OEC - Orion Engineered Carbons: Efficient FCF Allocation Creating Expansion

2023-05-09 13:36:28 ET

Summary

- Orion surpassed Q1 2023 expectations and provided solid guidance along with a share repurchase program until 2027.

- Historically, Orion has outperformed the market displaying their ability to effectively allocate FCF to foster growth.

- Orion's strategy to expand into renewable energy will increase its exposure to a high-growth segment and diversify revenues.

- According to my DCF assumptions, Orion is currently undervalued resulting in a buy rating.

Orion Engineered Carbons S.A. ( OEC ) has exemplified strong growth within its core business segments along with recent positive earnings and guidance. I believe that the stock is a buy due to its transition into key renewable inputs, their share buyback program, and Orion's relative undervaluation based on my DCF assumptions.

Business Overview

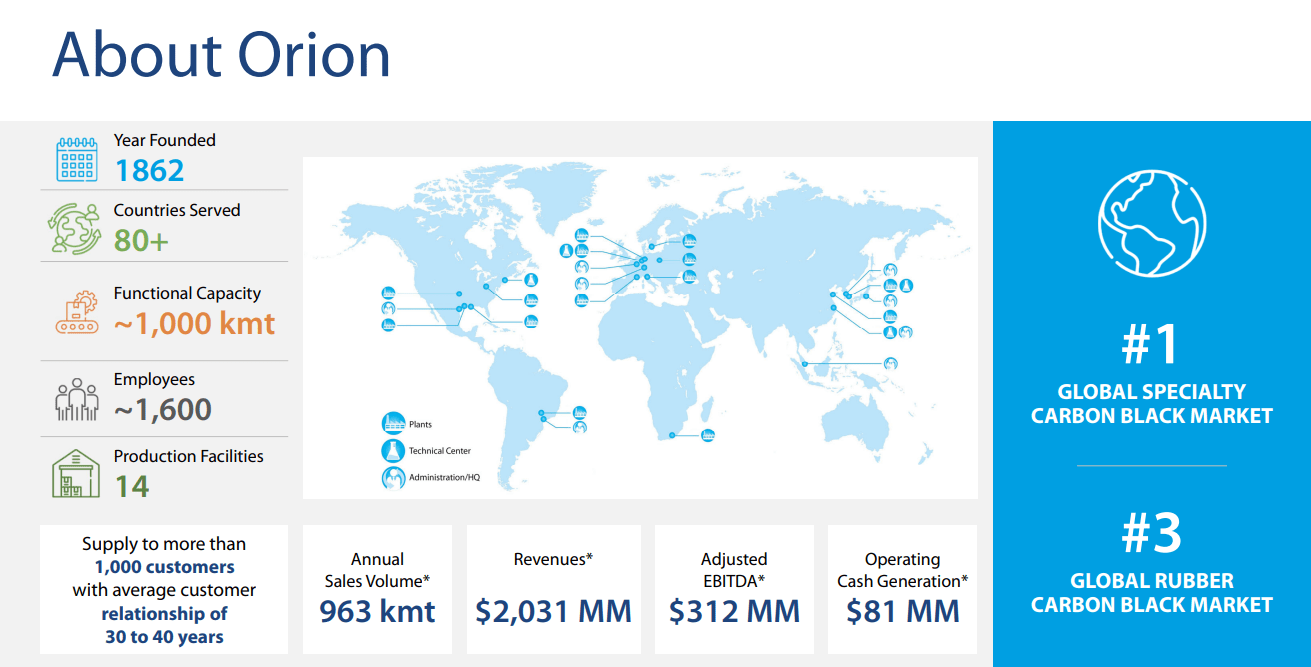

Orion Engineered Carbons S.A. and its subsidiaries are engaged in the production and global distribution of carbon black products. The company operates in two distinct segments, namely Specialty Carbon Black and Rubber Carbon Black. Its product range includes specialty carbon black grades for printing and coating applications, high-purity carbon black grades for the fiber industry, and conductive carbon black grades for polymers, coatings, and battery electrodes. Additionally, the company offers rubber carbon black products under the PUREX brand for mechanical rubber goods and under the ECORAX brand for tire applications. Orion Engineered Carbons S.A. is based in Senningerberg, Luxembourg, and has a workforce of 1600 employees.

