OGN - Organon: It's Darkest Before The Dawn

2023-11-30 02:52:19 ET

Summary

- Organon is a global healthcare company focused on women's health, with a diverse portfolio of prescription therapies and medical devices.

- OGN stock has been on a downward trend due to declining sales and excessive debt on the balance sheet.

- Despite challenges, Organon saw product sales grow 1% and achieved stability in its Established Brands division.

- As we can see from the already 'negatively revised' dividend estimates, the 9.8% yield will be even higher in FY2024 and FY2025. The stock is too undervalued, despite its debt burden, in my view.

The Company And The Stock

Organon & Co. ( OGN ) is a global healthcare company dedicated to enhancing women's health at every stage of their lives. The company focuses on developing and delivering innovative health solutions, including a diverse portfolio of prescription therapies and medical devices within women's health, biosimilars, and established brands. With a comprehensive range of over 60 medicines and products spanning various therapeutic areas, Organon distributes its offerings through multiple channels, such as drug wholesalers, retailers, hospitals, government agencies, and managed healthcare providers. Operating 6 manufacturing facilities worldwide, located in Belgium, Brazil, Indonesia, Mexico, the Netherlands, and the United Kingdom, Organon is committed to improving healthcare outcomes for women globally.

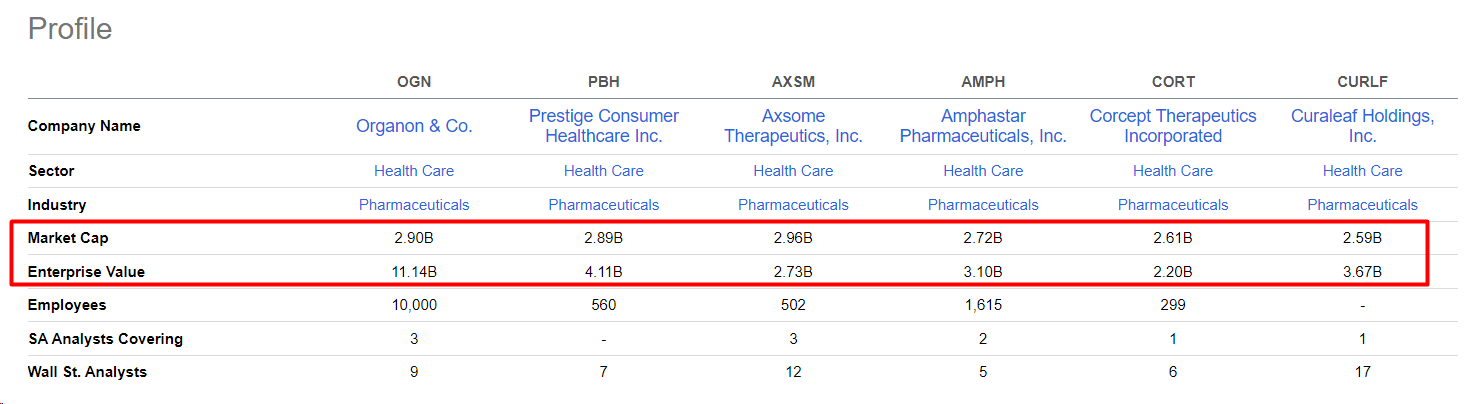

In 2020, Merck spun off Organon as an independent company, completing the process in June 2021 . The OGN share has been on a downward trend from the beginning of its independence and continues to fall due to declining sales and excessive debt on the balance sheet (the market capitalization today is only ~26.24% of the overall enterprise value, which is not normal among peers).

{kind=link}

As a significant portion of the debt was floating rate (tied to EURIBOR or SOFR), the fastest rise in Fed rates in decades increased the company's credit risks - hence the sharp drop in market capitalization (-59% YTD), in my view:

