ORGO - Organogenesis: Solid Revenue Generation From A Hyper-Trading Wound Care Company

2023-07-20 11:31:58 ET

Summary

- Organogenesis is a solid player in the surgical care product market.

- Over its long existence, it has developed an important slate of core competencies.

- Small-cap biotech is a risky area, none more so than Organogenesis.

- Despite its helter-skelter trading history., Organogenesis is a worthy acquisition candidate on pullbacks.

This is my second Organogenesis article after 02/2023's " Organogenesis: Quantifying The Opportunity (Opportunity). In Opportunity, I focused on using Organogenesis as an example to assist in the understanding and use of Seeking Alpha's quant rating system.

In this article my focus is on it skittish share performance and the substantive merit of Organogenesis as an investment.

A solid core business in surgical care products undergirds Organogenesis

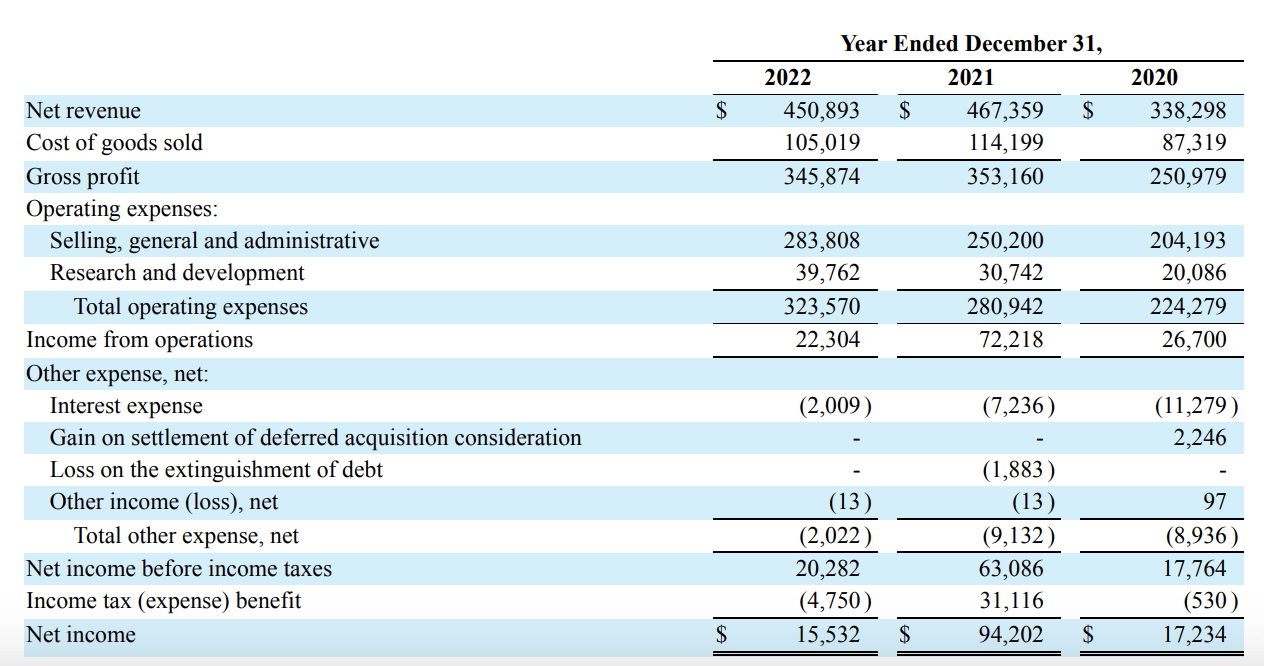

Unlike many of the small medical companies I cover, with a market cap of <$1 billion, Organogenesis has solid recurring revenues. Its results of operations chart excerpt below for years 2020-2022 from its 2023 10-K (p. 77) shows growth aggregating 38% from 2020 to 2021. Growth stalled the next year, only to show a downdraft of 4%:

{kind=link}

The analogous chart from its 2022 10-K listing its revenues from 2019 to 2020 showed growth of 30%. It attributed the growth primarily to an expanded sales staff (p. 94), similar to its explanation of the increase from 2020 to 2021.

Its 10-K reports its revenues in two groups:

- Advanced Wound Care, and

- Surgical & Sports Medicine

Advanced Wound Care is the larger of the two by a factor of 10. Surgical & Sports Medicine revenues hovered at ~$40 million until they dropped to <$30 million in 2022 (2023 10. K, p. 78).

