OGN - Organon: Poor Q3 Earnings Make Bear Case But Dividend Is Saving Grace

2023-11-07 13:04:38 ET

Summary

- Organon & Co. reported its Q3 earnings, last week, which revealed underperformance in its Women's Health division and struggles in its biosimilars division.

- The company's debt position remains high, with net debt standing at over $8 billion.

- Despite challenges, Organon continues to offer a generous dividend yield of ~9%, which may keep investors interested.

- Downgraded FY23 revenues guidance is for ~$6.2bn, with net earnings likely to fall under $1bn.

- Organon is failing to show Women's Health and Biosimilars can ultimately replace long term decline of Established Brands. This is challenging, but for now, the dividend is the saving grace.

Investment Overview

Organon & Co. (OGN), formed via Pharma giant Merck & Co.'s (MRK) spinout of its Established Brands, Women's Health and Biosimilars divisions, announced its Q3 earnings on Thursday, November 2.

I covered Organon's Q2 earnings in a deep dive note for Seeking Alpha in August. I gave the stock a "Hold" recommendation, outlining the dilemma investors/shareholders faced as follows:

The company's FY23 revenue guidance is for $6.25bn - $6.45bn, which is higher than its current market valuation of $5.9bn. This is rare for the pharmaceutical industry - amongst the 15 largest Pharma companies by market cap, the average price to sales ("P/S") ratio is ~7x. Organon is profitable, too - the company expects to generate $1bn of free cash flow before one-time charges this year - and pays a handsome dividend of $0.28 per quarter, which currently provides a yield of nearly 5%.

The key question for investors to consider is whether Organon management can generate sufficient growth from its Women's Health and Biosimilars division to offset the slowly declining sales of its established brands divisions, whilst paying down debt. If it can, then its modest market cap valuation is almost certain to rise significantly reflecting a growing business, but if it cannot, the valuation will become increasingly tied to the shrinking Established brands division, and will steadily erode.

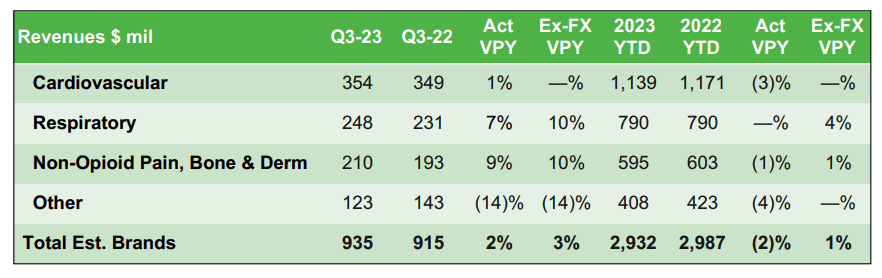

After Q3 earnings were announced last week, it's possible we now know the answer to the question I raised in August. In Q3, revenues from the Women's Health division shrank, falling from $454m in Q3 2022, to $418m, while the biosimilars division revenues rose ever so slightly, from $129m in the prior year period, to $142m in Q3 2023. Revenues from the established brands division actually held firm, showing 2% growth to reach $935m in Q3 2023, but this division is not intended for, and cannot be relied upon to support long-term growth.

