ORGO - Organogenesis: Quantifying The Opportunity

Summary

- Seeking Alpha's quant ratings system provides a valuable tool for analysis of thousands of stocks.

- Underlying metrics for momentum and revisions undercut Organogenesis' strong Quant valuation and profitability metrics.

- Quant ratings alone need supplementation; the stories underlying particular stocks help to round out a decision of whether or not to invest.

- There are risks associated with healthcare microcaps in general and with Organogenesis specifically.

This is my first look at Organogenesis ( ORGO ). It manufactures and sells surgical and sports medicine products to support the healing of musculoskeletal injuries and degenerative conditions.

I have selected it as an interesting foil to use in evaluating Seeking Alpha's rich quant ratings system ("Quant"). Initially I will explain how Quant works generally for healthcare stocks, then I will focus on its application in the case of Organogenesis.

Lastly I will give an overview of Organogenesis' substantive investment merits.

Quant provides a dynamic tool crunching important metrics

How it works

Serious investors with time to spare who have not already done so can spend some interesting and instructive time learning Quant's ins and outs. It is a tool rich with data. My particular field of interest is health care stocks.

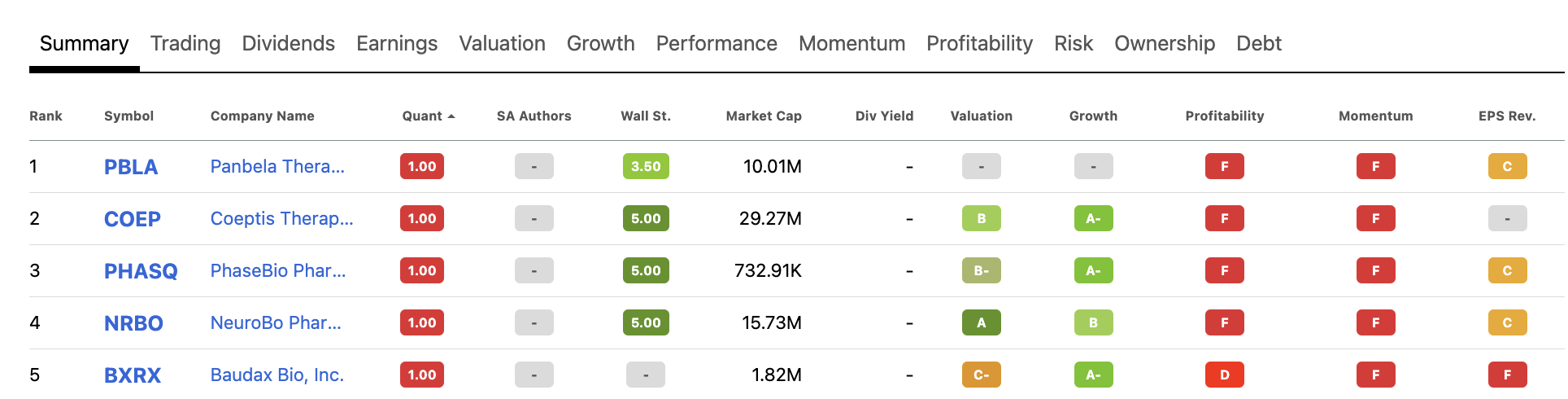

To access Quant's current (02/05/2023) universe of 1182 healthcare stocks go here . You can scroll through from the bottom five Quant rated healthcare stocks (1-5) as shown by the excerpt below:

{kind=link}

all the way down to the top two (1182-1183) below:

{kind=link}

This article refers to Organogenesis as the example for explaining how Quant works. Its 02/05/2023 rating finds it at a disreputable 138 below:

{kind=link}

Organogenesis' overall Quant rating is a shivery "Strong Sell". Wall Street Analysts and Seeking Alpha authors are more sanguine than Quant on Organogenesis. Seeking Alpha lists it as "not covered", however a 10/2022 Seeking Alpha article rated it a buy; the sole Wall Street analyst a hold. There is only one so question how significant this is. Limited or nonexistent analyst coverage is endemic in smaller healthcare stocks.

The fourth column lists Organogenesis' market cap, which as of 02/05/2022 was ~366 million; the fifth its dividend yield which is nil. The vast majority of Seeking Alpha's top healthcare Quant stocks pay no dividend. Many like Organogenesis because they lack the kind of surpluses which make dividends realistic. There are others who have plenty of resources, but also have plenty of targets for investment dollars, including their own stock.

