OGN - Organon: What I'm Looking For In This 8% Yield In 2024

2024-01-03 08:10:00 ET

Summary

- Organon, a pharmaceutical company, has a diverse portfolio of products in women's health and biosimilars.

- The company has faced challenges in its women's health segment but expects a turnaround in its top-selling drug and growth in the fertility business this year.

- Organon is focused on deleveraging its balance sheet and offers a high dividend yield while trading at a valuation far below that of health sector peers.

Stocks have been called a lot of things, with comparisons to a 'giant casino' being one of them. I don't think that's a fair comparison, however, as unlike the stock market, the odds are stacked against the gambler at the casino in the long run.

In the stock market, losses are capped at 100% of invested principal, but the potential for gains is uncapped. That's why stocks operate more like a parimutuel system, not unlike the horse track, in which anyone who understands the horses knows which are in the best position to win.

However, when the odds are established for each horse, it's no longer a sure bet that the pricier picks present the best potential return on investment. This brings me to the pharmaceutical space, in which the market has largely chased up leading weight-loss drugmakers like Eli Lilly ( LLY ) and Novo Nordisk ( NVO ) to high valuations.

While those are certainly high-quality companies generating strong cash flows, buying them at their current high valuations doesn't guarantee market-beating returns.

On the other hand, stocks like Organon ( OGN ) are trading at dirt-cheap valuations. I last covered OGN here back in July, noting its biosimilars growth and low valuation. OGN hasn't been one of my best picks, to say the least, as headwinds around its Women's Health division have driven the share price down by 29% since my last piece. In this article, I provide an update and discuss whether the stock remains a buy at present, so let's get started.

{kind=link}

Why OGN?

Organon is a global pharmaceutical company that has a portfolio of over 60 medicines and products in women's health. It also has a growing biosimilars business and established brands that were once a part of Merck ( MRK ) before OGN was spun off in 2021.

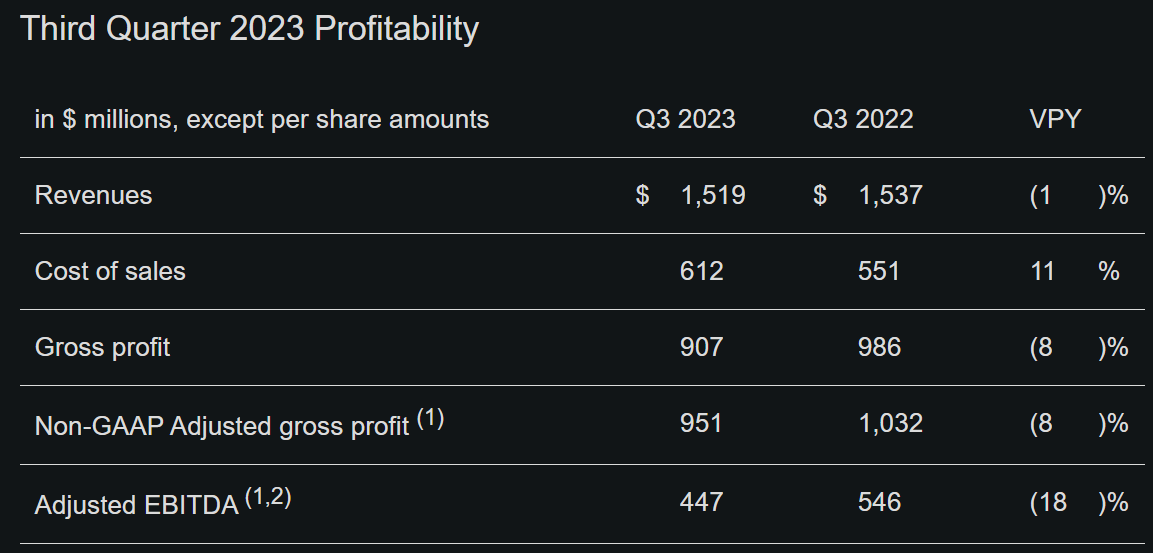

OGN is a company that's in transition, as it seeks to ramp up its biosimilars business to counter headwinds in other segments. While revenue has held up well, declining by just 1% in the third quarter, gross profit and adjusted EBITDA declined by 8% and 18%, respectively, due to challenging sales for higher margin products in Women's Health, like NuvaRing and Nexplanon.

