AVTXF - Origin Materials: Emerging As A Leader In Carbon Negative Materials

2023-03-06 13:23:46 ET

Summary

- Customer demand currently stands at $9.3 billion, even as Origin Materials has yet to begin commercial production.

- Origin 1 has begun mechanical completion and production is expected to start ramping up in the second quarter of 2023.

- Origin 2 remains on track and the company has sufficient funding for the construction of Origin 2.

- Strategic partnership with Avantium brings the strength of two innovative leaders into display.

- My 1-year price target for Origin Materials is $10.94, representing 120% upside from current levels.

This article was first posted in Outperforming the Market on 27 February 2023.

Today, the company I'll be writing about in this article is Origin Materials ( ORGN ).

I think that it is inevitable that one of the best alpha generating opportunities of our generation is that of the green transition.

We are sitting at the cusp of a long-term period of green transition where governments and companies globally will spend trillions into green investments. In 2022 alone, $1.1 trillion was spent on investments into the energy transition.

Origin Materials plays an important role in this transition as its mission is literally to "enable the world’s transition to sustainable materials as the leading carbon negative materials company".

It focuses on the global carbon emissions that come from the production of materials, which according to the Ellen MacArthur Foundation, makes up 45% of global carbon emissions. In an earlier article to members of Outperforming the Market, I elaborated on why I am adding Origin Materials to The Barbell Portfolio. Today, in this article, I aim to highlight some of the key investment thesis for Origin Materials and why it is such a compelling investment today. I have also written other articles on Origin Materials, which can be found here .

Investment thesis

Origin Materials looks to me to be emerging as a leading carbon negative materials company in the world. The company continues to see strong customer demand from large and global companies while executing well in its construction of Origin 1 and 2. With Origin 1 expected to start up by the second quarter of 2023, potential and existing customers of Origin Materials can then obtain large volumes of samples for testing and developing new products. I will be watching the ramp up of production in Origin 1 closely as this will indicate to me how management will be able to scale up production in subsequent plants and the execution in the construction of Origin 2 is also key given that it will be its first large scale manufacturing facility with huge economies of scale to be reaped.

Today, Origin Materials appears to be executing well in its strategy towards being a leading carbon negative materials company. The company also remains well funded for the construction of Origin 1 and 2 and expects to have sufficient funding until it achieves positive EBITDA, implying the business is poised for sustainable growth.

