OGN - Organon Q1 Earnings Review: The Better Viatris Still Not A Buy

2023-05-04 14:28:38 ET

Summary

- Organon reported obviously disappointing results today - OGN stock plunged more than 10% in response.

- In this update, I share my view on Organon's quarterly results and point out possible warning signs and reasons for the sell-off.

- I give an update on the company's significant debt and my opinion regarding its serviceability given the current interest rate environment.

- I also provide my thoughts on Organon's free cash flow which, to the frustration of shareholders, is not part of management's comments in the earnings release.

Introduction

Organon & Co. ( OGN ), specializing in women's health, announced its first quarter 2023 results today, May 04, 2023. I first covered the company in a comparative analysis with Viatris Inc. ( VTRS ), concluding that neither was a good investment from a dividend growth perspective, although I would feel more comfortable as an Organon shareholder for several reasons.

Since I did not see any outright red flags with Organon, I continued to follow the company and toyed with the idea of adding a small position of OGN stock in the "deep value" sub-segment of my portfolio, since the company is de facto priced for a terminal decline. So in this update, I share my view on the company's Q1 earnings report and indicate whether I now consider the stock a buy - after all, Organon looks very cheap during today's sell-off (18% baseline free cash flow yield) and pays a healthy dividend translating to a yield of almost 5%.

Organon Q1 Earnings Review

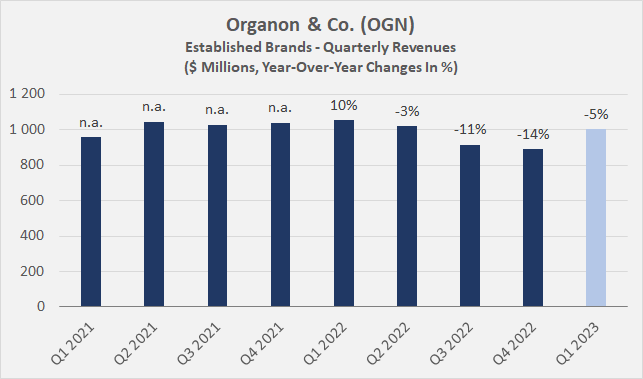

The company reported first-quarter revenues of $1.5 billion, down -1.9% from the same period last year, mainly due to currency effects. Organon generates about 80% of its revenues outside the U.S., so it seems reasonable to adjust the number for currency fluctuations. However, I consider currency effects to be largely a cost (or benefit) of doing business and generally do my research based on reported numbers. That said, I think it's positive to note that Organon's currency-adjusted revenues were up 3% year-over-year. This is largely the result of fairly robust revenues from the company's Established Brands segment, the life buoy, if you will, received from Merck to shoulder the debt assumed in the spin-off process. The segment accounts for about two-thirds of consolidated revenues, and I would argue that it is holding up quite well (Figure 1). For 2023, Organon expects performance to be roughly flat on a constant currency basis, so probably down in the low to mid-single digits on a reported basis. While the continued robust performance in Established Brands is definitely good news, I would say that a significant decline in this segment would be a clear warning sign given the still low revenues from the other two segments (Women's Health and Biosimilars) and the fact that Women's Health, in particular, is struggling with growth.

Figure 1: Organon & Co. (OGN): Quarterly revenues of the Established Brands segment (own work, based on the company's quarterly earnings reports)