{kind=link}

The product mix shift toward lower margin medicines and products combined with unfavorable foreign exchange (strength in the dollar) resulted in a lower full year 2023 adjusted EBITDA margin expectation of 31.0% at the midpoint, down 125 basis points from 32.25% at the midpoint previously.

Risks to OGN include the fact that NuvaRing, a form of birth control, lost its patent protection in 2023, resulting in a number of generic versions like EluRyng on the market today. NuvaRing revenue fell 26% during the third quarter to $37 million, and it's quite possible that its market share will continue to erode as competitive pressures ramp up.

At the same time, Nexplanon also declined by 4% in the last quarter, driven in part by headwinds in China. China remains a big market for Nexplanon, which is another form of birth control, and the government's ongoing review of healthcare practices "which commanded significant physician attention" was a headwind for the drug in 2023. While management believes the current issues in China are transient in nature, it remains to be seen for how long this headwind might last and is something worth paying attention to in the upcoming fourth-quarter results.

Nonetheless, management sees a turnaround for Nexplanon which is its top-selling drug, representing around 14% of total revenue. This is reflected by comments in late November at a Piper Sandler Healthcare Conference :

Going forward in 2024, it's going to be a very strong year for Nexplanon for 2 reasons in the U.S. One, our 340B business, which is a lower-priced federally-mandated business, has grown to about 1/3 of our overall business globally. And so that Merck [the predecessor company] used to give additional discount on top of the 340B price, and we've taken all that away. We removed that discount in September.

Plus we get the added price increase that we're taking next year, plus you get the incremental volume growth that we have. So, we expect low double-digit growth of Nexplanon next year. So, it's still our strongest product going forward. Nothing has changed dramatically.

Nonetheless, counter to birth control products, OGN has the opposite side of the spectrum covered with growing fertility treatments, and management believes that the fertility business in China remains a growth engine. That's because, like neighboring countries South Korea and Japan, China has been grappling with a declining birth rate. The country has been encouraging births through tax deductions, longer maternity leave , and housing subsidies. In addition, China announced in 2023 that it's offering free IVF fertility treatment, which could serve as a boost to OGN's fertility therapies.

Moreover, the U.S. fertility market is seeing higher employer coverage, as noted during the last conference call :

In the U.S., the fertility market is growing and demand is very strong. Strategically, we are working on an evolution of our go-to-market strategy into the reimburse market segment, which is rapidly growing. Over the past three years, the percentage of employers providing fertility benefits has increased from 30% to 40%.

Turning to the dividend, OGN currently yields an attractive 7.8% and the dividend is covered by a 28% payout ratio. This gives OGN plenty of cushions to pay down debt, as its net debt to adjusted EBITDA ratio stands above 4x, which is above the 3.0x level generally considered safe by ratings agencies. This is reflected by OGN's BB credit rating from S&P, which sits below investment grade. It's worth noting that management seeks to lower the leverage ratio to below 4x this year with a long-term target of 3x, down from 3.5x previously.

Lastly, while OGN is not a sleep-well-at-night type of stock, I do continue to see value at the current price of $14.42 with a forward PE of just 3.5x. At this price, OGN is priced for a significant terminal decline rate, but analysts actually expect 2.7% to 4.2% annual EPS growth over the next 2 years.

