OGN - Organon: The Federal Reserve Black Swan (Rating Upgrade)

2023-10-04 11:45:54 ET

Summary

- The stock of junk-rated Organon & Co. has lost more than 40% since my first article, largely due to interest rates continuing to rise.

- I take a close look at the company's debt and how I think the situation will evolve until 2028 - when OGN will have to refinance most of its debt.

- Besides a brief update on Organon's Q2 performance, I explain why the company's debt situation remains manageable even under a "higher for longer" scenario.

- OGN stock is cheap even under very conservative assumptions. In my view, it has become a classical deep value situation that justifies a speculative long position.

Introduction

Organon & Co. ( OGN ) stock has fallen sharply in recent months and is still in no-man's land when it comes to finding a bottom. In February 2023 , I cautioned against buying OGN stock, primarily due to profitability issues and its leveraged balance sheet. The stock was still more expensive than the "ugly duckling" peers Teva Pharmaceutical Industries Ltd. ( TEVA ) and Viatris Inc. ( VTRS ), which I also took a closer look at in that article. Since February, Organon stock has lost more than 40%, even taking into account its relatively high dividend. In a follow-up analysis in May, I was pleasantly surprised by the resiliency of Organon's base business, but still continued to avoid the stock. OGN has since fallen to nearly $16, largely due to interest rates continuing to rise. Considering that OGN was spun-off from Merck & Co., Inc. ( MRK ) only in 2021 - when interest rates were still extremely low - it doesn't seem hyperbolic to call this interest rate cycle a black swan for Organon. Who would have thought in mid-2021 that we would be back to 2007 interest rates in less than two years?

In this update, I take a close look at the impact of the current interest rate environment on Organon and whether the company can continue to navigate this environment. I also touch on Organon's Q2 results and explain why I think the stock has become a "deep value" pick.

So let's get to it…

Interest Rates To The Moon - Organon To The Ground?

A still hawkish Federal Reserve and a hot labor market are fueling fears among investors that interest rates will continue to rise. The 10-year Treasury bond yield recently rose above 4.8% , a level last seen before the Great Recession. Short-term rates are even higher, resulting in an inverted yield curve, but the degree of inversion has moderated significantly in recent months due to the depreciation of longer-term bonds.

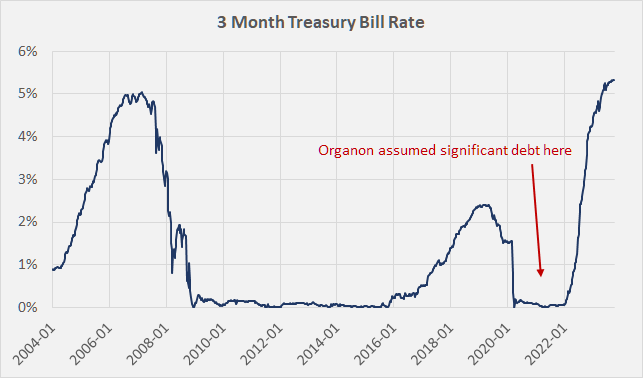

Given that Organon was only spun off in June 2021, one might wonder what's not to like about the fact that the company took on the significant debt to pay its parent company Merck the agreed-upon $9 billion distribution when interest rates were still extremely low? (Figure 1) It's the fact that Organon took on a significant amount of floating-rate debt and is now paying the price for this - in hindsight - obvious mistake.