{kind=link}

{kind=link}

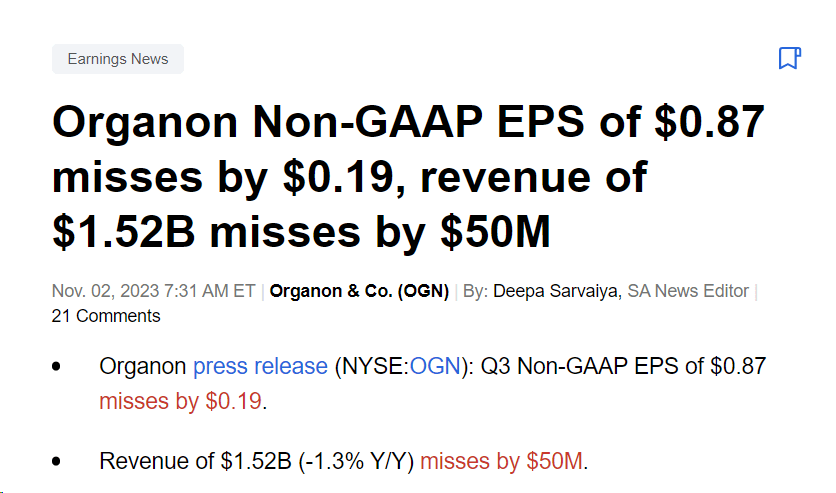

On the day the Q3 FY2023 results were published (at the beginning of November 2023), the stock fell sharply by 10.51% , then lost a further 12.8%, and is now trading almost 22% lower than before that earnings. What was in that report?

In Q3 2023 , Organon faced challenges from external factors affecting its business. The persisting strength of the U.S. dollar, a challenging economic and policy environment in China, and a slower-than-expected biosimilars market for Humira impacted the company. Despite these challenges, product sales grew 1% at constant currency, marking the eighth consecutive quarter of product growth.

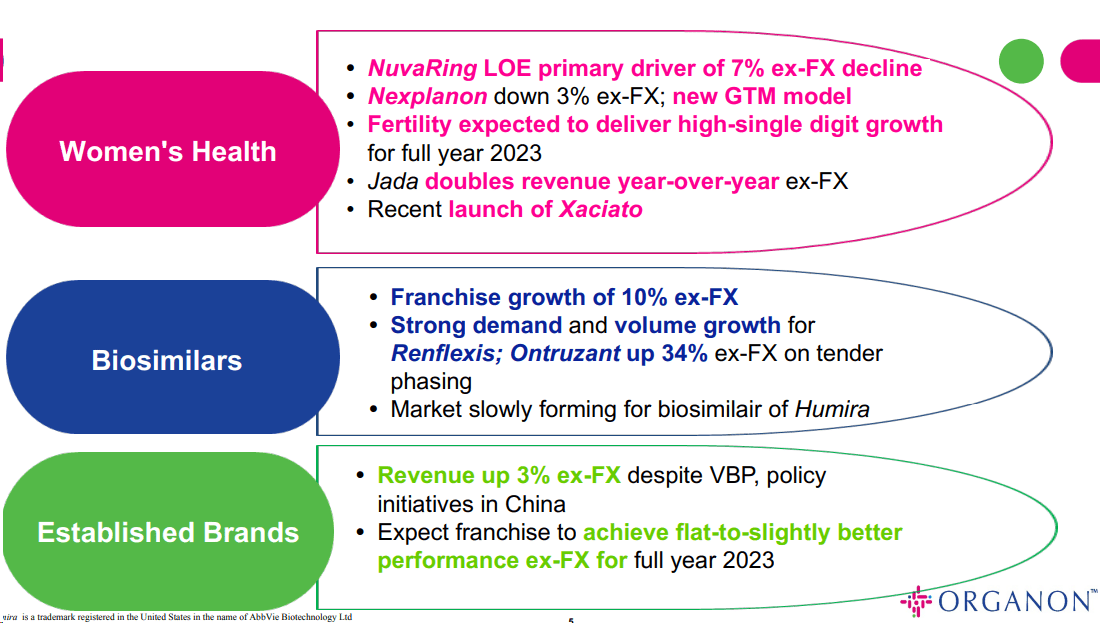

Total revenue, including lower-margin product sales to Merck, decreased by 1% at constant currency compared to the prior year. Women's Health declined 7%, Biosimilars grew 10%, and Established Brands, representing nearly 2/3 of the business, grew 3%.