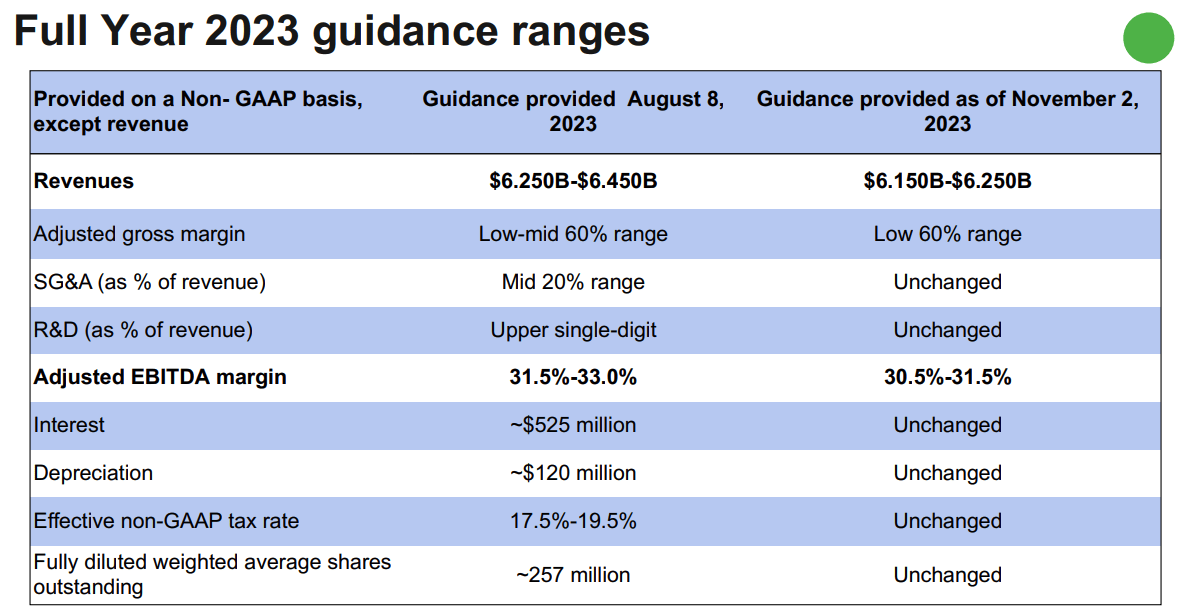

In short, this was a poor quarter for Organon and its stock price was punished, dropping from ~$15, to ~$13 after earnings were announced. Total revenues were $1.52bn, less than in Q1 and Q2 this year, and down ~1% year-on-year, also. Adjusted EBITDA fell by 18%, to $447m, and adjusted earnings per share ("EPS") was $0.87, down from $1.32 one year ago. Management lowered its FY23 guidance to $61.5-$6.25bn, and narrowed its adjusted EBITDA margin guidance to 30.5%-31.5%.

Women's Health Underperforms, But Management Insists It's Temporary

In its Q3 quarterly report/ 10Q submission Organon describes itself as "a global health care company with a focus on improving the health of women throughout their lives", which indicates where the company's priorities lie.

In total, however, the company reveals it "has a portfolio of more than 60 medicines and products across a range of therapeutic areas", and six manufacturing facilities, located in Belgium, Brazil, Indonesia, Mexico, the Netherlands and the United Kingdom.