Figure 1: 3 Month Treasury Bill rate (own work, based on data retrieved from the Federal Reserve's website)

{kind=link}

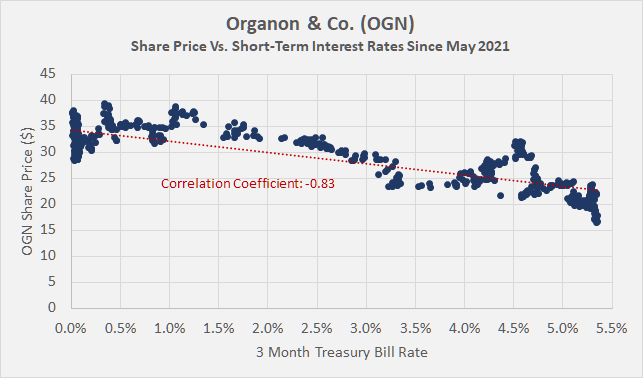

Interestingly, Organon's stock price has a strong inverse correlation with short-term interest rates (Figure 2), confirming investor fears that the company could be crushed by the high interest rate on its floating-rate debt. But is it really that bad?

Figure 2: Organon & Co. (OGN): Share price versus the 3 Month Treasury Bill rate (own work, based on OGN's daily closing share price and data retrieved from the Federal Reserve's website)

{kind=link}

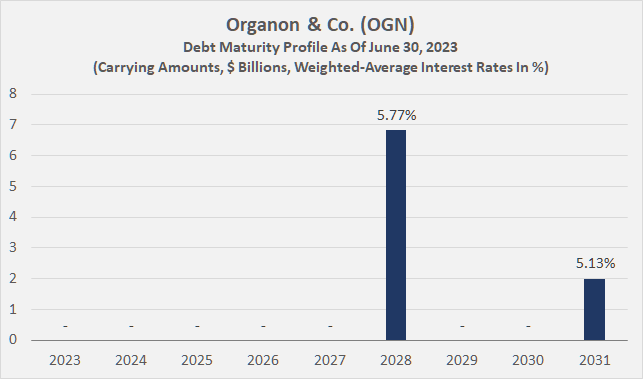

Figure 3 shows an updated maturity profile based on book values ($8.8 billion at the end of the second quarter of 2023) and the weighted-average interest rate for each bucket. Organon pays a 300 basis point premium on the SOFR (Secured Overnight Financing Rate), which is currently 5.3% , for its U.S. dollar-denominated term loan. For its floating-rate euro debt, the company pays a 300 basis point premium on the "adjusted EURIBOR" (Euro Interbank Offered Rate). I use the 1-week EURIBOR, currently at 3.9% , as a proxy. Organon's weighted-average interest rate is currently 5.6%, which is not that extreme given that the company has about $2.5 billion in U.S. dollar-denominated floating-rate debt (2028 term loan). Here, the still comparatively low EURIBOR and the quite favorably valued euro-denominated bonds maturing in 2028 (€1.25 billion) and the 4.125% secured bonds ($2.1 billion, also maturing in 2028) help.

Figure 3: Organon & Co. (OGN): Debt maturity profile and weighted-average interest rates (own work, based on company filings)

{kind=link}

As I explained in my earlier articles, Organon can be expected to generate free cash flow of at least $1 billion per year, so the company currently spends about one-third of its pre-interest free cash flow on interest payments. That's a lot, but given how well the base business is holding up, I don't think it's a serious issue.

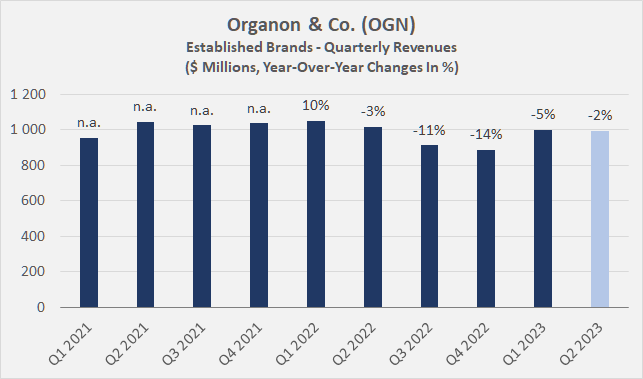

In the second quarter, management reported a slight decline in revenues of the Established Brands segment (-2% year-over-year, Figure 4), which currently contributes about 62% to Organon's top-line. The Biosimilars segment is still in its infancy, but the company definitely made headlines when it announced the launch of its Humira (adalimumab) biosimilar Hadlima in the U.S. in July 2023. Still, I remain rather cautious and patient about the segment's expected contribution to free cash flow, in particular because of the inherently competitive nature of the segment. The Women's Health segment (27% of revenues in Q2 2023) continues to show good performance (+7% year-over-year, +15% sequentially). Importantly, all three segments saw volume growth (slide 9, Q2 2023 earnings presentation ).