{kind=link}

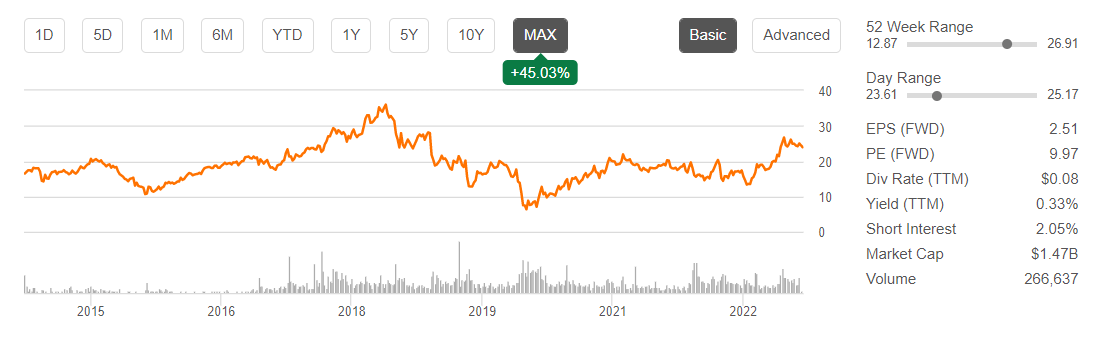

Orion Engineered Carbons' market capitalization stands at $1.472 billion, while their ROIC is at 9%. The company's stock price currently sits at $23.93, which is near its 52-week high. However, the price is potentially high due to their forward P/E being 11.8 compared to the industry median of 8.2. I believe that this premium for Orion is due to its strong and promising growth and future in the EV industry which justifies a higher price point.

Additionally, Orion Engineered Carbons pays a small dividend of 0.33% with an extremely safe payout ratio of 4.35%. This indicates that the company has ample FCF to carry out its CapEX plans, which include the expansion of new plants described in the article. I believe that if Orion is able to achieve growth in multiple avenues, maintaining a small dividend is fine as it allows Orion to use FCF to capitalize on upcoming trends such as lithium batteries used in EVs, where Orion creates an important conductive additive.

{kind=link}

Orion's first-quarter EPS surpassed expectations , exceeding estimates by 45% with a value of $0.74 compared to the anticipated $0.51. Meanwhile, the company's revenue grew by 3.3% year over year to $500.7 million. Despite facing macroeconomic challenges, the company managed to outperform expectations through its core business, achieving a record adjusted EBITDA of $101 million, up 22% from the previous year. This accomplishment in Q1 demonstrates that Orion has been able to utilize its specialty niche to accurately price its products, maintaining a strong financial standing and mitigating market declines, despite a slight drop in volume. The company also announced a 6.9 million share buyback program until June 2027 which will allow shareholders to receive long-term value and give Orion the ability to employ excess FCF during cyclical upcycles.

Looking ahead, Orion anticipates adjusted EBITDA for 2023 to be in the range of $350 million to $380 million, up 17% at the midpoint compared to 2022. Furthermore, the company expects its full-year 2023 adjusted EPS to be between $2.30 to $2.60, up 25% at the midpoint. These projections illustrate the company's ability to reposition itself for growth by achieving financial records and executing its expansion strategies effectively.