{kind=link}

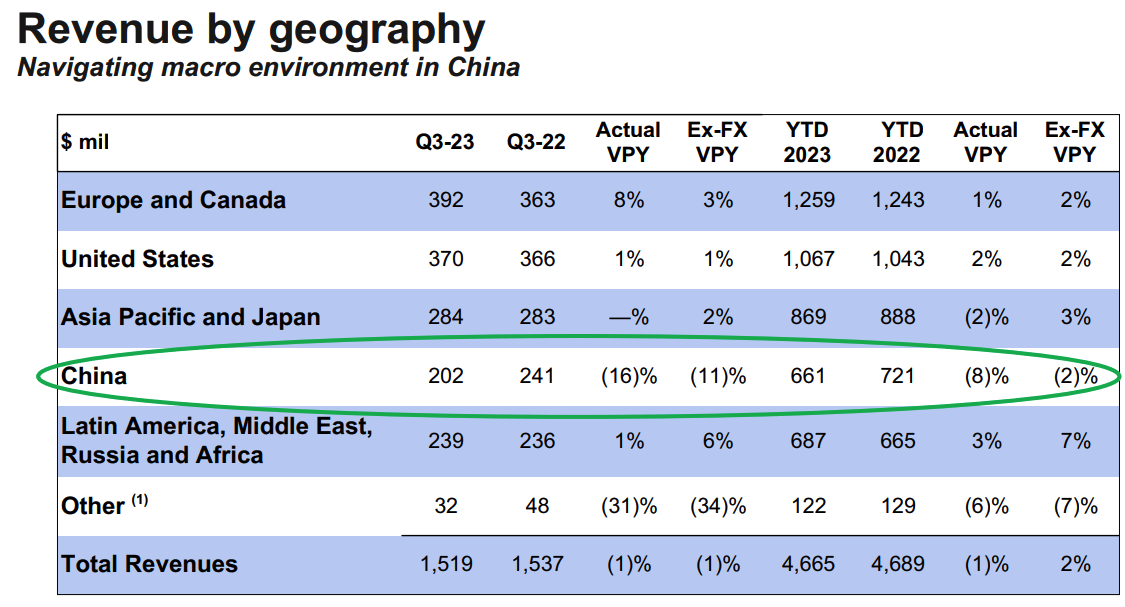

As we can see above, Organon sells its products across geographically diverse locations, and it is easy to pinpoint where the company underperformed last quarter - in China, where revenues fell 16% year-on-year, to $202m, a figure which accounts for ~13% of all Q3 revenues.

{kind=link}

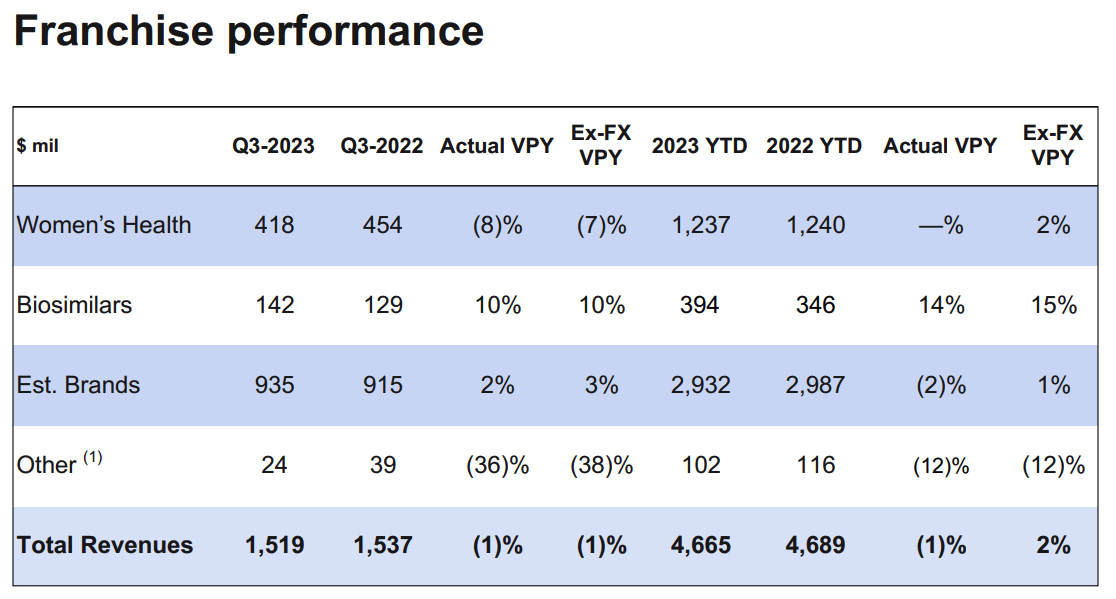

In its Q3 earnings presentation , Organon breaks down revenues by division, as shown above. Now we can see that the Women's Health division was largely responsible for underperformance in Q3, its revenues slipping from $454m to $418m.