{kind=link}

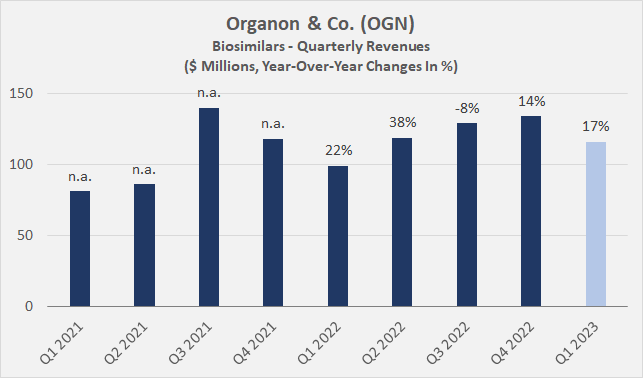

In Biosimilars, Organon recorded strong double-digit revenue growth thanks to Renflexis and Ontruzant (Figure 2). Renflexis is a biosimilar of Johnson & Johnson's ( JNJ ) immunology biologic Remicade (infliximab), and Ontruzant is a biosimilar of Roche's ( RHHBF , RHHBY ) oncology biologic Herceptin (trastuzumab). Of course, many investors are likely looking at Organon's biosimilar Hadlima due to the originator's (Humira, AbbVie, ABBV ) loss of exclusivity in the U.S. (already 2018 in Europe). While the broad acceptance of Humira and the cost incentive for pharmacy benefit management ((PBM)) companies rightly suggest that Humira biosimilars have a bright future ahead, I would not overstate Hadlima's earnings potential. A number of adalimumab biosimilars have been available in Europe since 2018 (e.g., Amgevita , Amgen ( AMGN ), Hulio , Viatris, Hyrimoz , Novartis ( NVS ), and Cyltezo , Boehringer). It should also be remembered that Cyltezo was the first FDA-approved interchangeable biosimilar to Humira. Add to that the fact that PBMs play an important role in setting the contract terms for inclusion of a biosimilar, and given the production scale of larger competitors such as Amgen and Novartis (via Sandoz ), I would argue that the biosimilars market is extremely competitive.

Figure 2: Organon & Co. (OGN): Quarterly revenues of the Biosimilars segment (own work, based on the company's quarterly earnings reports)

{kind=link}

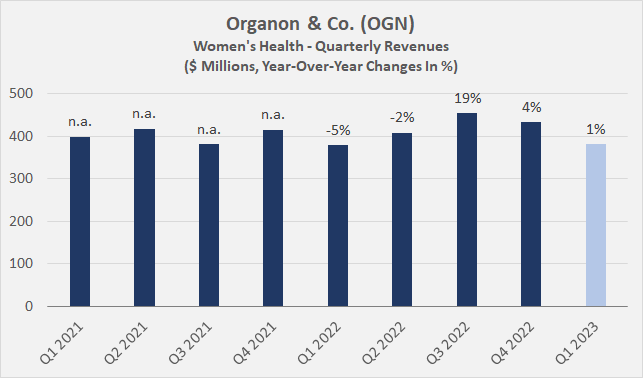

Finally, Women's Health remained virtually unchanged year-over-year (Figure 3), increasing revenues by 3% on a constant currency basis. According to management, sales of the segment's leading product - Nexplanon (-3% and -1%, respectively) - were impacted by customer buying patterns and are therefore expected to improve as the year progresses. In addition, COVID-19-related restrictions in China negatively impacted sales of Organon's fertility drug Follistim (-7% year-over-year on a constant currency basis), which I therefore also expect to improve in the coming quarters. At the risk of being overly conservative: growth in this segment was largely attributable to Marvelon and Mercilon and was therefore mostly inorganic in nature. It should be recalled that Organon acquired related marketing rights in China and Vietnam from Bayer AG ( BAYRY , BAYZF ) in February 2022. Nonetheless, and I noted this in my previous article, Organon's disciplined path of inorganic growth is definitely a plus compared to Viatris, which continues to struggle for direction and continues to "surprise" investors (see my previous analysis ). At the same time, I would argue that Organon has little alternative given its high debt load and non-investment grade credit rating.

Figure 3: Organon & Co. (OGN): Quarterly revenues of the Women's Health segment (own work, based on the company's quarterly earnings reports)

{kind=link}

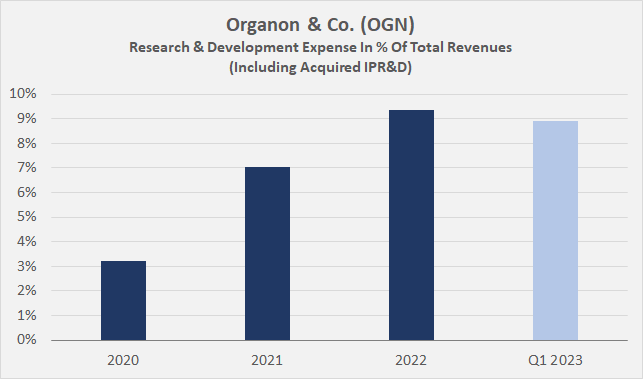

Quarterly gross margin was acceptably robust for a business characterized by drugs with weakening pricing power, declining 190 and 130 basis points on a reported and adjusted basis, respectively. Organon continues to invest heavily in the business (Figure 4), which was the main reason for the significant adjusted EBITDA margin contraction (-760 basis points year-over-year to 33.7%). Personally, I view Organon's continued high investment in the business as a positive, but I think the market largely views this as a sunk cost given positive results are not fully visible yet. For the full year, Organon continues to expect R&D spending to be in the high single digits as a percentage of revenues.