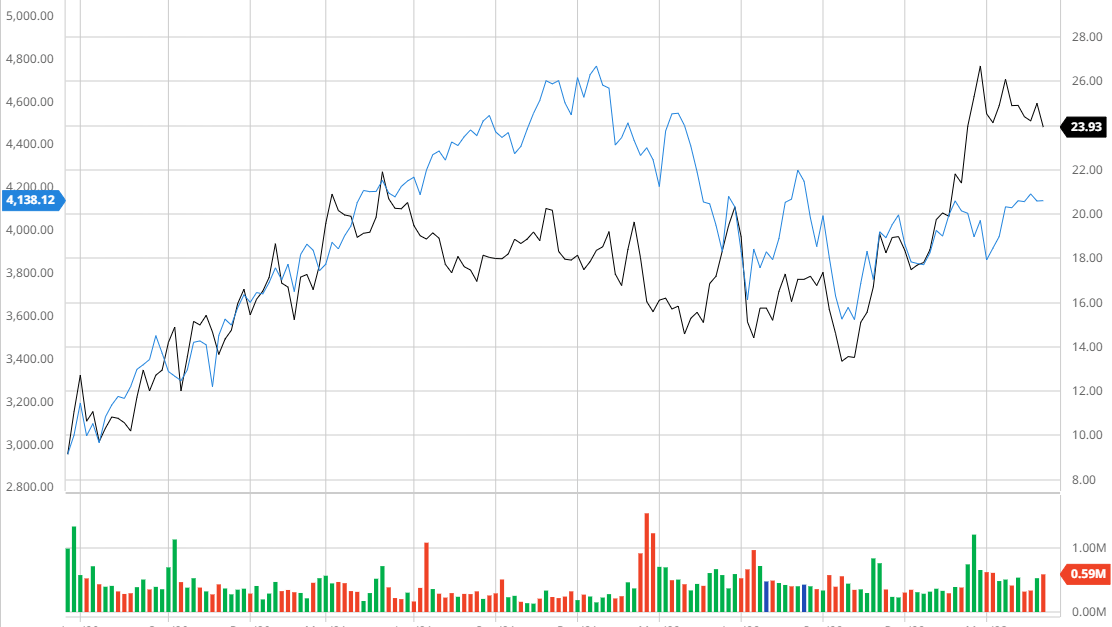

Orion's Outperforming the Broader Market

Over the past three years, Orion has consistently outperformed the S&P 500, which is a testament to its capability to expand production through strategic CapEX investments, as demonstrated by its high ROIC. In my opinion, the company's proficiency in deploying capital, combined with its robust core business model, positions it for long-term outperformance of the S&P 500, even in the face of cyclical market fluctuations. Additionally, Orion's ability to utilize its FCF to enhance shareholder value with things such as share buybacks, and grow the business further, strengthens its prospects for long-term success.

Orion Compared to S&P 500 3Y (Created by author using Bar Charts)

{kind=link}

Jumping on Long-Term Trends Using FCF to Foster Growth

Orion has demonstrated its ability to efficiently allocate capital to maintain and expand its business, evident in its continuous expansion into new segments, which positions the company favorably for the future.

An example of this is the large CapEX project announced on May 5th, 2022, wherein Orion plans to construct the only U.S. plant producing acetylene-based conductive additives, a crucial component in the value chain for lithium-ion batteries, high-voltage cables, and other products driving the global transition to electrification and renewable energy. The production process involves converting acetylene gas into a powder, which is added to lithium-ion batteries to enhance electrical conductivity and extend their lifespan, as well as high-voltage cables used in wind and solar farms.

With a commitment of $120 to $140 million of FCF, this project is critical to Orion's success, as it is expected to quadruple the company's production to an estimated 12 kilotons of volume per year. With the plant anticipated to commence operations in the latter half of 2024, Orion will be able to quickly capitalize on the investment and generate compounding growth into the future.

I believe that this new addition to Orion's business will enable the company to diversify its revenue streams while positioning itself within a high-growth industry that shows no signs of slowing down. Diversification in revenue segments, coupled with high growth, will create a seamless transition to a more stable business model, reducing cyclicality within the company's core revenues.

Houston Business Journal

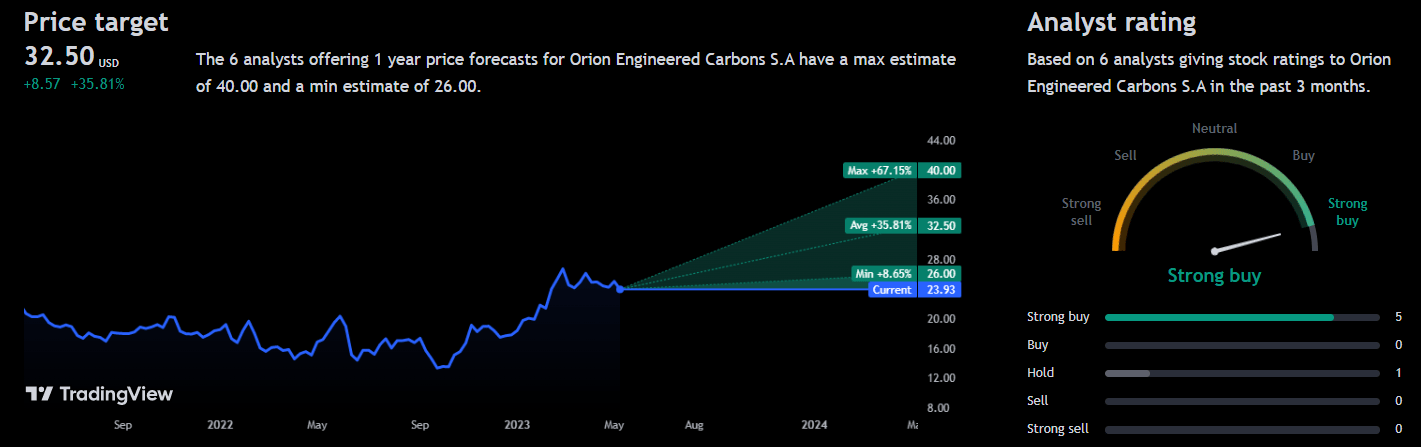

Analyst Consensus

Orion is rated as a "strong buy" by analysts, who have a favorable outlook on the company's growth prospects through the strategic allocation of its FCF. This positive sentiment is reflected in the average analyst's 1-year price target of $32.50, which represents a potential upside of 35.81%.

{kind=link}

Valuation

Before determining the fair value of Orion, it is essential to calculate the Cost of Equity and WACC using the Capital Asset Pricing Model. By factoring in a risk-free rate of 3.44%, I was able to calculate the Cost of Equity for Orion to be 7.97%.