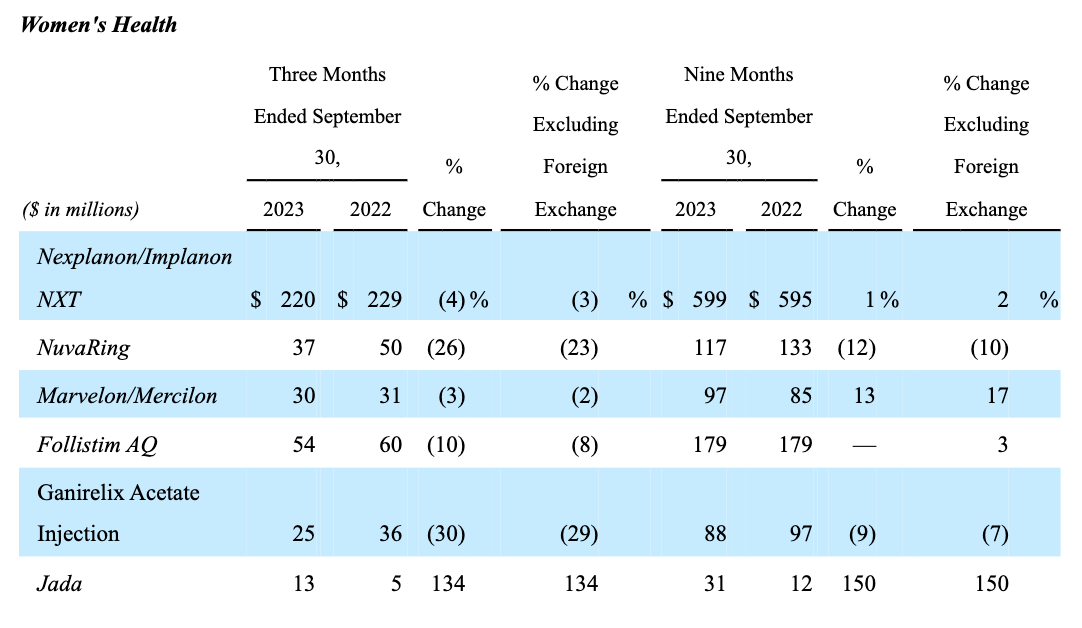

There are a couple of reasons for the division's underperformance, according to management. The first is that NuvaRing, a vaginal ring used for birth control, lost its patent protection this year - according to management (speaking on the company's Q3 earnings call ), there are already five generic versions of NuvaRing on the market. NuvaRing earned $133m across the first nine months of 2022, against $117m across the same period in 2023, and in Q3, NuvaRing revenues fell 26%, from $50m to $37m. The likelihood is that revenues will continue to erode at that rate going forward, as generics impact pricing and volume.

{kind=link}

Elsewhere across Organon's flagship division, there were more signs of underperformance, as we can see above, with sales of Nexplanon, another form of birth control, falling by 4% in Q3, to $220m, although across the 9-month period, a slight uplift can be observed. Sales of Marvelon/Mercilon, fertility treatments Follistim, and Ganirelix also fell, on account, according to Organon CEO Kevin Ali, of "the Chinese government's ongoing review of healthcare practices, which commanded significant physician attention".

Ali then suggested (in relation to China) that "this is a transient issue impacting the entire industry", before adding:

We anticipate a very strong fourth quarter, driven by identifiable market tailwinds in China as well as the onboarding of a large new customer win in the U.S.

Biosimilars Grows, But More Expected From Hadlima Launch

As shown above, Organon's Biosimilars division still only makes a small, albeit growing contribution to the company's overall revenues - accounting for ~8.5% of revenues in 2023 year-to-date, but ~9.5% in Q3 alone.

Renflexis, Ontruzant and Brenzys are biosimilars for autoimmune conditions, breast cancer therapy trastuzumab, and plaque psoriasis respectively, while Aybintio is a biosimilar for Bevacizumab - marketed and sold by Roche (RHHBY) as Avastin. Renflexis led the way in Q3, generating $69m of revenues, followed by Ontruzant, with $40m of revenues. Both showed solid year-on-year growth, although Brenzys sales fell year-on-year, to just $13m, from $24m in the prior year period, and Aybintio sales grew from $10m to $12m.

Arguably the biggest disappointment in this division was Hadlima, however, a biosimilar version of AbbVie's patent expired autoimmune megablockbuster (over $20bn revenues in 2022). Hadlima was launched in the US in July, but picked up just $2m of revenues in Q3, and $20m across the year-to-date, with $18m generated internationally, where Humira has been off-patent since 2021.

