OGN - Organon: Big Dividend And Upside Potential

2023-07-17 08:05:00 ET

Summary

- Organon, a global healthcare company, is a buy for value and income investors due to its strong growth in biosimilars business and 5.5% dividend yield.

- Despite a 20% YoY decline in adjusted EBITDA, the company has seen constant currency product sales growth for six consecutive quarters and is paying down debt.

- Risks to Organon include higher interest rates and increased competition, but these are considered to be already factored into the current share price.

Bargains may seem like they’re hard to find, especially with the win-streak that the S&P 500 ( SPY ) has been on as of late. However, I’m continuously reminded that it’s a market for stocks rather than the stock market, considering that the rally in AI and meme stocks is happening at the expense of a sell-off in other sectors.

This includes the pharmaceutical segment, which not long ago last year was a favorite among investors for their cash-rich businesses while tech stocks were shunned. With the tables now having turned, a number of pharma stocks are now appealing again.

This brings me to Organon ( OGN ), which I last covered in February, highlighting its balance sheet discipline, growth opportunities, and well-covered dividend. Like many peers in the pharma sector, OGN is now trading close to its 52-week low, as shown below. In this article, I discuss recent business developments and why the stock is a buy for value and income.

{kind=link}

Why OGN?

Organon is a global healthcare company that was spun-off from pharmaceutical giant Merck ( MRK ) in 2021. Its portfolio includes over 60 medicines across therapeutic areas, led by women’s health and an expanding biosimilars business as well as a stable franchise of established medicines. OGN employes over 10,000 people and over the trailing 12 months, generated $6.1 billion in total revenue.

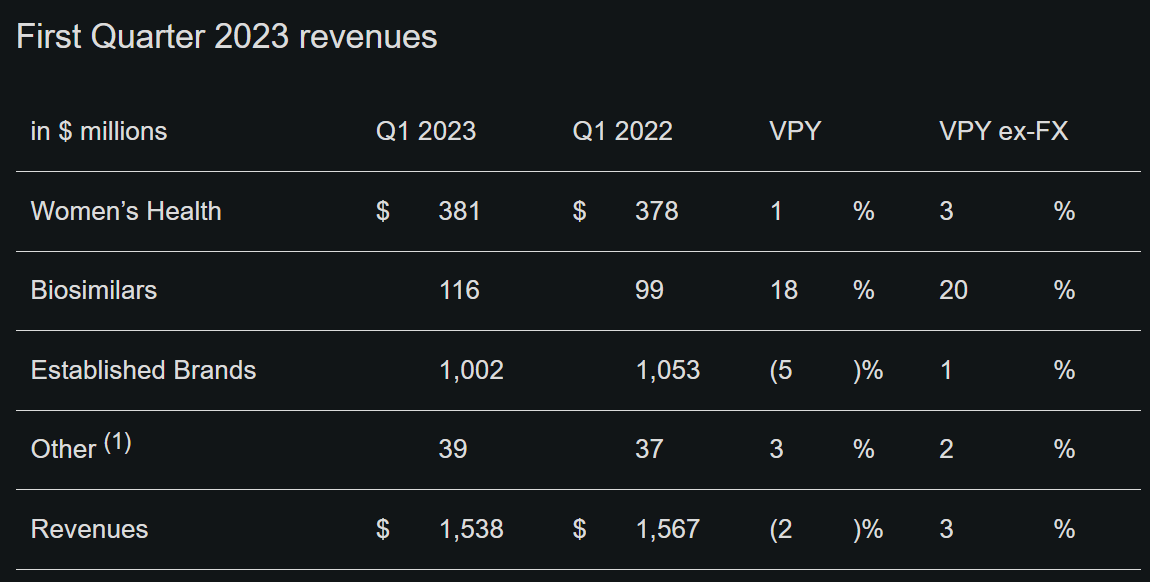

Despite what the trailing 12 month stock price movement may suggest, OGN’s business has actually grown, with Q1 marking its sixth consecutive quarter of constant currency product sales growth. All three franchises grew their top-line revenue, with biosimilars leading the pack with 20% YoY sales growth ex-currency, driven by demand growth in the U.S. and Canada. Plus, weakness in established brands in Japan was more than offset by strength in other APJ regions including China.