Created by author using Alpha Spread

Using this value, I calculated the WACC for Orion to be 6.49%, which is below the industry average of 9.89%.

Created by author using Alpha Spread

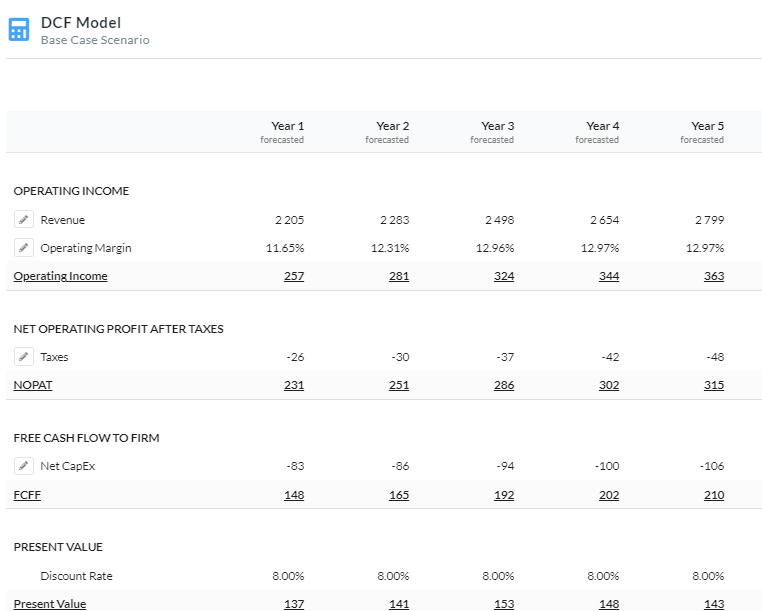

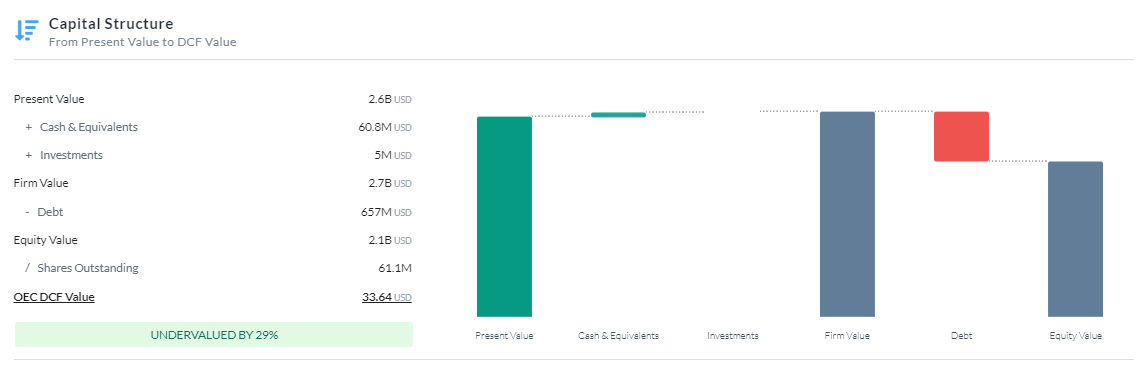

To determine the fair value of Orion, I employed a Firm Model DCF analysis using Free Cash Flow to Firm. After considering various factors such as the company's past performance, industry trends, and expected growth rate, I arrived at a fair value estimate of $33.64, which indicates that the company is currently undervalued by 29%. To arrive at this estimate, I utilized a discount rate of 8% for a 10-year duration and added a 1.51% risk premium to account for macroeconomic headwinds and the risk of a cyclical downturn. Furthermore, I predicted that Orion would continue expanding its operations and utilize their specialty in a high-demand industry to slightly expand margins over the years.

DCF Assumptions Year 1-5 (Created by author using Alpha Spread) DCF Assumptions Year 6-10 (Created by author using Alpha Spread) Capital Structure (Created by author using Alpha Spread)

{kind=link}

{kind=link}

Risks

Cyclical Shifts: The fluctuation of Carbon Black prices can lead to underperformance and result in a decrease in profits and pricing power. Such a scenario can create challenges for the company's FCF, limiting its ability to complete expansion projects or embark on new ones in a timely manner.

Macroeconomic Headwinds: Orion's business and financial performance may be adversely affected by the unpredictability of the global economy, which includes economic downturns, recessions, and currency fluctuations. This unpredictability may constrain the company's ability to enhance its core business segments or venture into new growth areas due to potential constraints in free cash flow.

Conclusion

To summarize, I rate Orion Engineered Carbons a buy due to their ability to effectively employ capital and use FCF to expand, and create shareholder value through repurchases, and because of their relative undervaluation, when considering my DCF assumptions.

For further details see:

Orion Engineered Carbons: Efficient FCF Allocation Creating Expansion