What it grades

Focusing on Organogenesis, columns 6-10 above lists its grades for valuation, growth, profitability, momentum and revisions on 02/05/2023. We can switch views and see a different graphic here with columns for its grades now, 3 and 6 months ago. For Organogenesis' this view on 02/06/2023 is excerpted below:

seekingalpha.com

Importantly this graphic illustrates the essential dynamic nature of Quant ratings. For example of the five grades shown for Organogenesis, the only grades that have held consistent over the 6 months are its "A" for profitability and its "F" for Revisions — now (02/05/2022), three and six months ago.

Underlying metrics

Each of the five grades is generated by a computer executing an algorithm on a chunk of underlying metrics. The exact algorithm is proprietary. The metrics are available as I describe in "A+ Top Quant Rated Healthcare Stocks For Value, Growth, And Profitability" ("Top Quant").

Organogenesis' Quant system "Strong Sell" rating requires investigation

Top Quant focuses on grading metrics for value, growth, and profitability; it downplays significance of grades for momentum and revisions. Organogenesis' overall "Strong Sell" despite "A's" for value and growth, suggest that its "D-" and "F" for momentum and revisions are clearly playing key roles. Accordingly they cannot be dismissed.

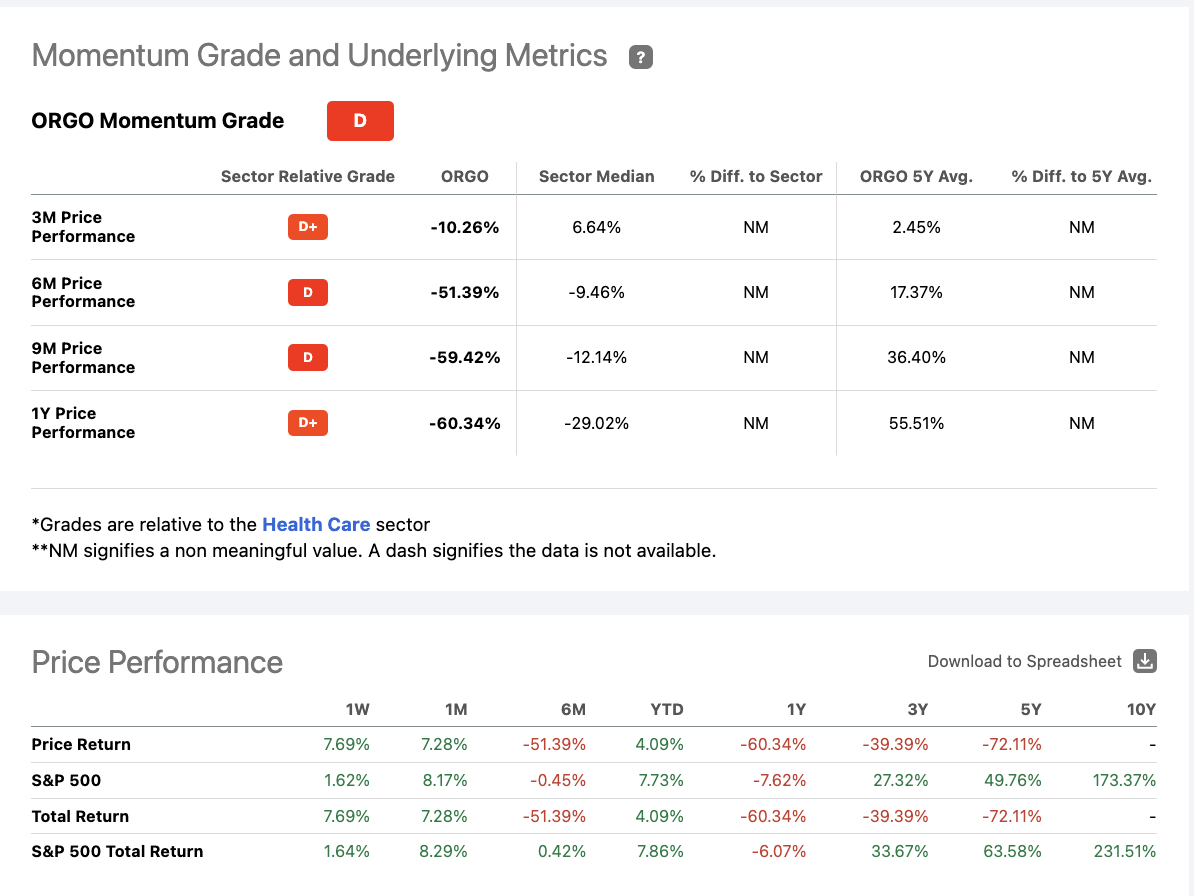

Checking into Organogenesis "D-" for Momentum takes one to a long page the top portion of which I excerpt below (note how it was D- on 02/05/2023 and is "D" on 02/06/2023 as I write):

