ORN - Orion Group Holdings: Top Construction Stock To Consider In 2024

2024-01-02 23:28:35 ET

Summary

- Orion Group Holdings has achieved a quarterly gross profit of $19.1 million, a 42.5% increase YoY.

- The company is focusing on improving profitability and has a high backlog of $920 million, exceeding its FY 2022 revenue.

- Orion Group is divesting its Central Texas business and focusing on Dallas and Houston, which offer higher revenue potential.

Construction company Orion Group Holdings ( ORN ) grew its quarterly gross profit to a $19.1 million representing an increase of 42.5% (YoY) from $13.4 million realized in Q3 2022. The company’s share price has surged 110.21% (YoY) indicating a positive turnaround into 2024 boosted by lower cost of revenues and operational expenses.

Thesis

Orion's focus on improving its profitability has seen it solidify its concrete business not just based on an adjusted EBITDA but also on quality revenue and higher operating income. The company has lined up various marine projects that will accelerate its overall momentum having won building/ design contracts for high-end businesses into 2024. I am particularly excited with the high backlog that stood at $920 million (as of Q3 2023) greater than the company's annual revenue of $748.3 million in 2022.

Business Value Proposition

Orion’s concrete business has been steadily increasing since Q1 2023 and it recorded sales at $50.8 million by Q3 2023 against the overall gross profit of $19.1 million. The gross margin in the sector grew by 390 basis points enhanced by low equipment costs and other operational efficiencies, especially in its dredging business that incurred low labor utilization cost. In its Q3 2023 financial call, Orion explained that it was exiting its Central Texas business and focusing on Dallas and Houston where it stated it would collect higher revenue quality.

First Dallas and Houston are what I would term, "hot spots" for both diverse business centers and efforts of energy transition respectively. For instance, a report shows that over the years Houston has registered more than “60 new low-carbon, climate startups and an innovation ecosystem for energy transition investments.” Further, it is not only the 4 th biggest US city but also houses at least “26 of the Fortune 500 companies.” On its part, Dallas has a great growth potential providing a home to more than 65,000 businesses including international and small businesses offering multiple employment prospects.

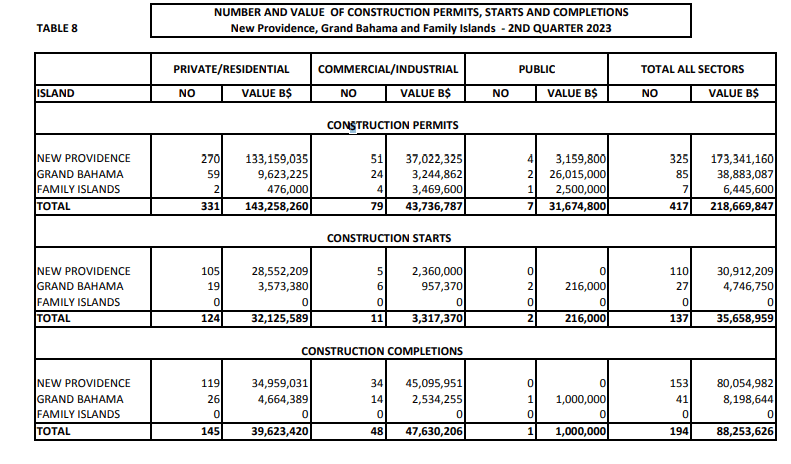

The company also announced entry into the Bahamas, where it was awarded a design-build turnkey contract for the “Grand Bahamas Shipyard Dry Dock Replacement project” valued at $100 million. The project’s conclusion is scheduled for Q4 2025 and will be done in conjunction with subcontractors from the Bahamas. One important aspect of the Bahamas is that the business environment in Q2 and Q3 of 2023, favored commercial and public developments as opposed to private spaces while permit values/ numbers continued to increase. Other than the Grand Bahamas, there are also the New Providence and Family Islands, which will also provide important businesses to Orion (as seen in the construction statistics below).

{kind=link}

Bahamas government construction statistics

There was a 100% (YoY) increase in the number of projects completed within the commercial/ industrial space in the Bahamas against a 7.54% (YoY) decrease in the number of private/ housing projects between Q2 2023 and Q2 2023. In turn, the value of public projects in the same period grew by 2,172.73% (YoY).

Market-level competency

Orion Group also announced a recent $121 million contract award in both the concrete and marine space, indicating its increasing skill & competency giving it a competitive edge in the market. Up to Q3 2023, Orion’s total backlog and projects contracts were valued at $920 million which is not only 5 times more than the company’s market capitalization (of about $160.5 million) but also $200 million plus more than the FY 2022 revenue of $748.3 million.

Of special interest is the recent mention of an oncoming dredging contract from the Army Corps of Engineering. The projects associated with this government agency are mostly on water infrastructure, including dams and levees (mostly in the civil works segment). In 2022, the Army Corps was allowed (through the Water Resource Development Act of 2022) the use of transaction agreements, that would allow the agency to use contracts for these projects in the absence of “procurement/ cooperative agreements of grants.”

Under such a transaction agreement, Orion will have the chance to offer its expertise on various concrete mixes helping the Army Corp with its environmental protection initiative. I view this strategy as an opportunity for Orion to explore new areas of collaboration to raise its revenue and expand its area of operation. With $50.8 million in bid wins in the quarter and Q3 2023 revenue at $169 million against a diluted share of $0.02, Orion is on the path to increasing its profitability into 2024.

Risk to the Business

Low cash availability

Orion’s cash stands at $3.9 million representing a 56.18% (QoQ) decline from $8.9 million recorded in Q2 2023. However, this cash balance shows a 44.4% (YoY) increase from $2.7 million realized in Q3 2022. S till, this cash is lower than the total debt balance that sits at $125.3 million, a 22.24% (QoQ) increase from $102.5 million recorded in Q2 2023. As seen, Orion's main form of financing has been debt that has eroded into the company's cash account.

Future opportunities to consider

In my view, Orion Group is a very attractive stock, considering it is trading under $5 with contracts and a solid backlog of almost $1 billion into 2024. Safe to say, it may be a target of major construction plays considering its renewed focus on the concrete market. Market leader Granite Construction Incorporated ( GVA ) recently completed the acquisition of Coast Mountain Resources for just $26.93 million without any material effect on its balance sheet. An acquisition of Orion Group (in my perspective) by GVA would push the stock to at least $7. GVA's revenue in the 3 months ending on September 30, 2023, stood at $1.117 billion. Of this amount, about $945 million was attributed to construction while materials took up $171.1 million. Acquiring Orion would bring on board, the marine segment thereby expanding the GVA revenue base.

Valuation

Orion’s forward enterprise value ((EV)) to sales stands at 0.40 against the industry average of 1.82 (representing a difference of -78.03%). Additionally, ORN’s forward price-to-sales ratio is 0.23 against the sector average of 1.45 (indicating a difference of -84.25%). These metrics show that ORN is highly undervalued with an upside potential above 75% into 2024.

Bottom Line

Despite the low cash-to-debt balance, Orion Group is a buy considering its growing revenue and contractual obligation within and without the US. The company's backlog is about $920 million into 2024, higher than its FY 2022 revenue. I have also considered the acquisition aspect of this stock with the valuation showing it has an upside potential of at least 75%.

For further details see:

Orion Group Holdings: Top Construction Stock To Consider In 2024