Figure 4: Organon & Co. (OGN): Quarterly revenues of the Established Brands segment and year-over-year growth rates (own work, based on company filings)

{kind=link}

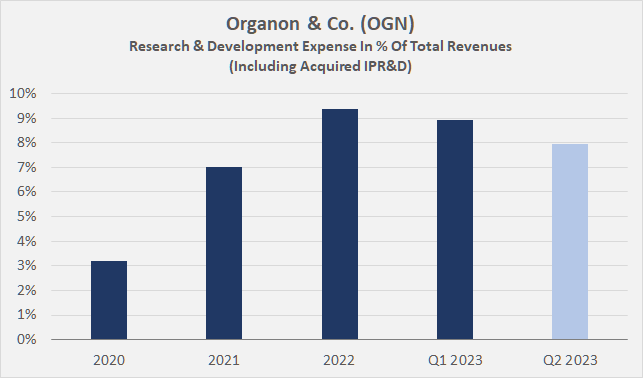

Overdependence on Nexplanon is a bit of a concern, but I think management's conservative approach to inorganic growth through acquisitions of other (smaller) companies and commercialization rights (see my first article), as well as continued high investment in R&D (Figure 5) and marketing (4% of 2022 revenues) is the right one. All in all, I believe the company is capable of growing its revenues over the years, albeit at a relatively slow pace, and the interest payments seem manageable despite the floating-rate debt of almost 40% of total debt.

Figure 5: Organon & Co. (OGN): Research & development expenses in percent of total revenues (own work, based on company filings)

{kind=link}

It became clear from the maturity profile that Organon has no short-term maturities. However, if interest rates do indeed remain "higher for longer," the company could be forced to agree to quite unfavorable rates due to the need to refinance in 2028.

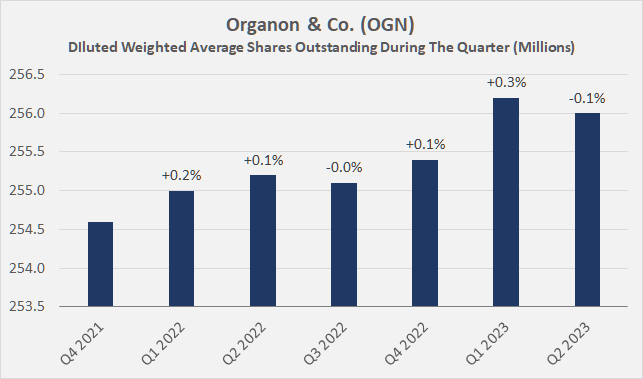

That said, considering that Organon is likely to be able to generate $1 billion in free cash flow annually, of which the company currently pays out less than one-third in dividends ($287 million on an annualized basis, conservatively using diluted shares outstanding), a significant portion of the pie can be used to pay down debt. I do not believe Organon will increase its dividend in the next few years, but the payout is expected to increase somewhat due to dilution from stock-based compensation. However, this impact on Organon's ability to pay down debt should be negligible, considering that the number of diluted shares outstanding has only increased by 0.55% since Q4 2021 (Figure 6).