{kind=link}

Clicking on the "?" reveals the following as a prose description of the momentum grade:

seekingalpha.com

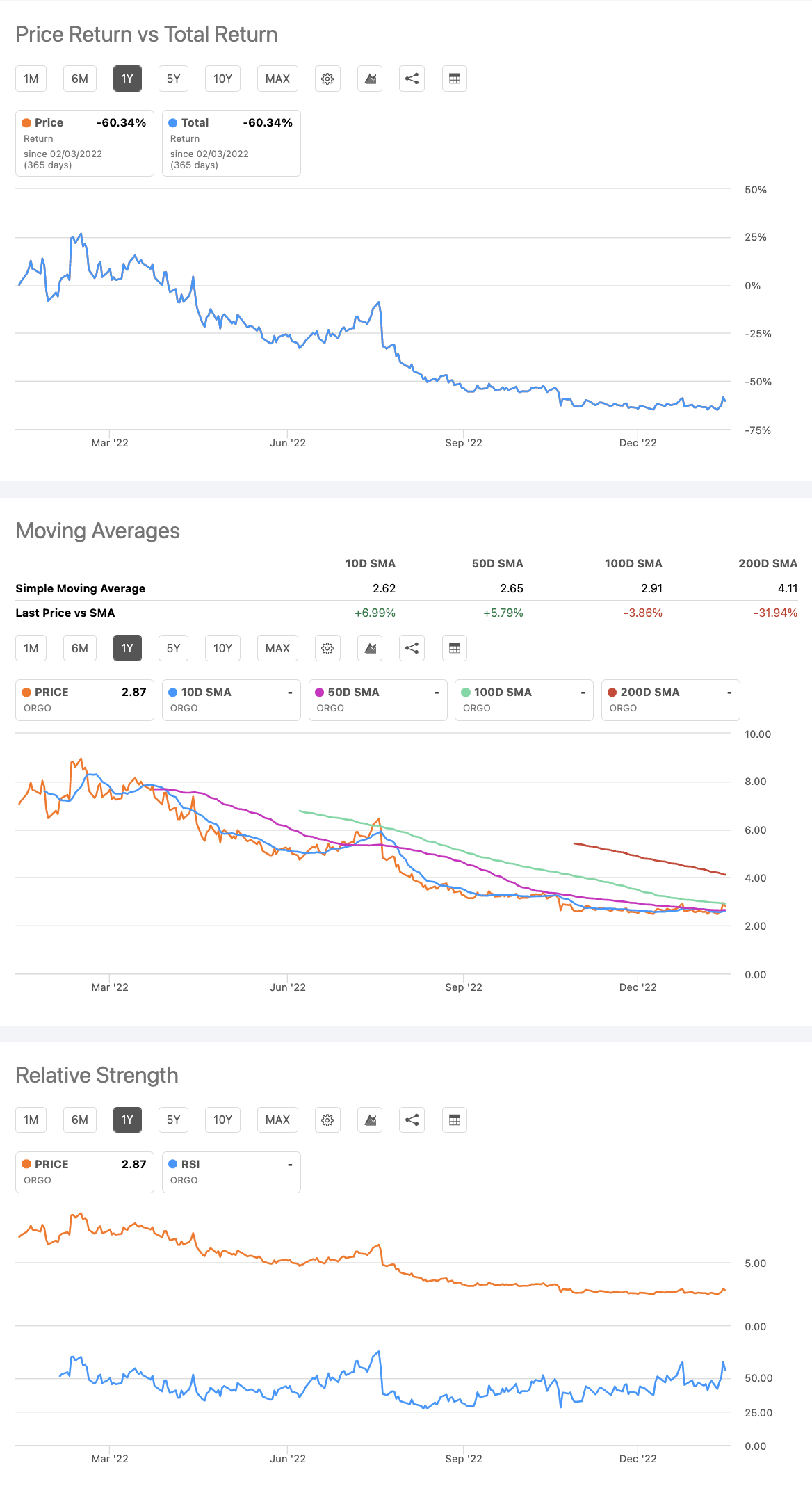

The momentum grade is straightforward. Organogenesis' "D" reflects underperformance on a wide array of obvious metrics. It includes graphics showing its underperformance on the measures listed. It also includes graphics showing the additional three metrics below:

{kind=link}

Price return vs total return, moving averages, relative strength — pick your poison, throw them into the magic Quant algorithm and out comes a nice neat momentum grade, in Organogenesis' case a "D" (on 02/06/2023).