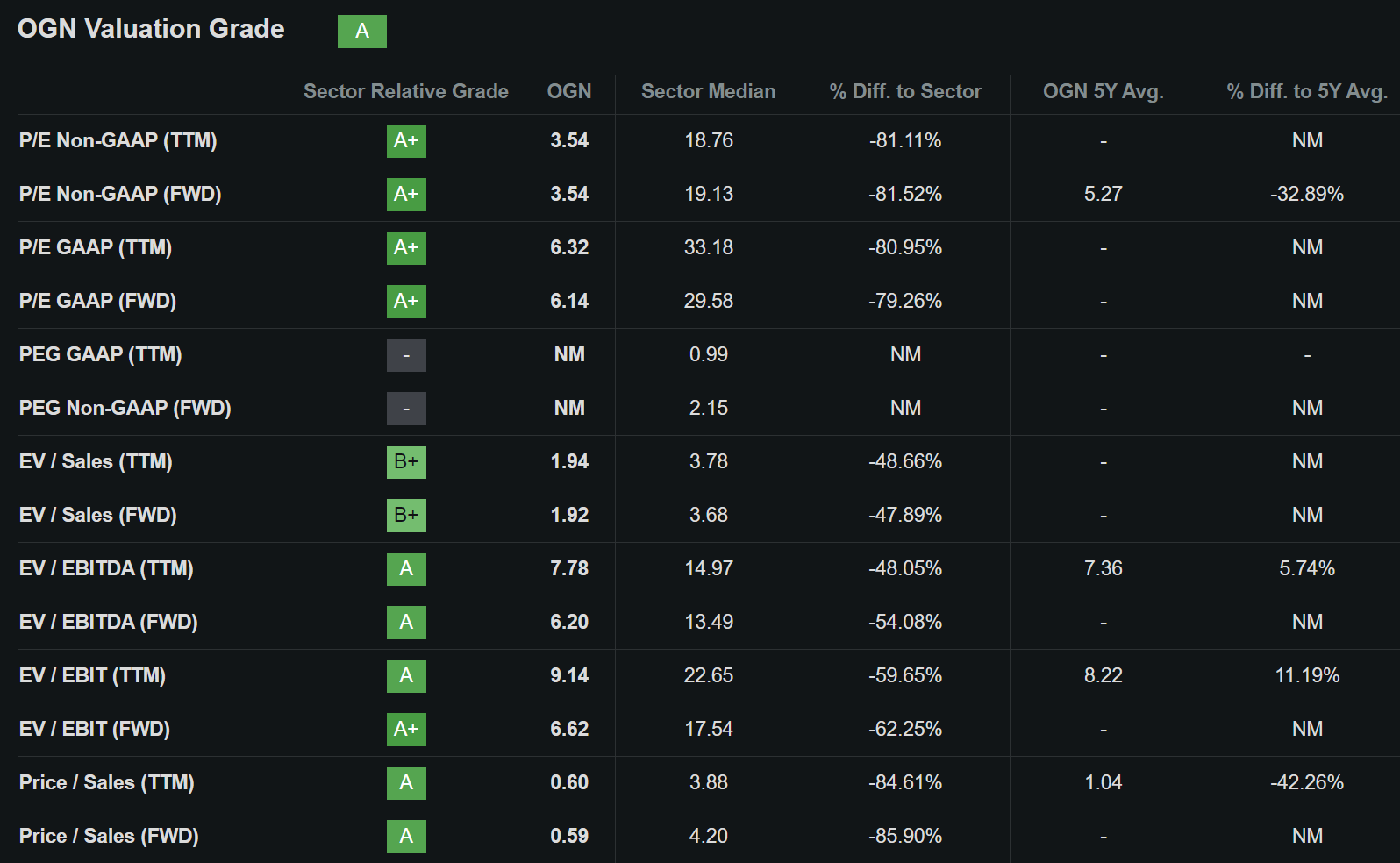

Plus, OGN could de-risk itself with debt paydown over the next 12-24 months, as it generated unlevered free cash flow of $515.6 million over the trailing 12 months. Debt paydown and a lowering of the leverage ratio could reduce the debt overhang that remains over the stock. As shown below, OGN's Price-to-Sales, PE, and EV/EBITDA metrics sit significantly below that of the median for the Healthcare Sector. EV/EBITDA is also a fair metric to consider since it includes the value of debt. While Wall Street has a consensus 'Hold' rating on the stock, the average price target of $20.33 sits significantly above the current price today.

{kind=link}

Investor Takeaway

Overall, Organon has a diverse portfolio of pharmaceutical products that present different growth opportunities. While it saw headwinds in birth control segments last year, its fortunes may change in 2024 with a potential turnaround in its top drug as well as tailwinds in the fertility business in the U.S. and China. Additionally, the company is focused on deleveraging its balance sheet and currently pays a well-covered and high dividend yield. The aforementioned is what I would look for from the company this year.

While OGN is far from being a sleep-well-at-night stock, investors appear to be adequately compensated for the risks with a far below-average valuation. As such, I maintain a 'Buy' rating on the stock as part of a well-diversified portfolio.

For further details see:

Organon: What I'm Looking For In This 8% Yield In 2024