{kind=link}

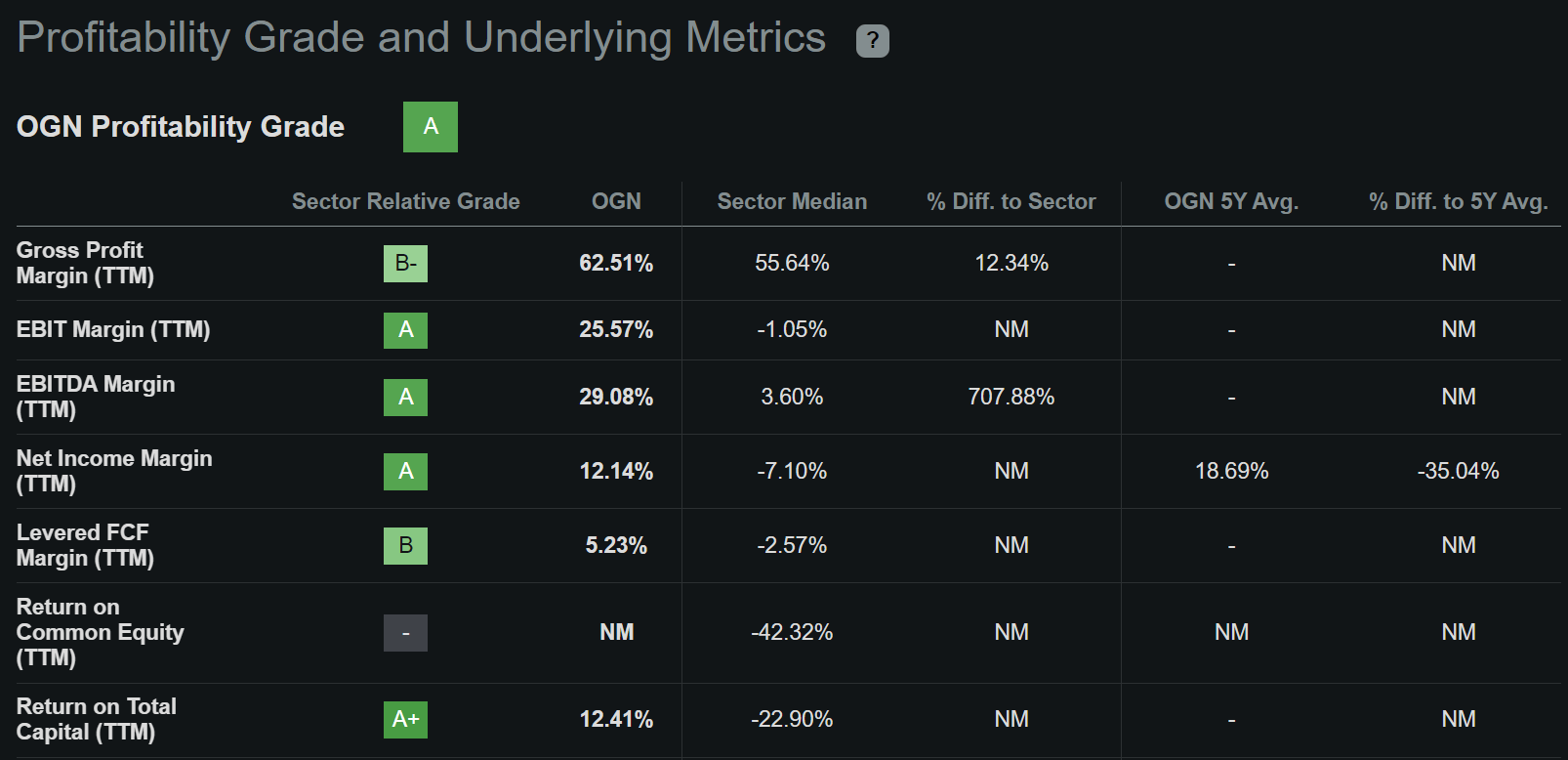

OGN saw adjusted EBITDA decline by 20% YoY due to unfavorable product mix in established brands and higher employee costs and interest expense on variable rate debt. Nonetheless, OGN still maintains plenty of pricing power, as reflected by its ‘A’ profitability grade, with strong gross, EBITDA, and net income margins, as shown below.

{kind=link}

OGN’s healthy margins also enable it to pay down debt with free cash flow. This is reflected by long-term debt declining by $422 million since the end of 2021, from $9.1 billion to $8.7 billion. While OGN’s net debt to EBITDA ratio of 4.6x appears to be high, its related to a couple of factors.

The first is due the weakening U.S. dollar, which resulted in an immediate true-up of the debt (the numerator in the aforementioned leverage ratio), since OGN carries debt in international markets. At the same time, the EBITDA (denominator in the leverage ratio) is based on the trailing 12 months, so there is a lag effect. Looking ahead, I would expect for the leverage ratio to continue to trend down, should management continue to make debt repayments.

The second factor is considering the fact that OGN has made 8 transactions since its spin-off. These acquisitions currently consume expenses due to ongoing drug developments and management expects for them to contribute to EBITDA in the medium to long-term.

Moreover, OGN’s recent biosimilar version of AbbVie’s ( ABBV ) Humira, which is a TNF blocker that was at one point the world’s #1 selling drug. OGN’s biosimilar version, called Hadlima, could continue to drive OGN’s strong growth for this segment. Hadlima has a list price of $1,038 , which is still 85% less than Humira’s list price.

Plus, management expects its prescription contraceptive, Nexplanon, to be a meaningful growth driver going forward. Growth was 6% YoY in the U.S. in the early part of the year, and the company is planning to increase supply in parts of Africa and Asia Pacific, where payers are expanding access to the product. Management believes that Nexplanon can reach $1 billion in revenue by 2025, implying strong growth.