Introduction to Origin Materials

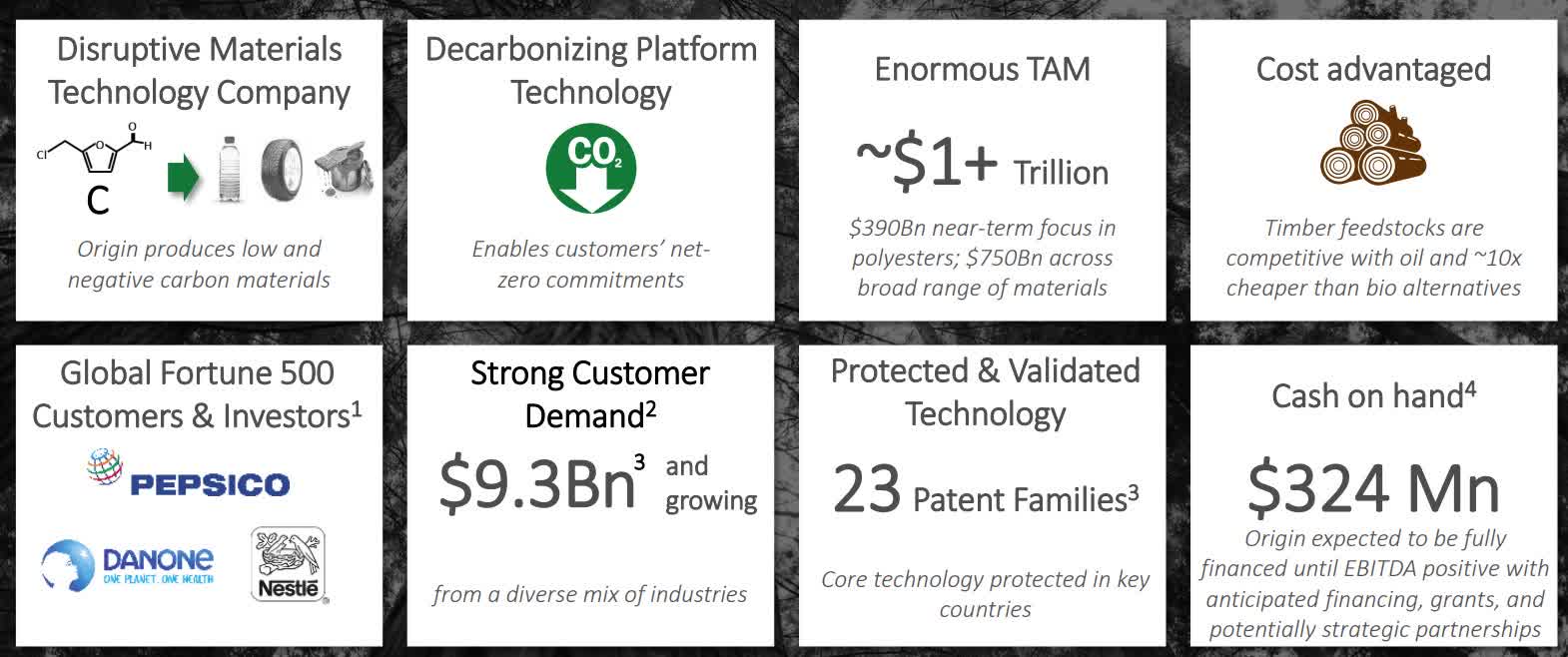

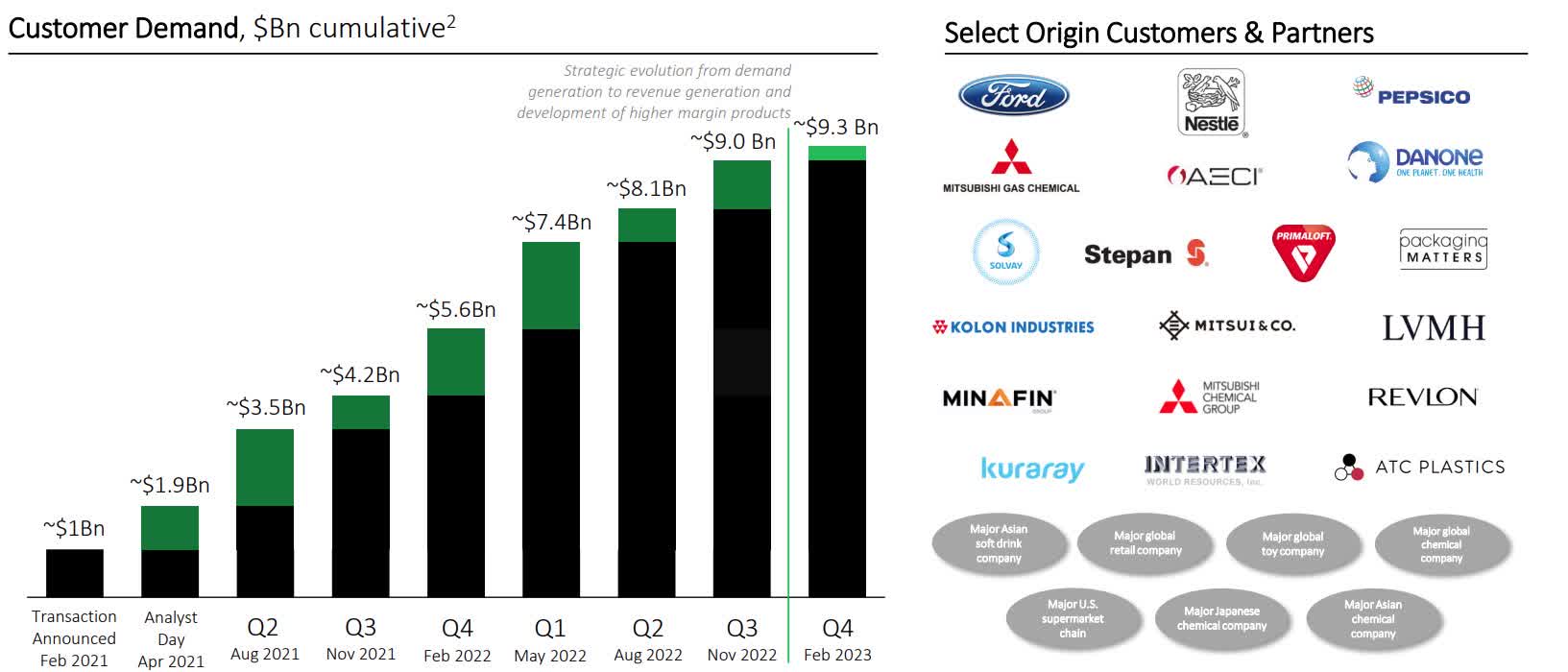

As a brief introduction to Origin Materials, it is a leading carbon negative materials company in the world. Its patented technology platform is able to use the carbon found in sustainable wood residues into useful materials and capture the carbon in the process of doing so. It has a large total addressable market of more than $1 trillion given the wide range of products that its platform can cater to. The company has $9.3 billion in customer demand in the form of off-take agreements and capacity reservations with large, global companies.

Most importantly in the current investment climate that we are in right now, Origin expects that it will be fully financed until it turns EBITDA positive as a result of anticipated financing, grants and even potential strategic partnerships it might obtain.

{kind=link}

Snapshot of Origin Materials (Origin Materials IR)

Customer demand remains robust

In the fourth quarter of 2023, management grew customer demand by $300 million, to a total of $9.3 billion today, which includes both capacity reservations and off-take agreements.

This was more than a 9x increase since Origin Materials decided to go public early in 2021.

{kind=link}

Origin Materials customer demand (Origin Materials IR)

In the quarter, management announced that there was a new strategic relationship with a major global chemical company.

Origin 2's para-xylene and PET capacity have mostly been committed and as a result of this, the sales team at Origin Materials have focused their efforts into marketing of higher margin products like carbon black and advanced CMF-derived products including FDCA and PEF.

Lastly, management remains positive about the huge sales pipeline it has built and remains in multiple active discussions with its existing customers about potentially expanding their current agreements and to bring in new potential customers.

Mechanical completion of Origin 1

On January 27, Origin Materials announced Origin 1's mechanical completion, which is on track with regards to the timeline that it has set for its operational targets.

With the announcement of Origin 1's mechanical completion, this means that the critical mechanical systems of Origin 1 have been installed and the team has started commissioning.