Figure 4: Organon & Co. (OGN): Research & development expenses, including acquired in-process research and development (IPR&D) expenses (own work, based on the company's 2022 10-K and the Q1 2023 earnings press release)

{kind=link}

While high R&D spending didn't contribute to the earnings miss (management had already projected high-single-digit investment in February), it was mainly higher interest expense (see below) and foreign exchange effects that caused the company to miss analysts' estimates by about 7%, or $0.08.

All in all, I take a slightly more positive view of the results than the market (OGN stock is down more than 10% at the time of writing), but I don't think it can be stressed enough that Organon needs to quickly ramp up growth in Women's Health and Biosimilars (the latter may prove difficult) to more than offset the eventual decline in Established Brands.

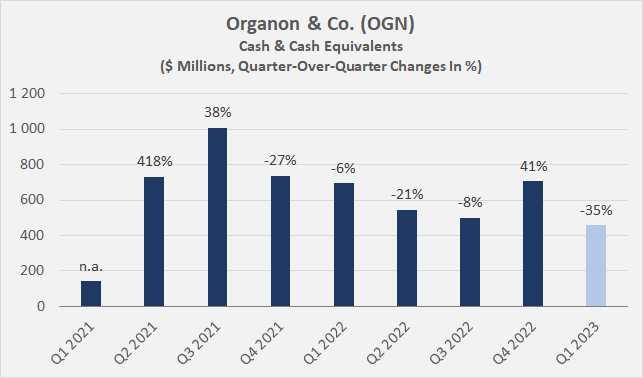

What bothered me most - although this is nothing new - was that the company reported lackluster cash flow numbers. As my regular readers know, I place a high value on cash earnings, especially in the context of a company like Organon that has significant debt. However, to strike a more positive tone, the company today declared a regular quarterly dividend of $0.28 per share (annualized cost of about $256 million, 25% of baseline free cash flow), so things probably aren't so bad after all, or are they? For the full year 2022, free cash flow was well below the prior year and, as expected, below my baseline estimate of $1 billion annually. As working capital-related effects normalize, free cash flow should recover in 2023. Therefore, it will be important to take a close look at Organon's cash flow statement when the 10-Q report for the first quarter is released. Finally, it seems worth noting that cash and cash equivalents (the only actual balance sheet number mentioned in the earnings press release) were comparatively low at the end of Q1 2023 and did not follow the same trend as last year (Figure 5).

Figure 5: Organon & Co. (OGN): Cash & cash equivalents (own work, based on the company's 10-Qs, 10-Ks, 2022 10-K and the Q1 2023 earnings press release)

{kind=link}

An Updated Look At Organon's Balance Sheet

As I discussed in my original article, Organon incurred a significant debt burden in the spin-off and its long-term debt was rated non-investment grade by Moody's ( Ba2 with stable outlook ). To be fair, the company has historically demonstrated its conviction through voluntary repayments of $100 million in Q4 2021 and another $100 million in Q2 2022 on its USD-denominated term loan (original amount $3 billion). The good news from today's earnings release is that Organon repaid another $250 million in the first quarter of 2023. While that doesn't sound like much, it is confirmation that free cash flow is unlikely to be so bad after all (see above).

In addition, it is important to remember that the loan is costing Organon dearly - LIBOR plus 300 basis points, to be exact. With 3-month USD LIBOR currently at about 5.33%, I think Organon has a big incentive to repay this loan (as well as the €750 million term loan) as quickly as possible. Assuming constant interest rates, the repayments since 2021 reduced Organon's interest expense from a hypothetical $543 million to $505 million annually. This is definitely a step in the right direction.