Figure 6: Organon & Co. (OGN): Diluted weighted average shares outstanding during the quarter (own work, based on company filings)

{kind=link}

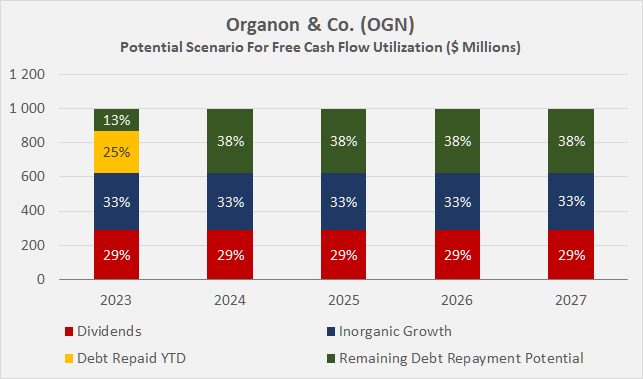

Even if we assume zero free cash flow growth and dividend payout growth at a rate of 0.3% (annualized dilution), and reserve even one-third of free cash flow for inorganic growth opportunities, Organon can still repay about $1.4 billion of its debt by the end of 2027 (Figure 7). This represents nearly 60% of the current outstanding U.S. dollar floating-rate debt and would reduce Organon's interest expense by about $140 million if interest rates indeed remain at current levels over the next five years. If Organon manages to grow its free cash flow at 2% per year, it could retire almost $1.8 billion of its debt.

Figure 7: Organon & Co. (OGN): Potential scenario for free cash flow utilization (own work, based on company filings and own calculations)

{kind=link}

In my view, continued emphasis on debt reduction will set the company up for a credit rating upgrade, which will put it in a better position when it has to negotiate refinancing terms in 2028. Recall that Organon was rated Ba2 by Moody's (non-investment grade), but with a stable outlook since the rating was assigned.

Now, as a prudent investor, one could argue that there is a risk that management is squandering excess free cash flow on potentially unprofitable acquisitions. However, given Organon's past transactions, one can conclude that management is indeed rather conservative and understands that it must prioritize debt reduction. This is also underscored by the occasional voluntary debt repayments. For example, the company repaid $250 million on its U.S. dollar-denominated term loan in the first quarter (p. 4, Q1 2023 earnings press release ). Of course, it is important to keep an eye on future debt reduction and whether management maintains its rather conservative course.

Finally, to paint a "worst case" picture, let's assume that short-term interest rates in the U.S. and E.U. continue to rise to 8% and 7%, respectively. Don't get me wrong, I don't think these are realistic expectations, but I nonetheless believe it is a good idea to evaluate Organon's debt servicing ability in such a scenario. The company's interest expense would increase from its current level of about $525 million to $610 million per year, which is still manageable even in light of the dividend. And even in the highly unlikely event that interest rates remain at such high levels for the next several years, Organon would still be able to repay $1.2 billion of its expensive term loan, which matures in 2028.

All in all, I think investors are currently being overly negative about Organon.

Conclusion

Current Organon shareholders are in an unenviable position. The stock continues to fall and there are no signs of a bottom. To some extent, the market is right to discount the company's stock because of the heavy reliance on floating-rate debt and junk rating. However, almost everything is too cheap at some point, and I think Mr. Market is currently overdoing it with OGN stock.