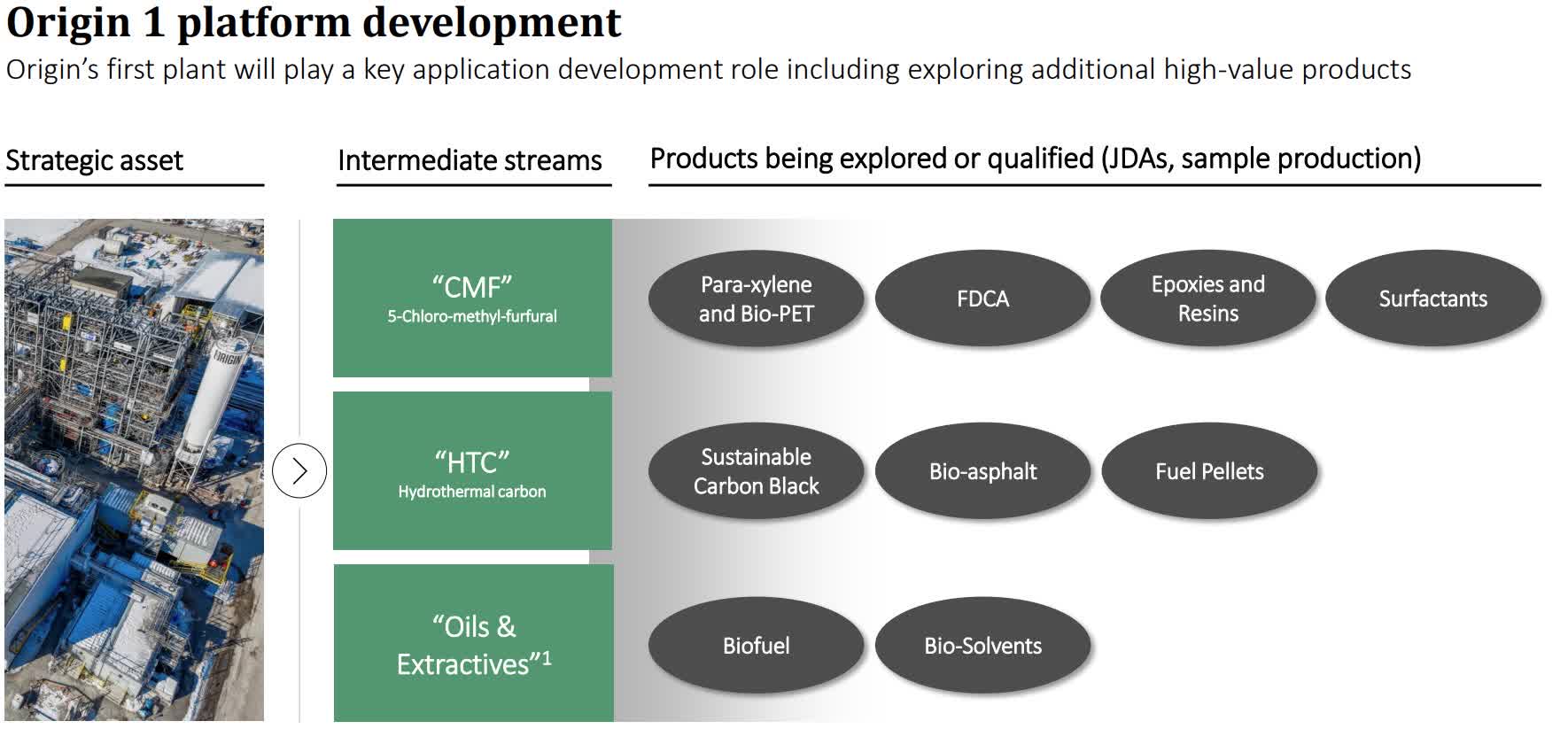

In addition, Origin 1 is seen as a key strategic asset to be used for helping to qualify Origin's higher value applications for its chloromethylfurfural (“CMF”) and hydrothermal carbon (“HTC”) products. This is because Origin 2 is expected to be the plant with much higher economies of scale and larger production capabilities. With Origin 1, management intends to use it to scale its technology as the volumes generated from the plant can be used to produce customers with more samples.

To add, Origin 1 is expected to allow customers to do further development work and test their products, eventually with the hope that new, higher margin and higher performance products can be developed. Some products that can be explored or qualified as a result of Origin 1's development role include sustainable carbon black, bio-PET, and biofuels, amongst other products as listed below. Eventually, some of these successful applications can then be commercially produced in Origin 2 or beyond. These products are deemed higher margin because they provide customers with improved performance and at the same time, because of the technology and platform of Origin Materials, customers are likely not able to use any other platforms other than that of Origin Materials to achieve a similar result.

{kind=link}

Origin 1 platform development (Origin Materials IR)

Management expects that commissioning will end and the plant will start up in the second quarter of 2023. Origin 1 will be ramped up throughout the year and will balance both outcomes of providing customers with samples to qualify materials and at the same time fulfil some customer demand.

As we get closer to the Origin 1 beginning production, I think that this will be a significant catalyst to the business. This is because Origin Materials will then be able to provide larger volumes of samples to its potential customers. These potential customers can then do the relevant testing or develop ways in which these materials to be utilized into their own products. At the end of the day, this could actually increase the customer demand and even encourage more of the capacity reservations to be converted to actual off-take agreements.

