages (MV3, MV2, BV2, and BV1). The construction of Village MV3, comprising over 1,200 private homes and public structures, will be the first to commence. This construction is crucial as it will provide Orezone with access to mining areas outlined in the 2024 mine plan.

The commencement of construction for MV3 village was delayed by two months due to sacred ceremonies associated with the new resettlement grounds. To expedite construction progress, Orezone has initiated the engagement of additional contractors.

Phase II expansion study

Since the 2019 feasibility study, Orezone has undertaken over 150,000 meters of drilling, leading to the discovery of the near-surface P17NE deposit and extensions of other recognized higher-grade hard rock zones within the main Bomboré deposit. The successful drilling campaign in 2022 is supposed to upgrade the inferred resources of higher-grade hard rock material to measured and indicated categories, consequently paving the way for an upgraded feasibility study expected to conclude by the end of the third quarter of 2023.

Recent metallurgical test results have validated more rapid leach kinetics (reduced from 42 hours to 24 hours) compared to those in the 2019 feasibility study. The proposed flow sheet will follow the same design as in the existing plant. Firm quotations for the SAG mill have been received. Modeling of the new mineral resource estimate has been completed, while modeling of the new mineral reserve estimate is currently underway. Furthermore, Orezone has initiated preliminary discussions with its senior lender, Coris Bank, concerning financing for the Phase II expansion.

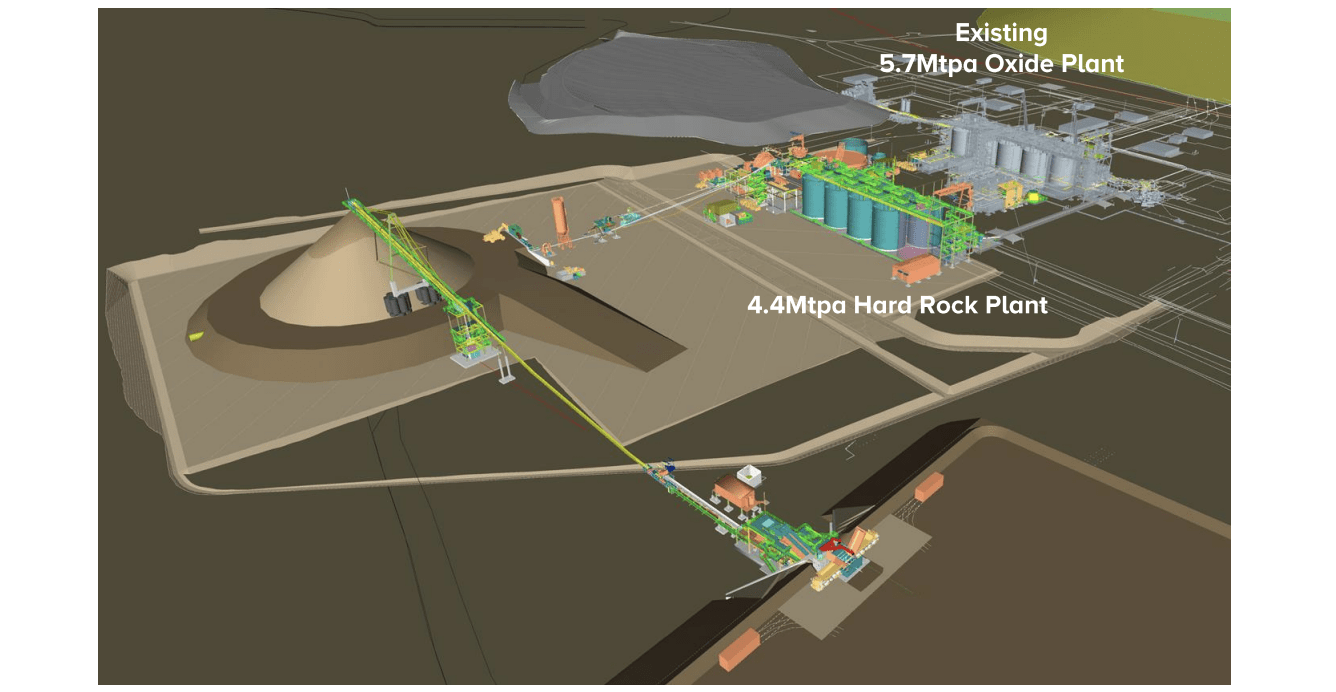

Buoyed by promising exploration results, Orezone is outlining plans to construct a new 4.4 Mtpa standalone circuit that will operate concurrently with the existing 5.7 Mtpa oxide circuit. The company aims to increase annual production from 134,000 ounces of oxide gold over the first ten years as in Phase I to 250,000 ounces of both oxide and sulfide gold in Phase II, as illustrated in Figure 6.