As for its "F" revisions grade that is another story. Unlike most of the other grades, excepting only valuation, it has no explanatory "?" with a popup explanation of how it works. When you select "revisions" from the grades graphic it moves you to Seeking Alpha's "earnings revisions" page .

Once there one finds an impressive array of visual graphics. However as the current saying goes, I'm not sure there is much of a 'there' there. Remember only one analyst covers Organogenesis, although two participated in its Q3, 2022 earnings conference call (the " Call ").

The fact that a single unknown analyst's outlook on Organogenesis is negative makes the "F" in revisions considerably less scary. It's time to move on from Quant, let's check out what's going on at the company.

Organogenesis' business is facing temporary headwinds

Q3, 2022 related reports such as its earnings release (the "Release") and the Call which took place on 11/09/2022 are very much the latest available information on Organogenesis. It has no later SEC filings, nor significant press releases .

It did announce participation in the 12/08/2022 Cantor Fitzgerald Medical and Aesthetic Dermatology, Ophthalmology and Medtech Conference. It does not offer a webcast on its website so it is unavailable.

The Release advised of net revenues as follows:

-

advanced wound care products of $109.5 million, an increase of 2% from the third quarter of 2021;

-

surgical & sports medicine products of $7.3 million, an increase of 15% from the third quarter of 2021;

-

PuraPly products of $63.7 million for the third quarter of 2022, an increase of 12% from the third quarter of 2021;

-

non-PuraPly products of $53.2 million, a decrease of 6% from the third quarter of 2021.

As for expenses they included:

-

R&D expense of $9.6 million for the third quarter of 2022, compared to $9.0 million in the third quarter of 2021, an increase of $0.6 million, or 7%;

-

selling, general and administrative expenses of $79.3 million, compared to $62.4 million in the third quarter of 2021, an increase of $17.0 million, or 27%.

During the Call CFO Francisco advised this increase was driven primarily by increased sales personnel. In all its net income came in at a disappointing $0.2 million for the third quarter of 2022, compared to a net income of $12.6 million for the third quarter of 2021, a decrease of $12.4 million.

It also represented a significant falloff from its net income of $8.7 million for the second quarter of 2022. During the Call CEO Gillheeney attributed Organogenesis' issues to a combination of transient concerns:

...amniotic sales results were impacted by continued competitive pressure in the office channel, which challenged our share of voice and slowed adoption of our amniotic technologies with new customers. We also continue to see impacts on existing customer demand as a result of aggressive pricing strategies from small amniotic players, leveraging the lack of CMS published ASPs for the skin substitute products.

Organogenesis is expected to report Q4, 2022 earnings on 03/08/2023. Until then investors can look to its 2022 guidance given during the Call:

-

net revenue between $448 million and $465 million, representing a decrease of approximately 1% to 4% year-over-year, and roughly flat on an adjusted basis — 2022 net revenue guidance range assumes net revenue from advanced wound care products is flat to down 2% year-over-year;

-

GAAP net income between $12 million and $20 million, adjusted net income between $22 million and $31 million;

-

EBITDA of between $31 million and $42 million and adjusted EBITDA between $46 million and $58 million.

Investments in Organogenesis involve significant risk

Shareholders who have been with Organogenesis for very long have gotten a visceral lesson in the plentiful risks associated with microcaps in the healthcare sector. Its price chart below tells the story:

Two of the specific risks that are most telling for Organogenesis relate to competition and its reliance upon coverage and financing decisions by The Centers for Medicare and Medicaid Services ( CMS ). These risks are the ones which have contributed to its underperformance in Q3, 2022 and will continue to be in play as long as uncertainty about its ongoing regulations continues.

They are far from the only ones. It has reasonable liquidity of $108 million in cash and cash equivalents and restricted cash, compared to $114.5 million in cash and cash equivalents and restricted cash at year end 2022. However it had to "pause" ongoing work on a planned manufacturing facility in Canton Massachusetts.

The project was coming in at 40% over budget. Whether this was due to overoptimistic budgeting or simple inflation, in either case, it is disconcerting. Management has indicated that it will not impact its ability to achieve its goal of greater than 80 margins.

Conclusion

While it is always alarming to see Quant render a "Strong Sell" rating on a stock in one's portfolio, I am not overly concerned about it in the case of Organogenesis. Its (02/06/2023) "A" grades for valuation and profitability mitigate strongly against overreaction based on its Strong Sell caution.

I consider it to be a solid hold albeit one that has risks. I would certainly hesitate in committing new funds until its competitive threats as described start to ease.

For further details see:

Organogenesis: Quantifying The Opportunity