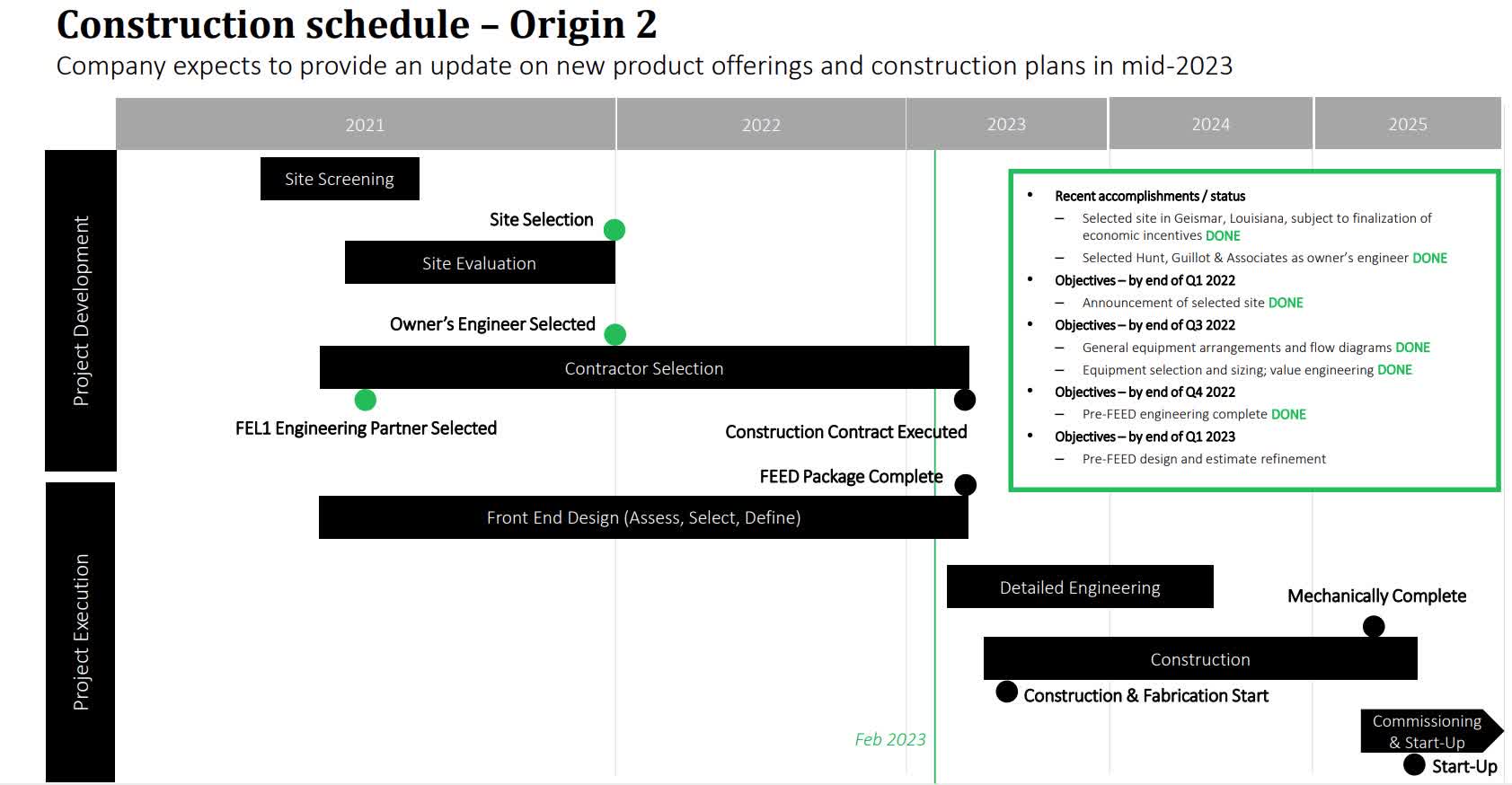

Origin 2's progress on track

For those who are unfamiliar with Origin 2, this is Origin Materials large scale manufacturing facility, located in Geismar, Louisiana. This plant in Louisiana is expected to convert about one million dry metric tons of wood residues every year and based on what was last disclosed, the plant is expected to cost about $1.1 billion. Lastly, the plant is expected to be operational in the middle of 2025.

Management reaffirmed progress on Origin 2's front end design, financing and construction planning remains on track.