{kind=link}

In the Women's Health segment, Nexplanon experienced a 3% decline in the quarter, prompting strategic decisions to facilitate growth in 2024. These decisions included adjustments to the U.S. go-to-market model and restrained participation in the annual Mexico tender. Meanwhile, the fertility business in China exhibited signs of recovery after a slower third quarter. In the Biosimilars business, the U.S. launch of Hadlima faced a slower market formation than expected. However, the company underscored its commitment to delivering economic benefits to patients and highlighted Hadlima's product attributes that position it favorably in the market. Established Brands showcased stability, achieving 1% growth year-to-date on a constant currency basis. This OGN's division played a crucial role in offsetting overall underperformance, with better manufacturing, pricing strategies, and the durability of brands contributing to its strong performance.

OGN's consolidated adjusted EBITDA was $447 million, with a 29.4% margin, and adjusted diluted EPS was $0.87, missing consensus EPS by 17.9%:

{kind=link}

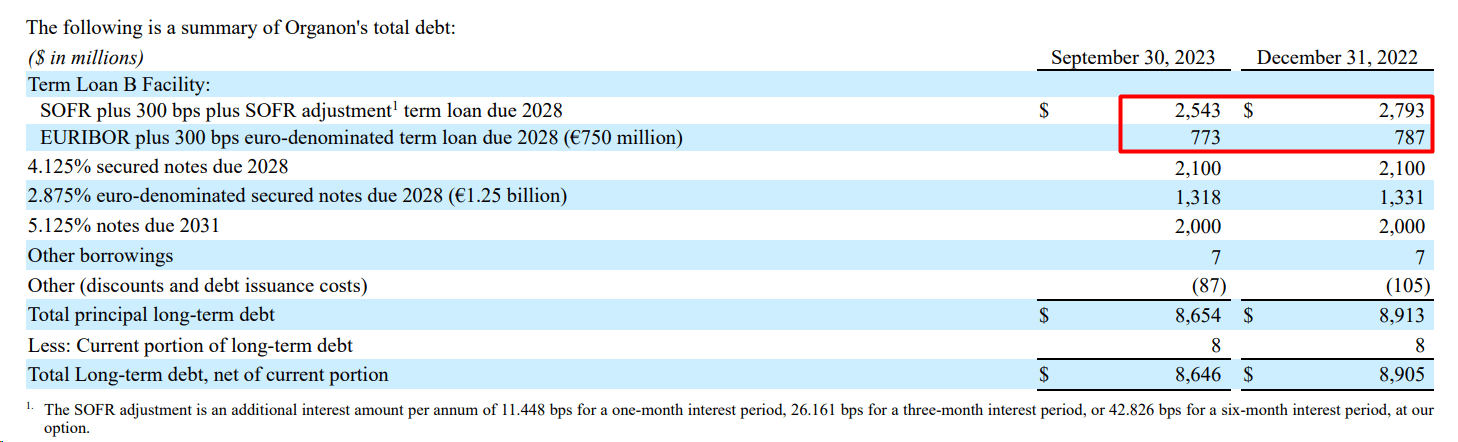

It looks like the company still faces challenges regarding its significant debt position, standing at over $8.6 billion, which may impact its ability to generate substantial free cash flow for debt reduction. Although FCF is growing again on a TTM basis after last year's decline, the picture is still frightening in my opinion:

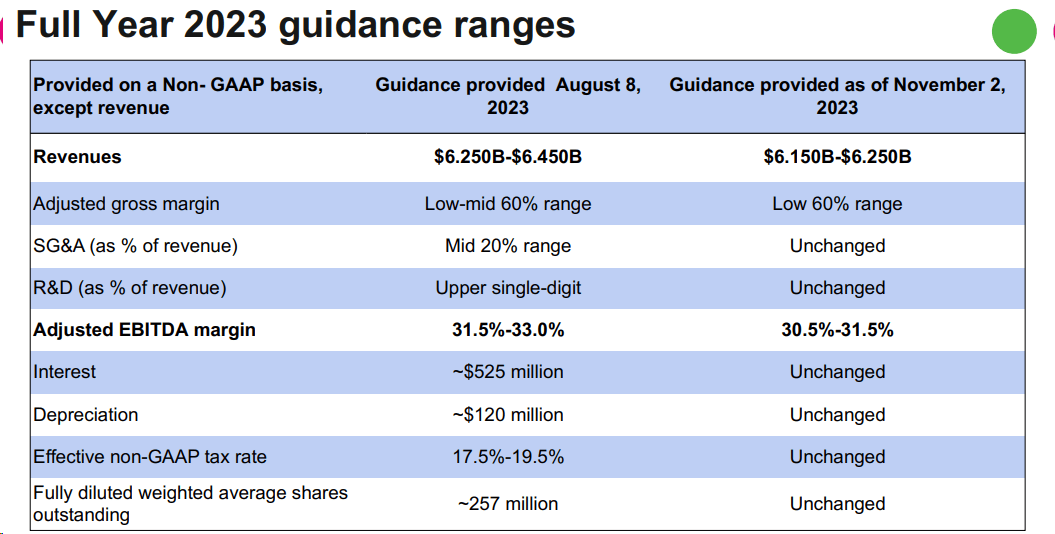

Also important to note is that OGN lowered its guidance for FY2023, changing revenue growth and margin expectations:

{kind=link}

One significant factor that contributed to the sales guidance revision was the persisting strength of the U.S. dollar, which harmed the company's financials. Additionally, the company faced challenges in navigating a complex economic and policy environment in China, affecting its operations in that region. The biosimilars market for Humira, particularly the launch of Hadlima in the U.S., experienced slower market formation than anticipated. Changes in the Women's Health segment, particularly with Nexplanon, also played a role, with strategic decisions made to position the product for future growth in FY2024. Other operational factors, such as adjustments to the go-to-market model for Nexplanon and limited participation in the annual Mexico tender, influenced the revised guidance. However, the management highlighted various headwinds as transient, expressing confidence in overcoming challenges and aiming for mid-single-digit revenue growth over the medium term.

Concerning China, Organon's management said during the earnings call that its focus is on transitioning business to the retail sector after the volume-based procurement process and expressed confidence in overcoming disruptions caused by policy changes.

Regarding capital allocation, OGN expects improvements in FCF in 2024, with an emphasis on managing costs tightly and achieving a balance between growth investments and leverage reduction.

Judging by the words of the management, OGN is set to show a recovery dynamic in the next couple of years. However, the level of debt is a major cause for concern. In my opinion, we have to look at the valuation of the company before we can draw conclusions about its attractiveness.

Organon's Valuation

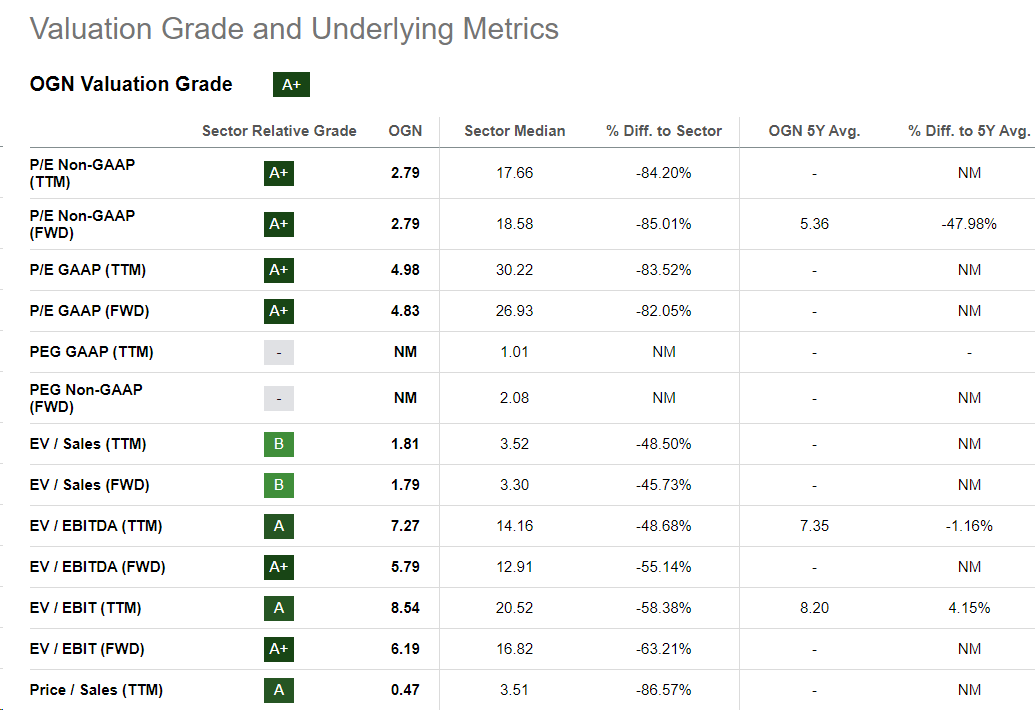

According to Seeking Alpha's Quant System , OGN is one of the cheapest healthcare stocks out there with a forwarding P/E of 2.8x and an FWD EV/EBITDA of 5.8x, which are 85% and 55% lower than the sector's median figures, respectively:

{kind=link}

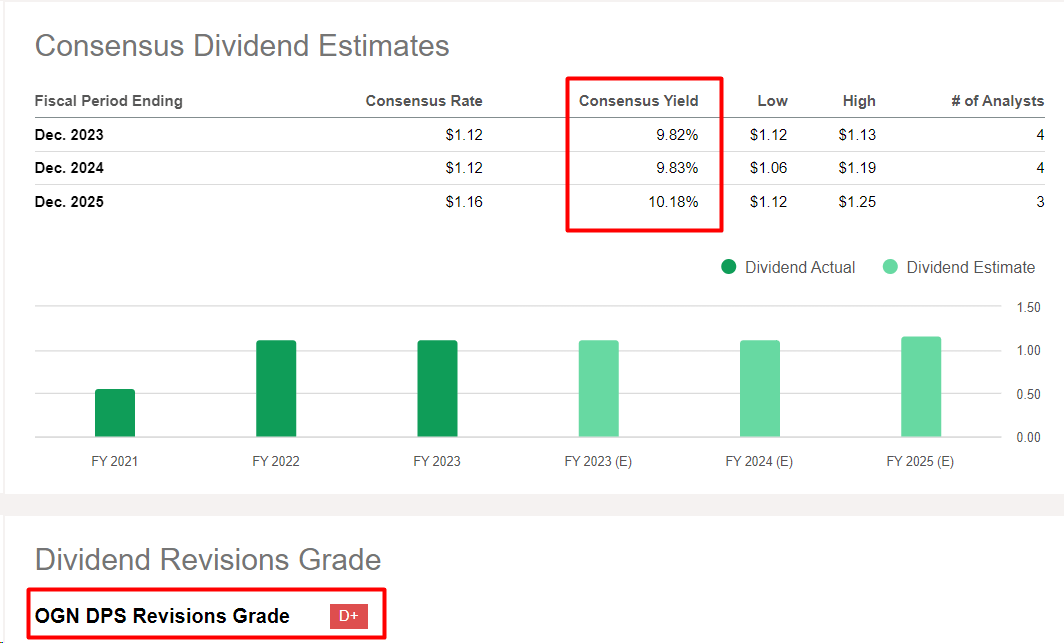

Moreover, despite the enormous debt on which interest must be paid, Organon does not forget to pay dividends, the yield of which recently reached 9.8% - the highest in Organon's public history:

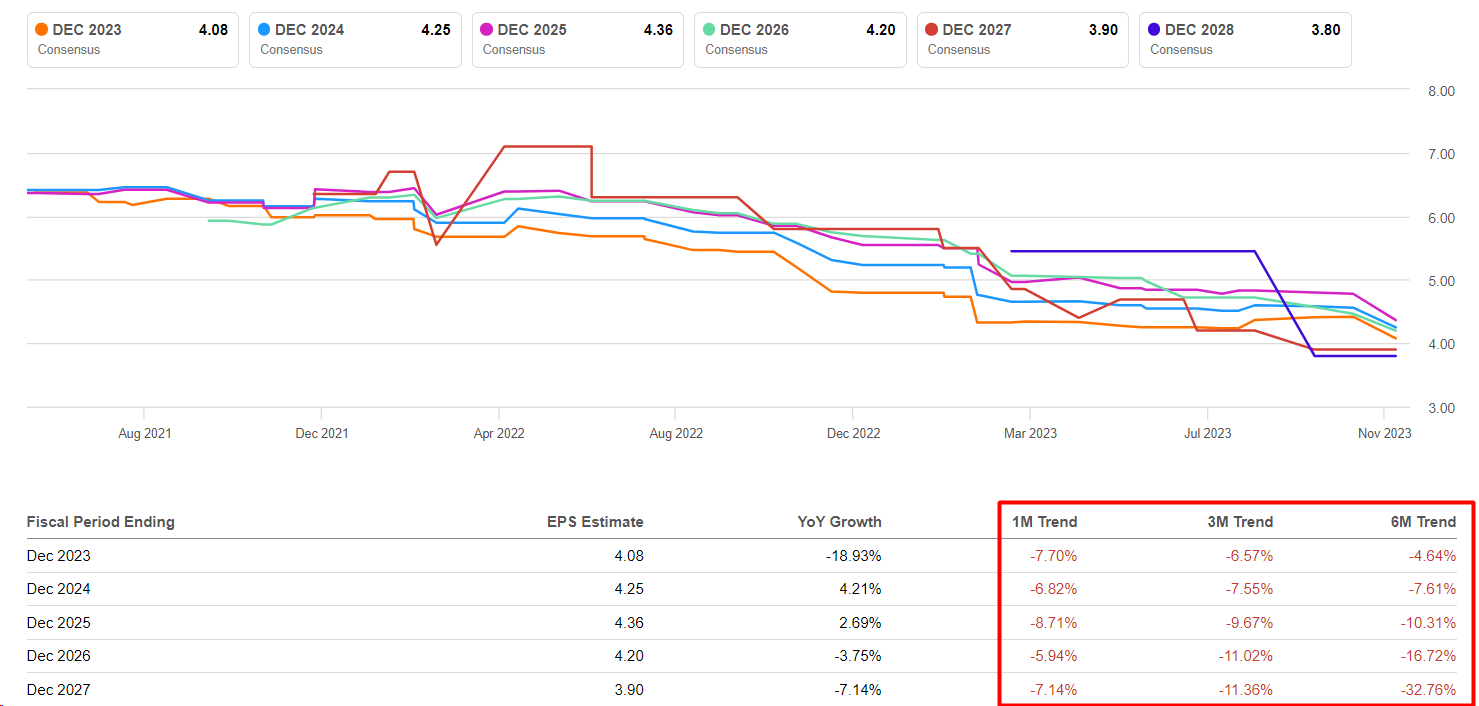

If we look at the history of OGN's earnings estimates, we see a plethora of downward revisions , the latest of which came after the terrible Q3 EPS miss:

{kind=link}

According to Seeking Alpha, OGN's dividend payout estimates have also been revised downwards in the last 90 days. However, as we can see from the already 'negatively revised' dividend estimates, the 9.8% yield will be even higher in FY2024 and FY2025:

{kind=link}

If we take a look at the payout ratio we'll see that it's constantly growing, which means that a larger proportion of a company's earnings is being used to pay dividends to shareholders. A continuously increasing payout ratio should be a cause for caution, in theory.

Therefore, I do not expect OGN to increase the dividend in the future more than the Street expects now. However, the current payout ratio of 50% makes today's yield quite sustainable, in my opinion.

The Bottom Line

Investing in Organon carries inherent risks, typical of the pharmaceutical industry. Regulatory uncertainties pose a substantial threat, as the company's products are subject to rigorous approval processes. Furthermore, the competitive nature of the pharmaceutical sector, potential pipeline setbacks, and the risk of litigation, including patent disputes and product liability claims, can significantly impact Organon's financial stability. Additionally, dependency on a few key products, the expiration of patents, and supply chain disruptions can pose challenges.

Also, the high debt burden raises concerns. If Organon faces difficulties in servicing its debt obligations, it may lead to credit rating downgrades, higher borrowing costs, and could even result in default.

So investors should be wary of these factors, and conduct thorough due diligence, before buying OGN stock's heavy dip.

Despite the existing risks, however, I believe that OGN is now fairly close to bottoming out - this conclusion is particularly obvious to me given the still relatively modest payout ratio and the extremely high and steady dividend yield of 9.8%. As for the company's debt, there is indeed a problem. But if we factor in a possible interest rate cut in 2024, interest payments are likely to fall. And EBIT already exceeds interest expenses by a factor of more than two, which looks sufficient in Organon's case.

I think it's a matter of time before OGN stock turns back to $15/sh.

So I issue a 'Buy' rating this time around.

Thanks for reading!

For further details see:

Organon: It's Darkest Before The Dawn