Fig. 6. Phase II brownfield expansion of the Bombore gold mine (Orezone)

{kind=link}

Upside and risks

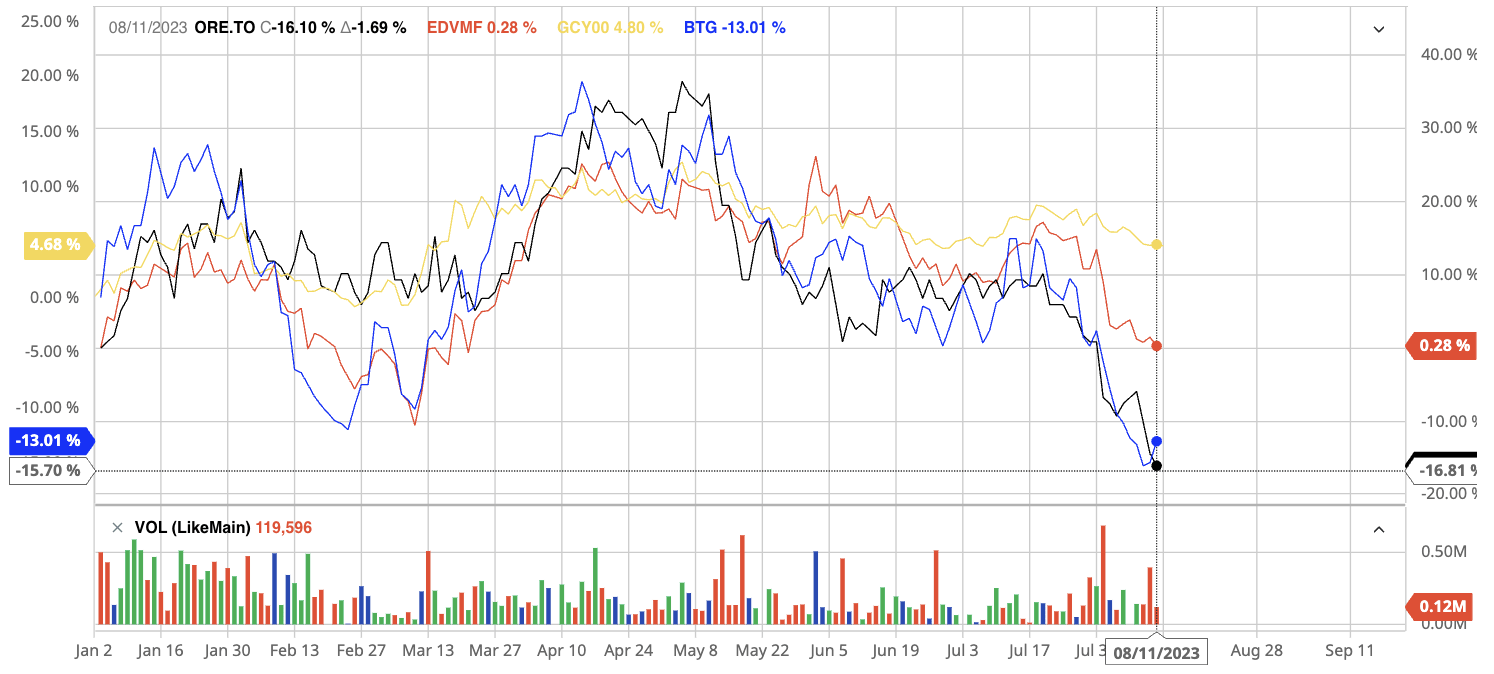

Orezone is currently valued with an EV/EBITDA multiple of 2.7X on a 2Q2023 run-rate basis, or at a P/FCF multiple of 3.2X on an adjusted last-twelve-month basis. In comparison to gold-producing peers like Endeavour Mining plc ( EDVMF ) and B2Gold Corp. ( BTG ) that also operate in West Africa, Orezone's valuation appears to be notably lower, especially when considering that Orezone has laid out a robust strategy to double its production in the upcoming years.

Fig. 7. Stock chart comparing the year-to-date performance of Orezone, B2Gold, Endeavour Mining and gold (modified from Barchart and Seeking Alpha)

{kind=link}

Referring to Figure 7, it's evident that both Orezone and its West African peers have underperformed in comparison to the 4.8% increase in the gold price since the start of 2023. Notably, both Orezone and B2Gold have experienced significant declines since July 2023. However, it's important to note that Orezone has much more production growth prospects in the foreseeable future than B2Gold.

I anticipate that a stabilization of operations at Bomboré and news flow regarding Orezone's growth initiatives in the upcoming two quarters should contribute to a potential appreciation of the share price. However, this potential for upward movement is accompanied by several risk factors.

Political stability has remained a major concern for investors interested in mining stocks operating within West Africa. Despite Orezone's impressive performance in terms of recovery factor (over 91% compared to the projected 87%) and even surpassing the nameplate plant capacity, the company might encounter new challenges during the construction of Phase II expansion. Fortunately, the management team led by Patrick Downey has established a reputation as highly capable mine builders, as evidenced by their on-time, under-budget construction of Bomboré Phase I.

Investor takeaways

The unexpected historical artisanal depletion in certain near-surface, higher-grade ore zones has indeed taken the market by surprise. Recent political instability in West Africa is a genuine cause for concern. However, the ~20% decline in Orezone's stock price since late July 2023 seems to be an exaggerated reaction.

Despite the recent setbacks, Orezone continues to be a low-cost gold producer with one of the most promising growth outlooks for the upcoming years. Therefore, I believe the next 2-3 months leading up to the 3Q2023 quarterly earnings release could present a favorable opportunity for risk-tolerant investors to acquire shares of Orezone.

For further details see:

Orezone Gold Appears Undervalued After Recent Selloff, Presenting A Buying Opportunity