OGN’s IVF treatments could also gain traction in the coming years, as management estimates that IVF is growing at a 5% to 10% rate annually worldwide. This is with consideration to families delaying childbirth in certain parts of the world, like Asia Pacific, with governments in Japan, Australia, Thailand, and Singapore expanding fertility access and/or providing incentives to encourage reproduction.

Meanwhile, OGN pays a well-covered 5.5% dividend yield at a 25% payout ratio. While dividend growth has been lacking, I would expect there to be growth after continued deleveraging of the balance sheet.

Risks to OGN include materially higher interest rates, which would increase interest expense. However, the recent June inflation report showed just 0.2% sequential inflation, down from the 0.4% in May, and this builds the case against interest rate hikes. Another risk is increased competition in key therapeutic areas could hamper the company’s growth estimates.

Lastly, it appears that plenty of risks have already been baked into the current share price of $20.52 with a forward PE of just 4.8. This appears to be too cheap considering that analysts expect around 6% annual EPS growth over the next 2 years.

Considering all the above, I don’t believe a PE of 6 to be out of the question in the near term, implying price target of $25.65. This could potentially result in double-digit total returns, and is more conservative than the average analyst price target of $28.88 .

Investor Takeaway

Organon trades at a PE ratio of just 4.8 and offers a 5.5% dividend yield, making it an attractive buy for value and income investors alike. The company has seen strong growth in its biosimilars business and recently launched its Humira biosimilar, Hadlima, which could drive continued growth.

Additionally, OGN is paying down debt and analysts expect around 6% EPS growth over the next two years. While OGN is not a sleep-well-at-night stock due to its high debt, OGN is trading cheaply considering the risks and could see potentially strong total returns.

For further details see:

Organon: Big Dividend And Upside Potential