Origin Materials announced that the Louisiana State Bond Commission approved the issuance of up to $1.5 billion of tax-exempt bonds, which will be used for the financing of Origin 2's construction.

{kind=link}

Origin 2 construction schedule (Origin Materials IR)

Management reiterated in the recent earnings call that they expect the construction of Origin 2 can be fully funded from the cash it has on its balance sheet, traditional project financing announced previously and potential strategic partnerships.

Strategic partnership with Avantium

Origin Materials announced a partnership with Avantium ( AVTXF ) to accelerate the mass production of FDCA and PEF for use in advanced chemicals and plastics.

I think that this is a one-of-a-kind partnership given that both partners have great strengths in their respective fields. Origin Materials is able to use its own platform to generate CMF from the carbon found in sustainable wood residues while Avantium’s YXY ® Technology can convert derivatives of Origin's CMF into FDCA. FDCA is the chemical building block for PEF.

PEF has been known to be an exciting polymer for some time as a result of its strong performance characteristics like heat resistance and durable strength while at the same time offering better degradability profile and is able to be fully recycled.

As both partners have strengths in their respective fields, I think that the two parties coming together can result in attractive unit economics and improved carbon footprint.

Financials and outlook

As of the fourth quarter of 2022, Origin Materials has $324 million of cash on its balance sheet.

As elaborated earlier, management expects that the current cash on hand, on top of other available financing, is able to finance the construction of Origin 2.

Given that Origin 1 is expected to ramp up from the second quarter of 2023, management is guiding for full year revenue to be in the range of $40 million to $60 million, with an assumption of gradual ramp up in Origin 1 and revenue to be recognized from Origin 1 from the third quarter of 2023. Management expects that for the full year of 2023, Origin Materials will have an adjusted EBITDA loss of $50 million to $60 million.

Valuation

My one-year price target for Origin Materials is $10.94, representing 120% upside from current levels.

I use a discounted cash flow model to determine Origin Materials one-year price target. Origin Material expects to bring Origin 2 online in 2025, and I expect $800 million in revenues in 2026 as a result of Origin 2 ramp up. I also expect Origin Materials to be EPS positive in 2026 with an EPS of $0.30.

Based on 2026 expected revenues, Origin Materials is currently trading at 0.89x 2026 P/S.

Assuming a 2x P/S multiple on 2026 revenue and discount that by Origin Material's cost of equity, this results in my price target of $10.94, implying an upside of 120% from current levels.

Risks

Execution risks

Origin Materials is moving to the next phase of its life as a public company when it is about to ramp up production in Origin 1 while managing the construction of Origin 2. As a result, there are risks of execution slippages in either project, which could provide downside risks in my view. This ramp up in Origin 1 could provide investors with evidence about how management is able to ramp up productions in the future for Origin 2 and execution remains key.

Risk of delays

I like that management has been executing well and it has been able to meet its timeline and schedule with Origin 1 and 2 so far. However, there is a risk that management could face some delays as a result of external factors, like supply chain disruptions. As such, management needs to make sure that its operational needs and timeline continue to be met with the ramp up of Origin 1 and the construction of Origin 2.

Competition

I think that Origin Materials has a differentiated and protected technology platform. However, if it does not continue to innovate and bring better products to the table, there are many other competitors out there that are doing research and development and continuing to bring new innovation to the space.

Conclusion

I think that Origin Materials is set up for success. With its huge customer demand of $9.3 billion even before commercial production has begun, this shows investors that global companies around the world see the strong value add that Origin Materials brings to the table. Furthermore, Origin Materials is able to provide a differentiated product offering as a result of its technology platform, and this technology platform is patented and protected from competitors. I also like that the company remains well funded, with Origin 2 financing secured and the company expects to be fully financed until it turns positive EBITDA. Furthermore, I like that management has been executing well as its Origin 1 plans have gone according to plan despite a difficult operating environment and Origin 2 also looks to be progressing well.

At the end of the day, I think that Origin Materials is well positioned to take up global market share as a leading negative carbon materials player in the long-term and the current risk reward perspective remains attractive in my view.

For further details see:

Origin Materials: Emerging As A Leader In Carbon Negative Materials