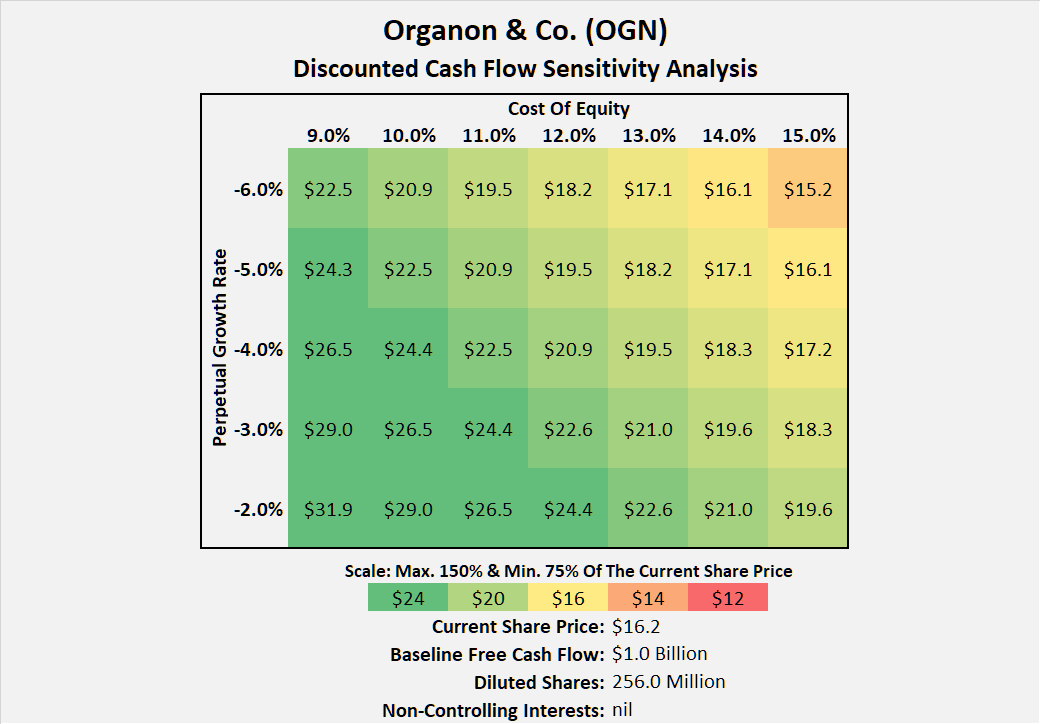

Figure 8, which shows a discounted cash flow sensitivity analysis based on my baseline expectation of $1 billion of free cash flow per year, highlights this quite well. Essentially, Organon is priced for a fairly rapid decline. Even if we assume that Organon's free cash flow declines at an annual rate of 6% (!) in perpetuity, the stock is currently fairly valued at a cost of equity of 14%. Granted, Organon's cost of capital is quite high due to its poor (but manageable) balance sheet, junk rating, and competitive environment (see my first article). But a 14% cost of equity more than adequately compensates investors for the risks taken, in my view. And even if we assume - quite conservatively - that Organon's base cash flow is only $500 million instead of $1 billion, the stock is still fairly valued today if management can maintain that free cash flow and investors are content with a cost of equity of 11%. Maintaining such a low level of free cash flow does not appear to be a major hurdle, especially given the fairly solid sales performance to date.

Figure 8: Organon & Co. (OGN): Discounted cash flow sensitivity analysis (own work, based on company filings and own calculations)

{kind=link}

The 6.9% dividend yield - which I consider pretty safe - is also quite enticing, but I would not expect dividend growth over the next few years, so the purchasing power of the income generated by owning OGN stock will decline.

The investment case is simple: Organon stock is priced for decline, and the current share price assumes that interest rates continue to rise and that the company doesn't gain traction in Women's Health and Biosimilars. But even if the company is indeed in decline, the stock is still fairly cheaply valued. I don't think Organon necessarily has a super-bright future, but I also don't think it's in terminal decline. Because of this, and because the debt situation - which looks catastrophic on the surface - looks manageable even if interest rates continue to rise, I am inclined to add a small position of OGN stock to the speculative portion of my portfolio. However, being a rather conservative investor, I would not invest more than 0.25% to 0.5% of my total portfolio value in this deep value opportunity.

Thank you for taking the time to read my latest article. Whether you agree or disagree with my conclusions, I always welcome your opinion and feedback in the comments below. And if there's anything I should improve or expand on in future articles, drop me a line as well. As always, please consider this article only as a first step in your own due diligence.

For further details see:

Organon: The Federal Reserve Black Swan (Rating Upgrade)