During the Q3 earnings call, CEO Ali told investors:

At an 85% discount, we priced Hadlima to enable expanded access and to bring the economic benefits of biosimilars directly to the patient. We've emphasized that's where we believe we can offer the highest value to patients. We have focused our commercial efforts on payers who want to bring lower net costs to patients. We estimate that together those plans represent about 40% of the covered lives in the US.

While not as rapidly as we may have hoped for, we're having success. Among the July cohorts of entrants, we're out prescribing our next closest competitor by a factor of over 3x. We're winning in both the commercial and managed Medicaid space across the competitive set, and we're rapidly closing in on the gap on Amgen's AMJEVITA, despite their six-month lead in the market.

With as many as eight Humira biosimilars expected to be on the market by the end of this year, and the original itself capturing over $9bn of revenues year-to-date, this is a crowded market, and Organon is not the only company offering its biosimilar at an 85% discount. As promising a field as biosimilars may be, it remains unproven as a reliable source of revenues for a company as large as Organon.

How Long Can Established Brands Prop Up Organon Business?

As we can see below, the strong performance of the Established Brands division saved Organon from an even worse Q3 performance after problems in China, within the Women's Health division, and the struggles of the biosimilar division to make meaningful sales.

{kind=link}

If we look at the 9-month performance in 2023, we can see that revenues are slipping, down 2% when compared to the equivalent period in 2022 - although FX adjusted, actual growth was ~1%. Ultimately, declining revenues are only to be expected. After all, if parent company Merck had believed any of the assets in this division had genuine growth potential, they would likely not have been part of the spin-out.

Organon management has put the strong performance of Established Brands in 2023 down to better manufacturing, stemming price erosion, an "entrepreneurial focus", and the "durability and diversity" of brands. That may be praiseworthy, but the reality is that drugs age rapidly in modern markets, which are fiercely contested, as new drugs command the highest prices and have the widest moat, protected by patents from competitors.

Organon may be effectively fighting the depreciation of these assets today, but doubtless investors and shareholders of Organon would rather have seen strong performance from biosimilars or Women's Health. This is summed up by comments made by Organon's Chief Financial Officer ("CFO") on the Q3 earnings call:

We are lowering our estimate of potential price erosion to $90 million to $100 million, down from $100 million to $150 million, an improvement from the bridge that we showed you last quarter. Here, we are seeing the momentum of our Established Brands portfolio being able to manage price erosion better-than-expected across several markets.

We have lowered our outlook for volume growth for the year and that underpins our revision to the revenue guidance. We have lowered our range to $370 million to $400 million or about 6% year-on-year growth at the midpoint, down from the 9% we were forecasting last quarter, as a result of changes we have made to our go-to-market model for Nexplanon, a slower-than-expected uptake of Hadlima and macroeconomic and policy headwinds in China.

Organon's success was supposed to be built around Women's Health and Biosimilars gradually replacing falling revenues within Established Brands. Instead, it seems the two newer divisions are struggling, while the old war horse continues to do most of the heavy lifting.