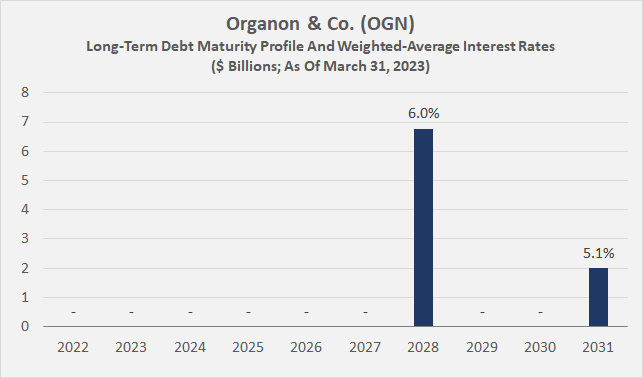

Rising interest rates continue to adversely affect Organon, so I surmise that yesterday's announcement of another 25 basis point rate hike also played a (small) role in today's sell-off. Since Organon did not release detailed balance sheet data in its earnings press release, I included the most recent debt repayment figure in my own data sheet to provide an updated debt maturity profile (Figure 6). It's quite reassuring that Organon has no short-term maturities, but time (and high interest rates) are definitely working against the company. After all, at the current weighted-average interest rate of 5.9% (based on management's guidance and the 2022 10-K), Organon spends about one-third of its baseline pre-interest free cash flow on interest payments. Note that the percentages in Figure 6 represent the approximate weighted-average interest rate on debt due each year.

Figure 6: Organon & Co. (OGN): Long-term debt maturity profile (own work, based on the company's 2022 10-K and the Q1 2023 earnings press release)

{kind=link}

Key Takeaways

Organon reported its first quarter results today, which were largely in line with expectations. I suspect that the substantial sell-off is at least partly due to the fact that Organon still does not disclose cash flow-related data in its earnings announcements, and investors probably still have the relatively weak 2022 free cash flow in mind. The market hates uncertainty, and given Organon's high cash flow needs (annual interest expense of more than $500 million, dividend costs of $256 million), I don't understand why management doesn't report cash flow-related numbers in its earnings press releases.

That said, I think it is important to note that free cash flow in 2022 was significantly impacted by working capital-related effects and should rebound in 2023. The $250 million voluntary debt repayment in the first quarter and the fact that another regular quarterly dividend was declared today are signs that free cash flow is improving - or at least management's expectations for free cash flow, given the decline in cash and cash equivalents, which did not follow last year's trend.

Looking at Organon's segments, I see the resilience of the Established Brands as rather positive, although management really needs to rapidly accelerate growth in Women's Health and Biosimilars. It will probably take a while for these two segments to be able to offset a decline in the Established Brands segment.

As discussed in my previous article, I view Organon's combination of disciplined growth strategy through acquisitions with significant R&D investments quite positively compared to Viatris, whose management continues to struggle for direction and misses no opportunity to "surprise" investors. That being said, I would not over-interpret Organon's solid 2.5% growth in its contraceptives segment against the backdrop of weak Nexplanon results, as it is attributable to the significant inorganic revenue contribution from Marvelon and Mercilon (+58% year-over-year on a reported basis). To be fair, however, management did mention this in the press release ("Organon gained rights in selected territories"), but conservative as I am, I would have chosen different words.

In summary, Organon continues to trade cheaply for several reasons. I do not believe that the double-digit share price decline was fully justified, and I stand by my original conclusion that I would feel comparatively comfortable as a shareholder of Organon (but still not comfortable enough):

"[…] the investment case is clearer, the baseline performance is more plausible, and even though the company's debt poses a greater risk than Viatris', which is still rated investment grade and largely consists of fixed rate notes. " from my article "Don't Buy Viatris And Organon Just Because Of The Dividends", published Feb. 13, 2023

However, due to the significant uncertainties and balance sheet challenges, I continue to not consider Organon a promising investment case and instead focus on adding to my existing high-quality equity holdings such as CME Group Inc. ( CME , see my analysis ) or starting a position in The Cigna Group ( CI , see my earnings preview ), both of which I currently view as fairly attractively valued.

As always, please consider this article only as a first step in your own due diligence. Thank you for taking the time to read my latest article. Whether you agree or disagree with my conclusions, I always welcome your opinion and feedback in the comments below. And if there is anything I should improve or expand on in future articles, drop me a line as well.

For further details see:

Organon Q1 Earnings Review: The Better Viatris, Still Not A Buy