Accordingly, I will focus on Organogenesis' Advanced Wound Care franchise. It consists of the following products:

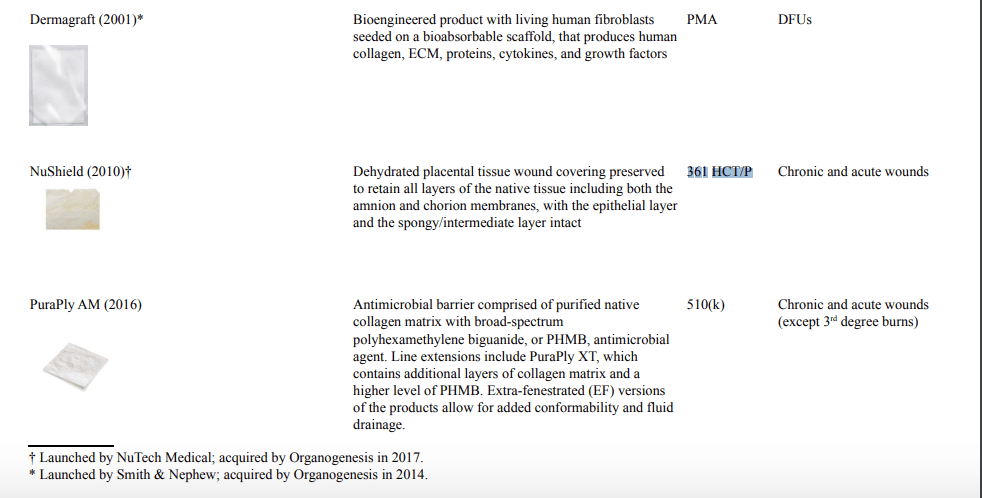

- Apligraf for the treatment of venous leg ulcers ["VLUs"] and diabetic foot ulcers ["DFUs"]

- Dermagraft for the treatment of DFUs (manufacturing currently suspended pending transition to a new manufacturing facility or engagement of a third-party manufacturer);

- PuraPly AM as an antimicrobial barrier for a broad variety of wound types and

- Affinity, Novachor, and NuShield wound coverings to address a variety of wound sizes and types.

Beyond disaggregating revenues between Advanced Wound Care and Surgical & Sports Medicine, its 10-K provides no more detailed revenue breakdowns. In its 2023 10-K Business Strategy section it notes that it is working to expand payer coverage for several products that have yet to attain "the broad commercial payer coverage enjoyed by Apligraf and Dermagraft".

The strong implication is that Apligraf and Dermagraft are its lead revenue generators. This being the case, Dermagraft's above-referenced manufacturing issues come to the fore. I can find no helpful status update on it.

Organogenesis does mention it in a Q1, 2023 conference call noting only:

We continue to focus on and invest in expanding our manufacturing capacity overall for our product portfolio and our pipeline product and specifically for developing manufacturing capacity for our Dermagraft and TransCyte products that were previously manufactured in California.

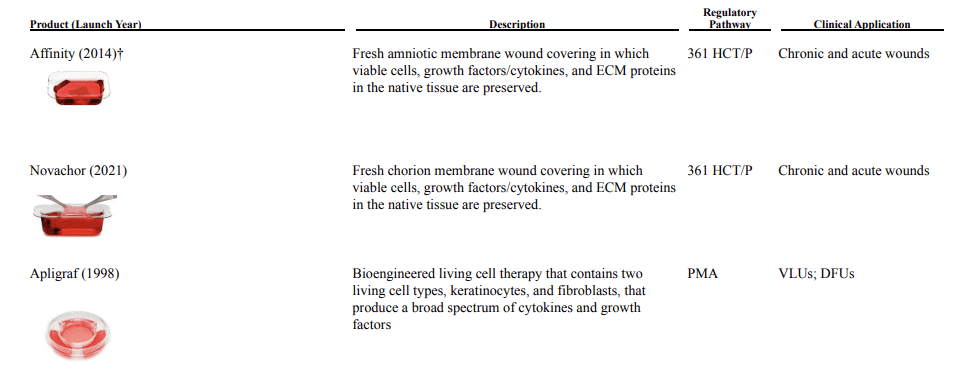

Organogenesis has productive core competencies generating its products and pipeline.

Core competencies

Organogenesis was founded back in 1985 as a technology spin-off from MIT. In its latest 10-K (pps. 21-22) it lists the following as its platform technologies: in regenerative medicine:

- Bioengineered Cultured Cellular Products;

- Collagen Biomaterial Technology Platform;

- Placental-Based Products;

- Antimicrobial Technology.

These have generated FDA approved wound care products as listed below in the table spliced from the 10-K:

seekingalpha.com (seekingalpha.com) seekingalpha.com

{kind=link}

{kind=link}

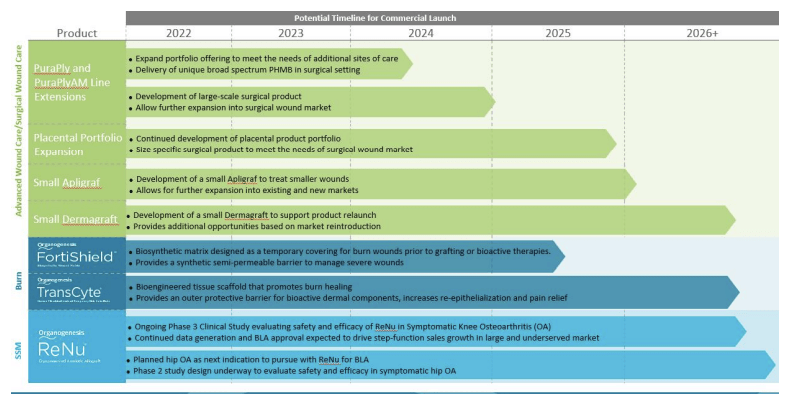

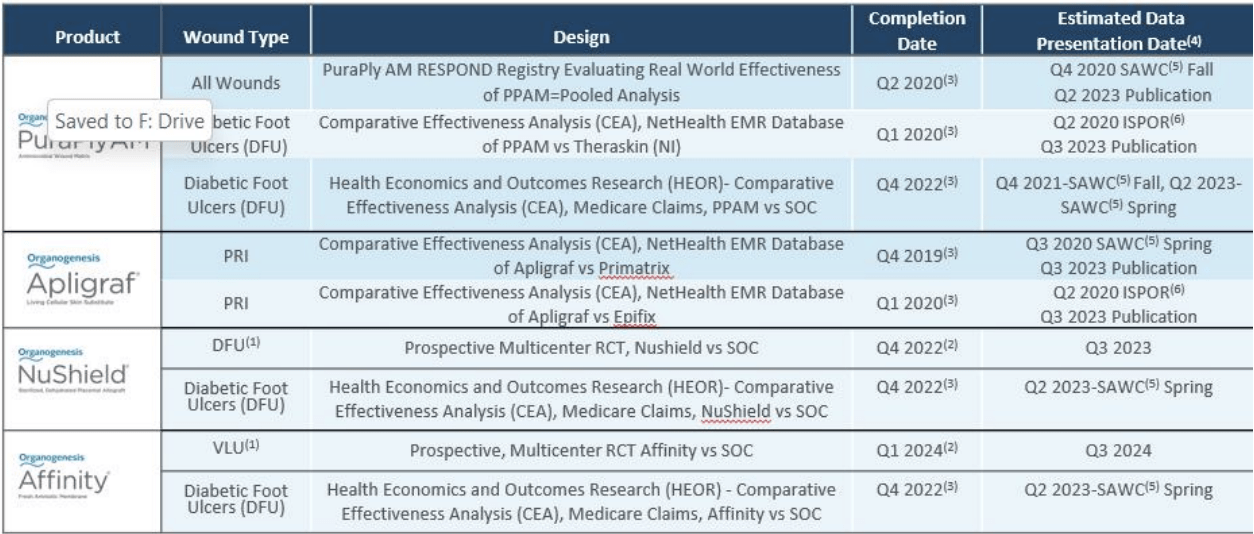

Pipeline and development

In addition to its approved products, it has a rich pipeline of products in clinical development as shown below:

{kind=link}

And it has an active research and development team working on new products and gathering clinical data as shown below:

{kind=link}

Organogenesis has devoted extensive resources over long years to build its presence and significance in the wound care arena. It has a wide array of competitors. These include the giant 3M ( MMM ) and mid-sized companies such as Smith & Nephew ( SNN ) and Integra LifeSciences (IART) along with an array of smaller companies such as Bioventus, Inc (BVS) and MiMedx Group (MDXG).

Organogenesis shares typify risk in the small-cap biotech industry.

Organogenesis' stock chart is sharp and pointed to say the least:

Its crazy upward spike on 01/09/2019 from its previous close of ~$13.44 to a mid-day high of $310.00 the next day drew the attention of Seeking Alpha's news feed with the following headline :

The wild ride with Organogenesis

The body of the article read:

Ultra-thinly traded Organogenesis (ORGO +6.8%) is a shining example of the wild ride only a biotech can deliver. On October 30, 2018, Nasdaq suspended trading in the regenerative medicine firm's shares ahead of delisting due to its failure to meet its requirement of at least 400 round lot investors. The company attended a hearing on December 13 to present its plan to address the issue. Nasdaq granted its request for continued listing of its Class A common stock until March 31 of this year while it implements its plan to increase the number of round lot holders. The trading halt was lifted at the open on January 8. Only 2,000 shares were traded at a range of $13.00 - 13.45.

Organogenesis' trading volume has thickened considerably in recent years as shown by the chart below of its share price and trading volume.

During the "price normalizes" chart, Organogenesis has traded as low as ~$1.79 on 04/26/2023 on daily volume of ~0.697 million to as high as ~$4.23 on 06/14/2023 on daily volume of 760,000. This represents an increase by a factor of ~2.36 in a period of less than 2 months.

As I write on 07/19/2023 Organogenesis is extending its bull run trading at $4.43.

Conclusion

In my opinion, Organogenesis has proven to be an unreliable repository for its shareholders' investment dollars. Its price turns on a dime based on slim news. Despite its manifest flaws I am attracted to its proven revenue-generating assets. I regard it as a buy on downdrafts.

For further details see:

Organogenesis: Solid Revenue Generation From A Hyper-Trading Wound Care Company