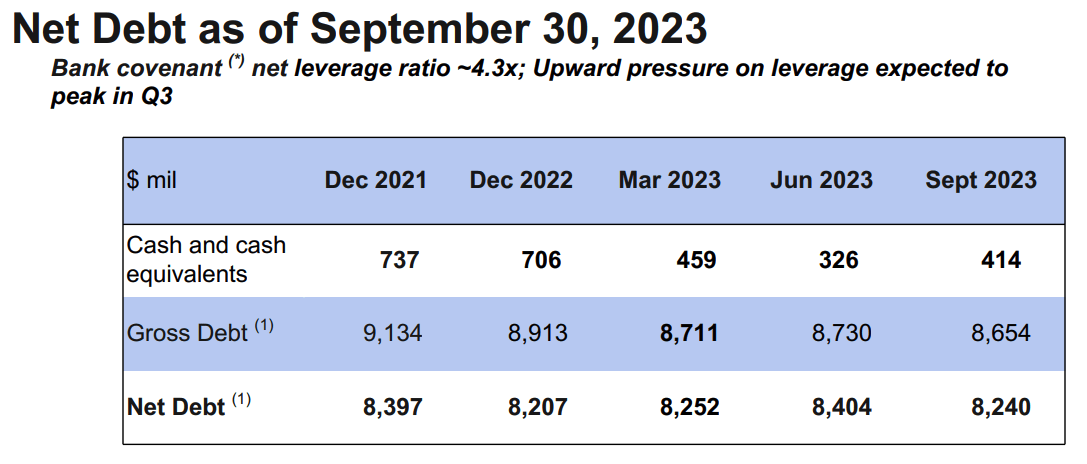

Organon's Unenviable Debt Position

Before fully completing its spin-out from Merck, Organon paid its parent a final parting gift, in the form of a tax-free dividend worth $8bn, meaning Organon began life as a listed entity in May 2021, with ~$9bn of debt. To have given its spin-out at least a fighting chance of making a good start to life, you could be forgiven for thinking Merck should have been paying Organon such a sum, rather than vice versa.

{kind=link}

As we can see above, Organon's debt position looks downright ugly, with net debt having been barely reduced since the end of 2021, and currently still standing at over $8bn. When the idea of saddling Organon with so much debt was first conceived, it may have seemed wise given interest rates were at historically low levels, but they have rapidly increased, and Organon's ability to generate masses of free cash flow to pay down its debt is limited.

{kind=link}

As we can see above FY23 guidance is now for $6.2bn at the midpoint, and if we do the math, Organon looks likely to generate ~$1bn in net profit, similar to the $917m generated in 2022. Debt therefore stands at >8x net earnings, and there is no guarantee, given management has not provided much in the way of long-term guidance, that the company will keep generating over $1bn per annum in profits.

Concluding Thoughts - Not All Doom and Gloom For Investors, But Significant Challenges Ahead

As I mentioned at the beginning of this note, Organon had, by most measures, a poor quarter, missing analyst's expectations on normalised EPS, adjusted EPS, and revenues, and its share price has been rightly punished - it is now down 55% year-to-date, and the company is valued at $3.2bn.

When Organon first began to trade on June 3, 2021, at a share price of ~$37, the investment opportunity was based on the share price being heavily discounted, precisely because of the difficult challenges faced by management, which I have discussed above.

The payoff for shrinking revenues with Established Brands - by far Organon's biggest division - was a very low price-to-sales ratio, and price-to-earnings ratio, and a generous dividend. This is still very much true of the company. Based on FY23 revenue guidance for $6.2bn of revenues, Organon's forward P/S ratio is ~0.5x, and based on net profits estimated ~$1bn, forward earnings per share ought to be ~$4, and price-to-earnings ratio therefore ~3x.

These ratios typically send a strong buy signal to prospective investors, but only if the underlying business has genuine growth potential. Organon is promising a strong 2024, with tailwinds in China, in the form of falling interest rates, fewer inflationary concerns, and incremental progress within its two "growth" divisions.

In my view, after doing research for this article, I find this investment proposition hard to swallow, unfortunately, as I am long Organon myself. The evidence that the company can generate long-term growth is scant at the present time - even if some current headwinds ultimately become tailwinds, Women's Health and Biosimilars simply don't look like businesses that can drive the company forward as Established Brands revenues inevitably decline when there is so much debt to pay down.

Organon does have one final card to play, however, that might keep investors interested - a dividend yield that currently stands at 9%. CFO Walsh told investors on the Q3 earnings call that:

We continue to believe that the business -- the cash flow profile that the business exhibits supports a dividend, certainly at the level that we have. There's no plans to change that in the near term.

If it weren't for the dividend, I would most likely be looking to sell my stake in Organon, but, so long as management can be trusted, the devaluation of the stock makes the dividend even more valuable, and so long as the dividend is in place, I can suspend my disbelief around long-term revenue growth, and hope that management can pull a rabbit or two out of its hat in 2024, when prevailing economic and geographic conditions are (hopefully) more favourable.

For further details see:

Organon: Poor Q3 Earnings Make Bear Case, But Dividend Is Saving Grace